RTX - SP500: Market Outlook For 2024 - Pump And Dump

2023-12-20 16:25:39 ET

Summary

- The S&P 500 Index is likely to rise to 5300 in 2024 due to P/E multiple expansion to around 22, and expected earnings around $240.

- However, there could be significant volatility as the baseline scenario of disinflation and expected Fed cuts is questioned.

- The disinflationary process is likely to end in June, at which point the baseline scenario will have to be reevaluated.

- The probability of a summer "slump" is high if inflation remains sticky and growth slows more than expected.

The baseline

The market prediction for the end of 2024 is really a gameplan - or the strategy for how to play the stock market over the next 12 months. The starting point is recognizing what the baseline scenario is, according to consensus market expectations.

Currently, the consensus market expectations are that: 1) the disinflationary process will continue, 2) which will allow the Fed to reverse some of the recent interest rate hikes, 3) which is going to significantly reduce the probability of a recession as the yield curve steepens and overall interest rate decrease, and 4) also reduce the probability of a credit crunch in the area of commercial real estate and regional banking as the wave of refinancing meets lower interest rates. In addition, the government budget deficit will likely become more sustainable, as the interest payments decrease with the lower interest rates.

Thus, primarily due to the expected Fed cuts in 2024 and 2025, the S&P 500 Index (SP500) earnings are likely to continue to grow, as the recession is avoided. Yes, the S&P 500 is already overvalued with the forward P/E ratio at 20, but the expected monetary policy easing will support the P/E multiple expansion. Thus, the gains for S&P 500 in 2024 will likely come from the P/E multiple expansion by around 10% from 20 to about 22, which would push the SP500 from 4800 (where I expect to close by the end of 2023) to around 5300 sometimes during 2024. So, this is my S&P 500 target for 2024: 5300.

As a result, my strategy is to play S&P 500 tactically from the long side in 2024 - meaning buy the dips, and keep some long exposure constant. This will be my strategy until the baseline scenario changes. The risk to the baseline scenario is that 1) the disinflationary process slows or ends prematurely, which forces the Fed to revert back to the "higher for longer," 2) the lagged effects of the prior interest rate hikes do cause a recession, which causes earnings revision, 3) any other currently unanticipated and unpredictable event, and there are many, for example geopolitical, U.S. election risks, and the government shutdown.

So, let's analyze in more detail the baseline scenario.

Inflation

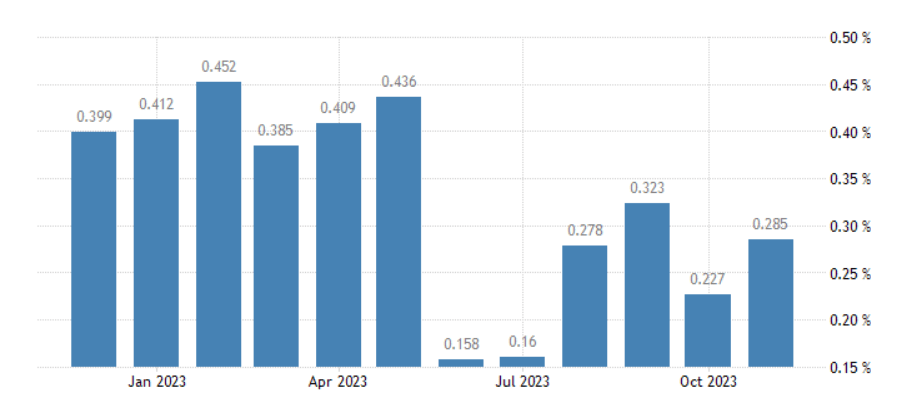

The disinflationary process is likely to continue until June 2024, based on monthly inflation numbers. Specifically, as the chart below shows, core CPI was running at above 0.4% month over month until May 2023, and then it sharply dropped below 0.2% in June and July.

{kind=link}

Core CPI has been running at around 0.3%, or slightly below, over the last 4 months, and if this pace continues, the annual core CPI will fall to 3.3% by June from the current level of 4%. If the monthly core CPI slows to 0.2%, the annual core CPI could fall to 2.8% by June.

What happens to inflation after June 2024? The disinflationary process could end. After the 2023 monthly core CPI readings of 0.4% are replaced by 0.2% or 0.3% readings, the disinflationary process will end, unless core CPI starts rising at 0.15% after June, which will be a difficult task. In fact, the much anticipated "last mile" effort to bring inflation to the 2% target will likely start in June. My hunch is that it will be difficult to get the monthly core CPI down to 0.15% without a recession.

The disinflationary process is also predictable over the next 6 months, given the importance of shelter in core CPI calculations. Specifically, when you look at the rents, the annual inflation is still above 6%. But the CPI calculation of rent inflation is lagging the real-time rents by about 6 months, and we know that the new tenant rents are falling sharply and are already down to 2% - and this is indication of the real-time rent inflation. Thus, it is predictable that the rent inflation will be falling, thus, the shelter inflation will be falling - and this will support the disinflationary process over the next 6 months.

The Fed

Given the disinflationary process, the market expects the Fed to cut aggressively in 2024 to 3.9%, and down to 3.25% in 2025. This is not much different from the Fed's dot plot, as the Fed sees the Federal Funds rate at 3.6% in 2025. However, the market expects that these cuts will be frontloaded to 2024, which makes sense due to the expected disinflationary process in the first half of 2024.

| Theme |

| Near Term |

| First cut |

| Dec 2024 |

| Terminal |

| Soft landing |

| Pause 5.33% |

| March 24 70% prob. |

| 3.9% Fed: 4.6% |

| 3.25% by Oct 25 Fed 2025: 3.6% |

The earnings

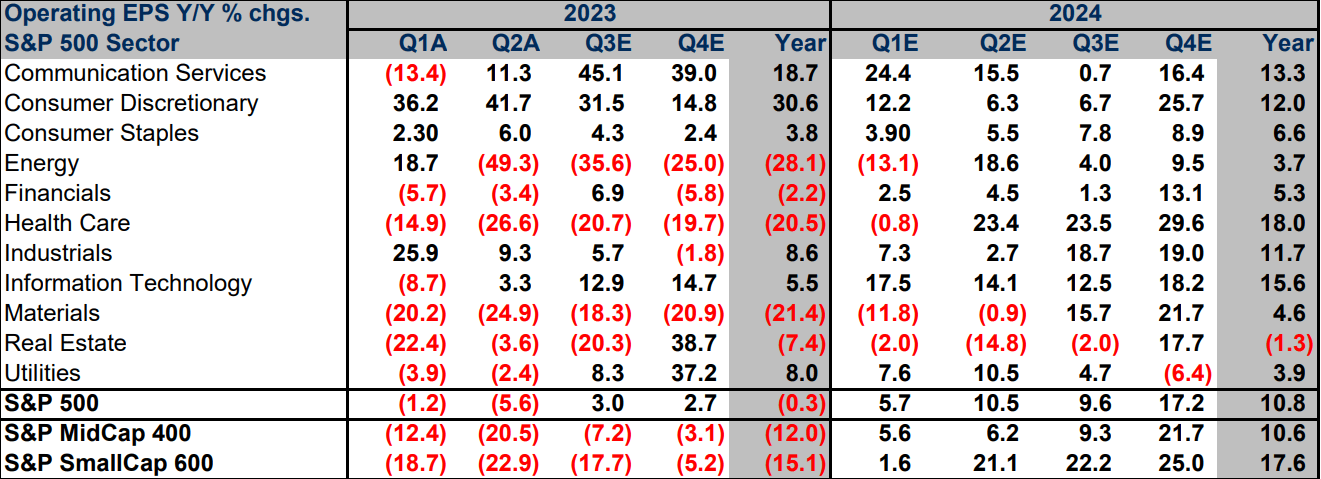

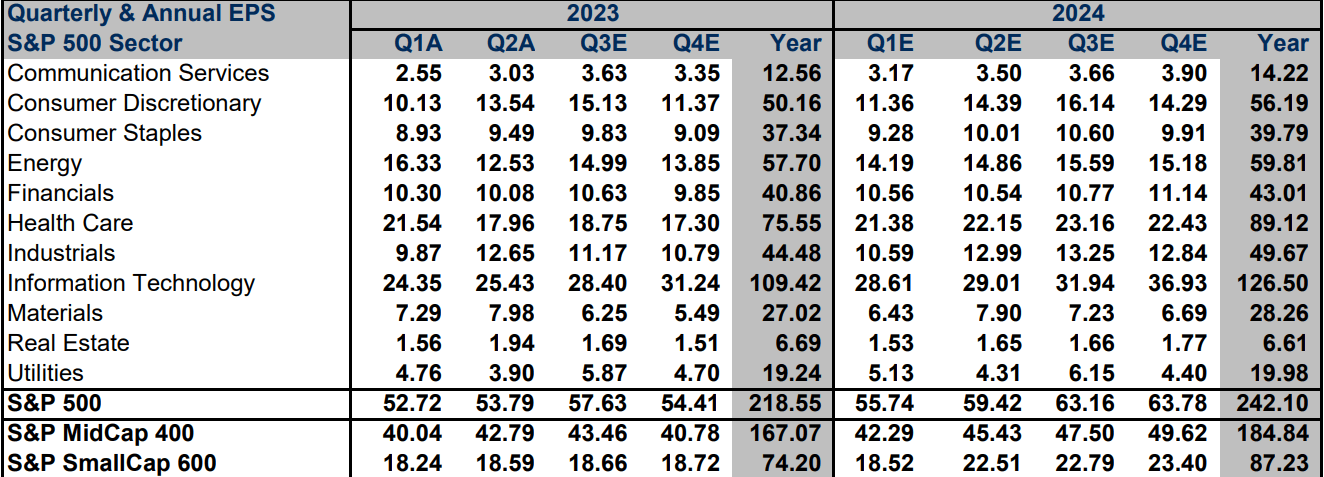

The bottom-up analysts currently expect 10.9% growth in SPDR® S&P 500 ETF Trust ( SPY ) earnings for 2024. Other than non-cyclical Healthcare sector ( XLV ), the earnings growth is expected to come from the magnificent 7 stocks in Technology ( XLK ), Communications ( XLC ) and Discretionary ( XLY ) sectors.

{kind=link}

Overall, the analysts estimate the S&P 500 earnings at $242 for 2024, but almost a quarter of those earnings come from the Technology sector, and over 35% of total S&P 500 earnings come from the sectors dominated by the magnificent 7 - Technology ( AAPL , MSFT , NVDA ), Discretionary ( AMZN , TSLA ), and Communications ( GOOG , META ). Thus, the AI theme will continue to be important in 2024, and whether the AI leaders will be able to monetize the GenAI technology will significantly affect the S&P 500 earnings.

{kind=link}

Overall, due to expectations of no recession, I assume that the analysts' earnings estimate of $242 will hold for 2024 - although, the S&P 500 will soon start reflecting the 2025 earnings estimates.

Valuation

The S&P 500 is currently trading at just below 20 forward P/E ratio - which is expressive based on historical averages. However, the P/E valuation is skewed by the expensive magnificent 7, and we see that P/E ratio for Technology sector is near 27 and for Discretionary at 25. These sectors are overvalued, but as we also see, earnings growth also comes from these sectors, so it makes sense to see some additional valuation premium in these sectors. Overall, everything outside Energy ( XLE ) and Financials ( XLF ) is moderately expensive.

CFRA

However, given that the Fed is expected to aggressively cut interest rates, due to disinflation, I expect that P/E multiple could expand by around 10% to 22. Thus, given the earnings projections of $242 and P/E ratio of 22, the target level for the S&P 500 is 5324, so let's round down to exactly 5300 level as the 2024 target.

Implications

The S&P 500 level of 5300 is just a target, which is valid for as long as the baseline scenario is valid. Yes, the S&P 500 could finish the year around 10% higher from today, which is nothing extraordinary.

However, I expect significant volatility, as the baseline scenario is questioned. First, I expect that S&P 500 will outperform during the first half of 2024 during the disinflationary process and as the Fed starts cutting. Thus, it is likely that the 5300 target could be reached by June.

The S&P500 target at 5300 will be modified as the baseline scenario changes, but it's likely going to hold until June. What happens after June? We could see a trading range until the November election, if the baseline still holds.

However, the disinflationary process will likely end in June, and if inflation proves sticky afterwards, we could see a sharp correction as the market starts questioning the Fed's ability to continue cutting interest rates.

Also, the lagged effects of the prior interest rate hikes will start to hit the economy, and it is likely by June we could see a mild recession, especially if the Fed does not cut in March.

Thus, we could see a mild recession or a very low growth with sticky inflation next summer - that's stagflation. In this scenario, the market could crash possibly by 20% or more, as earnings would be revised lower, and the Fed's inability to cut more aggressively would cause a multiple contraction.

Overall, 2024 could be a boom-to-bust year like 2008, but this is not a baseline scenario at this point. At this point, I see a 10% gain to 5300 level in 2024, and we are currently in a "pump" stage. However, I am aware of the possibility that there could be a "dump" stage starting in June as the disinflationary process possibly ends. Will adjust my targets accordingly.

Editor's Note : This article was submitted as part of Seeking Alpha's 2024 Market Prediction competition , which runs through December 20. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

SP500: Market Outlook For 2024 - Pump And Dump