CA - Spartan Delta: A Natural Gas Cash Cow With A Special Dividend

Summary

- Spartan Delta is a relatively new natural gas producer in Canada.

- The company was created in 2020 when an experienced management acquired an asset out of bankruptcy.

- More assets were acquired, and Spartan is now one of the most respected players in Western Canada.

- The cash flows were exceptionally strong this year thanks to the high natural gas price.

- This results in a lower than expected net debt position, and paved the way to declare a special dividend of C$0.50.

Introduction

I have been following Spartan Delta ( SDE:CA ) ( OTCPK:DALXF ) ever since the company was created in 2020. The experienced management acquired a natural gas asset from Bellatrix Exploration out of bankruptcy and has been aggressively rolling up additional natural gas and oil producing assets . Back in June 2020, when the stock was trading at C$3.20, I called Spartan Delta a ‘once in a decade opportunity’ . The stock is now trading more than 4 times higher and has announced a first-ever special dividend of C$0.50, which represents in excess of 15% of the C$3.20 share price when I first discussed the company.

The Q3 results were very strong despite hedging losses

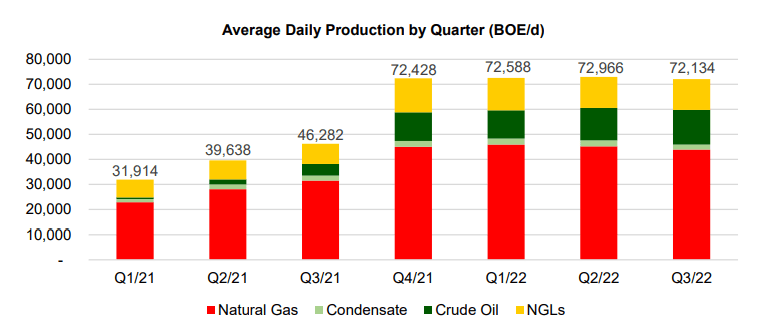

During the third quarter, Spartan Delta produced an average of 72,100 barrels of oil-equivalent, which is pretty much in line with the previous few quarters. Approximately 60% of the total oil-equivalent production consists of natural gas , as you can see below.

{kind=link}

The average natural gas price during the quarter was approximately US$8.20 for the Henry Hub selling point, C$5.50 for the AECO 7A and C$3.95 for the AECO 5A. Thanks to the different areas the natural gas is being marketed, the average natural gas price was C$5.04 while the average realized price was just C$4.12 as Spartan Delta is still dealing with some hedges. Going forward, these hedges should have a relatively lower impact.

{kind=link}

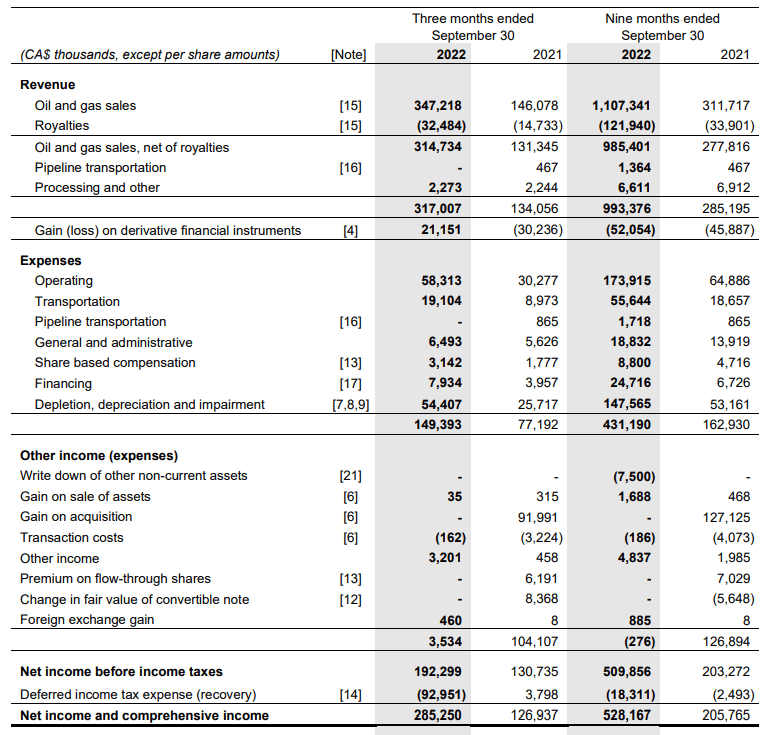

Spartan Delta reported a total revenue of C$317M net of royalties and recorded a $21.2M hedge gain. Unfortunately, as you can see below, this included about C$17M in realized losses and about C$38M in unrealized gains (and this will have an impact on the cash flow result of the company, I will explain this later).

{kind=link}

The operating costs remain pretty low, as you can see below. In excess of a third of the operating expenses are related to the depreciation and depletion expenses. This resulted in a pre-tax income of C$192M and thanks to a non-recurring tax benefit of almost C$93M, the reported net income was C$285M or C$1.84 per share.

{kind=link}

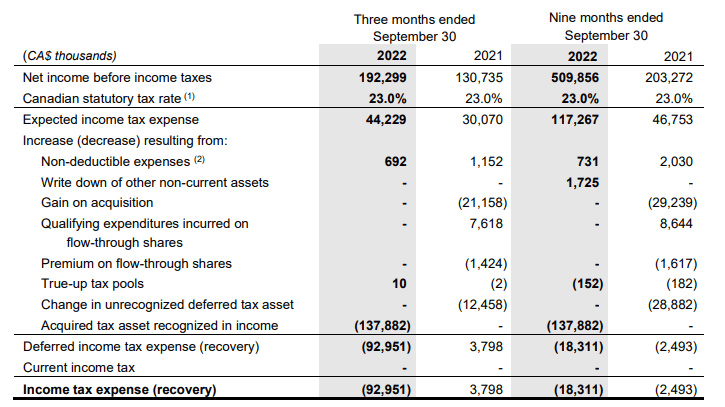

That tax benefit obviously is a non-recurring item and the breakdown below shows there was a tax asset included in one of the recent acquisitions. On an underlying basis, the normalized tax cost would have been just over C$44M but the C$138M tax benefit mitigated this resulting in a net tax benefit of C$93M.

{kind=link}

So excluding this non-recurring benefit, the underlying net profit would have been C$192M – C$44M = C$148M or C$0.95 based on the current share count of 155.5M shares outstanding.

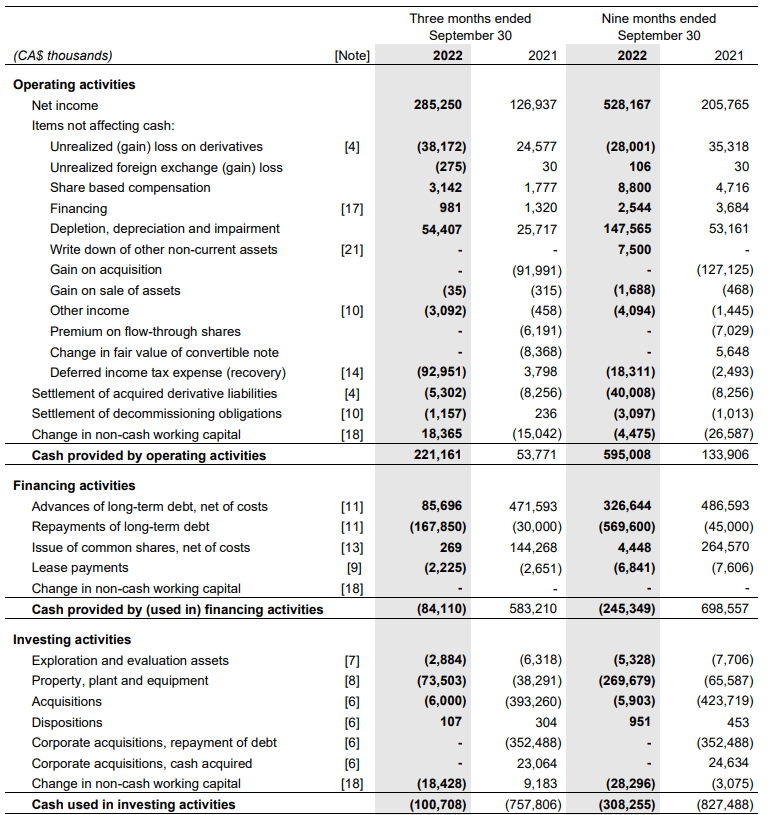

Looking at the cash flow, we obviously see the C$93M in net tax benefit being deducted again as this is a non-cash gain. We should also deduct the C$18M in working capital changes from the C$221M operating cash flow. This results in an adjusted operating cash flow of C$201M after also deducting the C$2M in lease expenses.

{kind=link}

Keep in mind this adjusted operating cash flow excludes the C$38M in unrealized gains on the hedge book but includes the C$17M in realized losses during the quarter. The total capex was just C$76M which means that despite the realized hedge losses, the adjusted free cash flow was still C$125M during the quarter. That’s C$0.80 per share. And the company should be able to increase its production rate at the current spending rate of approximately C$300M per year. That being said, Spartan will likely spend C$420M as per its FY 2022 guidance and that should result in a good set-up for next year with a higher average production rate.

The debt is going down fast, and this paves the way for a special dividend

This also means Spartan Delta won’t generate a lot of free cash flow in Q4 as the capex spending will increase to approximately C$150M. But that’s fine as the strong natural gas prices have helped the company to reduce its net debt faster than I had expected.

As of the end of September, Spartan had C$43M in cash and just C$144M in long-term debt resulting in a net debt position of just over C$100M. That’s much better than I expected and also much better than Spartan Delta expected.

That’s why the company announced a special dividend ofC$0.50 per share. This will only cost Spartan Delta C$78M (which means the net debt will likely increase in Q4 due to the above-average capex bill and this special dividend) although SDE is playing it smart. Although the stock will trade ex-dividend in December, the dividend is only payable in January which actually means the year-end balance sheet will likely show a net debt position of less than C$100M before the dividend-related cash outflow is recorded in FY 2023.

In any case, I am very happy with the special dividend as it represents a yield of in excess of 15% based on the C$3.20 share price when I called Spartan Delta a once in a decade opportunity. But even at the current share price the dividend represents approximately 4% at a payout ratio of less than 20% based on the annualized Q3 results.

Investment thesis

Spartan Delta promised to publish a return of capital strategy when it releases its 2023 guidance . As the company is generating enormous amounts of free cash flow, even at a realized natural gas price of just C$4, I expect to see an interesting dividend policy. Even applying a payout ratio of just 25% would result in a dividend of approximately C$0.80 per share based on C$4 natural gas.

I acquired my long position in Spartan Delta about 2.5 years ago and I am a very happy shareholder. Although I’m up over 400% on the position, I’m not selling any shares right now as the incoming dividend will reduce the total amount ‘at risk’.

For further details see:

Spartan Delta: A Natural Gas Cash Cow With A Special Dividend