CA - Spartan Delta: FCF Positive In Current Gas Price Environment Provides Excellent Torque

2023-12-04 10:30:00 ET

Summary

- Spartan Delta's Q3 results were impacted by weak natural gas prices, but the company still reported a net profit of C$9M.

- The company announced an acquisition and provided guidance for 2024, projecting production growth and positive free cash flow.

- Despite the current natural gas price, I maintain a long position in Spartan Delta and plan to add to it.

Introduction

I have been following Spartan Delta (SDE:CA) (DALXF) since the company came out the gates and I have already six-folded my investment thanks to the special dividend, the capital repayment, and spinning off Logan Energy (LGN:CA) (LOECF). I still own my original position in Spartan Delta and have been considering adding to this position, although the weak natural gas price in Canada indicates there is no real urgency to add to the position. The company recently announced an acquisition and guidance for 2024, and I felt this is a good moment to have another look at Spartan Delta to see if this is the right time to add to my position.

A look at the Q3 results

Just to be clear, I had very limited expectations for the third quarter of the year. The natural gas price was weak , so it was impossible to expect a good financial performance of Spartan Delta as the focus was likely on ‘limiting the damage’.

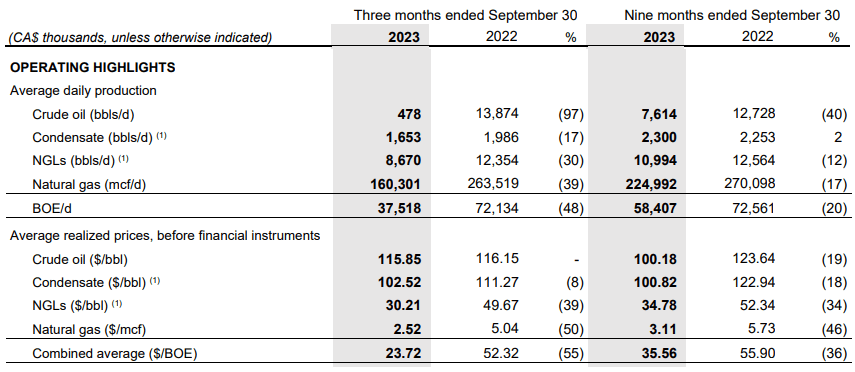

During the third quarter, the company produced an average of 37,518 barrels of oil-equivalent per day, and as you can see below, the vast majority obviously consisted of natural gas. The average realized price per barrel of oil-equivalent came in at just C$23.72, mainly due to the low price for the natural gas, as Spartan reported a realized price of just C$2.52 per mcf for the quarter (before hedges).

{kind=link}

The oil price was strong but that obviously wasn’t enough to compensate for the weak natural gas price as oil and condensate represented less than 6% of the oil-equivalent production rate.

The company reported a total revenue of C$82M and a net revenue of C$73M after adding the processing revenue and deducting the C$10.4M in royalty payments. Additionally, Spartan Delta recorded a C$2.8M gain on derivatives. This consisted of a C$33.9M realized gain and a C$31.1M unrealized loss.

{kind=link}

The total production costs remain low, and this definitely helped the company to report a pre-tax income of C$11.9M despite recording a C$4.9M loss on the sale of assets. As you can see below, the bottom line shows a net profit of C$9M, which works out to C$0.05 per share.

{kind=link}

In all my previous articles on Spartan Delta, I focused on the company’s cash flow profile. Spartan Delta generated a positive operating cash flow of C$63.2M and even after deducting the C$2.4M in lease payments and adding back the C$3.1M in working capital changes, the adjusted operating cash flow was approximately C$64M.

{kind=link}

Keep in mind, this still includes the C$33M in realized hedging gains. Those hedging gains were entirely related to the natural gas price and whereas the market price was approximately C$2.52 per mcf, but thanks to the hedging gains, the effectively realized price was C$4.63 per mcf. Those hedging gains definitely helped the company to cover the C$27.5M in capex which means the adjusted free cash flow was C$36.5M during Q3 and if you would exclude the hedging gains, the adjusted free cash flow result would have been just C$3.5M.

Definitely not great, but keep in mind the total capex guidance for H2 is C$47M, which means the Q4 capex will only be C$20M and the average quarterly capex would be approximately C$23.5M.

A small acquisition, and a preliminary outlook for 2024

Spartan Delta is re-establishing itself as a smaller company after completing the company-changing transaction earlier this year. This doesn’t mean the company is in a ‘no growth’ mode, and this was confirmed last week when Spartan Delta confirmed it acquired Duvernay assets for a total consideration of C$25M.

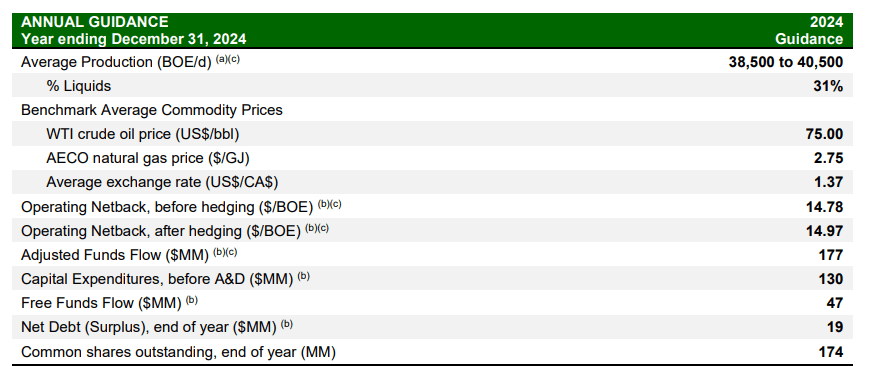

But more importantly, the company also announced its first guidance for 2024 in the same update. The company is guiding for production growth to 38,500-40,500 boe/day in 2024 (and the mid-point of this guidance indicates mid-single-digit production rate growth in 2024 and using a WTI price of US$75/barrel and an AECO natural gas price of C$2.75 (the current spot price is lower, but hopefully we will see a few months with a higher natural gas price which could also help Spartan Delta to lock in additional hedges), the funds flow is expected to come in at C$177M.

{kind=link}

The company is also budgeting a C$130M capex program. This isn’t just sustaining capex, but likely includes a substantial portion of expansion capex given the production growth projections. And based on the C$2.75 natural gas price, the company should generate C$47M in free cash flow, which works out to C$0.27 per share. For every C$0.25 change in the natural gas price, the free cash flow will fluctuate by C$15M per year, which means the ‘break-even’ point with zero free cash flow is around the C$2 mark.

This also means the company provides plenty of leverage going in the other direction. An average natural gas price of C$3.25 would result in a free cash flow of C$77M, or C$0.44 per share.

Investment thesis

While Spartan Delta definitely isn’t very exciting at the current natural gas price, I am most definitely keeping my long position unchanged and may add to this position as I continue to consider the company an excellent vehicle to gain exposure to the Canadian natural gas price. I also like Tourmaline Oil (TOU:CA) (TRMLF) (and I explained my reasons for owning Tourmaline in this article ), but Spartan Delta should provide more torque.

I have a long position in Spartan Delta, and I will likely add to this position.

For further details see:

Spartan Delta: FCF Positive In Current Gas Price Environment, Provides Excellent Torque