JBLU - Spirit Airlines And JetBlue Deal: No Soft Landings Here

2023-12-18 12:50:35 ET

Summary

- Spirit Airlines - JetBlue Airways merger is facing legal challenges from the U.S. Department of Justice, with a court decision expected in January.

- SAVE stock price has been volatile, trading as high as $20+ and as low as slightly below $9.

- The court is likely to rule in favor of the merger, offering a potential upside of 98.24%, but downside risks remain due to poor performance and liabilities.

Back in March 7, 2023 I wrote about the Spirit Airlines, Inc. ( SAVE ) and JetBlue Airways Corporation (JBLU) deal . At the time, my position was that: 1) a likely deal failure was priced in; 2) there wasn't much downside if the deal failed; and 3) there was a lot of upside if the deal succeeded from the $16.52 stock price.

Basically, everything has gone badly since that time. The merging parties have been taken to court by the DOJ, no settlement seems possible, and we're waiting for a decision from the judge (expected in January) on whether the merger can go through.

Meanwhile, the industry and the company have performed poorly since the merger announcement. The stock price has traded as high as $20+ and slightly below $9. It is currently $15.36, although shareholders have received around $1.20 in ticking fees and a $2.50 special dividend.

I've been reluctant to write about this situation because so much hinges on the court case. Others like podcaster Andrew Walker and people like Lionel Hutz of Valorem Legal Research have much better insight into mergers that are highly contested in the courts. Sometimes, I like these situations, as in the Elon Musk/Twitter saga or the Tiffany's acquisition by LVMH (LVMHF). As a general rule, however, I prefer much sleepier mergers with better risk/rewards. Having said all that, I've been asked a lot to chime in, so here goes.

I believe the court is most likely to rule that the merger can go ahead. From here out, Spirit holders receive $30.45 in value, although this can come in the shape of a merger payment (if and when it closes) or partly in the form of monthly ticking fees of $0.10. However you slice or dice it, the upside is an amazing 98.24%.

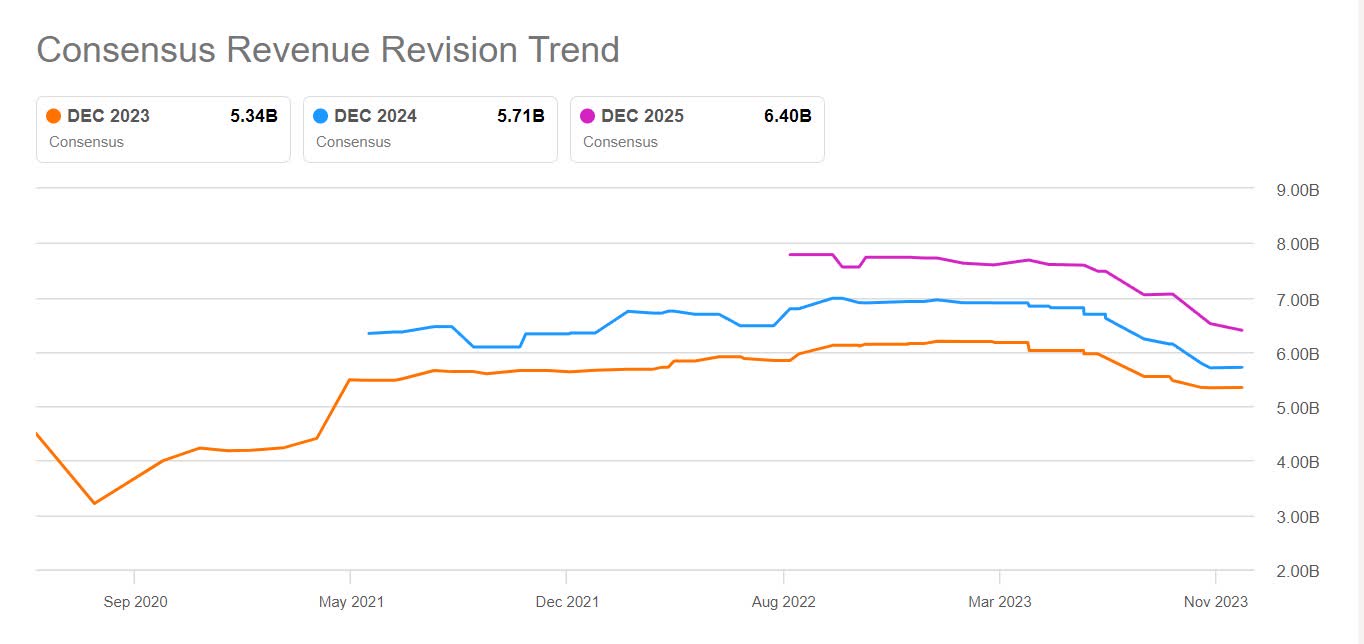

However, where things have changed the most, since my ancient initial write-up, is on the downside. Performance has not been good. I've pulled up the analyst revisions from Seeking Alpha to illustrate this:

revenue estimate revisions (Seekingalpha.com)

{kind=link}

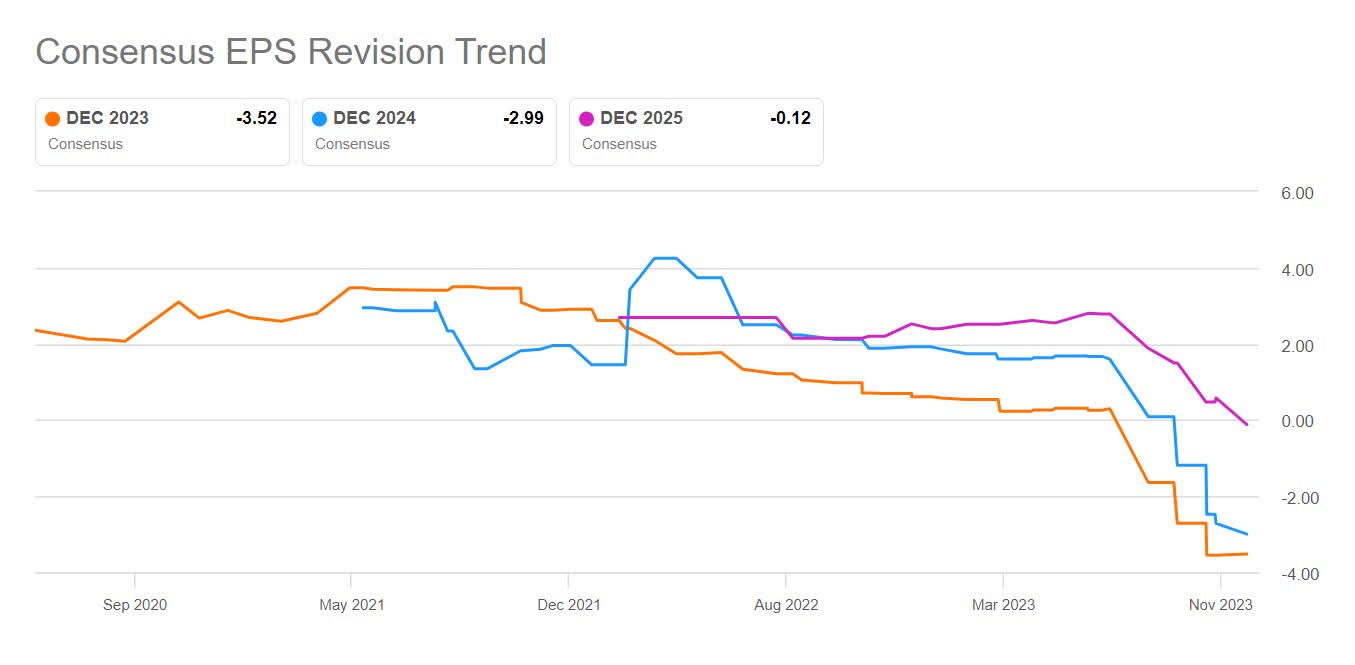

EPS revisions don't look great, either:

analyst EPS revisions (Seekingalpha.com)

{kind=link}

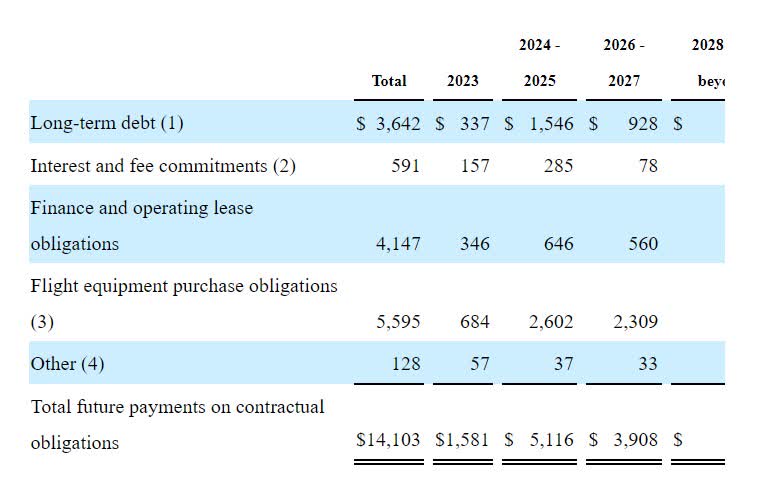

If the merger fails, everyone is immediately going to worry about the going concern. So far they aren't already, so I pulled up the liabilities from the 10-K :

Spirit liabilities (10-K SAVE)

{kind=link}

It's an ugly picture, with big payments due in 2024/2025 already. If I pull up valuation data across a range of small airlines up on Seeking Alpha, it appears to me that there is something of a merger premium baked into the current SAVE valuation:

| SAVE | ALGT | JBLU | SKYW | UP | ULCC | |

|---|---|---|---|---|---|---|

| P/E Non-GAAP (FY1) | ||||||

| NM | ||||||

| 11.57 | ||||||

| NM | ||||||

| 99.69 | ||||||

| NM | ||||||

| NM | ||||||

| P/E Non-GAAP (FY2) | ||||||

| -5.13 | ||||||

| 12.42 | ||||||

| -9.15 | ||||||

| 8.81 | ||||||

| -0.29 | ||||||

| 54.63 | ||||||

| P/E Non-GAAP (FY3) | ||||||

| -130.38 | ||||||

| 7.03 | ||||||

| 28.51 | ||||||

| 7.22 | ||||||

| -0.70 | ||||||

| 7.24 | ||||||

| P/E Non-GAAP ((TTM)) | ||||||

| NM | ||||||

| 7.72 | ||||||

| NM | ||||||

| NM | ||||||

| NM | ||||||

| NM | ||||||

| P/E GAAP ((FWD)) | ||||||

| NM | ||||||

| 13.34 | ||||||

| NM | ||||||

| 86.61 | ||||||

| NM | ||||||

| NM | ||||||

| P/E GAAP ((TTM)) | ||||||

| NM | ||||||

| 8.82 | ||||||

| NM | ||||||

| NM | ||||||

| NM | ||||||

| 16.86 | ||||||

| PEG Non-GAAP ((FWD)) | ||||||

| - | ||||||

| 0.15 | ||||||

| - | ||||||

| 1.64 | ||||||

| - | ||||||

| - | ||||||

| PEG GAAP ((TTM)) | ||||||

| - | ||||||

| NM | ||||||

| - | ||||||

| - | ||||||

| - | ||||||

| NM | ||||||

| Price/Sales ((TTM)) | ||||||

| 0.31 | ||||||

| 0.59 | ||||||

| 0.19 | ||||||

| 0.80 | ||||||

| 0.04 | ||||||

| 0.31 | ||||||

| EV/Sales ((FWD)) | ||||||

| 1.38 | ||||||

| 1.18 | ||||||

| 0.54 | ||||||

| 1.48 | ||||||

| 0.87 | ||||||

| 1.06 | ||||||

| EV/Sales ((TTM)) | ||||||

| 1.35 | ||||||

| 1.17 | ||||||

| 0.53 | ||||||

| 1.52 | ||||||

| 0.92 | ||||||

| 1.06 | ||||||

| EV/EBITDA ((FWD)) | ||||||

| 28.05 | ||||||

| 6.20 | ||||||

| 7.91 | ||||||

| 8.53 | ||||||

| NM | ||||||

| 6.81 | ||||||

| EV/EBITDA ((TTM)) | ||||||

| 153.59 | ||||||

| 6.14 | ||||||

| 7.78 | ||||||

| 10.24 | ||||||

| NM | ||||||

| NM | ||||||

| Price to Book ((TTM)) | ||||||

| 1.27 | ||||||

| 1.10 | ||||||

| 0.55 | ||||||

| 0.95 | ||||||

| 2.02 | ||||||

| 2.08 | ||||||

| Price/Cash Flow ((TTM)) | ||||||

| NM | ||||||

| 3.28 | ||||||

| 3.46 | ||||||

| 3.12 | ||||||

| NM | ||||||

| NM |

The company doesn't really stand out in terms of growth or profitability but it does tend to trade at the higher end of these ranges.

Besides the bad numbers, management's most recent commentary wasn't exactly rosy, either ( from the 10-Q , emphasis mine):

...“Softer demand for our product and discounted fares in our markets led to a disappointing outcome for the third quarter 2023. We continue to see discounted fares for travel booked through the pre-Thanksgiving period. And, unfortunately, we have not seen the anticipated return to a normal demand and pricing environment for the peak holiday periods. Given these continued trends, we are evaluating our growth profile and our competitive position. We have already taken the first steps by modifying the cadence of our aircraft deliveries through the end of the decade and slowing our capacity growth in the near term...

Finally, industry-wide, as evidenced by the U.S. Global Jets ETF ( JETS ), share prices haven't done well since just before the merger announcement:

On the bright side, the industry news has recently been a little better, as airline booking trends have strengthened in recent weeks, and the U.S. has seen record year-end holiday air travel.

More importantly, Alaska Air Group ( ALK ) is paying $18 per share for Hawaiian Holdings ( HA ), which traded at around $4.5 before the bid materialized.

Because the merger has been going on for such a long time and is highly contentious, I also think the shareholder base is a lot of fast money. If this deal breaks, it could go down hard. This could be mitigated a little by a special break fee that directs some money to SAVE shareholders if regulators shut the deal down. But at best, that's something like $0.70, and with $15 per share at risk, that's a minor consolation.

In my opinion, Spirit Airlines, Inc. equity is undervalued at around $15, but you're signing up for tremendous volatility over the coming months. The equity can get trashed under $5 or you can get the entire upside. A smooth ride is improbable. In that light, the Spirit Airlines options chain can be an attractive way to get exposure or enhance exposure. The June $30 2024 calls appear particularly overvalued to me. If you already hold shares, you could consider selling these @$0.22 cents. It can also be used as a discount to the same expiry $27.5 calls trading at $0.55 cents.

For further details see:

Spirit Airlines And JetBlue Deal: No Soft Landings Here