JBLU - Spirit Airlines: Chapter 11 Isn't On The Horizon

2024-01-18 20:10:21 ET

Summary

- Judge blocks JetBlue's acquisition of Spirit Airlines, causing stock to drop over 50%.

- JetBlue made a strong case for the merger approval, offering remedies to continue competition.

- Spirit Airlines faces bankruptcy risk, but the airline has cash and assets to stave off risk for a considerable time.

- The stock looks appealing at $6 with the domestic air travel market likely to improve in 2024.

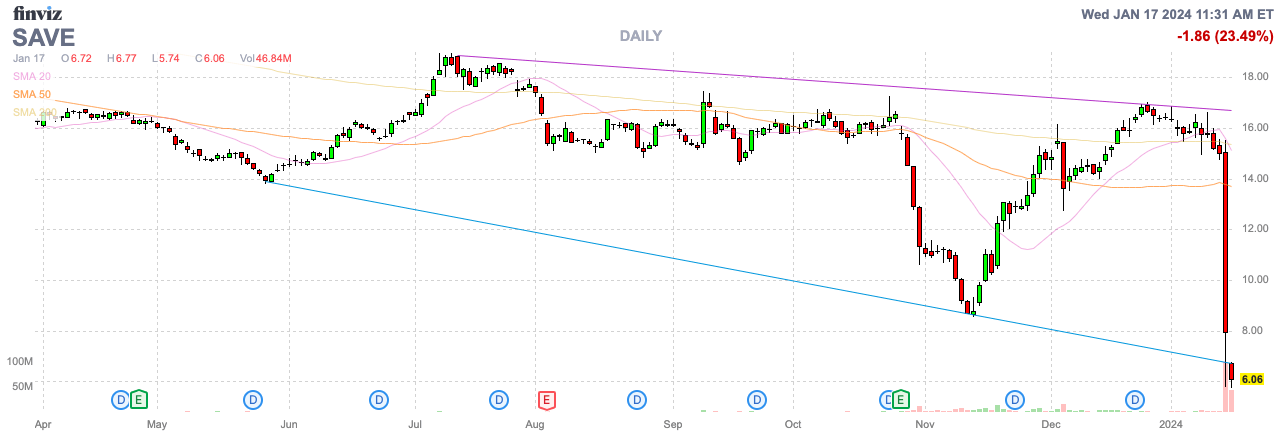

In a shocking move, Judge Young ruled against the JetBlue Airways ( JBLU ) acquisition of Spirit Airlines ( SAVE ). While the decision to permanently block the merger was a surprise, sending the stock down nearly 50% on the original news, the market reaction is far too extreme. My investment thesis is ultra Bullish on the stock following this massive dip and an over reaction to the weak results during the merger period.

{kind=link}

Proposed Merger Enjoined

The biggest concern with Spirit Airlines choosing the JetBlue Airways merger proposal was the likelihood the DoJ would sue to block the merger. For this reason, JetBlue provided upfront cash to Spirit shareholders amounting to nearly $4 in cash by now.

Even despite the fears, JetBlue appeared to make a strong case for the merger approval. The airline offered up remedies to continue competition in the ULCC market and JetBlue made the case during the trial that customers weren't harmed by the merger over the long haul.

The airline made the case that substantial harm wouldn't exist following the merger with the United Airlines (UAL) CEO making the case of the large airline and other ULCC competitors chasing any supply removed by the Spirit merger. JetBlue made the clear case that substantial harm doesn't exist with both legacy airlines and competitors flooding the market to replace the removal of Spirit Airlines.

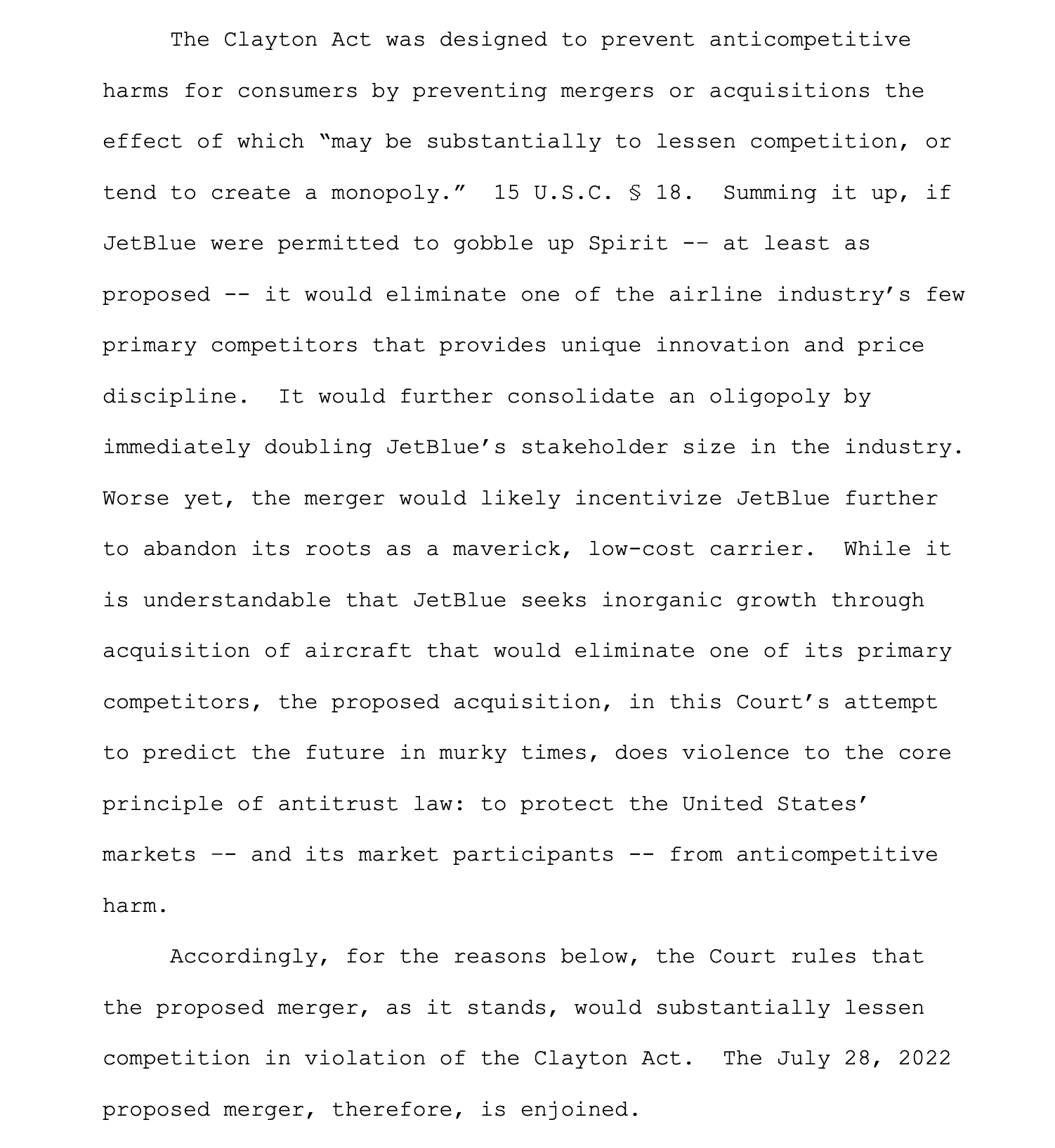

Judge Young didn't agree with the case presented by JetBlue suggesting Spirit customers would be harmed in the process of the merger, though questions abound on whether the law presented by the Clayton Act requires removal of all harms.

The following is a copy of the section in the ruling summing up the reason for the court blocking the merger:

Source: JetBlue/Spirit case document

{kind=link}

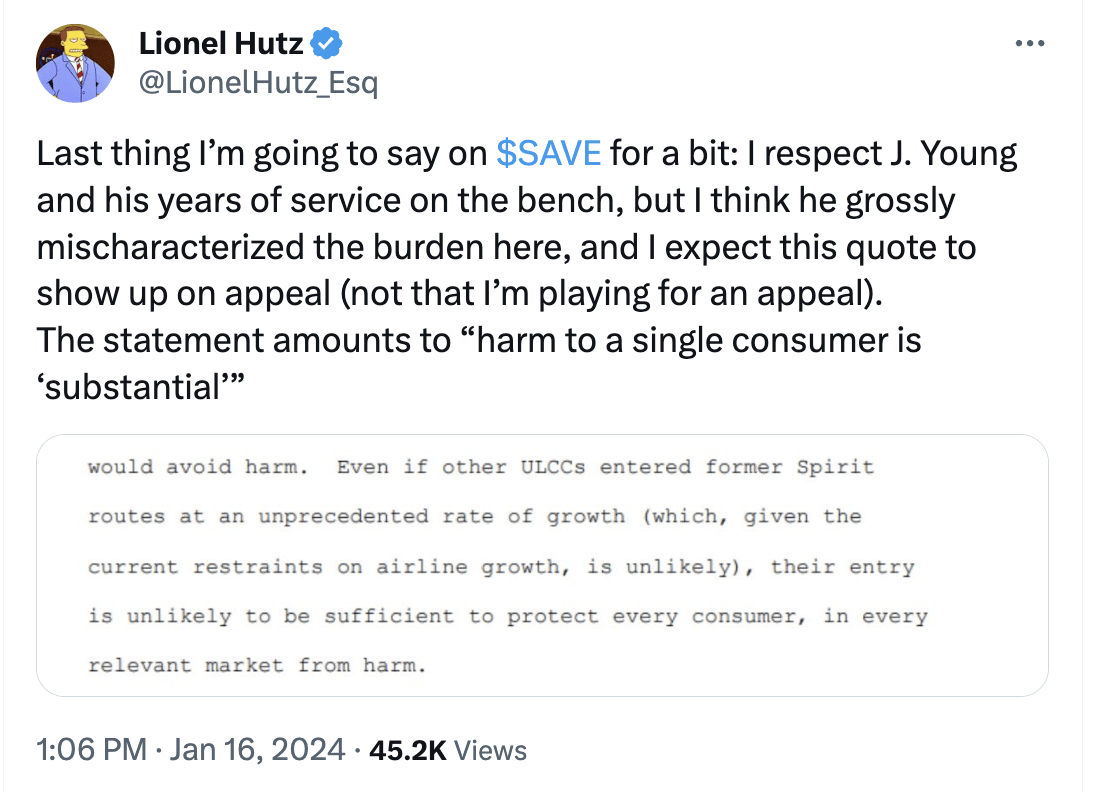

The airlines are still working on whether to appeal the case. JetBlue had provided a supplement to the court on the Illumina case suggesting the ruling required the finding of substantial harm to consumers in order to block the merger.

Most investors thinking the merger would be approved are shocked by this statement from the judge suggesting the merger can't harm any consumer via any relevant market. As mentioned in the tweet, JetBlue would likely focus on this statement in any appeal.

Source: Lionel Hutz Twitter/X account

{kind=link}

Irrational Bankruptcy Fears

The airline appears to have a case for appeal, but the investment thesis here is based more on whether bankruptcy risk is actually logical with the stock falling all the way to $6. The airline sector became very profitable during 2023, yet the ULCC sector is under substantial pressure now.

While TD Cowen proposed that Spirit Airlines would seek another buyer or end up in Chapter 11 bankruptcy , the airline appears headed for neither outcome. Spirit Airlines was just blocked from merging with JetBlue and the airline would seem unlikely to immediately pursue another merger.

The airline clearly had interest in merging with Frontier Group ( ULCC ), but one has to question whether Frontier wants to go down this path. Considering Alaska Airlines ( ALK ) has already agreed to a merger agreement with Hawaiian Airlines ( HA ), Spirit Airlines wouldn't exactly have any other options.

The airline reported some weak results during Q3'23, but Spirit Airlines isn't likely to need a Chapter 11 filing. The airline entered the Summer months expecting a massive profit and for multiple reasons Spirit Airlines ended up reporting massive losses.

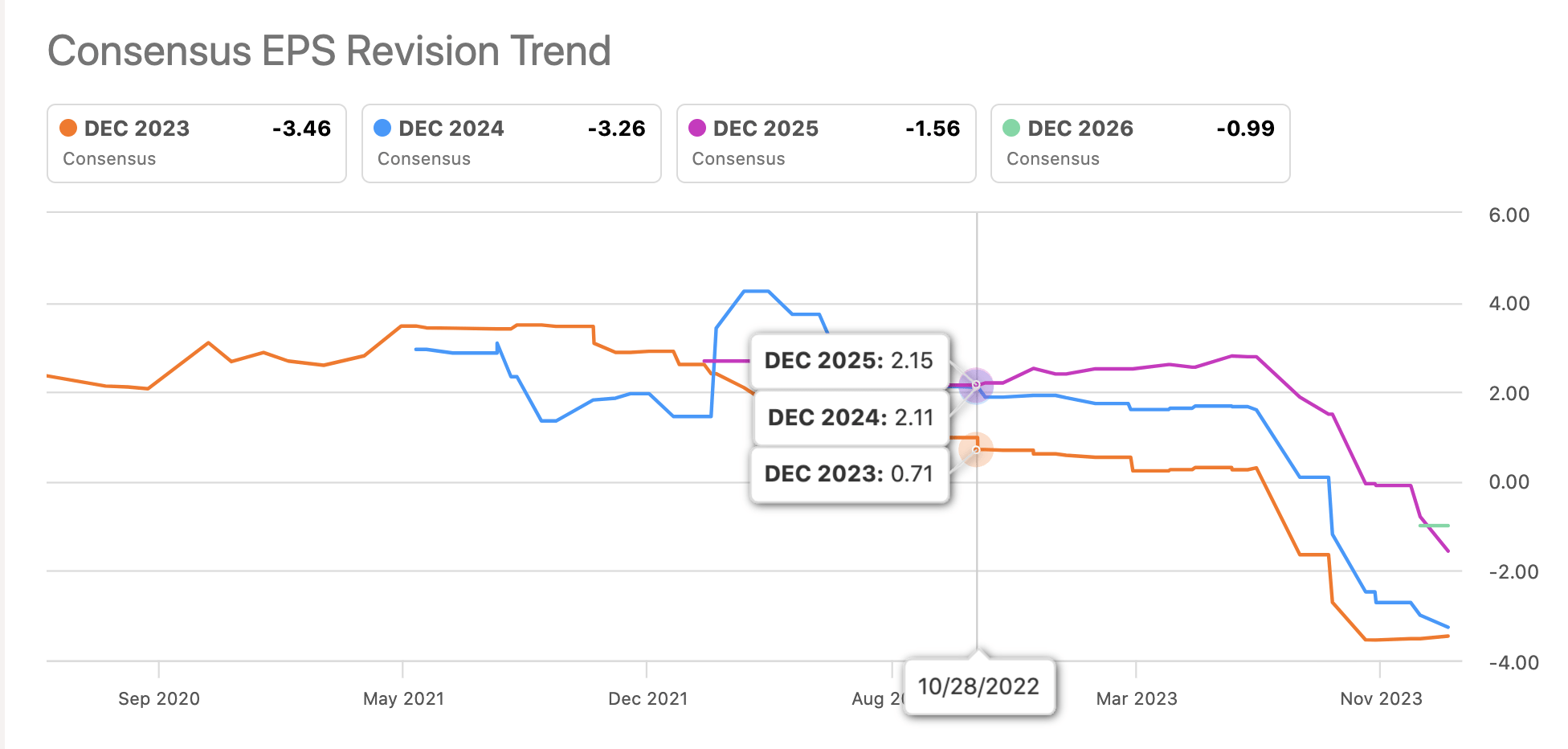

The consensus analyst estimates entering 2023 was for Spirit Airlines to earn nearly $1 per share for the year with forecasts for a $2+ EPS in 2024. The domestic sector ran into fare pressures with consumers focused on international travel and higher fuel costs hit profits just as fares were under pressure.

{kind=link}

In addition, oil prices have slumped leading to lower jet fuel prices. Also, Delta Air Lines ( DAL ) just confirmed capacity constraints on domestic routes will lead to higher yields in 2024 based on this statement from CEO Ed Bastian on the Q4'23 earnings call :

Domestically, supply and demand are coming into better balance as the industry adjusts to rising costs of production, and we are seeing a positive inflection in domestic unit revenue growth.

JetBlue provided a prime example of this scenario by recently reporting that Q4'23 results would top prior estimates. The airline released this information on December 7, just 2 days after the trial ended.

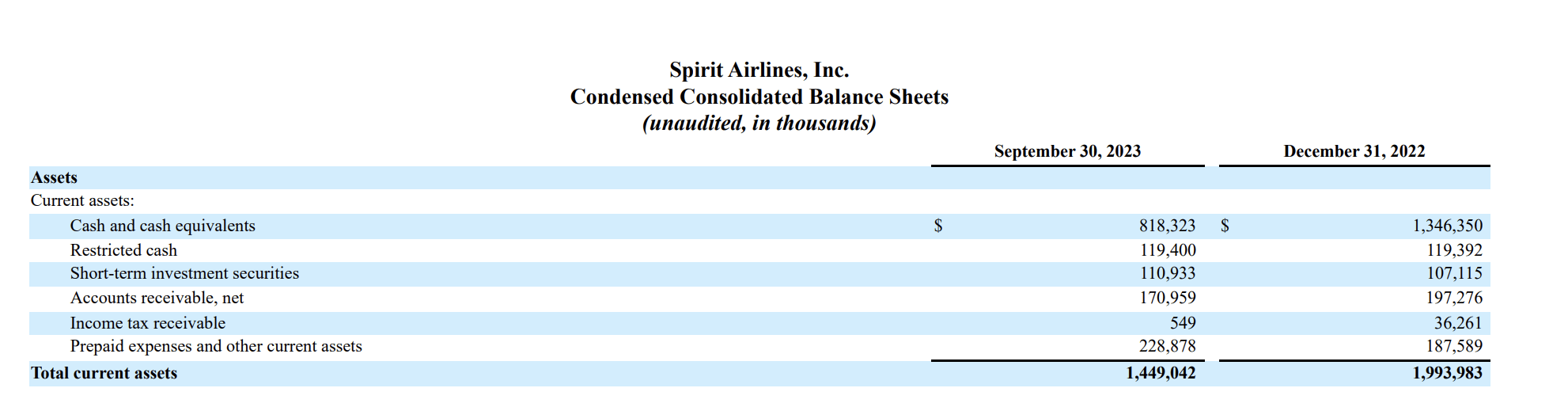

At the end of September, Spirit had a cash balance of $1.05 billion. The airline isn't in a dire position despite having a debt position of ~$3.3 billion.

Source: Spirit Airlines Q3'23 10-Q

{kind=link}

Investors commonly forget that airlines are asset rich. Spirit Airlines has $3.7 billion in net Property and equipment to offset any outstanding debt.

Only a week ago, Spirit Airlines sold 25 planes to generate $419 million in cash to repay debt. As mentioned, the airline has plenty of assets to repay debt and Spirit wouldn't be making these moves, if bankruptcy was in the cards.

The key to Spirit's survival is returning the business to producing profits and positive cash flows. The Q3'23 report was horrible with the airline reporting a loss of $158 million.

Remember though, Spirit Airlines and JetBlue had no incentive to report strong profits during this period because it would only provide fuel to the fire of the regulators to block the merger. Turns out, the Judge ruled harm existed anyway, though he clearly pointed out the risk blocking the merger provided no benefit, if Spirit Airlines ends up in economic trouble and isn't able to offer low-cost fares to passengers.

Takeaway

The key investor takeaway is that Spirit Airlines faces bankruptcy risk, if the airline doesn't improve financials. The catch here is that the airline has the cash and assets to stave off any risk for a considerable time and all signs point towards a better domestic market this year.

The airline is a bargain at $6 with expectations the domestic market will miraculously improve in 2024 and Spirit Airlines will return to the $1 to $2 EPS targets prior to the merger. In addition, the airline could still win merger approval on appeal providing substantial upside to the stock with the cash deal still valued at nearly $30 after deducting the prepayments.

For further details see:

Spirit Airlines: Chapter 11 Isn't On The Horizon