CA - Sprott: Higher Rates Still Do Hurt

2023-10-23 22:02:00 ET

Summary

- Sprott is a pretty idiosyncratic AM bet focused on physical trusts and commodity ETFs that can help investors get exposed to precious and renewable metals.

- There is a tense geopolitical undercurrent that helps bullion speculation, and secular trends for renewables that offer some tailwinds.

- However, fixed income is attractive again, and Sprott doesn't really benefit in its business from a higher rates environment.

- Just as importantly, there isn't as much margin for the equity when benchmark rates come up. It's too expensive for what it is.

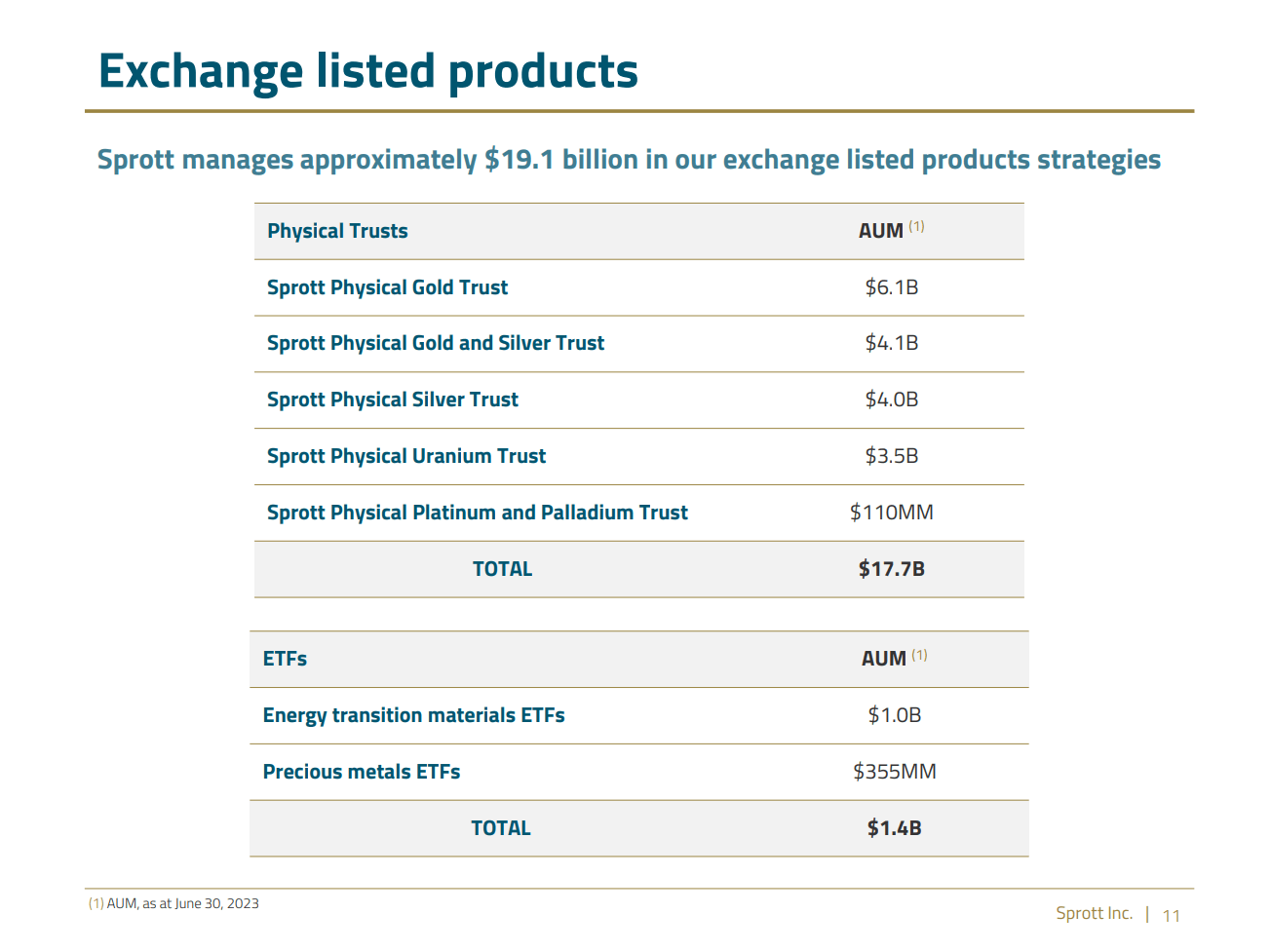

Sprott Inc. ([[SII]], [[SII:CA]]) is a worthwhile look into an interesting AM pick. They are big of physical trusts, including Sprott Physical Uranium ( SRUUF ), as well as ETFs that give access to precious metals and also lithium. Fees tend to be higher on these sorts of vehicles, especially physical trusts, and in an environment where the money market and cash have a lot of gravity, Sprott's exposures offset some of the pressures thanks to things like the renewable transition. Still, as we believe rates are going higher, Sprott is not attractive at current valuations.

Q2 Breakdown

YoY there has been decent performance in terms of EBITDA, sales, and AUM . AUM is up nicely at around 7% and EBITDA is up slightly on a 3-month basis despite the sales of the broker-dealer business last year in Canada. On a 6-month basis the effects are bigger of the broker-dealer loss, so EBITDA is down 2% there. AUM is down sequentially though by 1% , mainly driven by declines in the actual value of some of the trusts, even though there were inflows into the private strategies and the most important category of their exchange-listed products.

{kind=link}

There are a couple of positive tailwinds for Sprott. They are well placed for the renewable energy transition. There aren't that many uranium ETFs out there, and there's real scarcity of physical trusts. They also got their lithium Miners ETF listed on the Nasdaq ( NDAQ ) and other ETFs that select miners for key renewable energy materials, including a uranium mining ETF as well as copper. We are still seeing sequential inflows into these products.

This is in spite of the obvious fact that the higher rate environment means that money market products and yielding cash accounts have become the most lucrative they've been in recent history. Gold and silver have apparently seen a relatively weak correlation recently between the actual performance of these precious metals and the inflows into related ETFs, which Sprott covers.

We've looked at the historical correlation between flows into gold ETFs and the gold price. And there's a very strong relationship. Over the last few months, that is decoupled, and we think it's largely on the back of investors migrating to 5% essentially risk-free money market investments.

John Ciampaglia, Senior Managing Partner for Sprott

This is something that shouldn't last too long because if rates stay high for even longer than the market currently expects, bullion should come back into fashion as people worry about state finances. While the US is a bit of a special case because of its exorbitant privilege, we've already seen that currencies can get smashed by protest from bond markets in the UK around Liz Truss and her unfunded tax cut proposals. Moreover, we have a new undercurrent of geopolitical unrest, which always lends itself to speculation on bullion, and is likely why the price of bullion is still rising, even if inflows aren't as much. Moreover, when rates peak, which they probably haven't yet, cash will become less attractive. Cash will rather go into bonds, and as duration bets start getting made, risk management probably will reduce overall exposure to fixed income, with useful elements needed for the renewable energy transition or bullion likely to be interesting for allocators as they march to the beat of their own drum. In particular, there is still upside to uranium and the role of nuclear in renewable energy systems, since that had long been sidelined and will likely become a dominant technology for low carbon energy and electrification.

Bottom Line

The issue is Sprott is still quite expensive at a 17x PE. They are also still exposed to higher rates. Management is confident that rates will come down somewhat soon. We are not confident of that at all and think that just on the basis of deglobalisation we are going to have to see higher natural rates. While there may be some incremental benefit to the Sprott ETPs on offer, even if rates were to increase some more and start seeing peaks, it's not like the high-rate environment is a good thing. Renewable has its own secular case, as do the resources needed to make that happen, and bullion remains a speculative staple. These are good things. But the scope for strong incremental benefit as fixed income comes out of hibernation is somewhat limited, and with higher fixed income rates, the Sprott valuation is also problematic and doesn't really offer a margin of safety.

For further details see:

Sprott: Higher Rates Still Do Hurt