CA - Sprott Physical Gold and Silver Trust: Consolidation In Progress

Summary

- The CEF trust holds gold and silver bullion in a 65/35 ratio.

- Precious metal prices benefited from a reduction in the Fed's pace of interest rate hikes, with gold rallying over $300/oz in recent months.

- However, gold investors have gotten complacent and overly optimistic, forgetting that the Fed plans to keep interest rates 'higher for longer'.

- In a 'higher for longer' scenario, the U.S. dollar could rebound, pressuring gold prices.

The Sprott Physical Gold and Silver Trust (CEF) provides exposure to gold and silver bullion in a 65/35 ratio. It has a unique feature allowing unitholders redeem their holdings in physical bullion.

While gold investors were overly pessimistic in October, they have gotten overly optimistic in recent months due to the 'pivot' in the Fed's pace of rate hikes. However, they are ignoring the Fed's intention to raise interest rates 'higher for longer', which is potentially negative for gold prices. I believe a period of consolidation / pullback is necessary to reset expectations on gold and silver bullion.

Fund Overview

The Sprott Physical Gold and Silver Trust is a closed-end trust that holds unencumbered and fully-allocated physical gold and silver bullion stored at the Royal Canadian Mint.

The CEF trust has $4 billion in assets and charges a 0.51% management expense ratio.

CEF History

The CEF trust was originally called The Central Fund Of Canada, and its purpose was to act as 'The Sound Monetary Fund' . Its main selling point was that the precious metal bullion it held in trust were held on an unencumbered, fully allocated, and segregated basis. In 2018, Sprott Inc. acquired the right to administer the assets of the CEF trust and changed its name to the Sprott Physical Gold And Silver Trust.

Sprott Inc. was founded by Eric Sprott , a well-known Canadian investor synonymous with precious metals investing. However, in recent years, Mr. Sprott is no longer involved with the firm that bears his name.

Features Of The CEF

Fully allocated means that investors are the ultimate owner of the bullion held in trust, and the account provider is merely a custodian. In the event of a bankruptcy of the custodian, allocated account holders are the legal owners of the bullion whereas unallocated account holders must wait in line with other creditors.

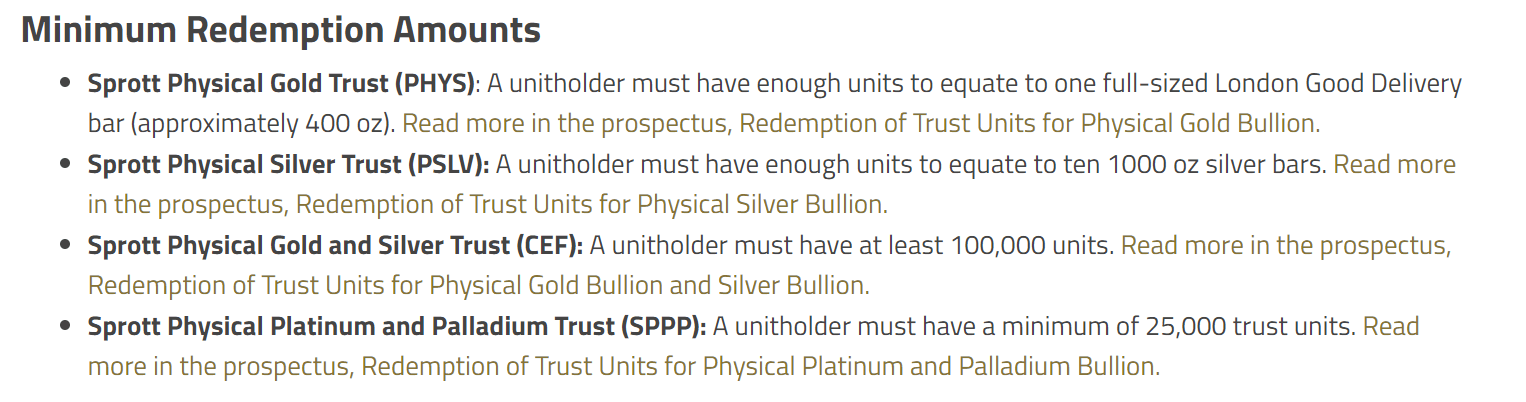

Another unique feature of the CEF trust and other Sprott physical products is that unitholders can choose to redeem their holdings for physical bullion, provided they meet the minimum redemption requirements (Figure 1). To my knowledge, Sprott is the only provider offering this feature.

Figure 1 - CEF has unique physical redemption feature (sprott.com)

{kind=link}

Portfolio Holdings

The CEF trust's holdings are very simple. It holds 1.4 million oz of gold and 58.2 million oz of silver bullion in trust at the Royal Canadian Mint (Figure 2). The split in market value of the trust's assets is 65% gold, 35% silver.

Figure 2 - CEF trust holdings (sprott.com)

Returns

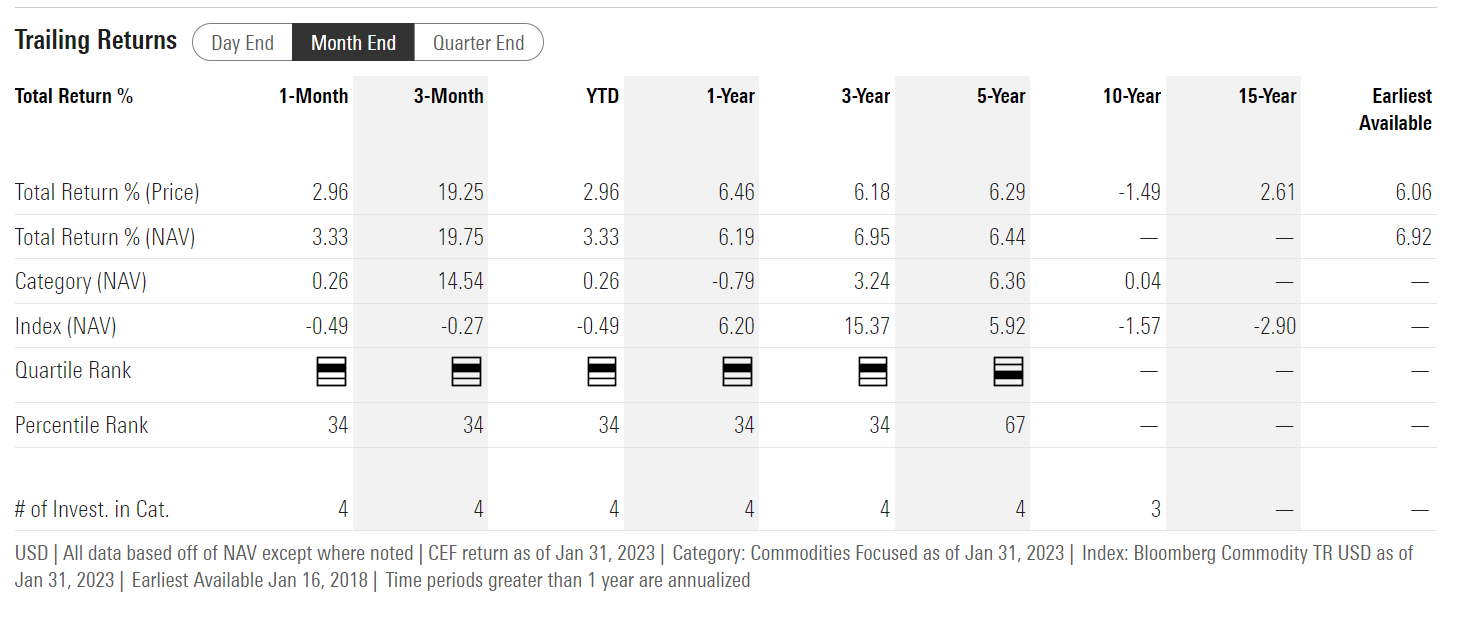

The CEF trust's historical returns follow that of gold and silver prices. Over the long run, the CEF trust has provided modest returns, with 3 and 5Yr historical returns on NAV of 7.0% and 6.4% respectively (Figure 3).

Figure 3 - CEF historical returns (morningstar.com)

{kind=link}

In my opinion, investors should not be looking at gold and silver bullion as investments to 'get rich' with. Instead, I believe the main purpose of a precious metal bullion allocation in a portfolio is as an insurance policy, whether it is against market crashes, hyperinflation, or some other market calamity. Gold has served as a store of value for thousands of years, and will likely act as a store of value for many years to come.

Gold Investors Have Gotten Too Optimistic

Readers who follow my research and articles will note that I turned bullish on gold in late October , when gold had fallen to $1620 and the bottom was falling out.

At the time, gold investors were worried that the Fed was going to keep hiking interest rates by 75 bps per meeting, putting upward pressure on interest rates and the U.S. dollar. However, by late October, there was market chatter of a potential 'Fed Pivot', spurred by a timely article from WSJ reporter, Nick Timiraos. Although Mr. Timiraos believed the Fed was going to hike by 75 bps at the November meeting, he also mentioned the Fed may be looking to reduce the size of future hikes.

Mr. Timiraos is one of the most plugged-in reporters, and has a reputation as the ' Fed Whisperer '. Sure enough, at the November meeting, the Fed indeed hiked by 75 bps, but signalled that they may slow down the pace of future rate hikes, as the Fed did not want to overtighten monetary policy. This was subsequently confirmed by a step down to a 50 bps hike in the December FOMC meeting, and recently, a 25 bps hike at the February meeting . However, while gold investors were too pessimistic in October, I believe the opposite is happening now and gold investors have gotten too optimistic.

Fed Aiming For 'Higher For Longer'

What a lot of investors seem to be forgetting is that while the Fed may be slowing down the pace of rate hikes, they also explicitly said that additional rate hikes may be required to get to a sufficiently restrictive monetary policy level. Furthermore, they expect to maintain the restrictive policy rates for a period of time, until they feel comfortable inflation is going back to their 2% target.

Financial Conditions Are Getting Too Easy

Instead, investors have chosen to only listen to what they want to hear, focusing on the step down in the pace of interest rate hikes. This has led to a significant rebound in financial markets and tightening of credit spreads since October, causing a massive loosening of financial conditions, reversing much of the work that the Fed tried to implement in 2022. According to the Chicago Fed's National Financial Conditions Index, financial conditions are now as loose as they were in early 2022 (Figure 4).

Figure 4 - Financial conditions have loosened to early 2022 levels (Chicago Fed)

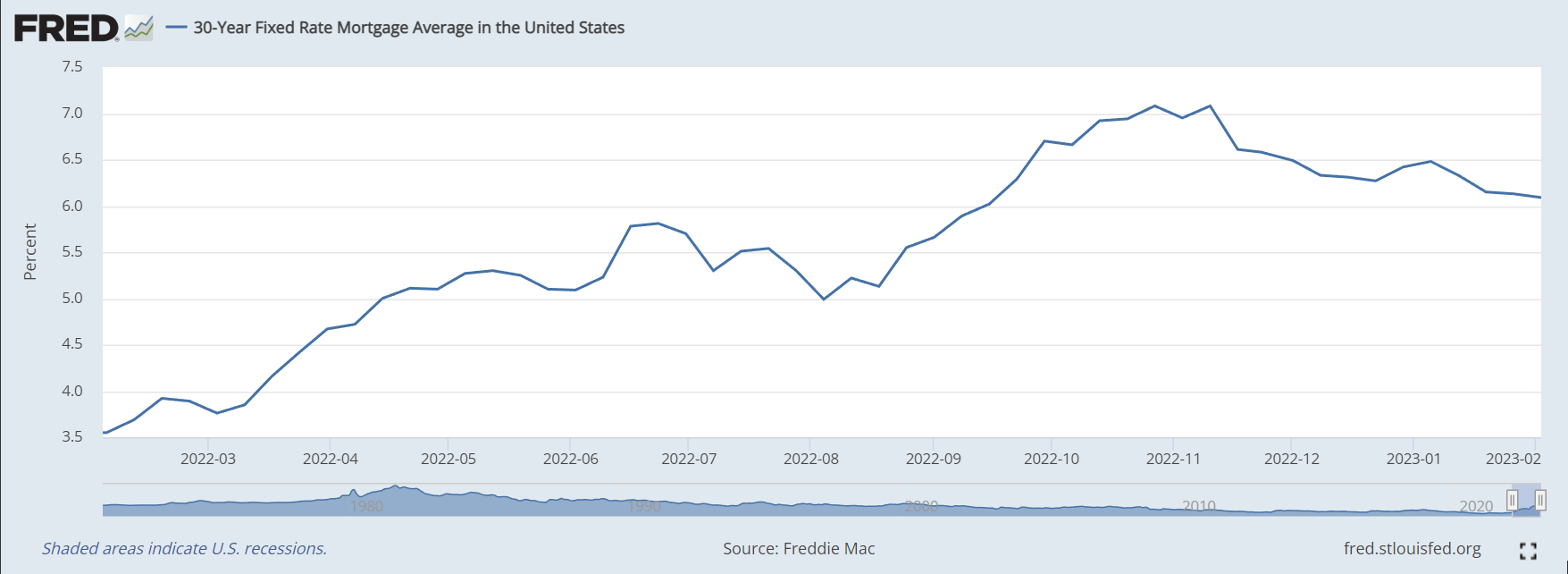

Loosening financial conditions have re-awakened animal spirits that could threaten the 'soft landing' picture. Already, we are seeing 30Yr mortgage rates decline by a full percentage point from the recent highs and pending home sales have started to rebound (Figure 5).

Figure 5 - 30Yr mortgage rates have declined by over 1% (St. Louis Fed)

{kind=link}

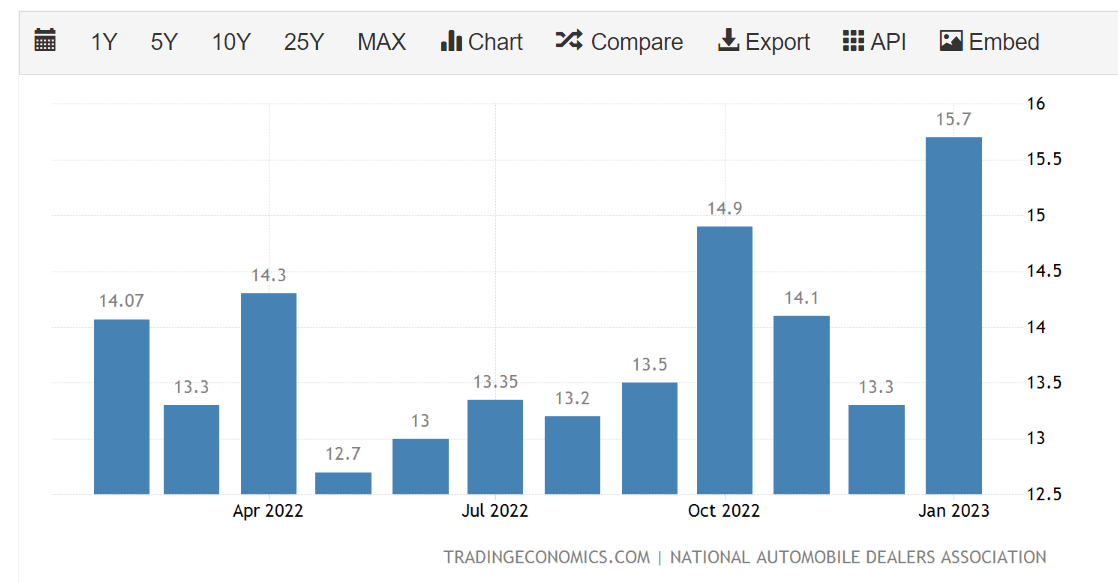

Likewise, U.S. auto sales surged 4.2% YoY to a 15.7 million annualized level, the highest rate in months (Figure 6).

Figure 6 - U.S. auto sales, seasonally adjusted (tradingeconomics.com)

{kind=link}

Could Inflation Make A Comeback?

If investors are not careful, the loosening of financial conditions risk reigniting goods and housing inflation that had been a big part of the recent disinflation story, with monthly headline CPI inflation declining 0.1% MoM in December (Figure 7).

Figure 7 - Headline CPI inflation declined 0.1% MoM in December ((BLS))

In fact, with gasoline prices rebounding due to tighter supply/demand balance from a re-opening Chinese economy and Russian sanctions, the U.S. could be facing a rebound in inflation figures in the coming months as the energy component in figure 7 above reverses. For example, in Europe, Spain recently saw a rebound in its inflation figures after many months of declines.

Higher For Longer Could Be Bad For Gold

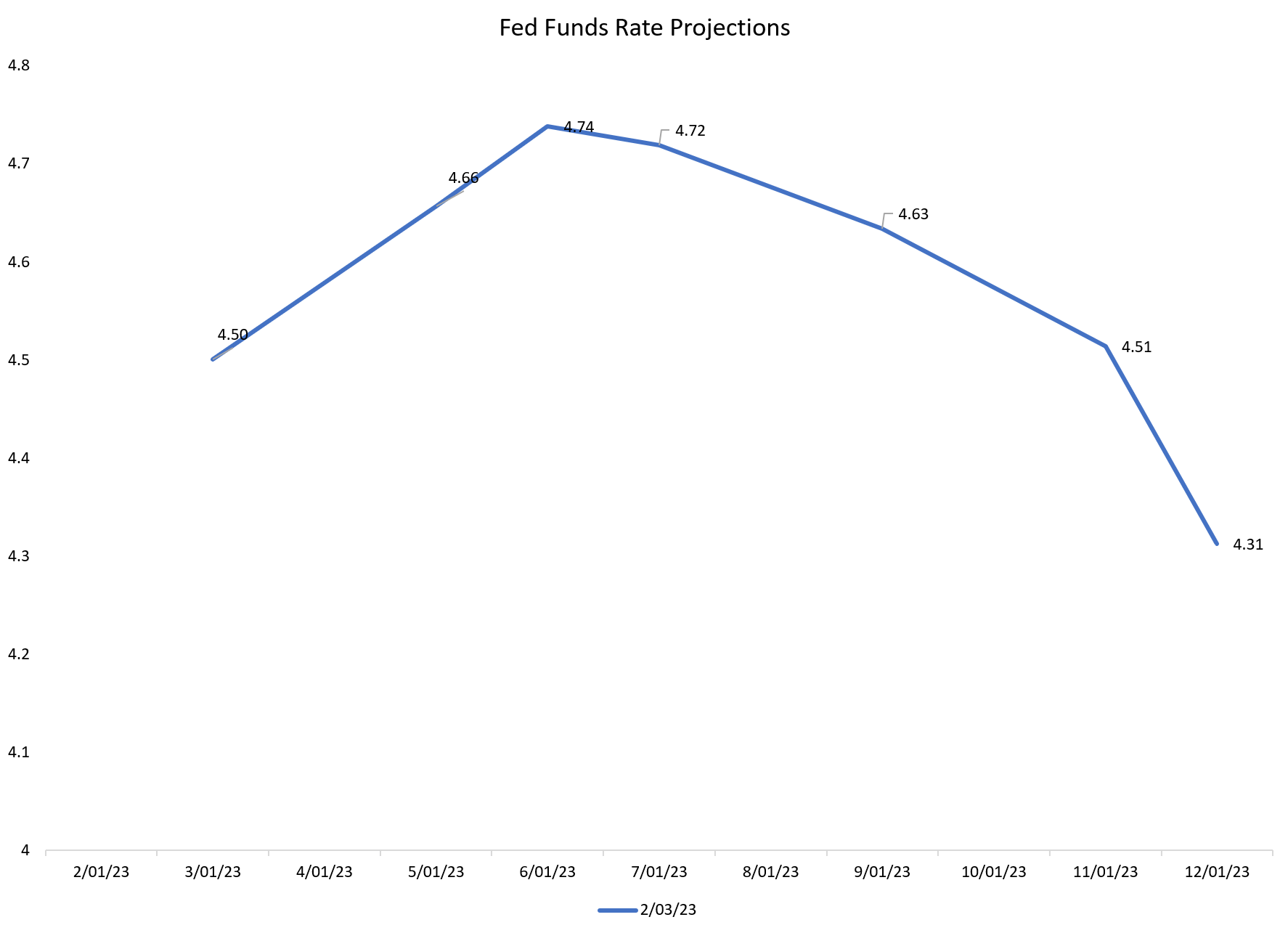

If inflation makes a comeback, investors need to be prepared for the Fed to stick to its 'higher for longer' plan, meaning market expectations for a 'soft landing' and a rapid decline in interest rates in the back half of 2023 may be misplaced (Figure 8).

Figure 8 - Investors expecting a rapid reduction in interest rates (Author created with data from CME)

{kind=link}

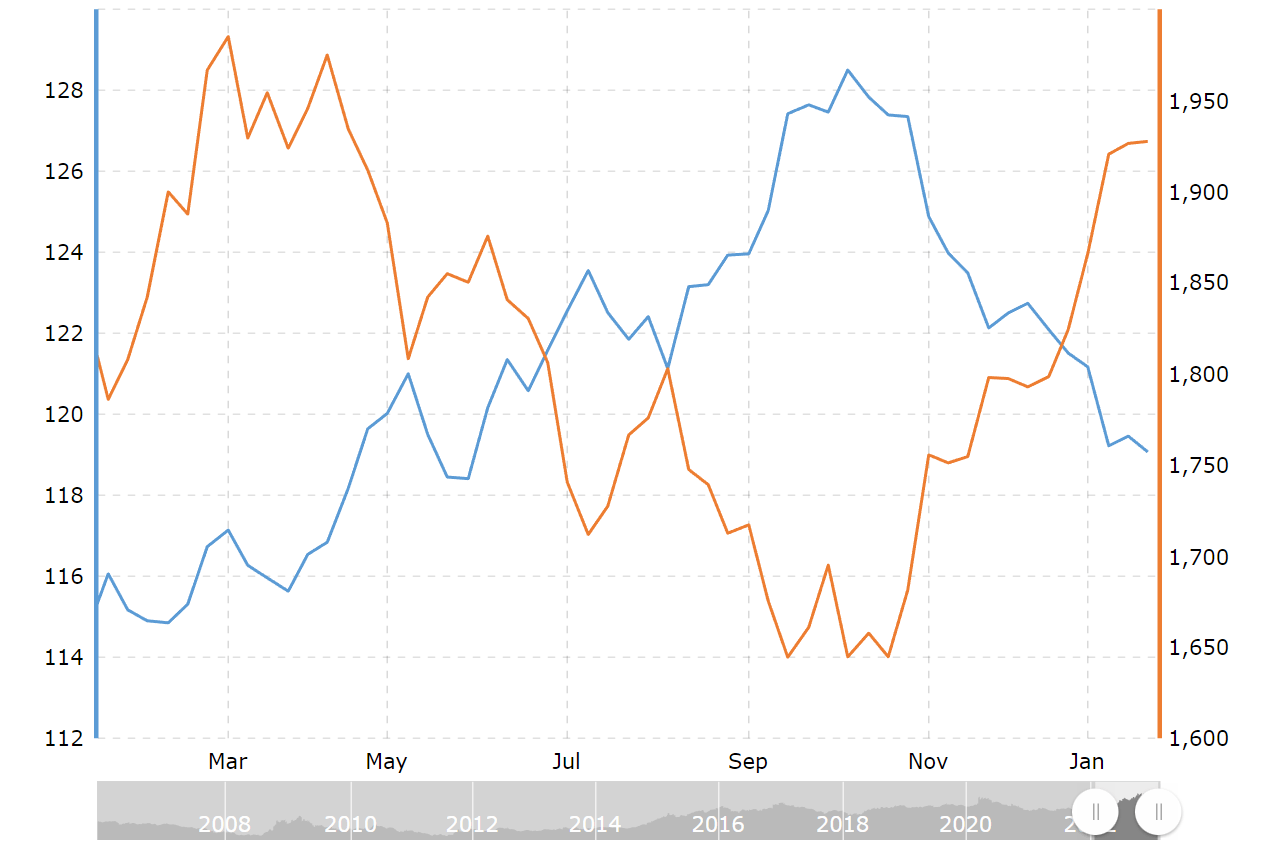

Since October, as the Fed became relatively more dovish and other global central banks like the ECB became more hawkish, the U.S. dollar suffered a massive decline. The broad trade weighted U.S. dollar fell by over 7% since late October (from 128.5 to 119.07 recently), sparking a 2-month $300/oz gold rally (Figure 9).

Figure 9 - Decline in U.S. dollar was the main driver in gold rally (macrotrends.net)

{kind=link}

If investors normalize their interest rate expectations to the 'higher for longer' path that the Fed has guided to, the U.S. dollar could rebound significantly and gold prices could tumble.

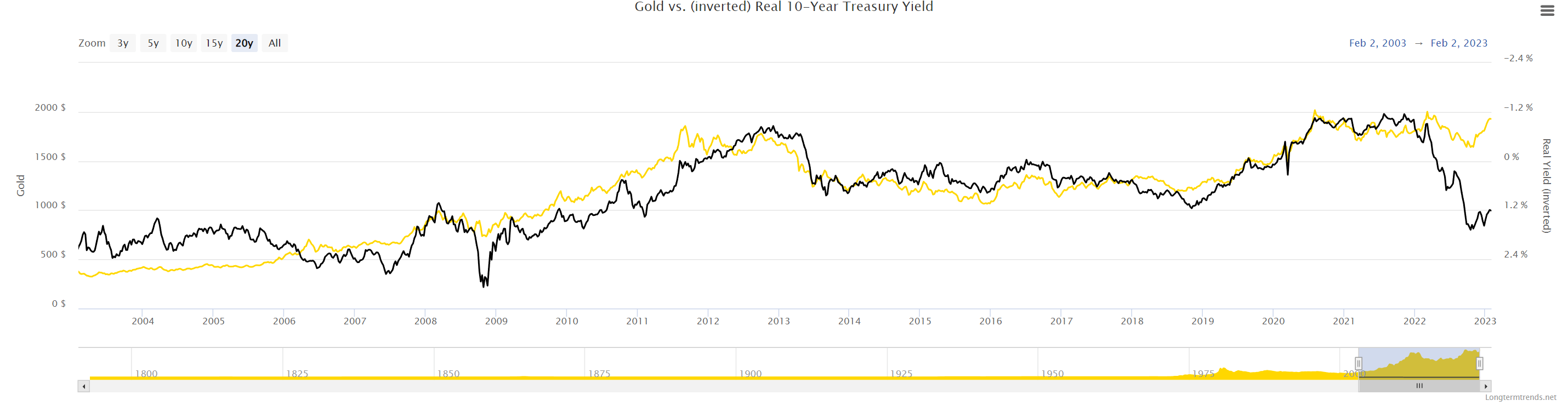

Furthermore, a higher for longer Fed could be bad for gold as higher nominal interest rates places upward pressure on real interest rates. Historically, gold prices have a -0.82 correlation to 10-Yr Real Interest Rates, measured as the Nominal 10-Yr Treasury Yield subtract the 10-Yr Inflation Breakeven Rate. Notice in figure 10 below, based purely on the real rate correlation, gold should be trading near ~$1,000.

Figure 10 - Real rates suggest gold prices should be much lower (longtermtrends.net)

{kind=link}

Strong Payrolls Could Be An Inflection

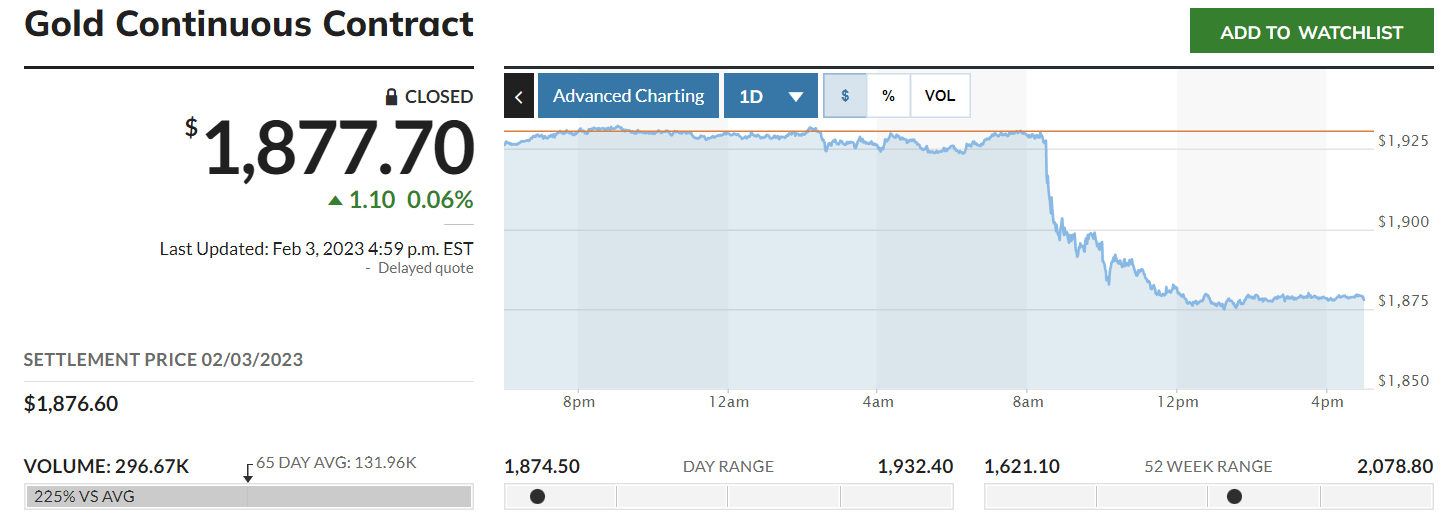

The strong non-farm payrolls figure on February 3rd could be the inflection point the U.S. dollar has been looking for. The January 2023 jobs report showed that U.S. non-farm payrolls increased by 517,000, blowing past estimates for a 185,000 increase. Prior month figures were also revised significantly higher (November added 34,000 and December added 37,000). Importantly, the unemployment rate fell 0.1% MoM to 3.4% vs. an estimate of 3.6%.

The extremely strong payrolls data threw cold water on investors' expectations of a 'soft landing' and the U.S. dollar index rose by 1.2% as bearish U.S. dollar traders were forced to cover and gold prices fell by $50 in response (Figure 11).

Figure 11 - Gold prices declined by $50 on February 3 (marketwatch.com)

{kind=link}

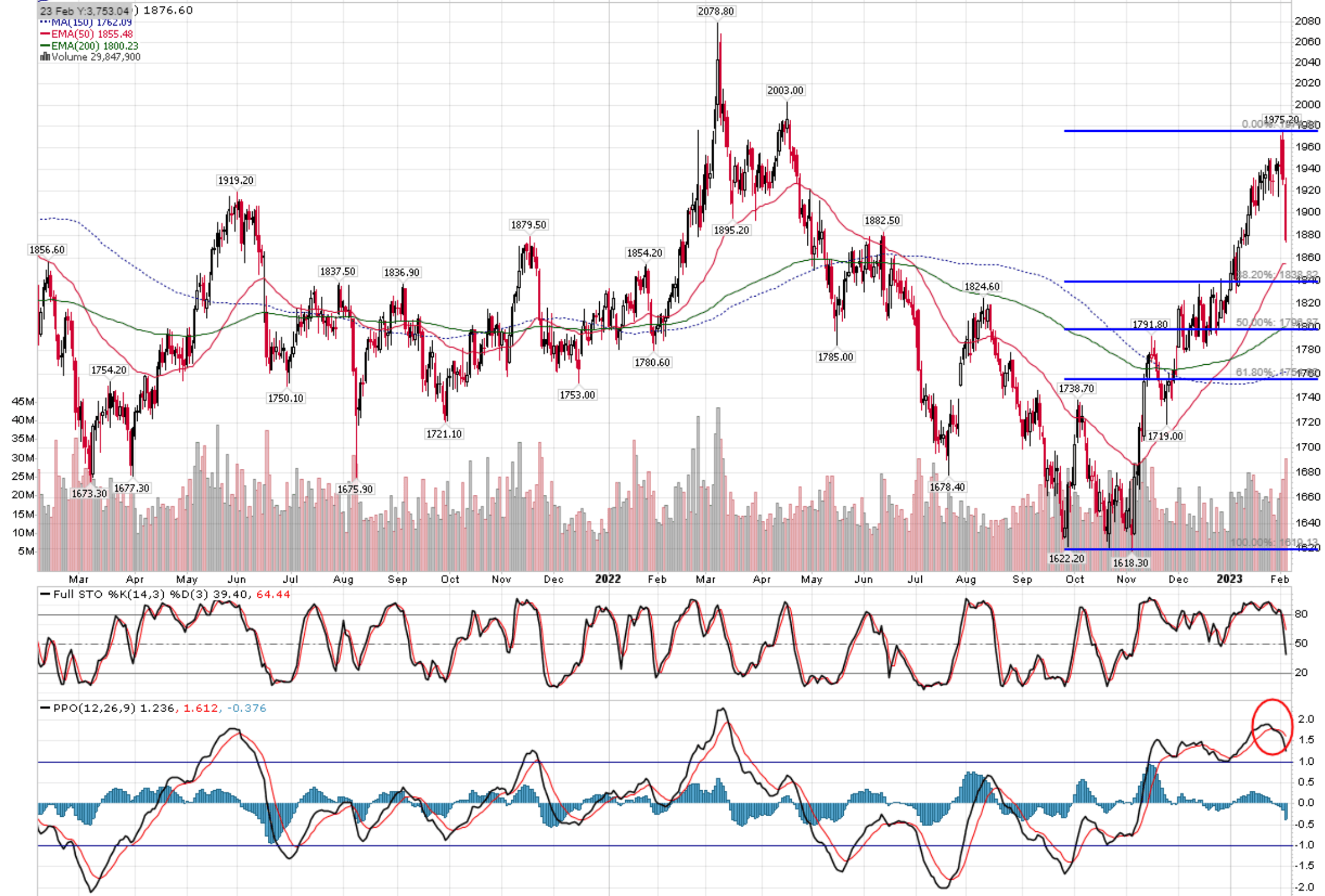

Technicals Suggest Consolidation / Pullback

Technically, gold prices are very overbought and prone to a period of consolidation/pullback. In a recent article on Wheaton Precious Metals Corp. ( WPM ), I suggested investors take profits on their gold investments ahead of the February FOMC meeting, and that call still stands. A mechanical bearish crossover in the PPO indicator suggest the pullback has already begun, with first downside at the 38.2% retracement level or ~$1840 on gold bullion (Figure 12).

Figure 12 - Technicals suggest gold correction has begun (Author created with price chart from stockcharts.com)

{kind=link}

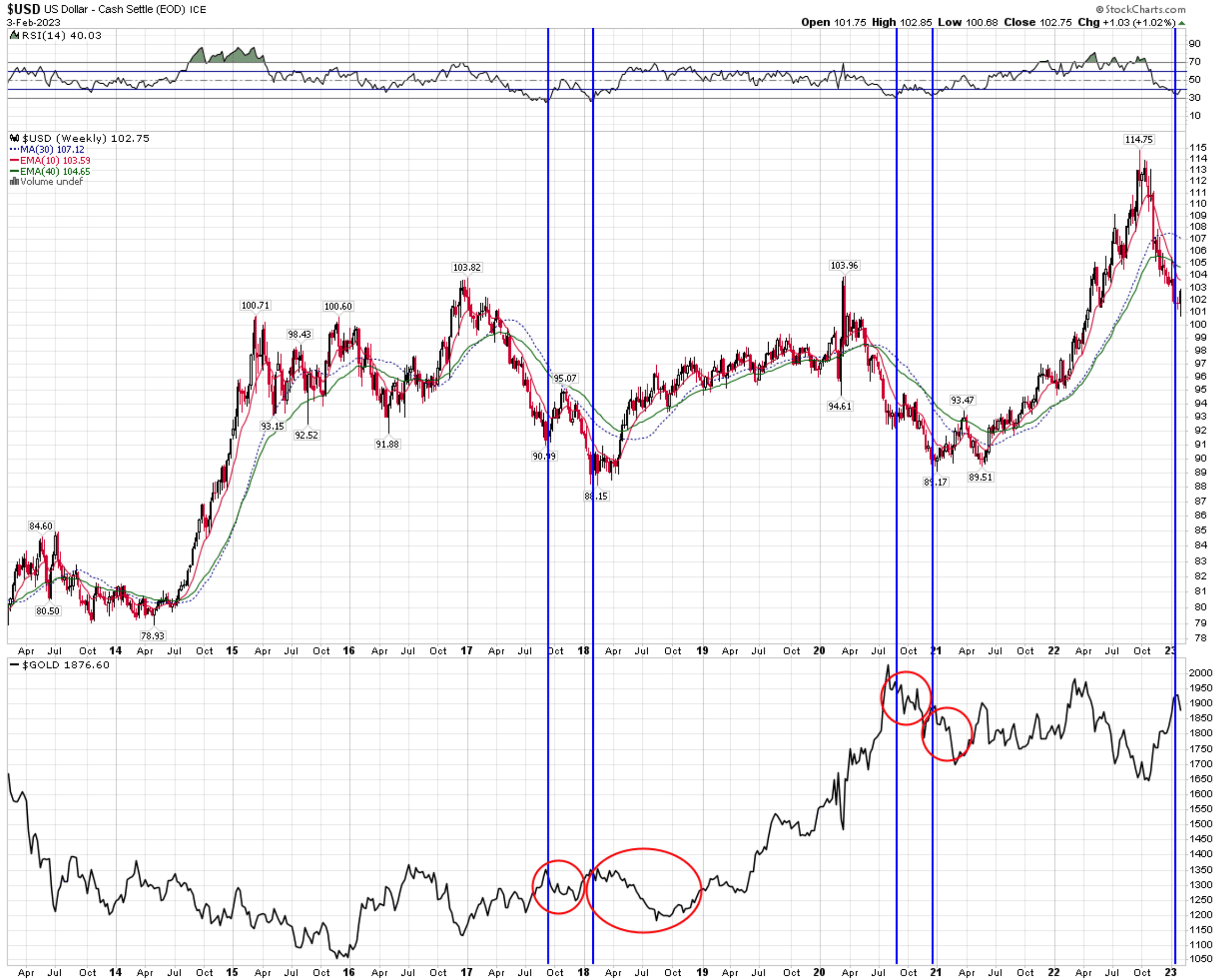

Ultimately, the U.S. dollar index has only been this oversold on a weekly RSI level 4 times in the past decade, and in every instance, gold prices saw a significant period of consolidation / declines (Figure 13). Even if the U.S. dollar ultimately heads lower like in 2017/18 and 2020, we should see a period of consolidation in gold prices.

Figure 13 - U.S. dollar index has been this oversold only 4 other times in the past decade (Author created with price chart from stockcharts.com)

{kind=link}

Conclusion

The CEF trust owns gold and silver bullion in a 65/35 ratio. It has a unique feature allowing unitholders redeem their holdings in physical bullion. I believe precious metal investors have gotten overly optimistic in recent months due to a reduction in the pace of the Fed's interest rate hikes and a period of consolidation/pullback may be necessary to reset expectations.

For further details see:

Sprott Physical Gold and Silver Trust: Consolidation In Progress