CA - Sprott Physical Uranium: Ready For Lift-Off?

2023-06-12 06:01:53 ET

Summary

- Uranium prices have not experienced significant upward movement despite favorable market fundamentals, leading to investor disillusionment.

- Recent divergence between Sprott Physical Uranium Trust's market value and rising spot prices may indicate a thinning spot market and depletion of secondary supplies.

- Factors supporting potential uranium price growth include rising mining costs, geopolitical events, strong demand from financial speculators, a growing nuclear fleet, and a tightening spot market.

Investor disillusionment is widespread in the uranium market. In the past couple of years, speculative capital flooded the sector, enticed by the allure of quick profits and reminiscent of the previous uranium bull market. During that time, uranium prices skyrocketed by over 1000% within three years, reaching an all-time high of approximately $140 per pound in 2007. However, the anticipated parabolic surge in uranium prices has yet to materialize, leading some investors to exit the space. This departure has added to the frustration, given the highly favorable market fundamentals. It therefore remains puzzling why uranium has not experienced a more significant upward movement.

The prevailing negative sentiment is evident in the decline of uranium miners over the past year, trailing behind the performance of the commodity itself. For instance, the Sprott Junior Uranium Miners ETF ( URNJ ) has underperformed the Sprott Physical Uranium Trust ( SRUUF ) in recent months.

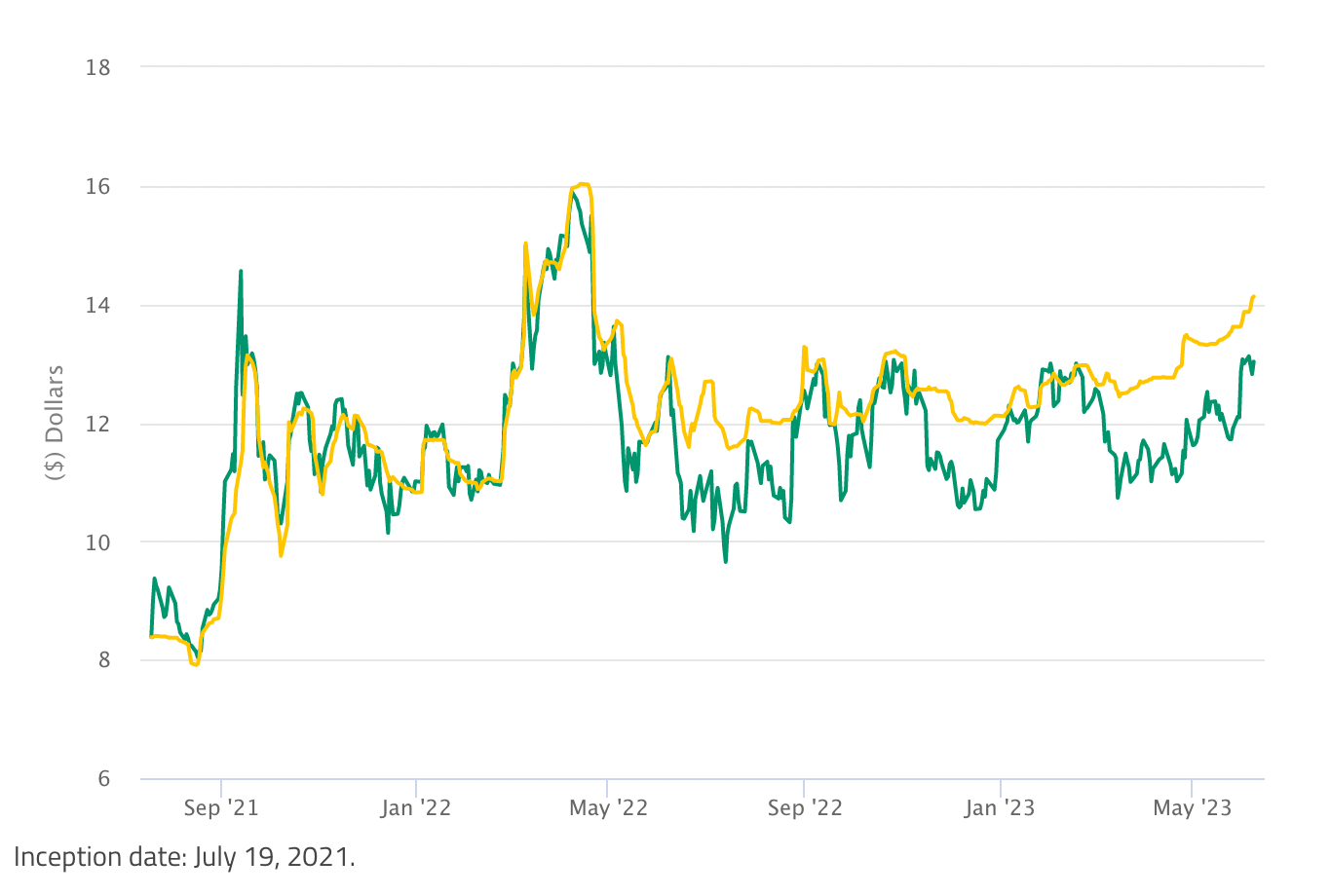

In turn, the Sprott Physical Uranium Trust (SPUT) has been trailing behind spot uranium prices, creating a divergence since last March. The chart below illustrates this discrepancy, with the yellow line representing the value of uranium backing each share in the trust (based on prevailing uranium spot prices), and the green line indicating its market value.

Market Price vs. Net Asset Value Since Inception for Sprott Physical Uranium Trust (sprott.com)

{kind=link}

During its early stages since inception in July 2021, when sentiment in the sector was optimistic, the trust frequently traded at a premium to its net asset value ((NAV)). However, more recently, it has been experiencing a significant discount, currently at approximately 8%.

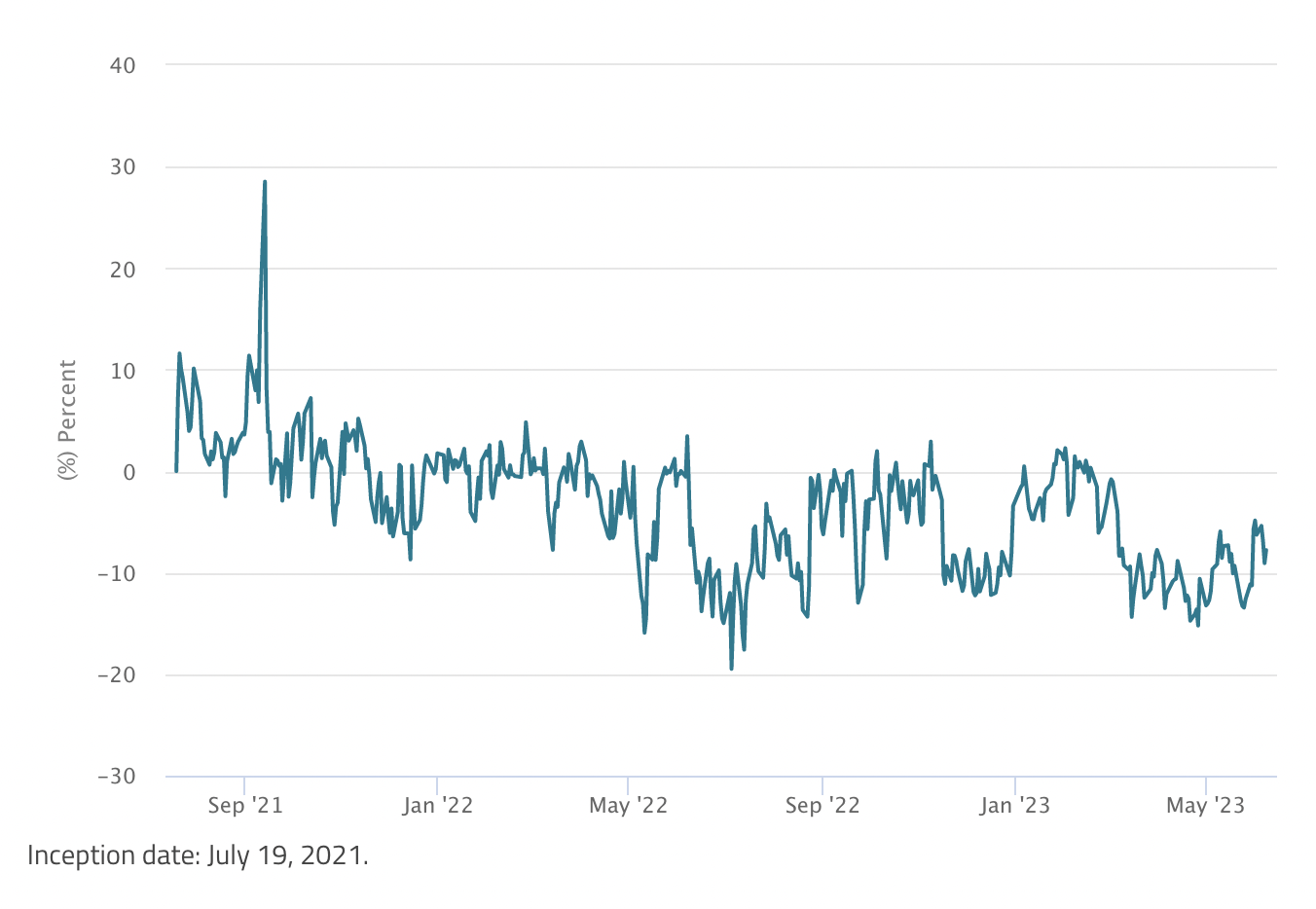

Historical Premium/Discount: Market Price to Net Asset Value (sprott.com)

{kind=link}

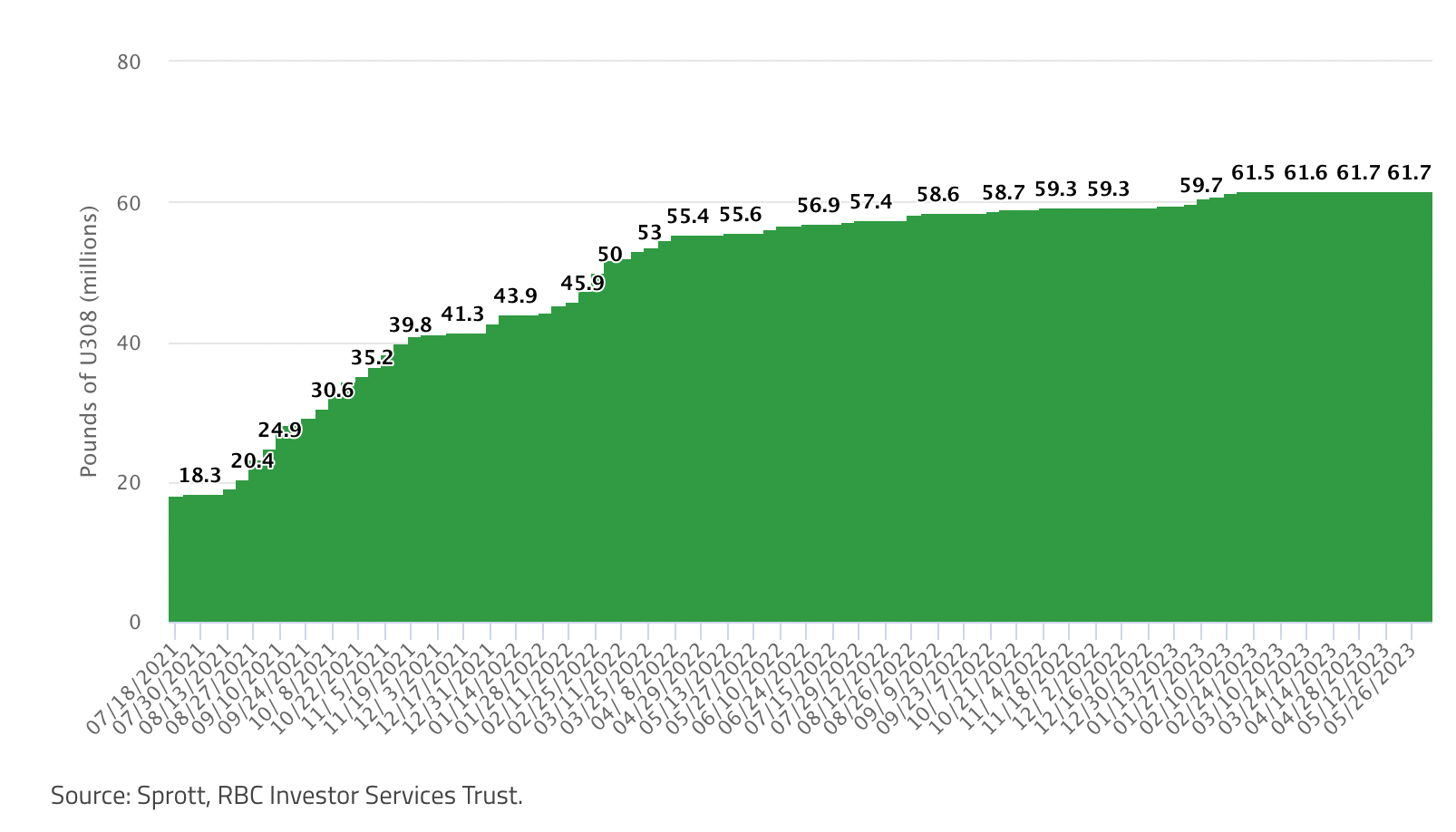

Due to the trust trading at a discount, it has halted its purchases of uranium in the spot market. As per the requirement of at least a 1% premium to NAV for issuing new shares, the at-the-market mechanism is currently inactive. The image below illustrates the rapid growth of the fund's uranium holdings after its inception, followed by a subsequent stagnation. Since March, there has been a complete cessation of new purchases.

{kind=link}

However, there has been an upward trend in spot prices recently. This divergence between the trust's market value and the rising spot prices may indicate a thinning spot market.

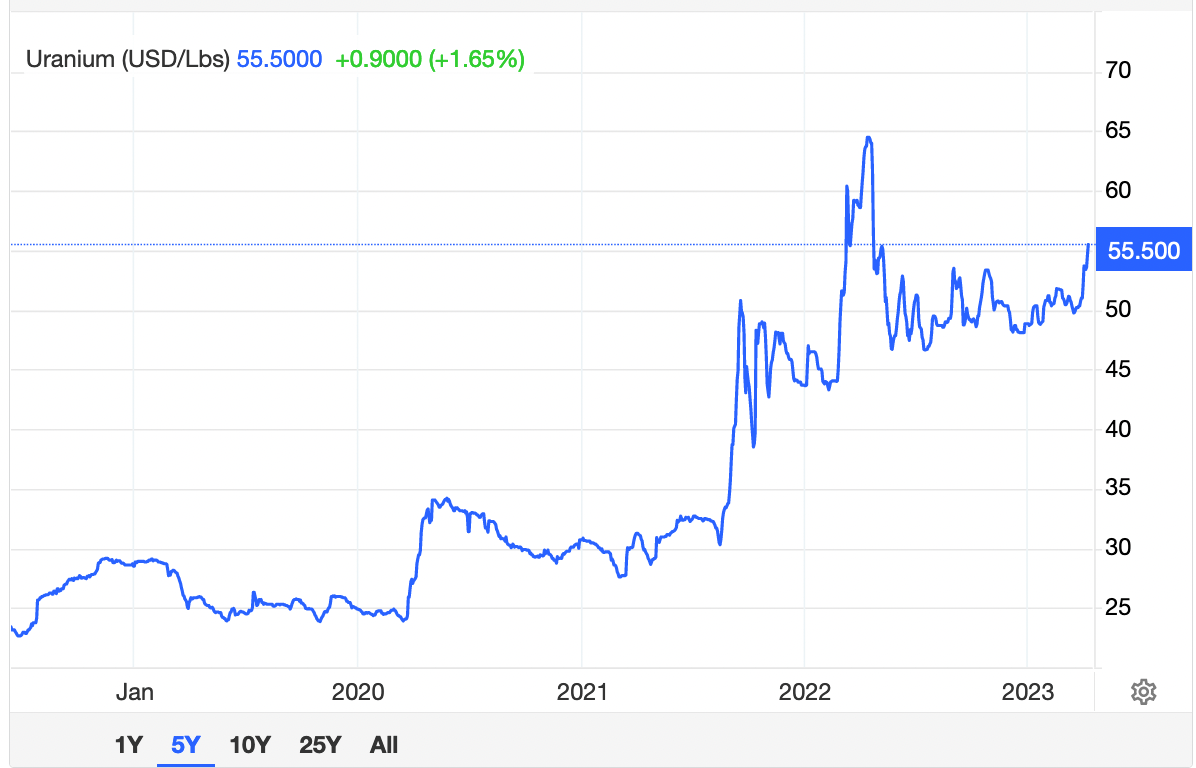

When we observe the price of uranium over the past few years, a pattern emerges where the price remains stagnant for extended periods and then experiences sudden spikes. It spiked in 2020 due to production declines caused by the COVID-19 pandemic. Another spike occurred in August 2021, shortly after the launch of the Sprott Physical Uranium Trust. A further spike followed in March 2022, triggered by Russia's invasion of Ukraine. Since then, uranium has been trading within the $45-$55 range. However, since April, there has been a steady climb in uranium prices, suggesting a breakout from its previous range. The recent upward movement in uranium prices was not triggered by any unexpected news. Neither was it influenced by the Sprott Physical Uranium Trust, since it has been inactive in spot market buying.

{kind=link}

The divergence could indicate that this latest price increase is driven by supply-side factors. After a decade of decreasing inventories resulting from primary production cuts, the uranium market may be shifting again towards being production-driven.

As I remarked in my last coverage of SPUT in February:

Predicting when secondary supplies will be close to exhausted is an incredibly hard job, because of the well-known opacity of the uranium market. This has always been the Achilles' heel of the uranium thesis.

Could the recent market activity indicate that secondary supplies are finally being depleted? If that's the case, we can expect spot and long-term prices to align more closely with the marginal cost of uranium supply.

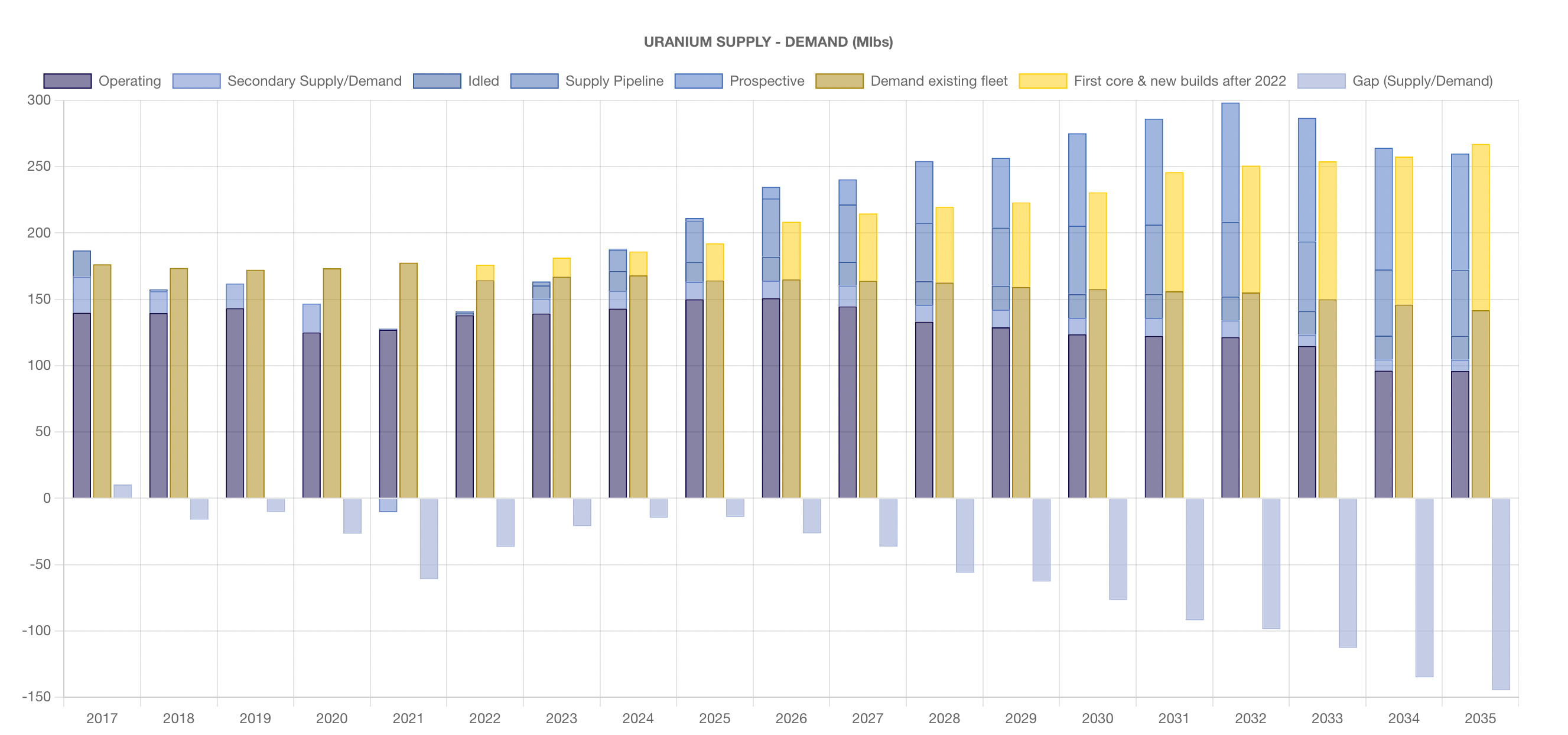

While global nuclear fleet demand is expected to remain relatively stable until 2024, UxC forecasts significant demand growth from 2025 to 2040, particularly from countries like India and China. This growth will require new production to come online. The following plot illustrates the historical and projected supply/demand balance up to 2035. Supply incorporates both primary and secondary sources, as well as idled capacity, ongoing development projects, and potential future projects. Demand includes both existing nuclear fleet demand and projected demand from reactors currently under construction or restarting, such as those in Japan. At the bottom of the figure, a widening supply/demand gap is visible, projected to exceed 100 million pounds in 2032. This gap does not consider new projects (both under development and prospective), but it does include idled capacity. Therefore, new projects are vital to bringing the market into equilibrium.

{kind=link}

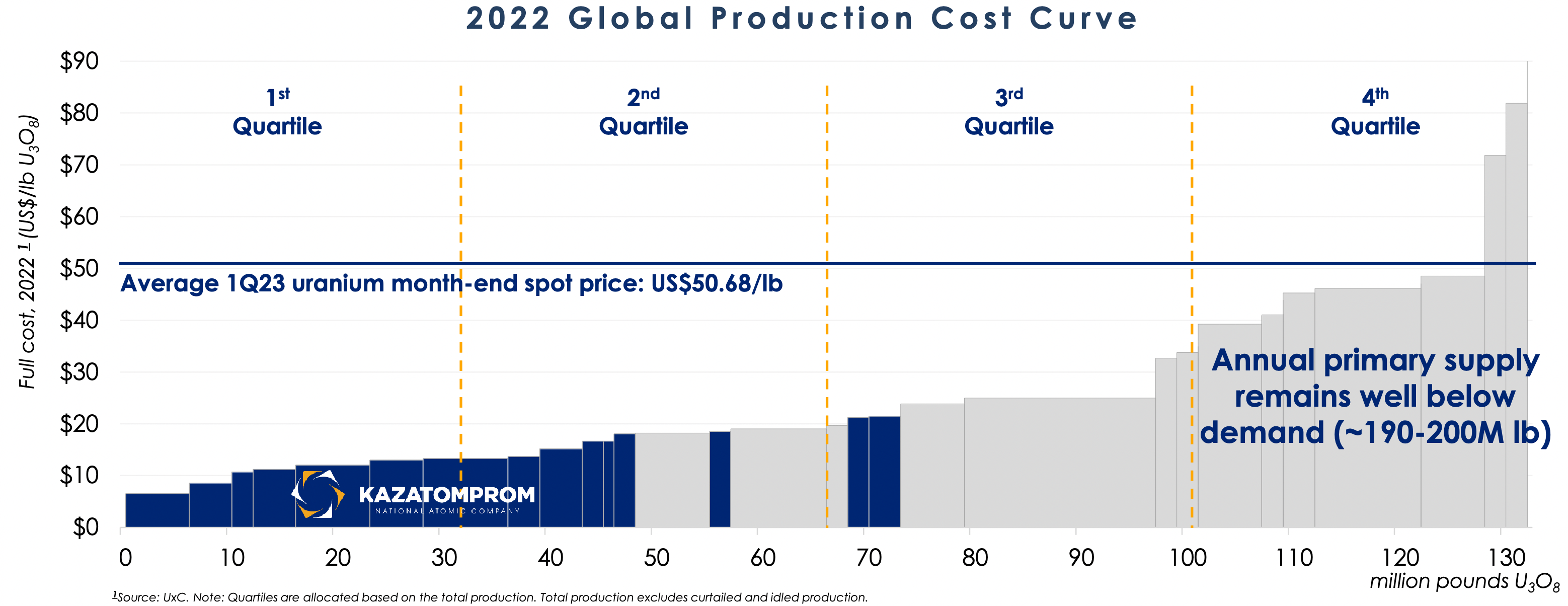

The following plot shows the uranium global production cost curve for 2022, taken from Kazatomprom Investor Handout . The marginal cost of new production is above $85 per pound, which is 50% above current spot prices. Considering persistent inflationary pressure and the difficulty in permitting and developing new assets, this estimate is probably going to rise over the next decade.

{kind=link}

As depicted in the previous chart, Kazatomprom possesses the largest uranium resources and the most cost-effective assets in the sector. However, it currently faces challenges such as inflationary pressures and logistical difficulties that may hinder its ability to ramp up production in response to a surge in uranium prices. While I still consider Kazatomprom a solid investment, its attractiveness has diminished since the start of the Russo-Ukrainian conflict due to a rising geopolitical discount.

This is why I believe that physical uranium offers the most favorable risk-to-reward ratio at the present time. However, there are risks to this thesis, such as a nuclear accident similar to Fukushima that could lead to a global shift away from nuclear power, as well as the potential for rising primary supply. Although new production could come online in the short to medium term, given the available spare capacity of companies like Cameco and Kazatomprom, I expect primary production to disappoint over the next decade, particularly considering the geographical concentration of uranium reserves and resources in politically challenged countries (apart for Canada and Australia, the largest uranium resources are concentrated in Russia, Kazakhstan, and Namibia). This exposes the uranium market to future disruptions and price volatility. A recent example is Namibia , the largest uranium producer in Africa, where the government is contemplating taking ownership stakes in new mining projects.

A possible recession in the latter half of 2023 in developed nations would not significantly impact uranium prices. Most uranium purchases are conducted through long-term contracts by utility companies, which are not as susceptible to short-term demand drivers as oil or coal. In fact, uranium has been the best-performing energy commodity over the past 12 months, despite concerns about a potential recession.

The main challenge remains predicting uranium inventories, particularly in relation to secondary sources of supply. It is important to recognize the risk of being locked into an illiquid investment with no yield, especially in the current inflationary environment. Nevertheless, there are several near-term catalysts that could indicate further upside potential for uranium prices:

- Improved market sentiment: If sentiment improves, potentially driven by bullish price action, SPUT could trade at a premium again, potentially sparking a new price rally.

- Entrance of new financial players: The anticipated entrance of new financial players in the physical uranium market is also expected to reduce available supply. Zuri-invest is set to launch a new investment vehicle in the form of an Actively Managed Certificate ((AMC)). Zuri-invest aimed to raise $100 million. It is still unclear how much they have raised, and how much of the amount raised has already been deployed. Their uranium AMC is not yet trading. The recent move in uranium prices could have been a result of their spot market activity, or could be speculation in anticipation of their entrance into the market.

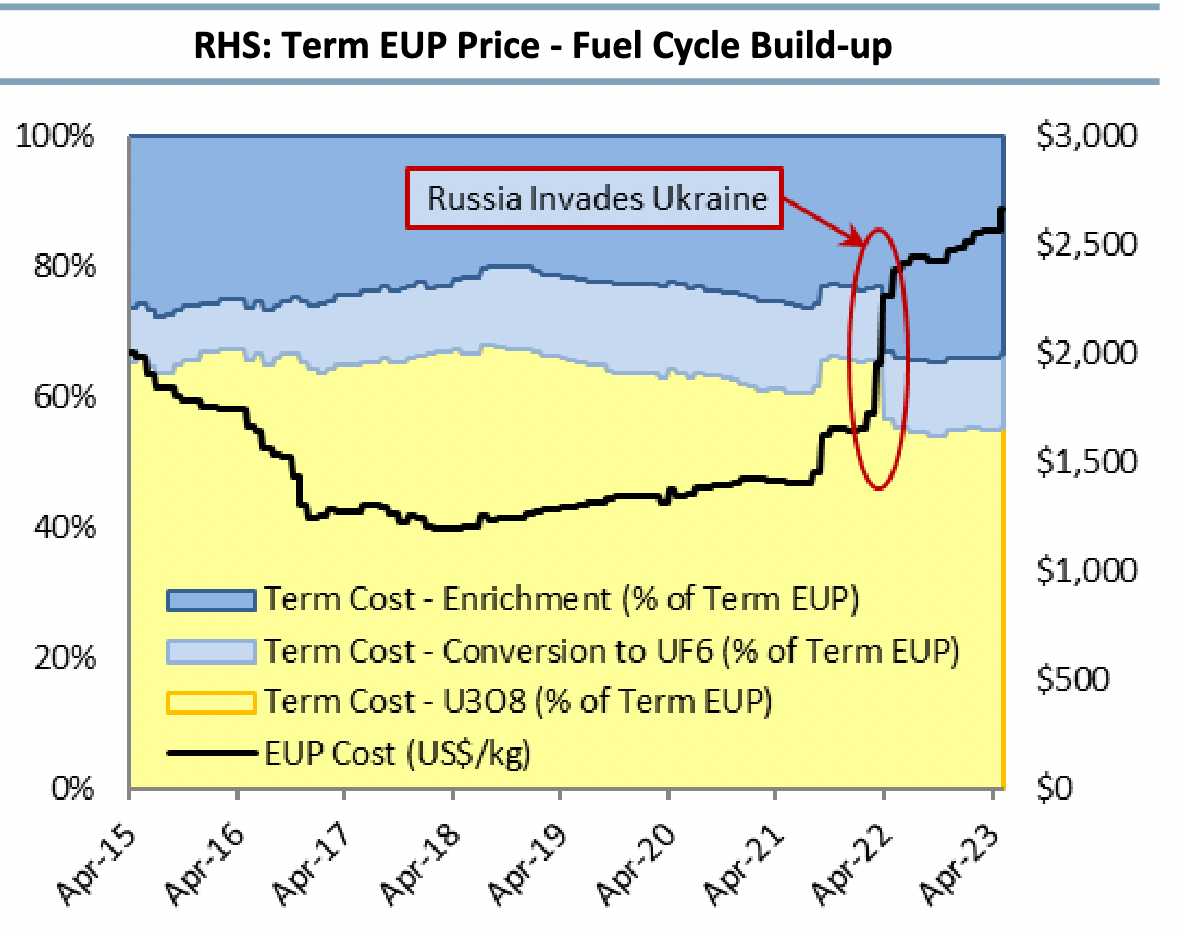

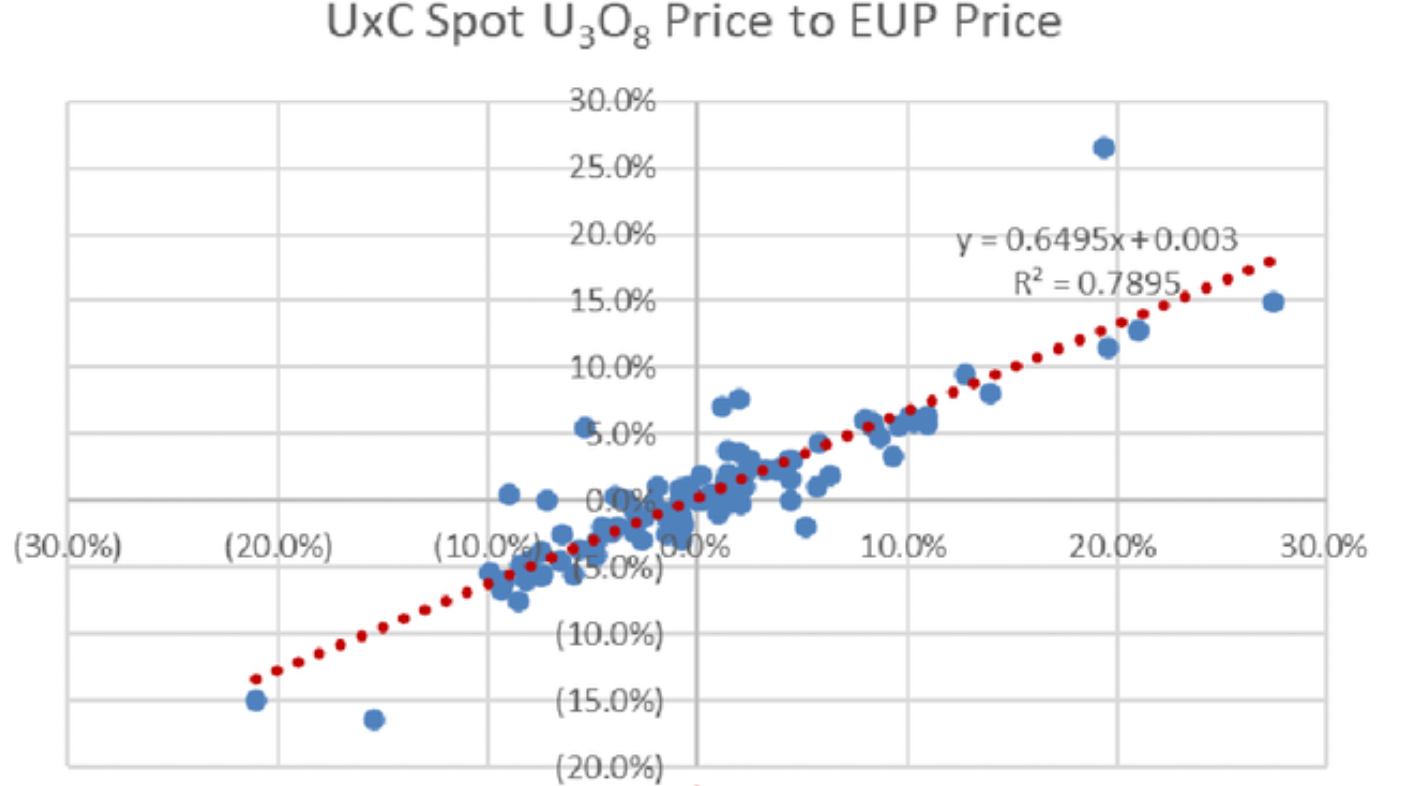

- Enrichers turning to overfeeding : Enrichers shifting from underfeeding to overfeeding represents an additional source of uranium demand. While the Russo-Ukrainian conflict did not lead to a sustained increase in uranium prices, prices for conversion and enrichment services have risen disproportionately due to Russia's significant share of global enrichment capacity (Russia represents only around 5% of uranium mining supply, but it accounts for around half of global capacity for enrichment services). In the short term, there is no strong correlation between price changes in different uranium products. However, in the long term, a significant correlation exists. One mechanism that contributes to this correlation is enrichers shifting from underfeeding to overfeeding.

Term enriched uranium product (EUP) price, made up of the sum of uranium, conversion and enrichment costs (UxC, Haywood Securities)

{kind=link}

Correlation between one-month changes in U3O8 prices and in EUP prices (UxC)

{kind=link}

In conclusion, as the mantra goes, inevitable does not mean imminent. Substantial appreciation in the long-term price of uranium is inevitable. However, it looks like that it might also be imminent. The Sprott Physical Uranium Trust offers a compelling opportunity to play the uranium thesis. The downside is limited by uranium already trading below the marginal cost of new production and the trust trading at a discount. On the upside, there are several factors supporting the potential for price growth, including rising mining costs, the possibility of geopolitical "black swan" events, strong demand from financial speculators, a growing nuclear fleet, enrichers shifting to overfeeding, and signs of a tightening spot market.

For further details see:

Sprott Physical Uranium: Ready For Lift-Off?