SPT - Sprout Social: Discounted Valuation Provides An Attractive Investment Opportunity

2023-05-16 05:00:46 ET

Summary

- Sprout Social operates in a $44 billion total serviceable market for social media management.

- Sprout is growing revenue almost twice as fast as the group average of its competitors at 32% projected YoY growth in CY24.

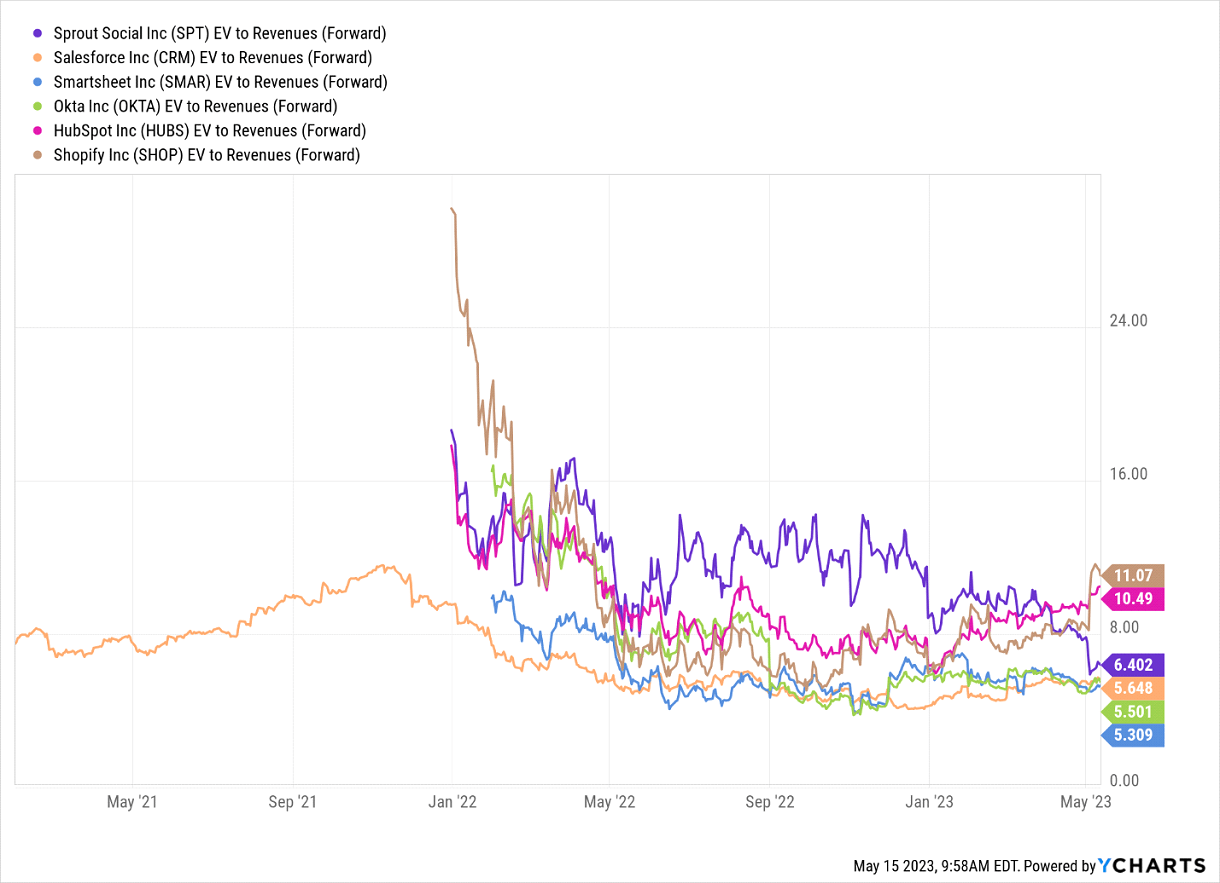

- Despite previously being considered a high-growth/high-multiple stock, the company's valuation has contracted to around 6x EV/CY24E Sales, which is in line with the overall SaaS peer group.

Investment Thesis

With a $44 billion total serviceable market [SAM] in social media management, Sprout Social, Inc. ( SPT ) is well-positioned to succeed and take advantage of changing consumer lifestyles. The company has been investing in its platform to cater to the needs of enterprises, which I believe will lead to higher average contract values [ACV] and retention rates. The stock trades at an attractive valuation, and hence I view the stock as a long-term buy at current levels.

{kind=link}

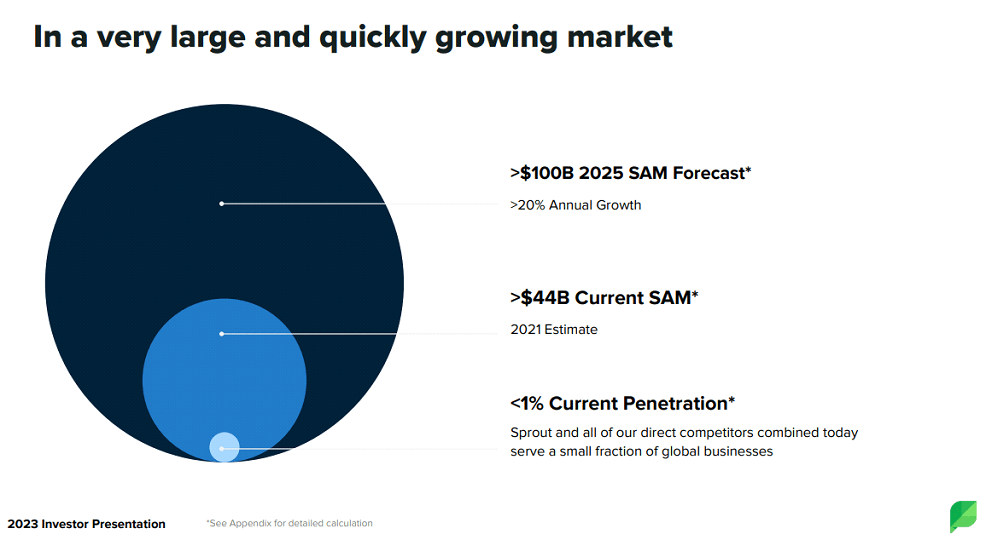

Large and Underpenetrated Opportunity

Sprout Social determines the potential market for social media management platforms based on the average spending level of customers in different segments, and they estimate a serviceable addressable market of $44 billion. Currently, Sprout and its competitors only serve 3-5% of this market, indicating that there is plenty of room for growth. The market is fragmented, with no clear dominant player. While Sprout, Khoros, and Sprinklr, Inc. ( CXM ) are the most comprehensive offerings available, Sprinklr and Khoros are more enterprise-focused, while Sprout is geared towards SMBs and is expanding to target larger businesses. Additionally, there are various point solutions available, such as HootSuite, which specialize in specific functions like publishing.

{kind=link}

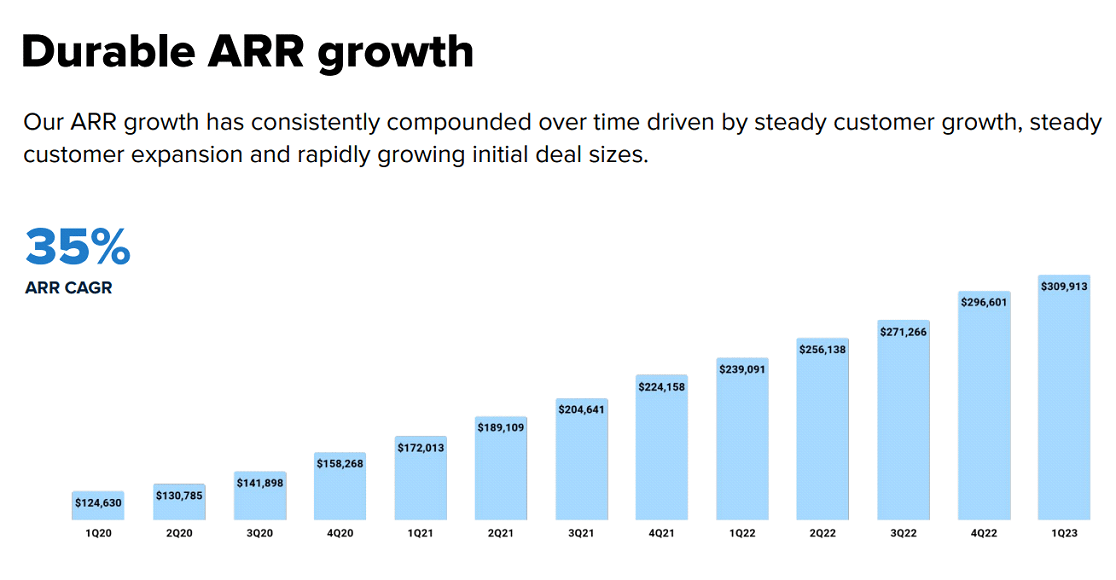

Sprout Social has experienced stable growth in its top-line over the last several quarters. The chart below illustrates this trend, where outside of a larger step up due to the Simply Measured acquisition in Q1 of 2023, growth has been very consistent. In the last reported quarter, the company grew ARR ~29% year-over-year at a scale of +$309 million.

{kind=link}

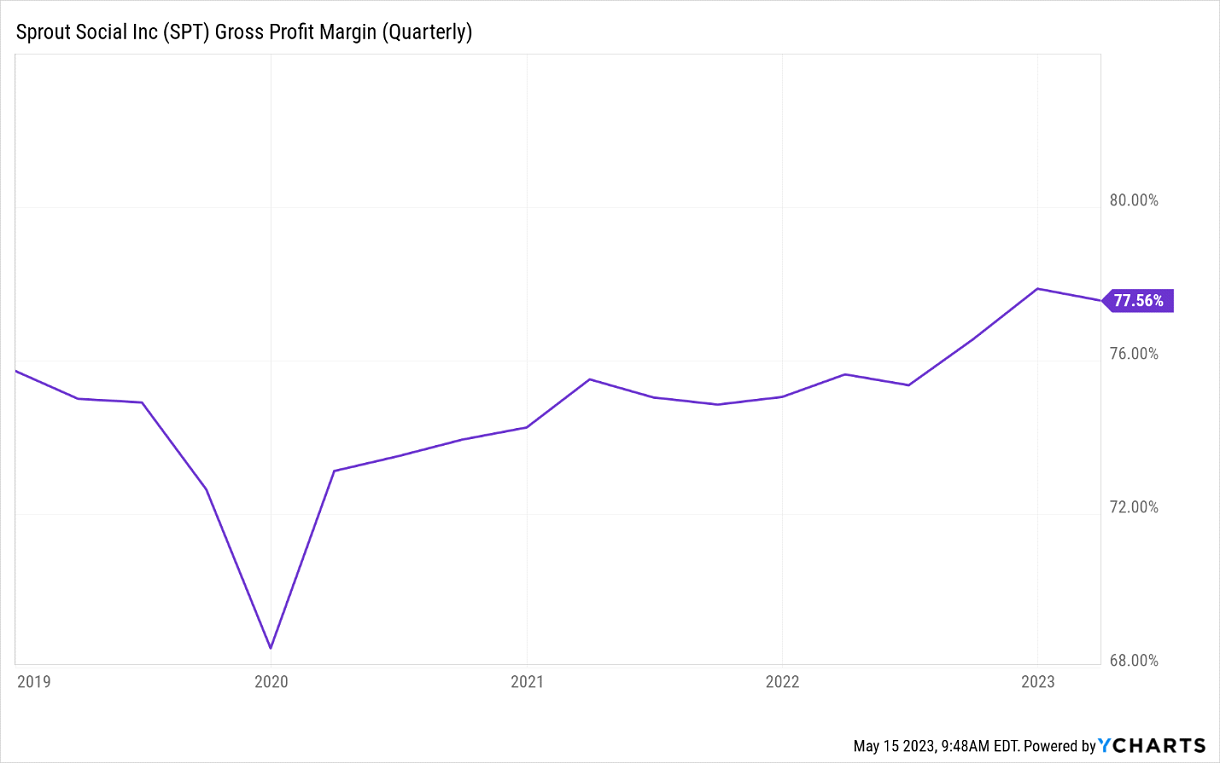

As a relatively new public company that has yet to reach its full potential scale, Sprout Social has room for improvement in its expense profile. Although the company's operating margin is lower than its peers, it has already seen some benefits in gross margins as it consolidates hosting costs for Simply Measured next year. I believe that Sprout has the potential to further improve its operating margin in the future.

{kind=link}

Valuation

Sprout Social has the ability to operate in a large and growing market opportunity with robust secular tailwinds behind it. Additionally, the investments made into premium product offerings, such as Social Listening and Premium Analytics, can serve to expand the current SAM more rapidly. It is rare to find an asset with a growth runway like this and a reasonable valuation in software. However, once dubbed a high growth/high multiple name, and hence could potentially see some short selling, the Sprout multiple has contracted to the point that I see as a relative floor. At ~6x EV/CY24E Sales, shares now trade in line with the overall SaaS peer group. This comes despite the fact that at 32% y/y growth in CY24, Sprout is growing revenue almost twice as fast as the group average of its comps. On top of this, the company is making strides to become more profitable, as evidenced by the guidance for 230bps of margin improvement this FY. I also see the current valuation level as the relative floor for the name, as I believe it would be logical for shares to trade at a premium to CXM, given better fundamentals.

{kind=link}

Risks

Although Sprout has the advantage of entering an untapped market and having a unique opportunity, the market is highly competitive and fragmented, which poses a risk. The market is still evolving, and the competitive landscape could change before Sprout fully scales its business. Furthermore, there is a possibility that larger players in adjacent markets may acquire social media management companies like Sprout, posing a potential threat. Sprout's success heavily relies on its integration with major social media platforms such as Facebook, Twitter, Instagram, LinkedIn, and Pinterest, and any negative changes in these relationships could negatively impact Sprout's ability to offer a comprehensive solution to its customers.

Investors' Takeaway

SPT operates in the social media management market with a $44 billion SAM. With only a 3-5% market penetration, there is significant growth potential as social networks continue to gain popularity for customer engagement. Sprout is investing in add-on features such as Social Listening and Premium Analytics to attract larger enterprise customers and drive higher average contract values and retention rates. The stock trades at an attractive valuation, and hence I view the stock as a long-term buy at current levels.

For further details see:

Sprout Social: Discounted Valuation Provides An Attractive Investment Opportunity