SPT - Sprout Social: Downgrading On Deceleration And Valuation

Summary

- Sprout Social's attractiveness as a rebound play has lessened as competing software companies now sport much lower valuations.

- Trading at ~8x forward revenue, Sprout Social is now at a premium to other growth SaaS peers.

- The challenging social media environment and reduction of ad budgets may directly impact Sprout Social, which provides tools for social media marketing managers.

- We have already seen deceleration creep into Sprout Social's results.

It's hard to emphasize this enough: now is the time to be combing through our portfolios, adding rebound stocks and re-emphasizing growth names while also removing stocks whose fundamentals have soured or valuations are no longer as appealing as before.

With this in mind, I've reviewed Sprout Social's ( SPT ) merit in my portfolio and have decided to trim the position. Over the past twelve months, this social media management software stock is down nearly 30% - technically putting it in a bear market, but much better than other SaaS plays. At the same time, I'm worried about how Sprout Social will withstand current macro headwinds which are especially harsh to the Internet advertising/social media ecosystem.

Now neutral on Sprout Social, I view the company as a fairly balanced mix of positives and negatives.

On the bright side for this name:

- Sprout Social plays in a >$50 billion TAM, driven by still-nascent business adoption of social media. Many companies, especially SMB-type clients, are still figuring out social media for the first time, meaning that the majority of Sprout Social's market is greenfield. The company estimates its current TAM at >$50 billion.

- Nearly pure recurring revenue. Nearly 100% of Sprout Social's revenue base is SaaS, with its customers paying recurring fees to use Sprout Social's post schedule, monitoring, and analytics tools.

- Platform agnostic and technology that is one-size-fits-all. Sprout Social has expertise across all the major social media platforms, including Facebook ( META ), Instagram, Twitter, Pinterest ( PINS ), Snap ( SNAP ), and even TikTok. Sprout Social's technology also uses a single code base that is applicable to all clients, meaning there is no need to custom-configure its solutions for any particular client.

On the other hand, however, I'm increasingly worried about how the macro environment will impact Sprout Social's underlying business. Sprout Social, for investors who are unfamiliar with its product, is a tool primarily meant for social media managers to curate, upload, and run analytics on their social media advertising and content. Needless to say, with most companies expecting a recession in the near term, discretionary spend including advertising has been pulled back. With lower ad budgets in circulation, this may mean layoffs among the professionals who manage social media advertising - directly striking at the heart of Sprout Social's user base.

Longer term, I still think Sprout Social will capitalize on secular tailwinds favoring the social media landscape: this being said, I don't think now is the right time to buy or add to an existing position, due to Sprout Social's valuation. At current share prices near $53, Sprout Social trades at a market cap of $2.92 billion. After we net off the $182.1 million of cash (unencumbered of debt) on Sprout Social's most recent balance sheet, the company's resulting enterprise value is $2.74 billion.

Meanwhile, for FY23, Wall Street analysts are expecting Sprout Social to generate $328.9 million in revenue, representing 29% y/y growth. Considering Sprout Social decelerated quite significantly to a low-30s growth rate this quarter and with a potentially darkened outlook for social media and advertising in 2023, I don't consider these estimates "de-risked." Nevertheless, taking Wall Street consensus at face value, Sprout Social trades at 8.3x EV/FY23 revenue. Note that most SaaS companies in the 20-30% growth range have re-rated to revenue multiples in the 4-5x range.

The bottom line here: to me, it's best to adopt a "watch and wait" stance on Sprout Social; this is not the best rebound stock to play in 2023.

Q3 download

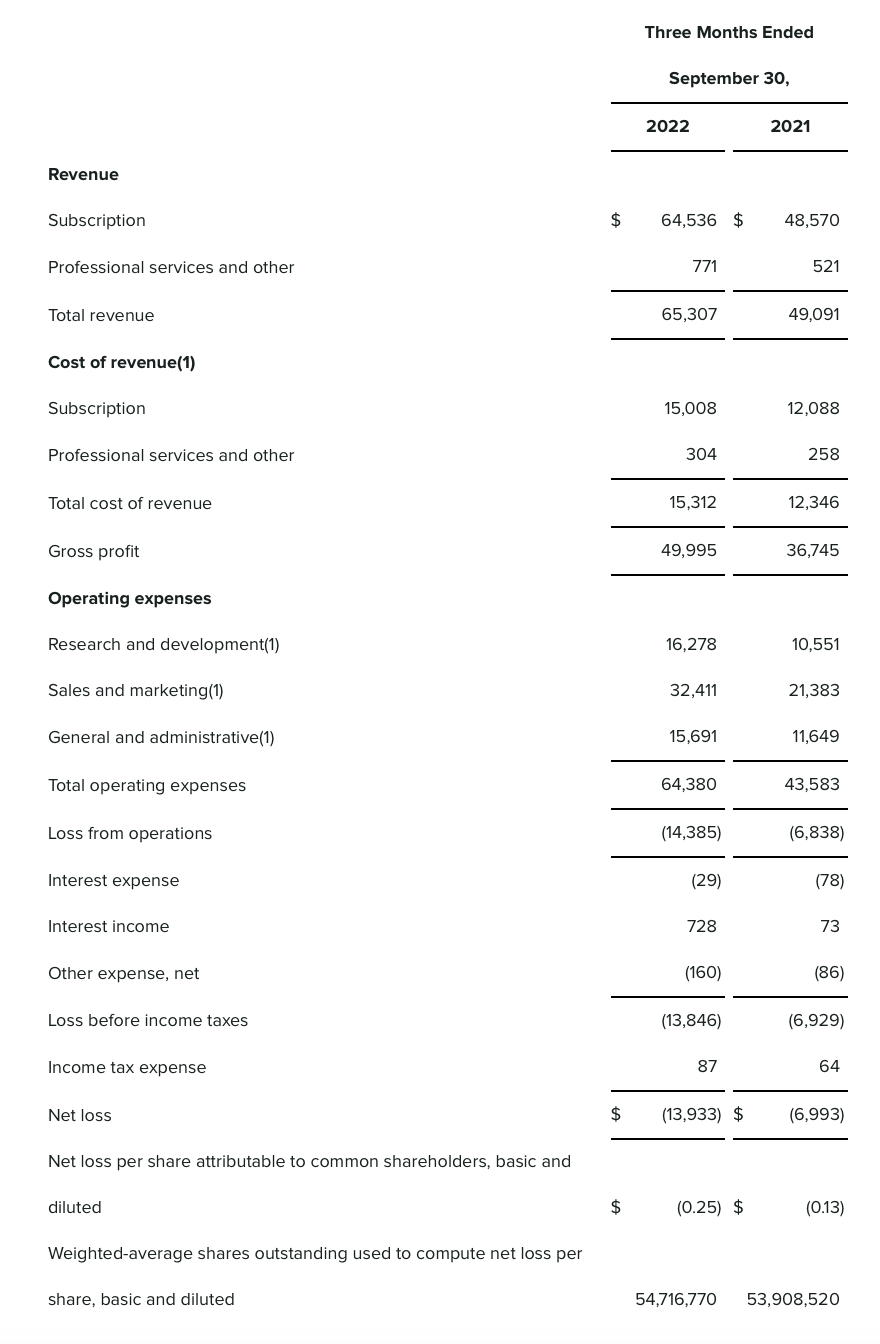

Let's now cover some of the highlights from Sprout Social's most recent quarter. The Q3 earnings summary is shown below:

Sprout Social Q3 results (Sprout Social Q3 earnings release)

{kind=link}

Sprout Social's revenue grew 33% y/y in Q3 to $65.3 million. This barely beat Wall Street's expectations of $65.0 million (+32% y/y), and also decelerated four points versus 37% y/y growth in Q2.

The company noted that the macro environment has caused "strain" on the business. In particular, the deal process has slowed (in terms of both new customer acquisition as well as upsells) for smaller customers rather than for enterprise clients.

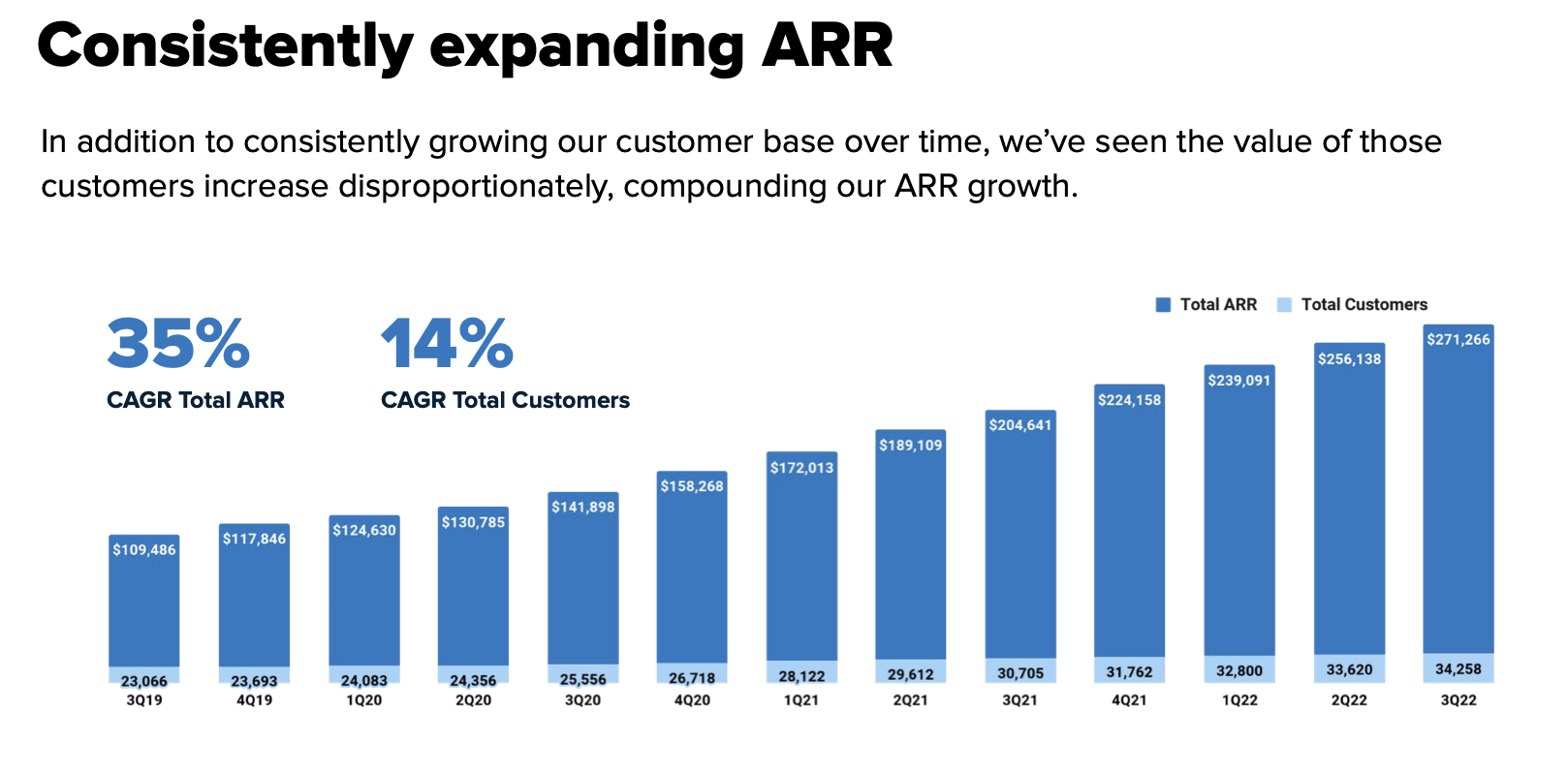

ARR, meanwhile, also grew 33% y/y to $271.3 million, decelerating from 35% y/y ARR growth in Q2.

Sprout Social ARR trends (Sprout Social Q3 earnings deck)

{kind=link}

There is a potential upside catalyst here: Sprout Social is planning on increasing the prices of all its subscriptions, capitalizing on the current inflationary environment to pass on costs to clients.

Per CEO Justyn Howard's remarks on the Q3 earnings call:

The last time we made meaningful pricing changes was in 2017, which creates more than 500 material new product enhancements, including the vast majority of features, workflow, networks and integrations at core Sprout today.

As we look to realign the entry price to Sprout to match the most productive parts of our business, we've made 2 changes. First, effective this week, we've changed the pricing that new customers see including meaningful price increases across all of our subscription tiers and the addition of an enterprise plan, which includes our premium offerings.

Second, starting in Q4, we will begin making modest price increases for our existing customers for the first time, many of which are paying the same price they were paying a decade ago. By aligning our pricing, product, go-to-market and customer success strategies around the most productive customers and potential customers, we believe we have the opportunity to accelerate our brand competitive and category leadership as well as our growth."

Sprout Social's lowest-tier paid plan, in particular, saw a 2x price jump. The company expects these changes to produce an acceleration in ARR growth rates in the near term. We will caution, however, that the impact to churn will be unknown: especially as Sprout Social cited weakness in the lower end of its customer base, price increases that are also aimed at the lower-tier products may hurt the company's traction in the SMB base even further.

From a profitability standpoint, Sprout Social continued to hover around breakeven, with pro forma operating margins of -2% in the quarter slightly improving from -3% in the year-ago quarter. The company expects price increases to have a net-positive impact on margins in FY23, and has re-committed to its target of delivering between 100-300bps of operating margin expansion each year.

Key takeaways

Given a souring macroeconomic backdrop (with a potential partial offset in price increases) as well as a rich valuation, I'm no longer as keen on Sprout Social as I was in the past. Move to the sidelines here and focus your investments elsewhere.

For further details see:

Sprout Social: Downgrading On Deceleration And Valuation