SPT - Sprout Social: Hanging Tight But Upside Is Capped (Ratings Upgrade)

2023-11-06 16:53:36 ET

Summary

- Sprout Social's stock has dropped 20% this year due to underperformance and compression in valuation multiples.

- The company's Q3 earnings showed a re-acceleration in top-line growth and strong performance in ARR adds.

- Sprout Social addresses a large TAM and has high-margin recurring revenue, but the macro landscape and valuation are concerns.

Sharp market moves over the past week have all been about interest rates (or more specifically, the hope that they won't rise again). In light of waning interest rate fears, however, investors still have to be incredibly cognizant of valuations - which can't sit too high when risk-free yields are still hovering around 5%.

With this in mind, we should keep a close eye on Sprout Social, Inc. ( SPT ), the social media management stock that has taken a ~20% tumble this year. Yes, the company has underperformed peers, but its macro landscape and growth rates have tightened as well, all of which have contributed to a compression in its valuation multiples.

However, another mantra I champion is that we must constantly be watching our positions and be willing to update our theses especially in a volatile market. I last wrote a bearish opinion on Sprout Social in September. Since then, the company's stock has dropped a further ~10% while also releasing Q3 earnings that demonstrated a re-acceleration in top-line growth. With these two factors in mind, I'm upgrading my viewpoint on Sprout Social back up to neutral.

In the mid-to-low $40s, I see a relatively balanced bull and bear case for Sprout Social. On the bright side for this company:

- Sprout Social addresses a TAM of over $50 billion, driven by still-nascent business adoption of social media. Many companies, especially SMB-type clients, are still figuring out social media for the first time, meaning that the majority of Sprout Social's market is greenfield. The company estimates its current TAM at over $50 billion. Its growth rates of over 30% y/y demonstrate the relative earliness of its market.

- High margin recurring revenue- Nearly 100% of Sprout Social's revenue base is SaaS, with its customers paying recurring fees to use Sprout Social's post schedule, monitoring, and analytics tools. This revenue stream also comes at very high gross margins, giving Sprout Social the formula for a profitable software business once it reaches scale.

On the flip side, however, we should be careful of the following:

- Sprout Social is purpose-built for social media managers, and the current macro landscape is unfavorable for this niche. Companies are slashing their sales and marketing budgets - both for advertising spend as well as the G&A headcount that supports it. While social media management as a core company function will continue to see secular tailwinds, we'll likely see retrenchment as companies tighten their belts.

Valuation is another watchlist item for Sprout Social. At current share prices near $45, the stock trades at a market cap of $2.49 billion. After we net off the $121.4 million of cash and $75 million of drawn revolving debt on Sprout Social's most recent balance sheet, the company's resulting enterprise value is $2.44 billion.

Meanwhile, for next fiscal year FY24, Wall Street analysts are expecting Sprout Social to generate $424.5 million in revenue (+29% y/y). Now, we note that this estimate may prove aggressive considering Sprout Social's growth had already decelerated to a 29% y/y pace back in Q2 - and considering tight macro conditions, I don't find it likely that growth rates will sustain at those rates through next year. Nevertheless, taking consensus estimates at face value, Sprout Social trades at 5.7x EV/FY24 revenue.

Now, that's hardly expensive - as the stock certainly traded, along with many other 30-40% growth peers, at double-digit multiples of revenue during the heyday of the pandemic. But neither does that multiple scream value with room to rebound, which is why I'm more content to stay on the sidelines here and retain my neutral rating.

The bottom line here: keep Sprout Social on your watch list if the stock keeps falling. I'd be a willing, unhesitant buyer here if the stock dropped to $37 (representing a 4.8x EV/FY24 revenue multiple), but until then, steer clear.

Q3 download

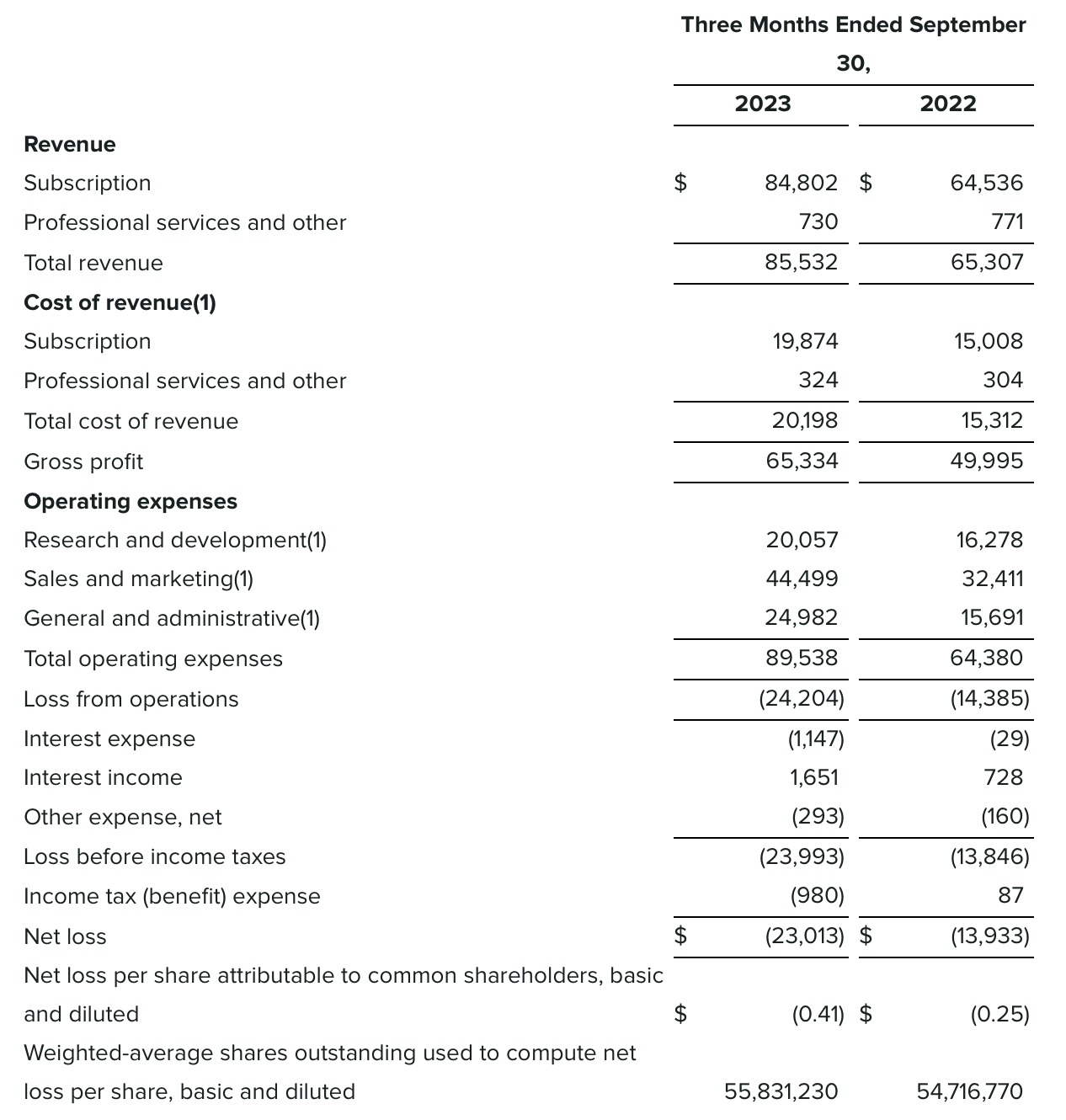

Let's now cover Sprout Social's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

Sprout Social Q3 results (Sprout Social Q3 earnings release)

{kind=link}

Sprout Social's revenue grew 31% y/y to $85.5 million in the quarter, beating Wall Street's expectations of $84.2 million (+29% y/y) by a two-point margin. Growth also re-accelerated to 31% y/y after falling to 29% y/y in Q2 (and it had been at 31% y/y in Q1).

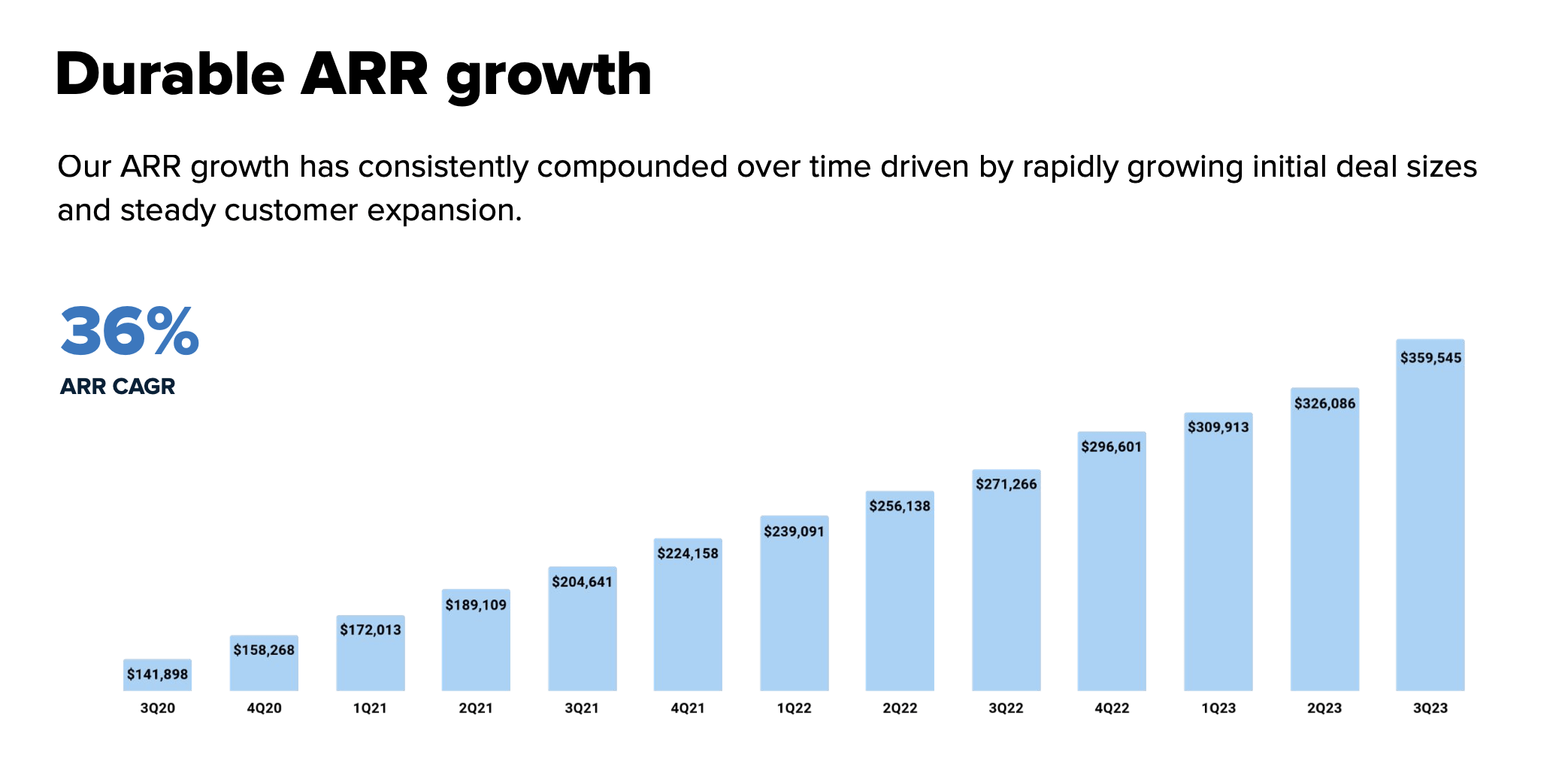

Sprout Social ARR trends (Sprout Social Q3 earnings release)

{kind=link}

Similarly, the company showed strong performance in ARR adds, as shown in the chart above. On a nominal basis the company added a net $33.4 million to its ARR in the third quarter, which is a dollar-based record for the company. ARR also grew at a 33% y/y clip, both faster than revenue growth at 31% y/y as well as outpacing Q2's 27% y/y ARR growth clip. Again, the strength of Sprout Social's top line results in Q3 is the bulk of what drove my rating upgrade to neutral.

The company noted that broadening its partner ecosystem has been tremendously beneficial to ARR expansion. In particular in Q3, the company noted its integration with Salesforce - many customers onboarded Salesforce Service Cloud in conjunction with Sprout Social to address customer queries via social media. The company is expecting another ARR record for net adds in Q4.

Note that the company did complete a very small tuck-in acquisition of a rival platform called Tagger in Q3. However, Tagger generated just $5 million of revenue in the trailing five months, so this is not the primary driver behind Sprout Social's ARR or revenue growth acceleration this quarter.

Here's helpful anecdotal commentary on the go-to-market landscape from CEO Justyn Howard's prepared remarks on the Q3 earnings call, particularly on enterprise adoption:

The combination of our ongoing breakout upmarket, rising utility for our software, strengthening multi-product strategy, and our entrance in influencer marketing have Sprout at the starting line of our next great growth chapter. During Q3, we saw continued record new business ACVs, and total ACV growth at a record 40% year-over-year. This was driven by 49% year-over-year growth in our 50K plus ARR customers, an acceleration in our premium module attach rates, and a further acceleration in our enterprise business [...]

Another key component of our current and future execution is our platform strategy. Only 6% of our customer base has adopted two or more premium products. And we see massive potential to unify what should be standard social capabilities for all global businesses. Total premium module attach rates were even stronger than our impressive Q2, increasing of more than 27%. We were also excited to surpass $100 million in premium module ARR this quarter."

From a profitability standpoint, Sprout Social notched an effectively breakeven -1% pro forma operating margin (which is relatively impressive for a company at its scale and at an over 30% growth pace), versus a -2% margin in the year-ago Q2.

Key takeaways

With its revival in revenue and ARR growth rates in Q3, plus a slightly cheaper stock, I'm more sanguine on Sprout Social's prospects through the end of this year and into early next year - but given its valuation is still sitting close to ~6x revenue, I don't see much upside for this stock either. Keep this on your watch list, but don't rush in to buy just yet.

For further details see:

Sprout Social: Hanging Tight, But Upside Is Capped (Ratings Upgrade)