SPT - Sprout Social: Remain Buy Rated As Operating Metrics Remain Sound

2023-11-17 06:20:31 ET

Summary

- Sprout Social's Q3 revenue surpassed estimates, driven by subscription revenue and non-GAAP gross profit.

- The company saw growth in larger customers, increasing aggregate ACV and ARR significantly.

- The partnership with Salesforce presents a significant opportunity for Sprout Social to upsell its products and expand its market.

Overview

My recommendation for Sprout Social (SPT) is a buy rating, as SPT continues to see success in upselling and penetrating the upmarket. The partnership with Salesforce is also developing nicely, which should provide SPT with a large customer base to extend its growth runway. Note that I previously rated buy rating for SPT as I believed investors were focused on the wrong metric. Investors would be able to better assess SPT financials as it churns away the non-core subs.

Recent results & updates

SPT's 3Q23 quarter revenue of $85.5 million surpassed consensus estimates of $84.2 million, mostly driven by the $84.8 million in subscription revenue. The $66.8 million in non-GAAP gross profit is also above expectations of $65.4 million. Growth in non-GAAP gross profit led to an improvement in non-GAAP EBIT to -$0.6 million, which again beat consensus estimate of -$2.4 million.

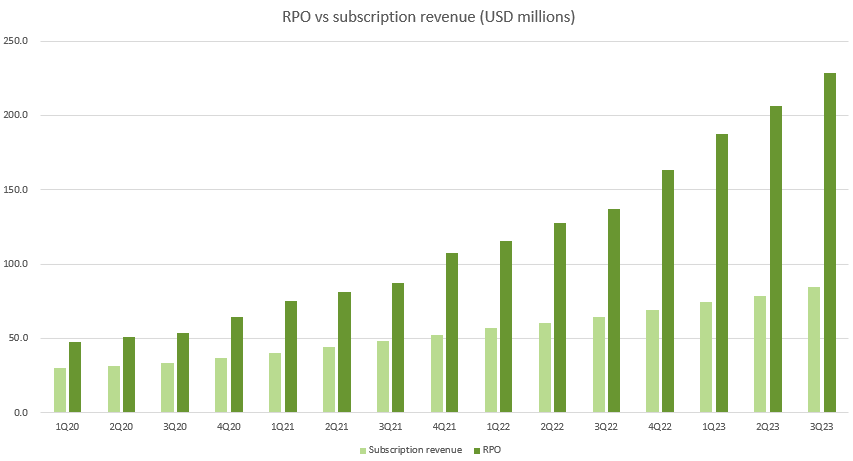

In the quarter, SPT continues to shrink its customer count by 5.5% annually and 2.3% sequentially, resulting in a net decrease of 776 customers. As I have noted previously, these are non-core customer churns, which is expected and should not raise any huge alarms. Performance in other operating metrics continues to paint a strong picture of the business. Particularly, SPT's upmarket focus was evident in their large-customer metrics for 3Q, with the number of customers with annual recurring revenues [ARR] of $10,000 or more increasing by 32.7%, which equates to 720 net new adds, bringing the total to 8,111. Also, the number of customers with an ARR of $50,000 or more increased by 48.5%, which equates to 133 net new adds bringing the total to 1,252. These performances are even more fantastic when compared to recent history. With these adds, SPT saw its biggest annual increase in aggregate ACV (average contract value) over the preceding 8 quarters, with a growth rate of 40.2% y/y, bringing the total to $11,102. Consequently, SPT ARR increased by $359.5 million, or 32.5%, a significant increase above the 27.3% growth seen in 2Q23. As a result of this robust performance, SPT's current RPO grew to $167 million, a big increase of 51%, and total RPO increased by 67.1% to $228.7 million. The implication is simple: the higher the RPO, the better the revenue outlook. If we look at SPT historical subscription revenue and RPO relations, they tend to move in the same direction.

{kind=link}

Another growth driver worth noting is SPT's consistent success with premium module cross-sell and up-sell initiatives. As of 3Q23, premium module ARR has topped $100 million, and attach rates are over 27%. Since only 6% of SPT's customer base has adopted two or more premium modules, I believe SPT could expand ARPU further. Given that the current success in going upmarket is largely driven by core premium modules rather than the recently acquired Tagger, the opportunity set is certainly huge. To give a sense of the difference in magnitude, according to the 3Q23 call, Tagger has 3 to 4x the current SPT ACV.

"With 3x to 4x current Sprout ACVs and a meaningful opportunity to further differentiate the customer value proposition, we believe Tagger has potential to be a greater than $100 million ARR business by 2028." from: 3Q2023 earnings call

Lastly, the growth outlook for Social Studio remains fantastic as SPT is expanding their partnership and integrations with Salesforce. The most recent development is that SPT is already landing Salesforce customers who were not on Social Studio. I think the possibility extends far beyond merely landing on Salesforce's Social Studio platform, given Salesforce's vast client base. As I've already indicated, SPT has incredible cross-selling and up-market penetration capabilities. Therefore, the collaboration with Salesforce gives SPT a chance at a market beyond just the Social Studio converts. Again, to give a sense of the magnitude, Salesforce has more than 150 thousand customers worldwide, which is more than 5x the size of SPT.

Valuation and risk

Author's valuation model

According to my model, SPT is valued $64.24, representing a 20% increase. My expected upside is now lower than my previous model given the increase in share price, but I think 20% is still quite attractive. My target price is based on 30% growth, 100bps lower than my previous assumption as I realign expectations with management's guidance (management guided to ~$331 million for FY23 revenue). I have my belief that growth could accelerate by more than 30% as the churn impact from non-core customers should continue to taper, and the positive impacts from upselling and other growth should further outweigh them.

From a valuation perspective, SPT forward revenue multiple has increased by 1x since my last post, indicating that the market is gradually aligning with my view on SPT. I am assuming valuation will stay at this 7x since SPT growth outlook remains positive.

{kind=link}

For risk, I think the major focus is still on the customer churn. While these are non-core churns that I expect to taper off eventually, steep acceleration in customer churn might hurt the headline figures much more than I expect. Recall that in the previous quarter, the stock price dropped by a ton as the declining customer count spooked investors. This might happen again if the churn accelerates.

Summary

My buy rating on SPT remains as 3Q23 demonstrated strong operational metrics. While a decline in customer count is notable, it primarily reflects non-core customer churn, not posing significant concern. Encouragingly, SPT saw a substantial rise in larger customers' numbers, elevating aggregate ACV and ARR significantly. The partnership with Salesforce is one to look out for as I believe it represents a massive opportunity for SPT to upsell its products.

For further details see:

Sprout Social: Remain Buy Rated As Operating Metrics Remain Sound