GO - Sprouts: A Potential Bulletproof Business Model For The Next Recession

2023-04-28 12:27:21 ET

Summary

- The U.S. economy is on shaky ground; now is the time to position for the upcoming recession.

- Sprouts Farmers Market is a well-run, highly profitable company in the most stable industry out there.

- The valuation at 9.8x free cash flow is attractive for long-term buyers.

- The company continues to buy back shares.

Recession : It's a word that's been on the minds of investors for the last few months.

While there's been quite a bit of debate recently about the topic and whether or not the U.S. will see two consecutive quarters of negative GDP growth, one thing is for sure: it pays to be prepared.

Today, we'll examine whether or not we think the U.S. is headed for a recession. And, just in case the worst comes to pass, we'll examine our favorite stock pick to weather the economic turbulence. Let's dive in.

Is A Recession Coming?

As we just mentioned, there's been quite a robust back and forth among economists, political commentators, traders and financial professionals as of late about whether or not the U.S. will be entering a recession in the second half of this year.

Our opinion? On balance, we think it's likely that the U.S. will enter a recession sometime in the next 12 months. Why? Because the most reliable leading economic indicators that predict GDP with a high level of accuracy are weak and continue to deteriorate.

{kind=link}

Let's start with the ISM Reports on Business. The Manufacturing PMI came in at 46.3, which was a step down from its previous reading of 47.7. If you're unfamiliar with the PMIs, any score above 50 signals economic expansion, and any score below 50 signals economic contraction. The Manufacturing PMI has been highly accurate (85%+ accuracy) over the last 70+ years in predicting GDP with a 6 to 12-month time lag, which makes it valuable now in trying to figure out what's going to happen next. As both the reading AND rate of change are negative, it's very tough to get bullish on GDP, or the market in general.

What about the NMI, also known as the Non-Manufacturing PMI? It's a mixed bag. While the reading is still technically expansionary, the rate of change is negative signaling slowing growth, best case.

The Yield Curve (highly negative), Consumer Sentiment, and Housing Permits - and by extension, bank's propensity to lend - are all also negative and flashing warning signals.

Net net, it seems likely that a recession is on the horizon.

How To Position

So, if conditions are contractionary, what is the best way to position?

Conventional trading wisdom states that in a period where poor economic performance is expected, you should look to be long defensive names and short cyclical ones. Typically, these definitions are broken down by sector, like so:

| Cyclicals |

| Defensives |

| Consumer Discretionary |

| Consumer Staples |

| Energy |

| Telecoms |

| Industrials |

| Healthcare |

| Materials |

| Utilities |

| Financials |

| Real Estate |

| Technology |

While the table above is a great starting point, it isn't a perfect way of separating out companies that are sensitive to the business cycle. There will be communications stocks whose earnings are highly sensitive to GDP, and industrial companies whose earnings are completely uncorrelated with the broader macroeconomic / business environment.

In our view, it really comes down to elasticity of product. In economics, elasticity just means the price sensitivity that customers have towards a certain product, good or service. For example, Lululemon yoga pants are an elastic good (no pun intended). When you're feeling wealthy, you'll buy some. When you're feeling stretched, they're the first thing to go. This is the opposite of inelastic goods. Groceries, rent, and gas for your car are expenses that are almost impossible to remove from any budget.

Thus, in a recession, we should be looking for the best companies, in the most stable industries, who sell the most inelastic products.

Enter our favorite pick.

Sprouts Farmers Market

Sprouts ( SFM ) checks all of the boxes we've been looking for so far. Recession? Check. Defensive industry? Check. Inelastic goods? Check. No matter how bad things get, people have to eat. Plus, in downturns, people tend to eat out at restaurants less and buy ingredients more, which is an actual business boon to grocery retailers around the country.

But why Sprouts? There are lots of public grocery store chains, like Kroger ( KR ), Albertsons ( ACI ), Grocery Outlet ( GO ), and more.

In short, we think they're the best operator in the space. Let's take a quick look at their performance.

{kind=link}

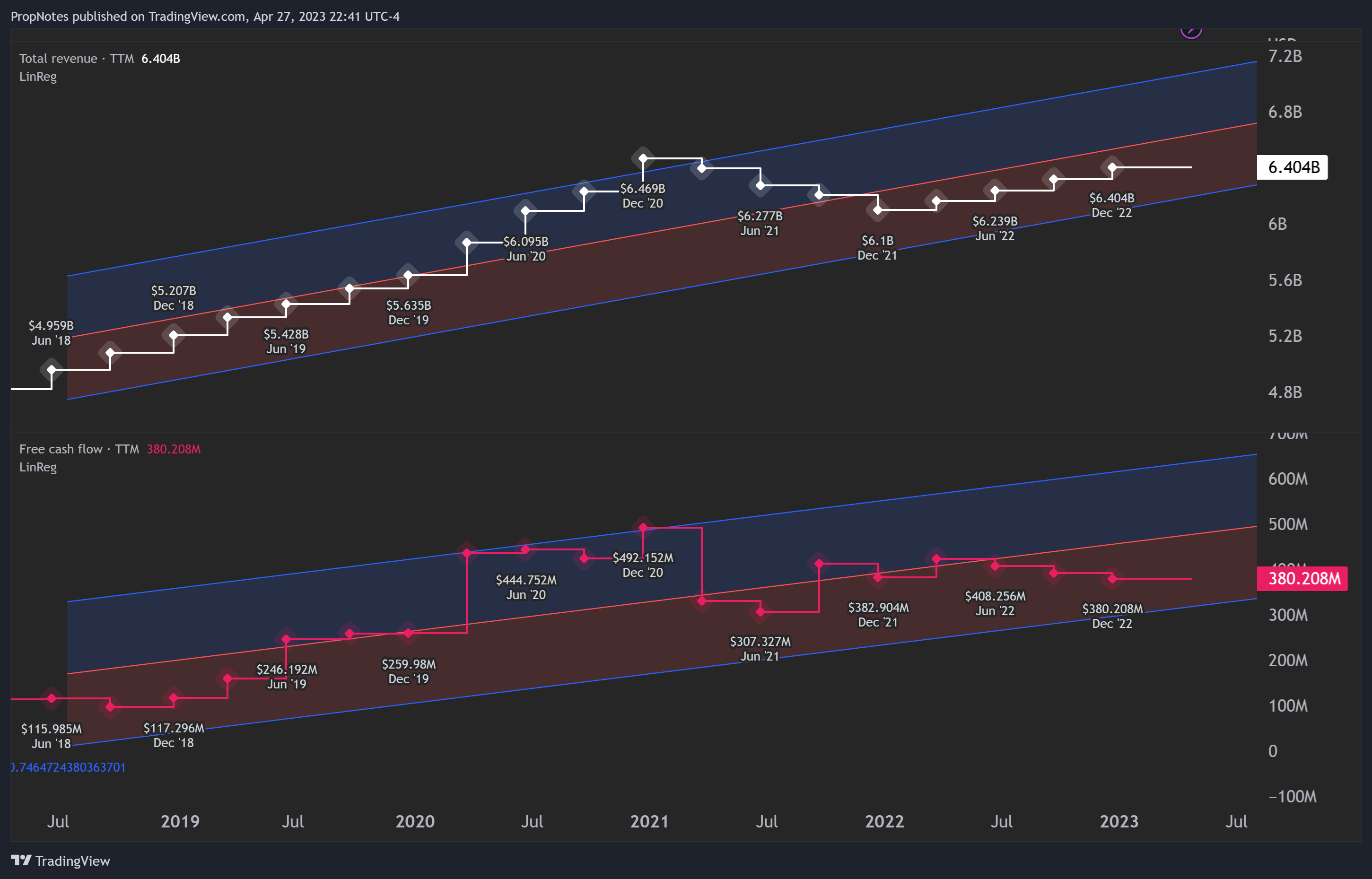

As you can see, Revenue and Free Cash Flow are trending in the right direction. Both top-line sales and bottom-line profitability are up considerably over the last 5 years, and net income margins sit at around 4%, which is impressive for the grocery category. This margin should act like a shock absorber in an economic downturn and cushion the company from bad breaks or other hardships that may be encountered.

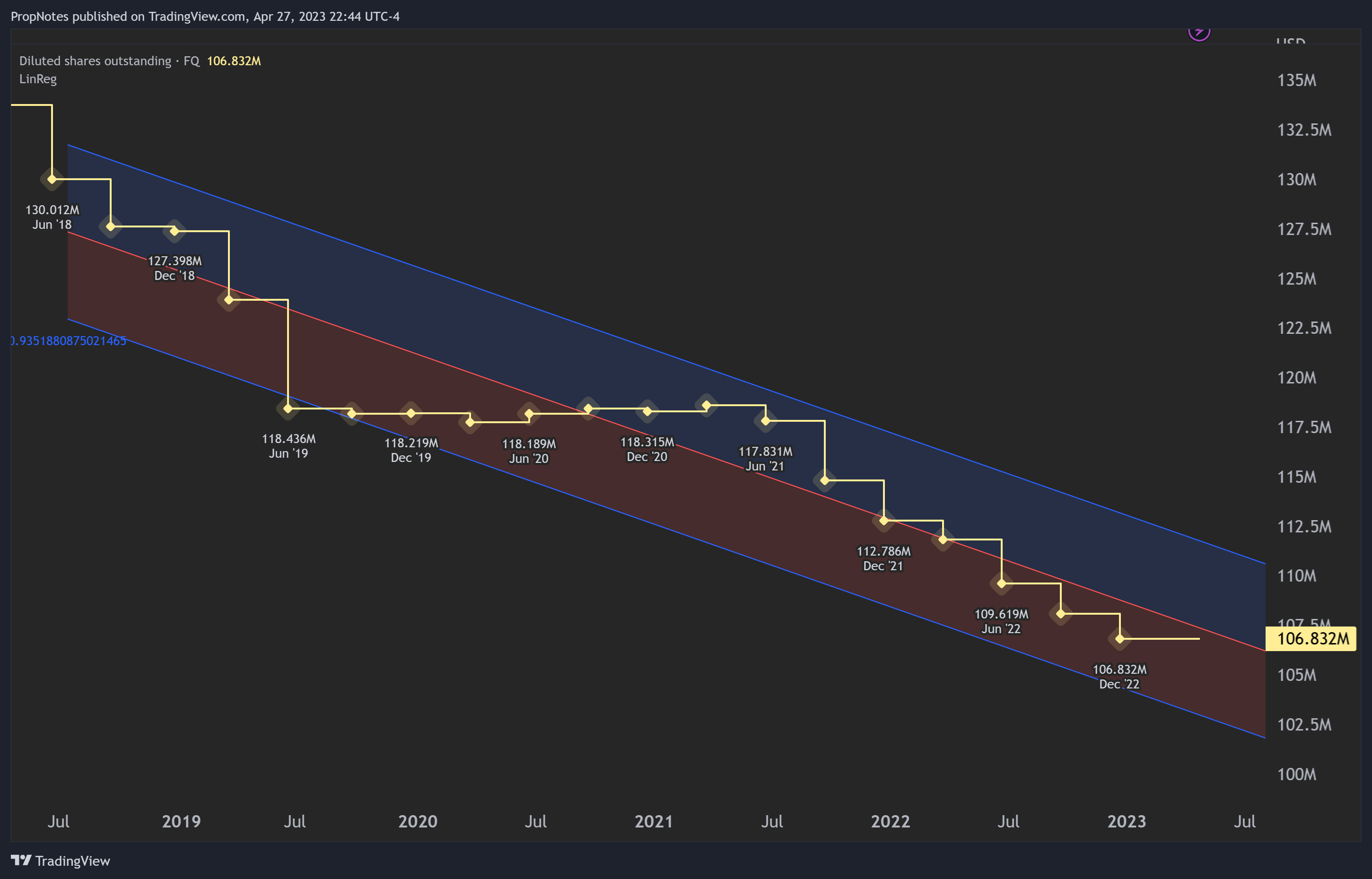

The company is also buying back shares hand over fist:

{kind=link}

Since 2018, share count has dropped by over 20%, from 130m shares outstanding to just over 100m. When combined with the company's growing top line and profitability, SFM has very favorable supply and demand dynamics for its shares.

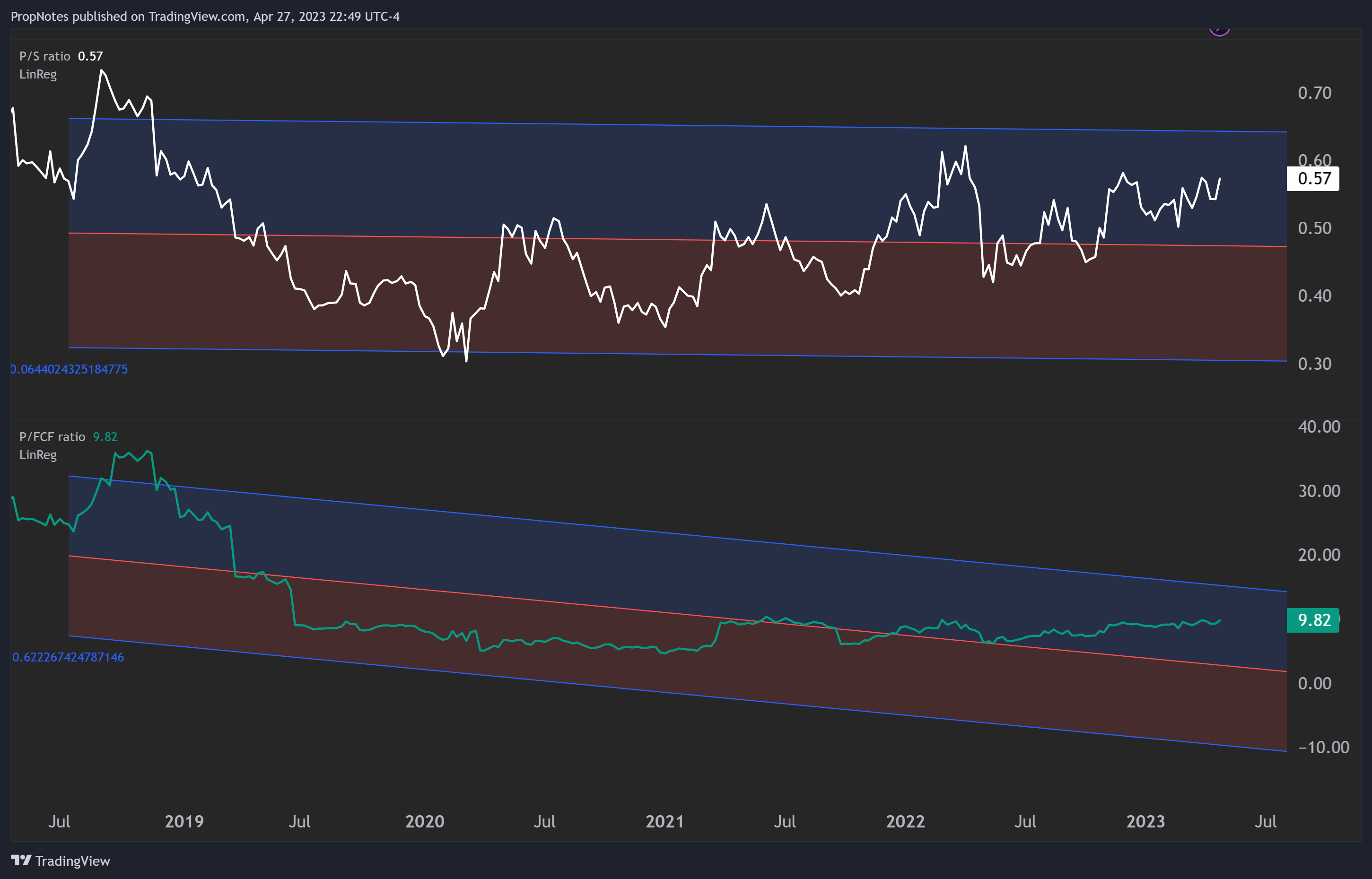

Supply and demand for shares may look good, but the valuation also looks attractive:

{kind=link}

While the company isn't trading at its cheapest valuation on a historical basis, 9.8x Free Cash Flow for a high-performing company is a relative bargain vs. the performance and valuation of other peers in the space.

Finally, the company doesn't pay a dividend. This is a great feature for us for two reasons. First, it's a more tax efficient way to return capital to shareholders. While income can be great, buying back shares at good times is far more accretive to long term investors. Second, it means that there isn't an entrenched shareholder base that has built up over time that would dump on our position should the dividend be cut during a tough period.

Add it all together, and we think it's the best company / stock in the space.

Historical Performance

Sprouts performing well in during economic downturns isn't just theory, either. The company and its shares have performed well in practice.

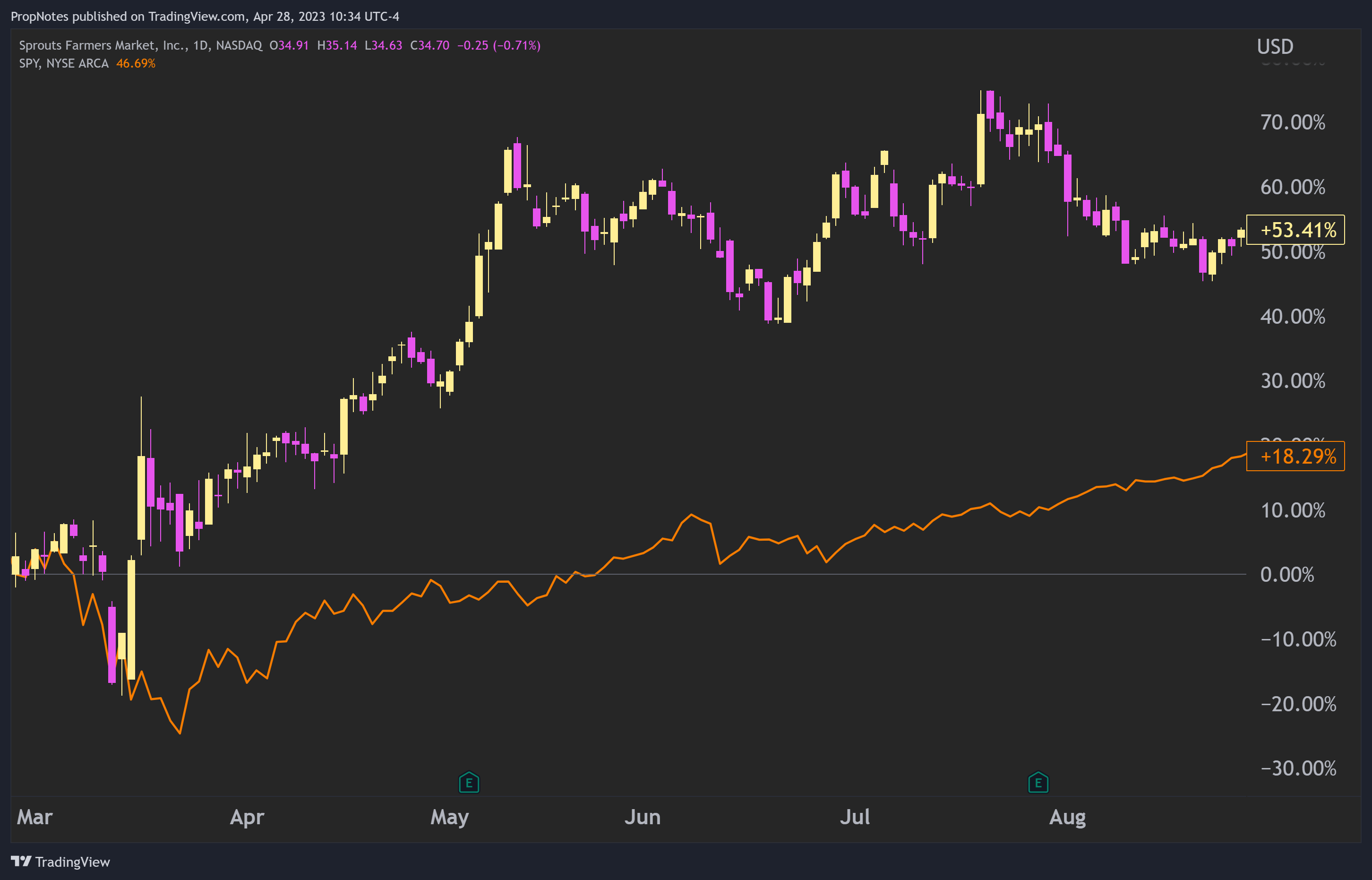

In the six months following the start of the pandemic, SFM investors enjoyed massive outperformance vs. the broader market which was thrown into chaos:

{kind=link}

Sprouts outperformed by more about 35% in that time. Not bad!

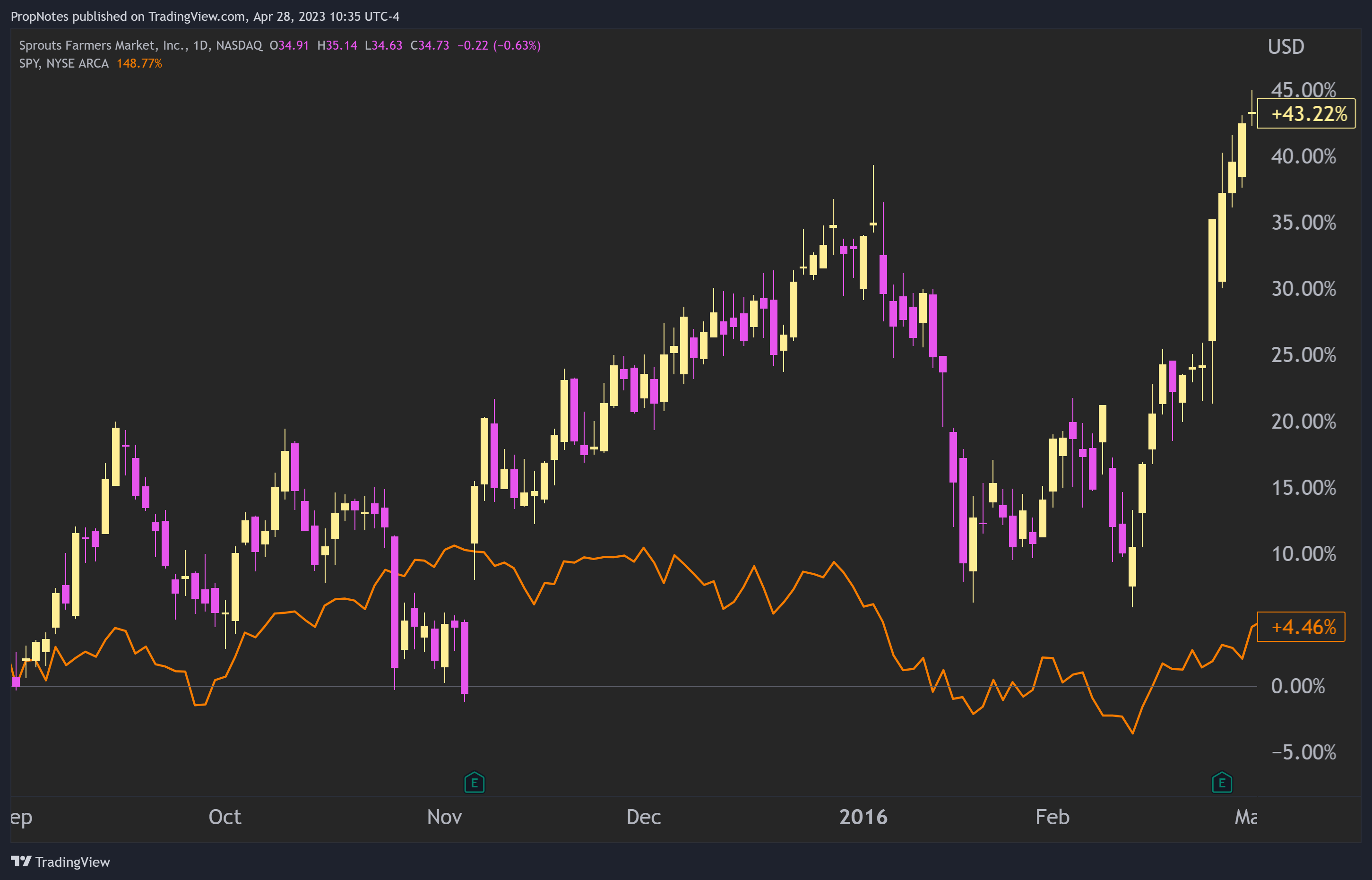

What about a more traditional economic contraction? Another good example of this happened in late 2015 and early 2016 when the ISM's dipped below 50 and the markets suffered some severe setbacks. How did SFM perform? Like a champ:

{kind=link}

In the 6 months that defined this economic pullback, SFM shares outperformed the market by nearly 40%.

Clearly, SFM is a good choice for slowdowns due to its inelastic business model.

Other Options

As we mentioned before, there are other options in the grocery space. Why Sprouts?

None have the combination of value, performance, profitability, and growth that Sprouts has.

Kroger is bigger, which is an advantage in a downturn. However, margins are lower, the stock is nearly twice as expensive on an FCF basis, and the company is undergoing a messy wedding to Albertsons, another public grocery chain.

The aforementioned Albertsons is also an option, albeit not a very good one. Aside from the messy potential wedding to Kroger, margins are really weak, and growth has suffered. TTM FCF is below where it was in 2021 and doesn't look poised to rebound anytime soon.

Finally, Grocery Outlet is a peer, but not a realistic option. The company's growth has actually been alright, but margins have deteriorated and the company currently trades at 70x FCF. No bueno.

Thus, we are left with Sprouts as our favorite pick.

Risks

While we think SFM is the best pick for a potential recession, there are a few risks with this thesis.

Business Execution : If management fails to continue delivering on the strong results outlined in this article, then financial performance and the stock price may be in trouble. The track record is strong, but the risk of management mistakes is always present in any investment.

Relative Underperformance : If a recession doesn't actually hit, then SFM buyers may stand to be underexposed to cyclical companies and a re-acceleration in the economy. This could lead to material underperformance.

Size : Sprouts is simply smaller than some competitors. While the company has robust margins for its industry, should a protracted recession hit, then the lack of scale inherent in the company vs. competitors like KR could hurt operational performance.

Summary

In sum, we think a recession is on the way, and that SFM is one of, if not the best places to hide out while the storm passes. Strong capital discipline, profitability, growth, and valuation make the stock a perfect fit for any recession-conscious portfolio.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Sprouts: A Potential Bulletproof Business Model For The Next Recession