SPY - SPY: 3 Things That Could Cause The Next Bear Market

2023-11-06 16:49:34 ET

Summary

- Equities had their largest rally since late in 2022 last week on a huge drop in the yield on the 10-Year Treasury.

- However, trading action felt more like a relief rally than any new 'inflection point' for market direction.

- The potential for recession in 2024 is high and this is not reflected in the current prices for equities.

- 3 potential triggers for a recession and a bear market in 2024 are discussed in detail in the paragraphs below.

Overconfidence precedes carelessness ."? Toba Beta.

S&P Sector Performance (Seeking Alpha)

Last week, markets had a " rip your face off" rally that saw the best weekly performances from the S&P 500 (SP500) and Nasdaq (COMP.IND) since the last quarter of 2022. The rally was triggered by the largest weekly fall in the 10-Year Treasury yield since 2011.

Last Week - 10-Year Treasury Yield (Market Watch)

{kind=link}

This felt more like a relief rally after several months of dismal performance for investors more than an " inflection point" for equities. There was also a short squeeze element to the rise as well. Thursday and Friday saw the most heavily shorted stocks notch an average 11% gain.

Last week's trading action did little to change my longer-term view that equities will experience a bear market at some point in 2024. Here are the most likely triggers for that event.

Recession:

This is the most likely cause of the next bear market. I have written many times about the deteriorating condition of the American consumer that is responsible for nearly 70% of all economic activity. Most recently in an article entitled The Consumer Is Starting To Buckle back on October 12th.

The consumer is facing many headwinds including reduced buying power since 2021 thanks to high inflation levels, record credit card and revolving debt as well the lowest personal savings rate since the Great Financial Crisis some 15 years ago.

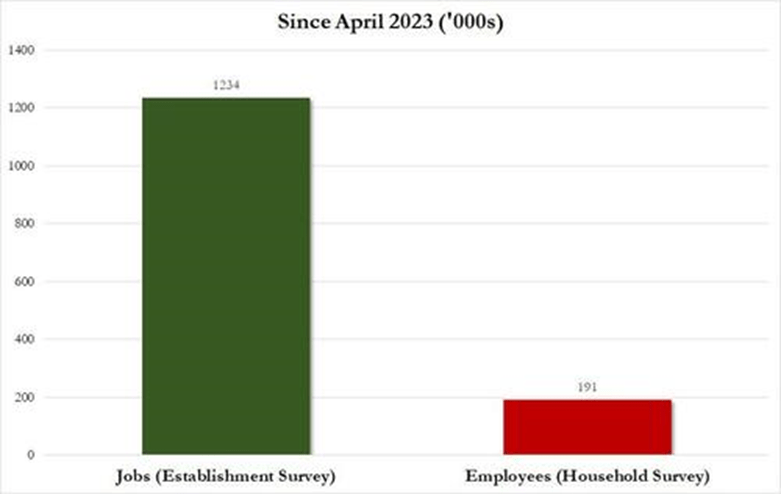

We can now add a weakening jobs market to the challenges facing the American consumer. Friday's October BLS Jobs report had less positions created than expected. In addition, both the August and September BLS jobs numbers were revised down significantly. That now makes for eight of the nine monthly BLS readings in the first three quarters of 2023 that subsequentially were ratcheted down.

It should be noted that 384,000 net individuals became newly unemployed in October, according to the Household Survey. This survey has consistently showed lower job growth than the much more reported BLS survey over the past six months. This is because BLS doesn't account for Americans that are holding two or more jobs. This soared by nearly 400,000 in October, according to the Household survey, to stand at a record 8.5 million.

{kind=link}

It is hard to see how the consumer doesn't crack soon given personal savings have been depleted, inflation is still far above the Fed's target and job growth is noticeably slowing. Savings are now contracting as percentage of national income.

U.S. Bureau of Economic Analysis, Game of Trades

This has only happened two times before over the past 75 years: The first was during the Great Financial Crisis and the second was during the Covid lock downs in the first half of 2020.

We are also seeing a significant deterioration in the conditions in the Commercial Real Estate or CRE sector. I have documented the increasingly dangerous situation here many times since this spring, most recently in an article entitled Something Will Break Soon on October 9th.

Trepp, Morgan Stanley Research

Some $1.5 trillion of CRE debt needs to be refinanced over the next three years and at much higher interest rates at a time where values on many categories of CRE property, such as office and retail, have fallen significantly in recent years. This means delinquency rates and write offs will continue to increase across the space which will trigger increasing headwinds for the regional banking system given its large exposure to CRE debt.

Delinquency Rate By Property Type (Trepp )

Whether it is the deterioration of conditions for the consumer or CRE, one or both is likely to result in recession in the year ahead.

War:

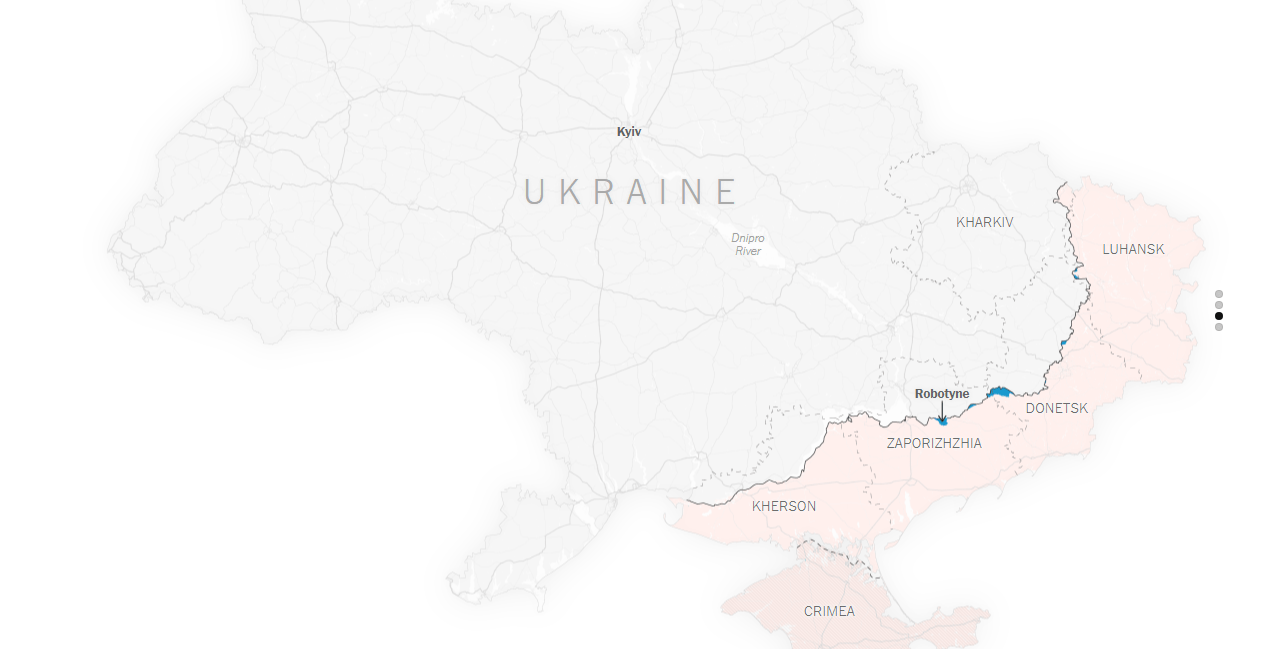

The biggest land war in Europe since WWIII is now more than a year and a half old. As my regular readers on Real Money Pro and Seeking Alpha know, I have said from the beginning of this conflict, that this war will end in the following way. Russia will keep Crimea, influence and/or control on the four eastern provinces in Ukraine known as the Donbas and a land bridge between the two land masses. It is only a question of how much blood needs to be spilled and how much Western treasure will be spent before that logical conclusion comes to pass.

{kind=link}

Even the NY Times recently admitted that Russia now occupies more land now than at the beginning of 2023 despite Ukraine's recent offensive. The question is will this conflict escalate from here, before peace talks begin and this region will remain a wildcard for investors.

Naval-Technology.com

We now have a new situation to be cognizant of since the slaughter of more than 1,400 civilians and soldiers on October 7th in Israel, which included some 30 Americans. The country's response is to eradicate Hamas in Gaza. An understandable action, but one that could escalate quickly and draw in other players such as Hezbollah and/or Iran. This could have grave potential consequences for global energy supplies and prices given how much oil and LNG moves through the straits of Hormuz (18% of global natural gas and more than 18 million barrels of crude daily). A potential and significant terrorist act in the U.S. or more likely Europe in response to large civilian casualties in Gaza is also a potential scenario.

{kind=link}

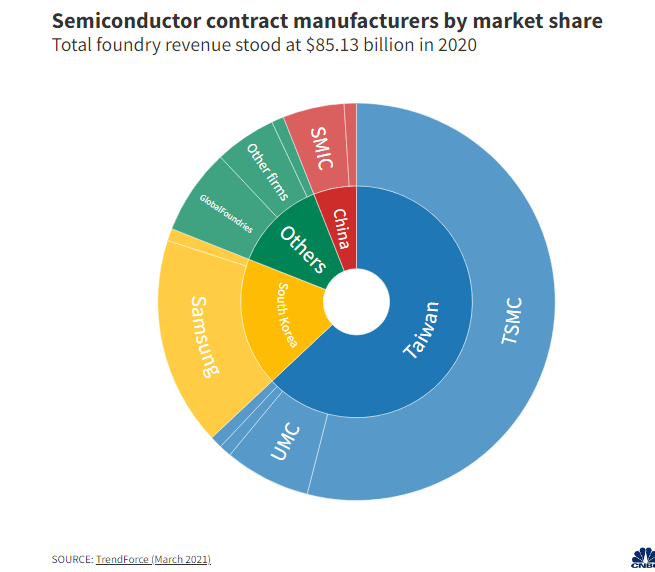

Then there is a Taiwan. Would the middle Kingdom use the divided attention of the West and Israel to finally act on its long-held desire to retake Taiwan? Much speculation around this subject has been aired in 2023. And while this scenario is remote, it would be devastating to the global economy if for no other reason how dependent on semiconductor supplies coming from Taiwan the rest of the globe is as the country produces over 60% of the world's semiconductors and over 90% of the most advanced ones.

Debt Crisis:

While the yield on the 10-Year Treasury (US10Y) had its biggest weekly drop in 12 years last week, interest rates are still near their highest levels in a decade and a half. This eventually will have huge implications for the federal budget given the national debt is fast approaching $34 trillion and the United States debt to GDP levels is nearing its record high during WWII.

Congressional Budget Office, Capital Economics

Unfortunately, the country is continuing to run massive deficits even during the economic expansion that has taken place since lock downs starting to come off during the initial phases of the Covid outbreak. At some point, it is easy to see a significant " hiccup" in the treasury markets occurring which could have substantial ramifications for the economy and the markets.

Treasury Department & OMB

Costs to service the federal debt have already exploded with outlays for debt service roughly doubling in FY2023 compared to FY2021. With just over half of the national debt needing to be refinanced over the next three years, these costs will continue to escalate at a sharp rate.

Yen Vs.USD (Market Watch)

This type of crisis may occur in Japan first given the country has a debt to GDP ratio of north of 260%. This is a key reason the Yen has been so weak against the greenback so far in 2023.

Recession Impacts:

Historically, most U.S. recessions have resulted in a bear market in equities. I see no reason why this will not be the case this time. This is especially true given interest rates are much higher than they have been for a decade and a half. Valuations also seem more than stretched here in an economy that is growing still.

Goldman Sachs sees S&P 500 earnings being $237 in FY204. This means the S&P is priced at 18.5 forward earnings with a 1.5% dividend yield. Quite dear when short term treasuries are yielding more than five percent and earnings estimates will come down significantly if a recession scenario plays out.

Charlie Biello - Chartered Financial Analys

Individual and popular stocks are priced even more extremely. Take Apple ( AAPL ) , which has the highest market capitalization of any stock. As of Friday's close, the stock is priced at 29 times earnings and 7.3 times revenues. Far above its 10-year average of 20 times profits and 4.7 times sales. And those averages occurred when interest rates were much lower. In addition, and both earnings and revenues are predicted to decline for Apple shareholders in 2023.

Given this outlook, I took advantage of the blowoff rally on Thursday and Friday of last to add some more and cheap "portfolio insurance" to my holdings in the form of long dated, out of the money bear put spreads on the SPDR® S&P 500 ETF Trust ( SPY ). They will pay off hugely and offset the losses on the long side of my portfolio should a recession and bear market emerge in 2024, which seems at least a 50/50-coin flip currently.

There is no more insidious poison than hubris ."? C.A.A. Savastano.

For further details see:

SPY: 3 Things That Could Cause The Next Bear Market