SPY - SPY: Bulls Can Sleep Well At Night Ahead Of The February Fed Meeting

Summary

- We expect a shift in the messaging towards monetary policy at the February 2nd Fed Meeting which can work as a catalyst for risk assets.

- The latest December PCE data showed inflation ended 2022 well below the Fed's forecast from the last FOMC.

- We highlight ongoing themes during the Q4 earnings season.

- We are bullish on the S&P 500 and see more upside in the SPY ETF.

Stock market bulls are loving this rally and it's coming at the expense of doom-and-gloomers or anyone betting on a big crash lower. Compared to the start of last year, the tables have turned and it's the bears painfully sitting on the wrong side of the trade.

Indeed, the S&P 500 ( SPY ) is up more than 6% in the first weeks of January, and 16% higher since the lowest levels of 2022. Even as a large segment of the market may have entered 2023 pessimistic, our sense now is that the consensus is finally coming around.

We've been bullish and our message here is that there is more upside with room for investors to jump in long and add exposure to equities based on several important developments. We're looking forward to the upcoming February Fed Meeting which could set the stage for the next leg higher.

The Fed Was Wrong At The December FOMC

The biggest shift has been related to the inflation outlook which has made a complete 180 compared to fears in the first half of 2022 of "hyperinflation" or that consumer prices were simply out of control. There's a lot less uncertainty now which is positive for risk assets.

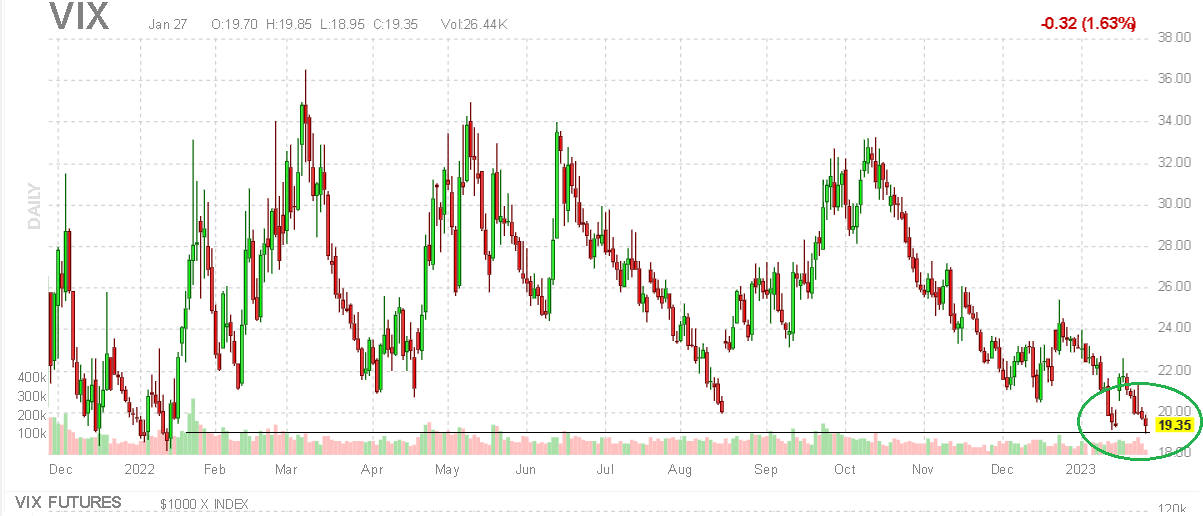

The VIX Index ( VXX ) often referred to as "Wall Street's Fear Gauge" has dropped decisively under 20, the lowest level in a year. Credit spreads , as an indicator of the risk of corporate defaults, have narrowed sharply as a good backdrop for financial conditions. We can also point to the weakening Dollar which supports a rebound of global activity. We think these trends are just getting started.

{kind=link}

Simply put, data in recent months has turned much more favorable suggesting the biggest headwinds from last year have passed, with implications for the next step in Fed policy.

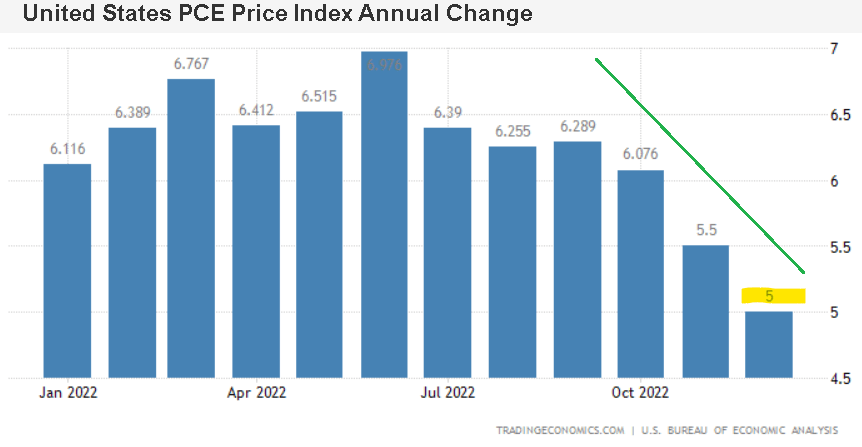

Case in point, let's go back to the last Fed meeting in December, which included updated quarterly economic projections . On December 14th, the group published its 2022 Personal Consumption Expenditures (PCE) inflation forecast with a view that the rate would end the year at 5.6% or 4.8% for the Core-PCE, which excludes the impact of food and energy.

source: St. Louis Fed

The newsflash today is that those estimates have turned out to be way off. The key here is to note that those Fed projections were made before the final November PCE print later in the month which surprised the downside and the latest just-released December figure .

The headline PCE ended 2022 at 5.0% while the core rate came in a 4.4%. By this measure, the Fed's PCE inflation forecast missed by 60 basis points or 40bps on the core side. Keep in mind that the market estimates heading into these last two PCE reports were already being revised lower going back to last month with the earlier CPI data. This trend is a game changer also reflected in lower inflation expectations.

{kind=link}

What Will the Fed Do Next?

In other words, the data the Fed is looking at has progressed much more favorably than imagined just six weeks ago and risk assets including stocks are responding to that. Sure certain components of the price basket remain volatile like "eggs" or "medical services" but the big picture is clear regarding the direction.

Over the next few months, the annual inflation rate will begin to hit particularly tough comps from the first half of 2022, further driving downside in the headline rate.

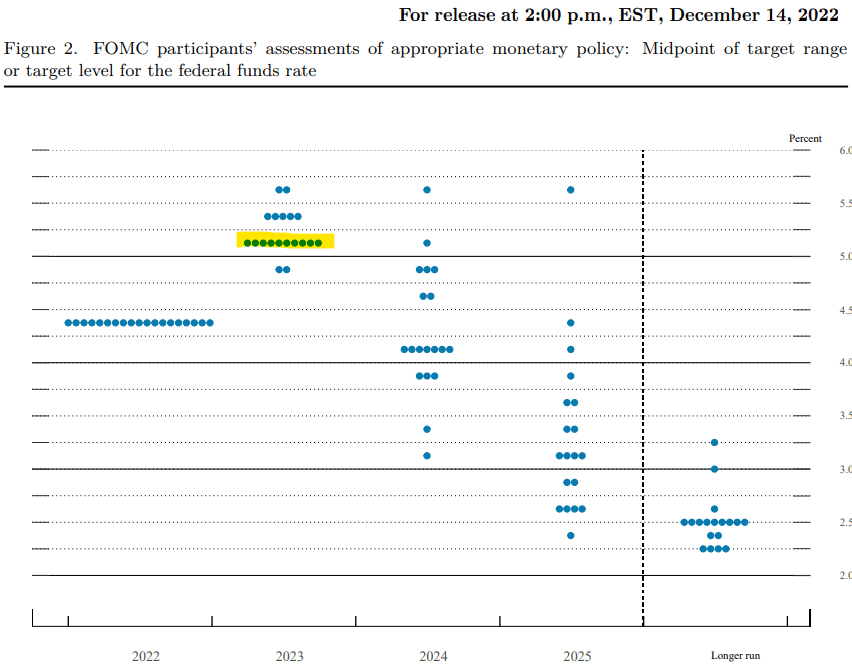

So all that leads us to the fabled "dot plot" which is the closely watched projected trajectory of the Fed Funds Rate by the FOMC participants. From the last Fed meeting, the controversy centered around the tick higher in the 2023 Fed Funds Rate target to 5.1%.

Making the connection with the recent inflation data that has been cooler than the Fed's baseline, the messaging and outlook for "appropriate monetary policy" presented in December is now stale at this point.

{kind=link}

Call it a "pivot" if you want, but the reality here is that the Fed now has room to adjust its policy stance based on real hard data. Everything suggests there is downside to the dot plot and Fed Funds Rate trajectory in the next update.

Further rate hikes may not be necessary to reach success in stabilizing consumer prices, anchored over the long run under 3%. There is a consideration that the transmission effects of the 2022 rate hikes are still working through the economy, and the Fed understands that.

Our call is to expect a single 25 basis points hike to the Fed Funds Rate on February 2nd, which is also currently the consensus, and that could be the end of the cycle. More important will be the new flexibility to adjust its tone and messaging away from the "fire and brimstone" narrative that was a staple in 2022. The Fed is data-dependent, and the data is on the side of stock market bulls.

The bond market is already responding to these views based on the pullback in yields. Again, this is a source of debate with some making the inference that interest rates are pricing in a "recession" or collapse in economic conditions. The more mundane and glass-half-full interpretation is simply that the lower bond yields reflect the lowered inflation trend, based on easing structural pressures being the supply chain disruptions and skewed pandemic dynamics that are looking more and more transitory.

Again, the Fed has room to make changes to its policy based on "hard" data, and not because they are just magically abandoning their inflation battle, or caving to signs of a collapsing economy.

What About Stocks?

So putting it all together, that's why stocks are rallying because the cooling inflation setup provides a boost in everything from economic activity to consumer budgets, and also businesses that get relief on the cost side. The latest Michigan Consumer Sentiment Survey confirms this view, indicating a rebound as consumers respond to these trends.

It's also notable that the Q4 GDP data showed the economy has remained resilient alongside trends in the labor market. The "soft landing" scenario for the U.S. and global economy remains alive and well. A 5% Fed Funds Rate apparently is manageable which is something few may have believed this time last year.

A baseline of low expectations opens the door for companies to beat estimates over the next several quarters. In our opinion, there is a path for conditions to evolve more positively going forward. even at a higher plateau of rates.

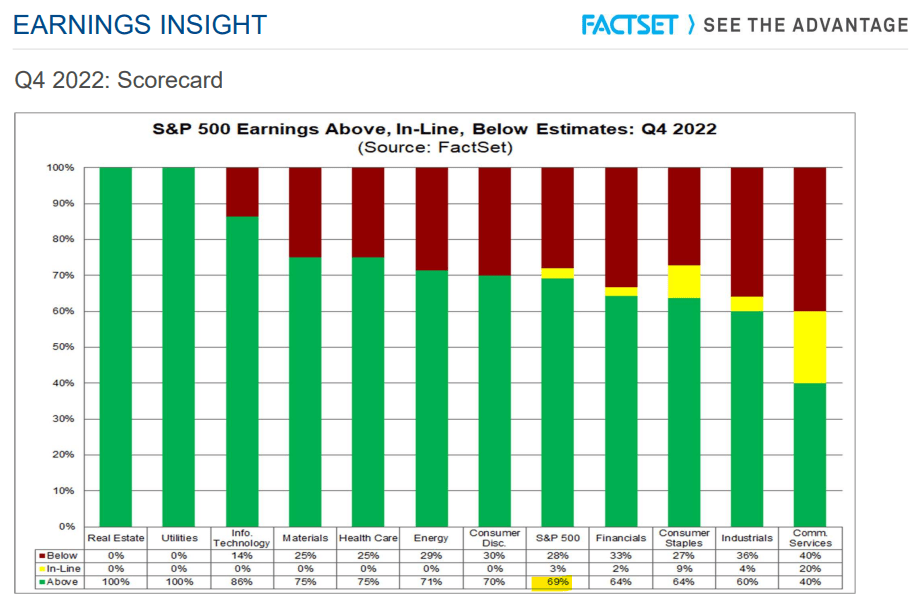

On this point, the Q4 earnings season has been overall good with some high-profile earnings beats against some weaker trends. The data we're looking at suggests that with nearly one-third of S&P 500 companies reporting thus far, 69% have posted EPS above expectations.

The only people disappointed here are those expecting companies to start missing left and right which did not happen, which explains some of the market strength.

{kind=link}

Guidance has been softer, but there are some notable exceptions like Johnson & Johnson Co ( JNJ ) which noted a full-year revenue and earnings target above market estimates. Boeing Co ( BA ), while missing estimates, noted a strong order book for its aircraft with a climbing backlog globally.

It's also encouraging to see shares from a mega-cap leader like Microsoft Corp ( MSFT ) continue to rally even with soft guidance. Growth leaders like Tesla Inc ( TSLA ) and Nvidia Corp ( NVDA ) have led higher amid a theme of outperforming beaten-down tech.

What's more important is that market-wide valuations look attractive. On a forward twelve-month basis, the S&P 500 is at a P/E multiple of 17.5X, which is below the average for the past decade. The reason we like that figure is considering it's in an environment where macro conditions improve and interest rates stabilize.

{kind=link}

The bullish case is that 2023 earnings estimates have room to be revised higher over the next few quarters which will make stocks appear increasingly cheap. Getting into 2024, the market theme could be centered around strengthening conditions and accelerating earnings.

We sense that the trading environment has started to evolve with bulls in control, as dips get bought while shorts are forced to chase higher. This is in contrast to 2022 when it was difficult for rallies to sustain momentum. By this measure, there is something different with the market in 2023 that is reversing many bearish themes and trends from last year.

Final Thoughts

The setup for the upcoming FOMC with Chairman Powel simply acknowledging an improved inflation outlook may be enough to set the stage for the next leg higher in stocks.

An evolving market narrative that the end of the hiking cycle is on the horizon while economic conditions rebound is what we see taking shape right now that has lifted stocks. From here, "good news" is good news, shutting the door on the most apocalyptic predictions from 2022.

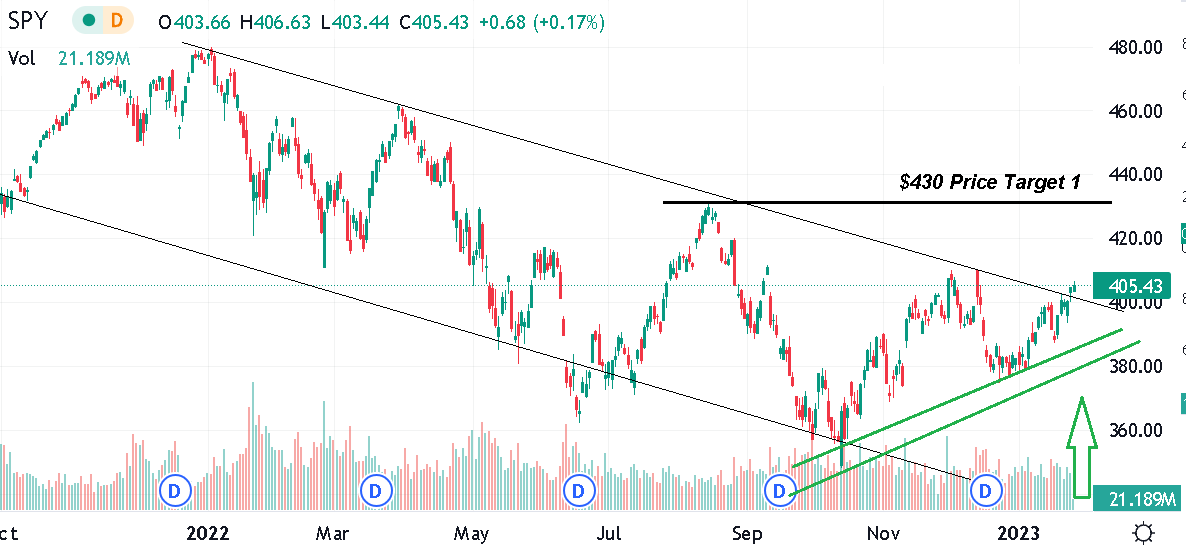

Our next target for the S&P 500 is for a retest of $4,300, corresponding to approximately $430 in SPY. We also reiterate a year-end target for the S&P 500 at $4,777, or $480 which takes it back to near the all-time high. You can read more about that view in this article from December .

We always like to end up covering some risks to our forecast. What we can say is that it won't be a straight line higher so an expectation of continued volatility is fair.

The situation in Ukraine also adds uncertainties with an escalation of the conflict beyond the current imbroglio as a possibility that would undermine and bullish thesis. Similarly, a sharp resurgence of inflationary pressures would also force a reassessment of the outlook. On the macro side, evidence of surging unemployment or a sharply deteriorating economy would be concerning, although we don't see that right now.

{kind=link}

For further details see:

SPY: Bulls Can Sleep Well At Night Ahead Of The February Fed Meeting