AAPL - SPY: The Market Is All In On A Fed Pivot - Will Powell Call The Bluff?

Summary

- Traders are clamoring for a Fed pivot and have upped their bets on massive interest rate cuts and the return of QE and money printing.

- The S&P 500 has pushed back above 4000 while the 10-year Treasury yield has plunged from 4.2% to about 3.4%.

- Meanwhile, the Fed has signaled no intentions to cut rates in 2023, and inflation is showing signs of a resurgence. Traders are going all-in with bad cards.

- Cash will soon pay 5% risk-free, and is actually the best hedge against inflation going forward.

- The stock market is trading back to near bubble prices, while the real estate bubble is slowly rolling over. Buckle up!

The S&P 500 ( SPY ) has staged a face-ripping rally this January, led by trader hopes that the Fed will pivot, cut rates back to 0%, and print more money. After the blow-off top in early 2022, the broad index had fallen about 25% by October as the market began to take the Fed's inflation-fighting credibility seriously. Since then, financial conditions have eased considerably. Stocks have recovered a bit less than half of the bear market decline, yields have fallen sharply, and the US dollar has rapidly declined against the yen and euro. Oil bottomed in early December and now has staged its own rally. The trouble for traders is that behind the scenes, these loosening financial conditions are fueling the next wave of inflation and pushing the Fed pivot further out of reach. We've seen this movie before. We're now in the third round of Fed pivot mania after the massive July/August rally and the November rallies both petered out. Against this backdrop, the FOMC meets Tuesday and Wednesday of next week and chair Jerome Powell will deliver more hints to the market about its future rate hiking plans in his press conference. So is the Fed pivot coming, or will Powell call the market's bluff? Let's dig in.

Back To The Meat Grinder?

Famed stock market strategist and GMO founder Jeremy Grantham recently issued a warning for investors in 2023, calling stocks accidents waiting to happen, and warning about the future economic consequences of the real estate bubble in the US and abroad. Grantham has a target of 3200 on the S&P 500, cautioning that when the excess savings built up during the pandemic run out, the support for the economy "will be gone." Despite shrinking for two consecutive quarters earlier in the year, real GDP grew by an estimated 2.1% in 2022, as the economy catches up with the damage sustained during the pandemic and pushes back toward its pre-pandemic trend. The question now is how much we'll end up paying for the COVID spending binge when the eventual recession does hit.

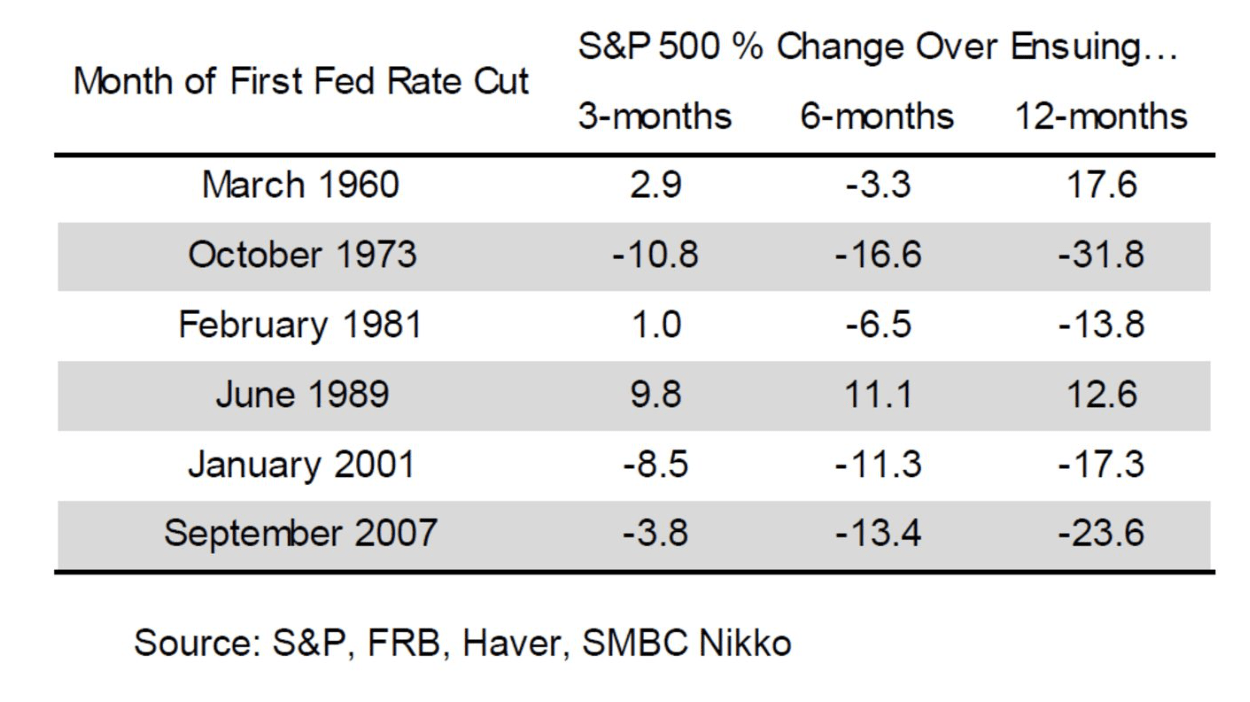

Grantham isn't permanently bearish on everything - his note indicates his preference for value stocks in the short run and green energy stocks in the long run. But perhaps the most interesting is his historical research on past "fed pivots," and how they have affected the outcome of asset bubbles in the past. Because pivots tend to portend economic hurricanes, traders begging for a pivot should be careful what they wish for!

Rate cuts after "Great Bubbles"

{kind=link}

Granted, this isn't a complete history of rate cuts – the Fed has many times cut rates to help stimulate the economy, including during the " maestro " years when Greenspan would cut rates by a bit to spur the markets and then raise them to back the markets off.

But when you take a broader historical sample , you see that Fed pivots can help the economy (a little) but generally aren't capable of reflating asset bubbles. The exception was the pandemic, but the real firepower there came from fiscal stimulus ( helicopter money ), not from monetary policy. Since the great American experiment in modern monetary theory caused massive consumer price inflation and angered millions of voters, that's off the table now, especially with Republicans taking over the House of Representatives. History shows that the Fed is not more powerful than the business cycle, or recessions would have been outlawed long ago otherwise!

{kind=link}

Of course, the usual suspects are bearish as well. Mohammed El-Erian has argued that the Fed should hike by 50 bps in its meeting next week to a 5% Fed funds rate to help stave off a second wave of inflation. I think he's right – there are a bunch of signs of trouble brewing in inflation. The Fed is almost certainly going to go 25 bps at the next meeting, hammering home the point that they excel at communication but fail at economic forecasting as they continue to fight "transitory inflation" in its third year. Morgan Stanley ( MS ) chief strategist Mike Wilson has warned that earnings will not live up to expectations and that markets will sell off. JPMorgan ( JPM ) strategist Marko Kolanovic, typically the more bullish foil to Wilson – has turned " outright bearish ." Dr. Michael Burry also has taken to Twitter to share his thoughts on why the rally won't last, comparing the current market to the 2000-2002 bear market that was marked by multiple 20% rallies .

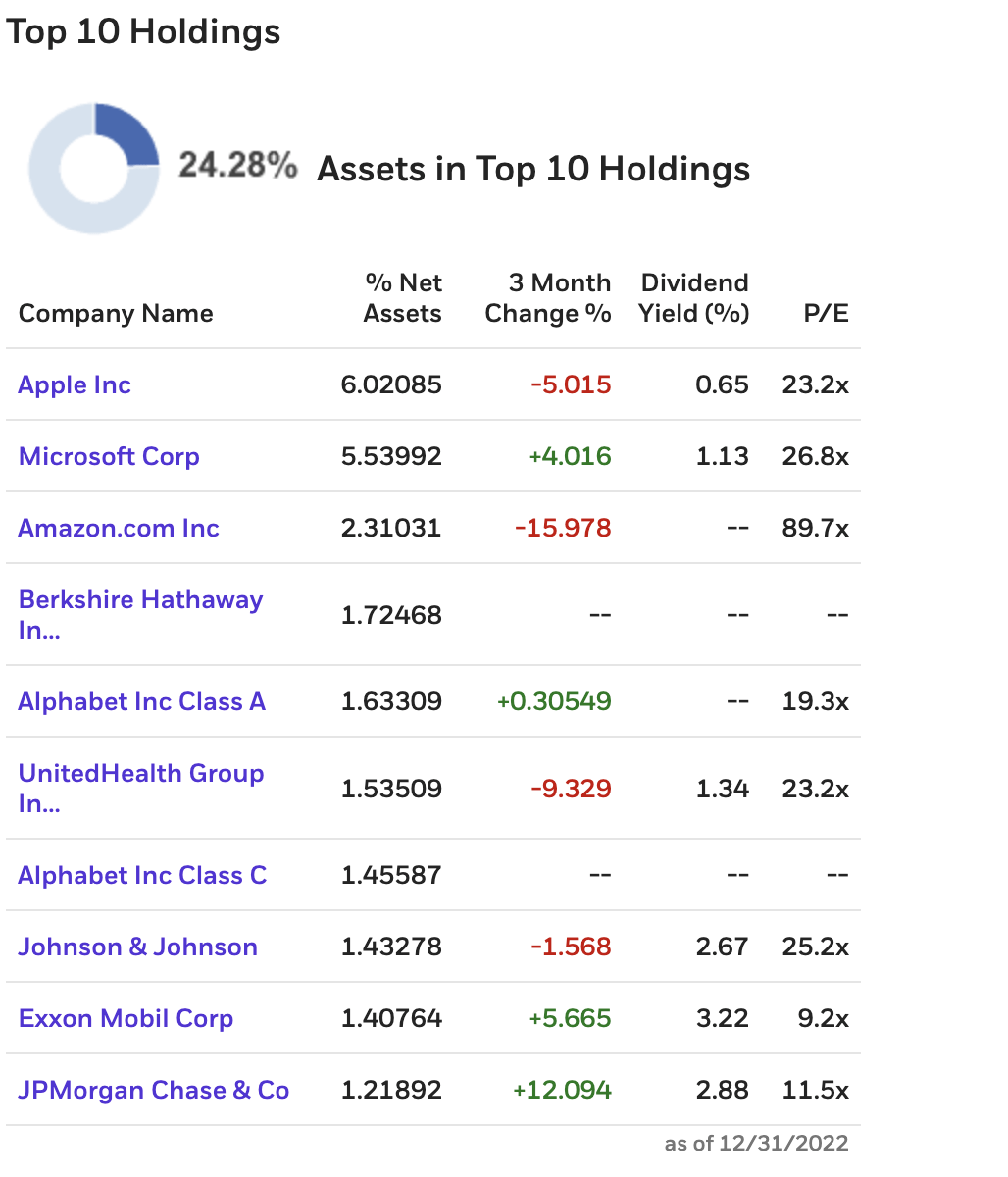

For what it's worth, here are the top 10 holdings of the SPY and index, as well as the valuations as of year-end 2022 (note that this predates the January face-ripping rally, so you'll want to add about 6-7% to these to get today's PE ratios)

Top Holdings in the S&P 500

{kind=link}

Amazon ( AMZN ) is sitting at a 90x PE and Tesla ( TSLA ) is out of the top 10 after its 2022 meltdown. Value is starting to make a comeback with Exxon ( XOM ) and JPMorgan sneaking back into the top 10, but multiples are still overall too high. Apple ( AAPL ) is sneakily overvalued – smartphone sales just posted their biggest-ever decline. Johnson & Johnson ( JNJ ) is similarly overvalued, EPS growth prospects are lousy while the multiple is high.

Inflation Is Hard To Kill

So what's happening on the inflation front? There are some warning signs.

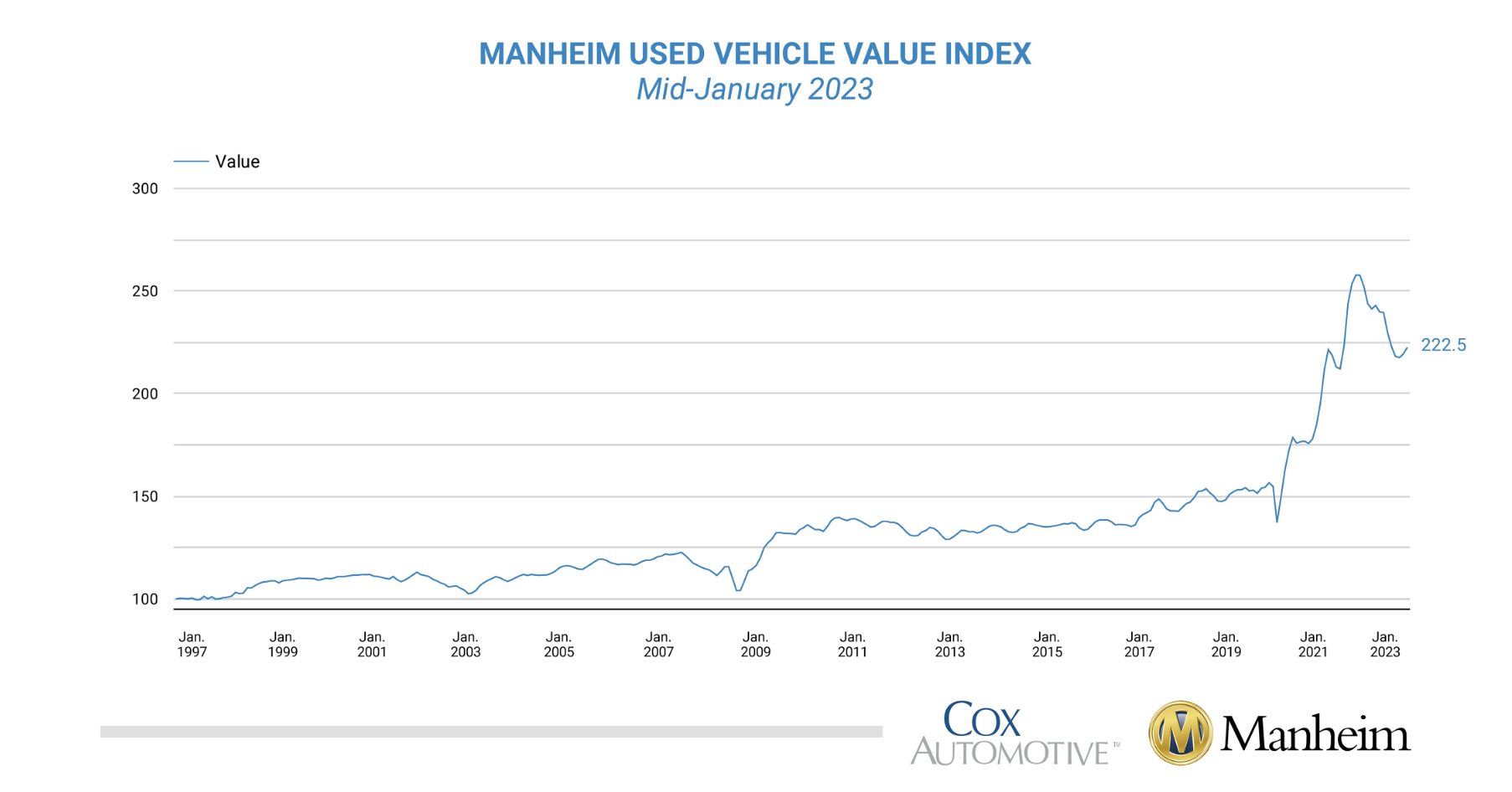

1. First, there's a lot of pent-up demand for used cars. Falling used car prices were helping the Fed's inflation fight, but this has now reversed, according to data from Mannheim. The l atest data from Mannheim shows that used car prices are up 1.5% in the first two weeks of January, partially reversing earlier declines.

Wholesale Used Car Prices (Mannheim)

{kind=link}

2. Second, the dollar ( DXY ) is much weaker, which will work to push up import prices in 2023 like clockwork. The dollar held down inflation in 2022 (particularly in commodities), and if the Fed is seen as backing off hikes in 2023, the dollar will push inflation back up. With China reopening as well and oil up about 15% off of the lows, commodities are going to pressure inflation as well.

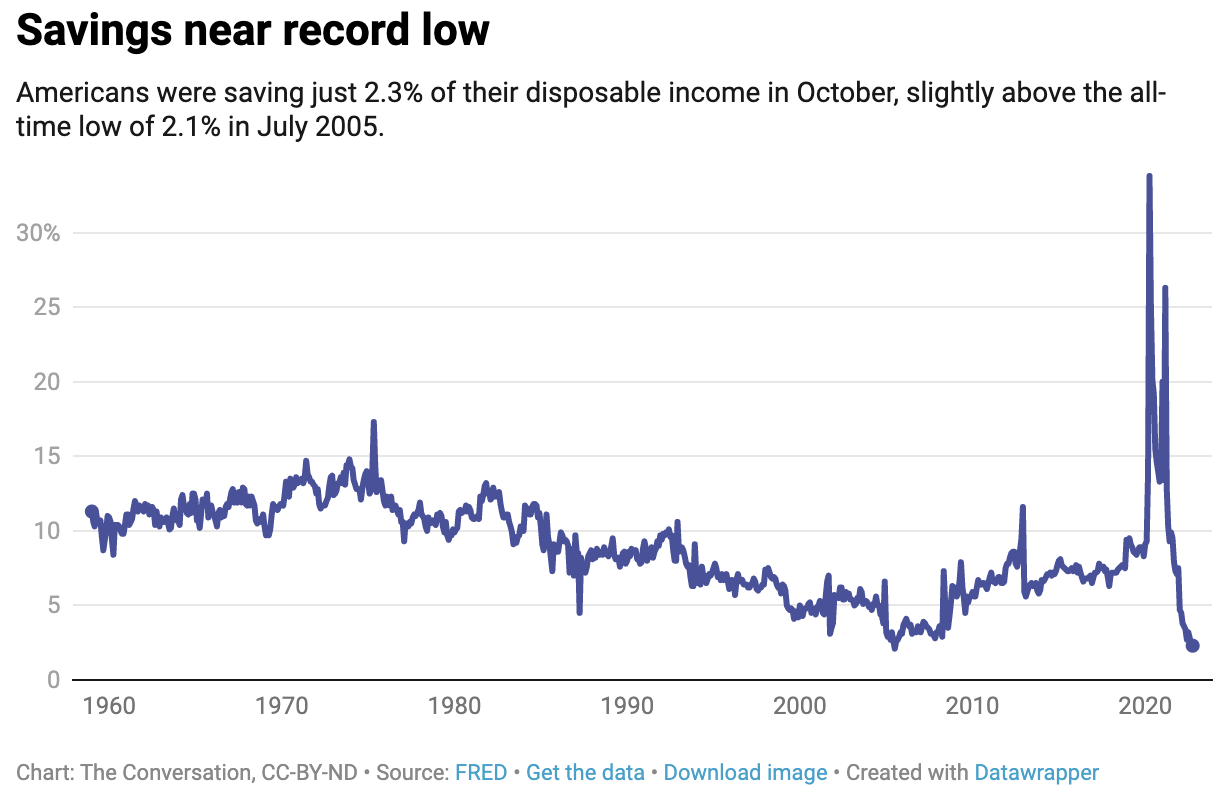

3. However, the real trouble is from the US savings rate being as low as it is. The labor market is tight but tight labor markets causing higher wages isn't really a big negative in my opinion. What's a negative is that people are spending all of their economic earnings and then borrowing more on top (when you account for the student loan pause that the Republican Supreme Court will dismantle). This is a macroeconomic time bomb. Consumers spending more than they earn causes inflation in the short run and makes the economy increasingly vulnerable to a deep recession in the future. The only other time the savings rate was this low was 2005-2007 , coincidentally during the last real estate bubble, and right before the economy imploded.

US Savings Rate (The Conversation)

{kind=link}

Savings rates near record lows while consumer prices continue to grind higher is an obvious problem. Having studied the history of successive waves of inflation in the 1970s, the Fed has taken great pains to push back on market expectations that they'll pivot and cut rates. But the market continues to ignore the Fed, gleefully pumping money into speculative assets and making bets that profit if rates fall. The real estate market moves like an aircraft carrier, but housing prices are falling steadily from bubble highs in the US and in other overvalued markets globally. Bulls will tell you that sky-high rents are starting to fall, but even those have proven sticky to start the year with COLA adjustments kicking in.

Will The Fed Pivot?

Despite calls from Elon Musk and Cathie Wood , the Fed is unlikely to pivot in the near term, and in the case they do, it will be because the economy has ground to a halt, in which case stocks will be much lower. Fed funds futures are pricing about 200 bps in rate cuts starting this summer to the end of 2024. The Fed itself is saying that they're going to raise rates and hold them to assess inflation. The Fed's summary of economic projections " dot plot " indicates that they may be willing to cut rates in 2024 if inflation comes down, but not in 2023. A couple of problems with this view:

First, core inflation is still running a bit higher than the Fed funds rate. Furthermore, most of the tightening hasn't really worked its way through the economy yet. Bridgewater, the world's largest hedge fund, broke this down in an excellent macro piece a couple of weeks ago. The Fed looks at core inflation, and markets celebrated when that came in at 0.3% for December. But this was helped greatly by used cars and trucks, as well as from a quirky non-cash health insurance adjustment. Even if core inflation continues to come in around 0.3% per month, that still compounds to 3.7% per year, far above the Fed's 2% target. With all the factors we mentioned before combining to push up inflation, inflation likely isn't going to go away on its own. The factors pushing up core inflation– runaway consumer spending and services inflation are still in place. And now, some of the factors that were pushing inflation down (strong dollar, used car market, China lockdowns) are now reversing. Some nasty inflation surprises are likely coming this spring and summer before inflation is finally crushed.

Second, even if the Fed is more successful at controlling inflation, 3.5% core annual inflation and 5% interest rates aren't inconsistent if the Fed is serious about achieving its long-run inflation target. A large portion of the market seems to believe that the Fed will go back to zero rates and QE, as evidenced by the lack of compensation in terms of real yields. Inflation breakevens are rising , and real yields are down to around 1% annually for 10-year Treasuries, after being closer to 2% in October. Historically, the free market sets real yields at 2% or higher, and with the Treasury running big deficits and the Fed running a QT program, it's hard to see how bond yields (and mortgage rates) don't push higher, ratcheting up the pressure on the economy in the months and years to come.

Powell has an interesting choice here on whether to push back on the market's forceful rally or to let traders know in no uncertain terms that they cannot expect a bailout from the Fed. My guess is that the Fed is once again forced to crush markets' dreams of a pivot, especially if my views regarding early indicators of inflation end up being shared by the FOMC. Remember that markets are reflexive – the economic conditions for today's rally were set by tighter financial conditions in the fall that led to better inflation numbers. In turn, the conditions for the selloff in October were set by the panic rally in risk assets over the summer that the Fed had to crush at Jackson Hole . The more the market bets on a Fed pivot, the less likely it is to happen, and vice versa.

SPY and S&P 500: Valuation and Fundamentals

What's a bit weird about the current market rally is that it's come in the face of worsening estimates for earnings. There's some cognitive dissonance here. Consumers are very pessimistic about the economy, but they're collectively spending over 100% of their monthly income. Similarly, a recession is widely expected, but the way stocks are priced is indicating near-exuberance about future earnings prospects! Stocks are priced as if the Fed pivot has already happened.

Stocks like Kimberly Clark (KMB) have reported that sales are up, costs are up, and volumes are down, indicating pressure on profit margins and unit sales. Microsoft ( MSFT ) laid off 10,000 and warned about the macroeconomy in its quarterly conference call , leading to whipsawing action in the stock after hours. Broadly, the S&P 500 trades for about 18x 2023 earnings estimates , which has only happened twice in the last 50 years, during the tech bubble and during the 2019-2022 bubble. In reality, these earnings estimates are including consumers spending excess savings, so they're about 10% too high.

Based on the actual earning power of consumers and normalized post-pandemic profit margins, stocks are trading for about 20-21x earnings, which is close to the bubble highs in late 2021. I've written at length about some of the structural issues (deficits, debt, demographics) that are going to drag down earnings growth going forward, but you don't even need those to understand that the S&P 500 isn't offering much compensation for 2023. The S&P 500 should earn about $195 for 2023 as margins continue to shrink without fiscal stimulus propping them up. This sets up the conditions for the S&P to fall 20-25% in 2023.

Fortunately, as an investor, you don't have to participate in this madness. Cash is paying 4.5% now and will be paying 5% or more soon. Incoming inflation data may force the Fed to hike even more, pushing rates up to 5.5% or higher. Stocks are likely to return 8%-9% in the long run at current prices, so you can get two-thirds of the return of stocks with none of the risk, as well as the option to buy in when the "stuff" eventually hits the fan. Cash is your best hedge against inflation here because if CPI comes in worse than expected over the next few months, then the Fed is likely to respond by hiking rates more.

Key Takeaways

- January has seen a furious rally for stocks. The rally is driven mainly by P/E multiple expansion and Fed pivot hopes – not improved earnings prospects for stocks.

- Stocks are priced near bubble highs, which makes no sense given that money market funds are closing in on 5% yields. Housing is still in a bubble, although pressure is rapidly building with prices falling and existing home sales plunging to 2008-era lows.

- Inflationary pressures in used cars, commodities, and services are building while financial conditions remain loose, pushing hopes of a Fed pivot out of reach.

- On a macro level, US stocks are still broadly overvalued after the pandemic everything bubble, although there are a few deals to be had in individual names. International stocks ( VEA ) are better, but you still are likely to get better entry points ahead when financial conditions tighten.

- Pivot mania 3.0 will likely end the way the first two rounds ended, with the market sobering up and catching a cab home to new lows after more data comes in.

For further details see:

SPY: The Market Is All In On A Fed Pivot - Will Powell Call The Bluff?