CA - SQM: Slight Dividend And P/E Advantage For Investors Vs. Albemarle

2023-04-13 16:39:47 ET

Summary

- With the more than 50% decline in lithium prices, from all-time highs, lithium mining stocks have taken a beating, making this a good potential entry point for investors.

- After examining large lithium mining peers Albemarle & SQM, I decided to invest in both, since there are some potential advantages as well as risks associated with either one.

- The global lithium market is likely to see tightening in the near future, which should help to stabilize the price near current levels, after which a rebound in lithium prices is likely.

- SQM seems like a slightly better bet, on a higher dividend, as well as a slightly lower P/E.

Investment thesis: The recent decline in lithium prices of more than 50% from recent highs is arguably creating a favorable window of opportunity for investors to start building a position in lithium miners or to add to their already-existing positions. As I already highlighted in a recent article, I decided to take up a small, cautious position in lithium mining startup, Lithium Americas (LAC). Startups come with added excitement as well as a higher risk profile. I tend to keep such investments to only a very small portion of my overall stock portfolio, with well-established companies, a proven track record, and solid finances being my preferred choice for the bulk of my positions. In light of this, I recently bought SQM (SQM) and Albemarle (ALB) stock. I decided to buy both because both offer unique favorable opportunities and they each have their own unique risk profile. Having both in the portfolio amounts to reduced risk, and both companies have a proven track record of putting in solid financial results on the back of the high lithium prices we saw last year. SQM is emerging as a slight favorite in my view, due to its generous dividend. Overall however I favor diversifying my lithium position by investing in multiple companies.

Albemarle & SQM both saw solid financial results last year

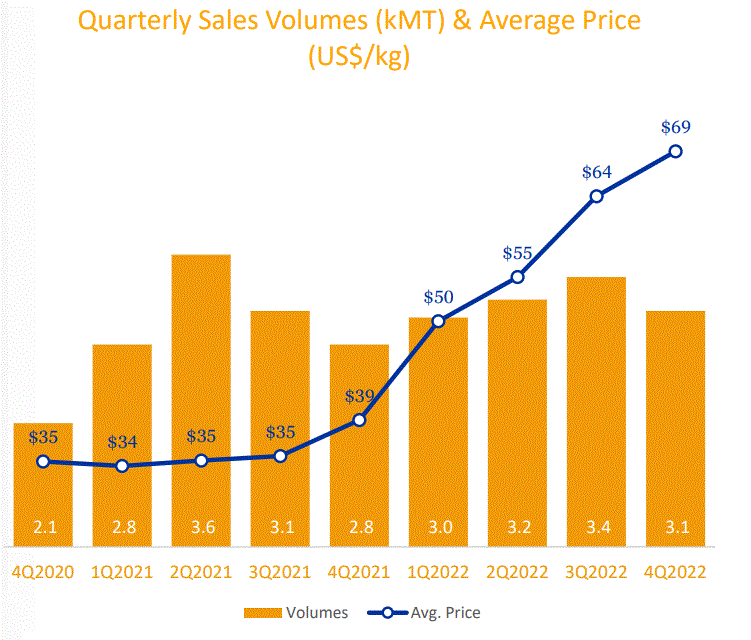

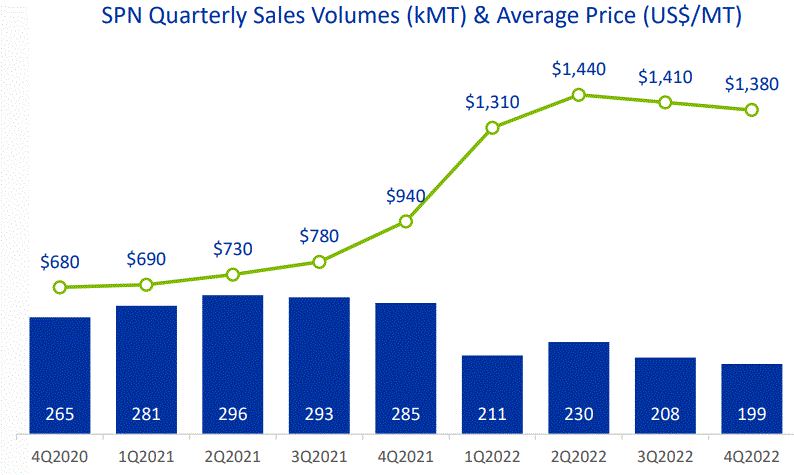

Albemarle's full-year financial results were impressive all around, with revenues coming in at more than double 2021 levels. SQM similarly saw impressive 2022 results . Its revenue was up about triple compared with 2021. More impressive for both were the profit margins. Both of them similarly achieved profit margins of just under 37%.

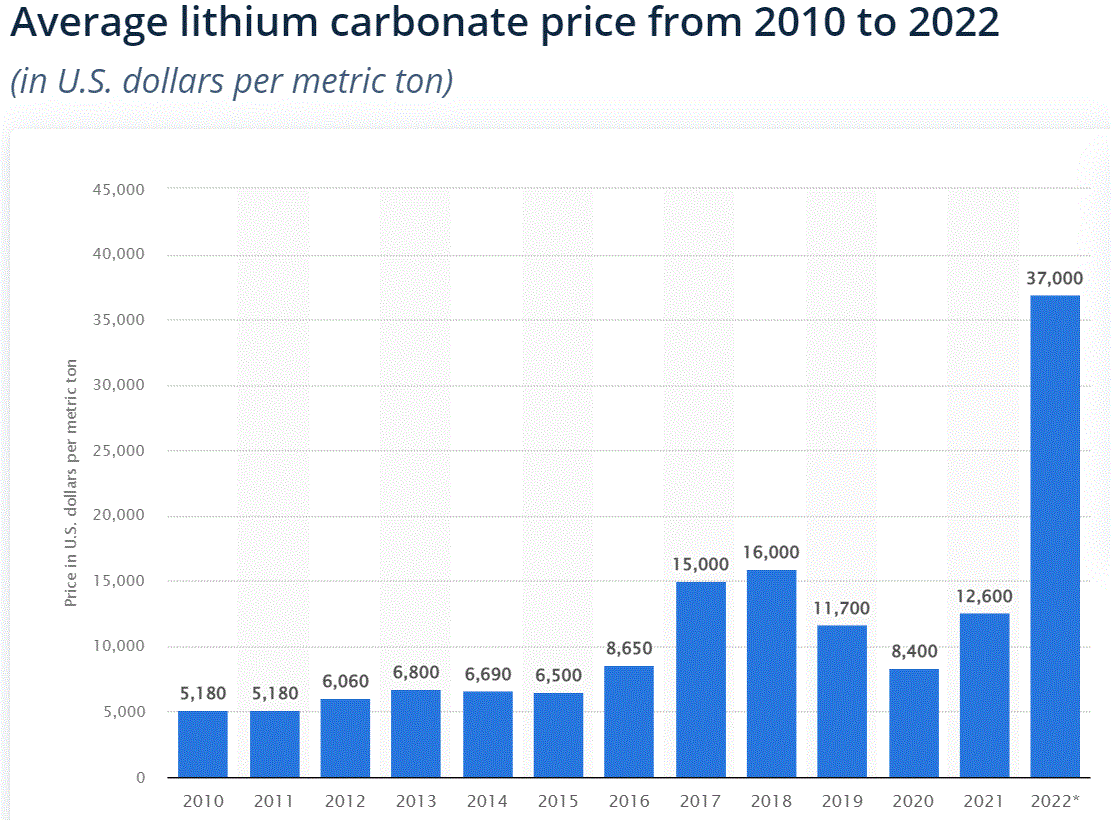

By far the biggest contribution to the stellar financial results, which helped the stock price of both companies achieve all-time highs, has been the lithium carbonate price spike.

{kind=link}

If we look at the longer-term stock price evolution of lithium mining producers such as Albemarle and SQM, we see that their stock performance is very closely tied to the lithium carbonate prices we see expressed in the yearly averages above.

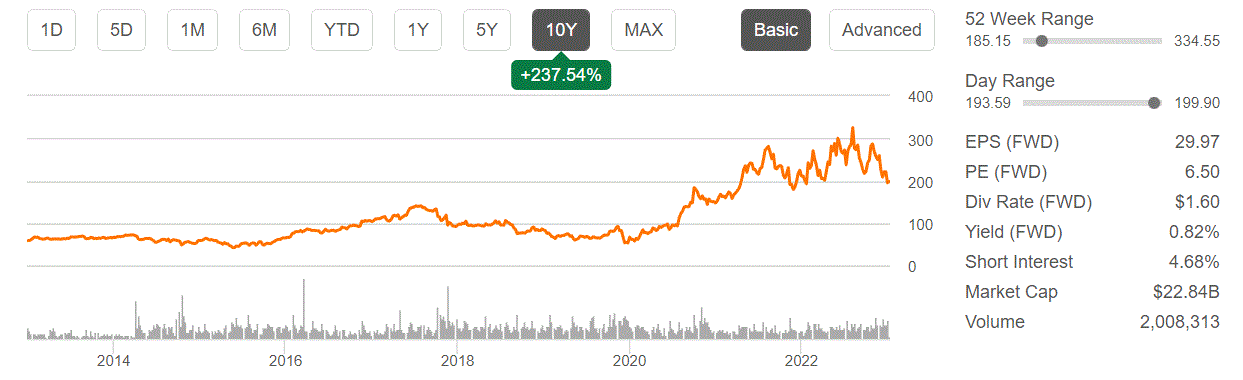

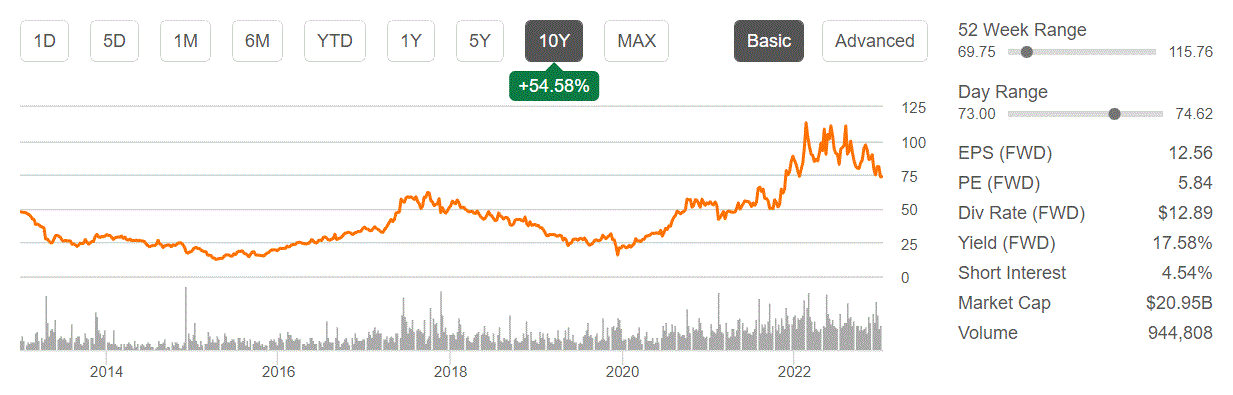

Albemarle financial metrics & stock price (Seeking Alpha) SQM financial metrics & stock price (Seeking Alpha)

{kind=link}

{kind=link}

There is some variation in terms of the stock performance of the two lithium mining giants in relation to lithium carbonate prices, and there is a very obvious discrepancy in terms of the magnitude of stock price gain of over 200% for Albemarle over the past decade, compared with SQM's gain of just over 50%. Having said that, it is clearly the case that lithium prices are by far the main determining factor in terms of their respective stock performances.

It should also be noted that while SQM's stock price performance has been far inferior to Albemarle's, it does not make it a potential repeat underperformer for the next ten years. Those financial results came in impressive, in some ways matching Albemarle in terms of profitability improvement on the previous year and so on. There is also the very generous dividend that SQM currently pays, which essentially provides a 100% return within about seven years if the dividend is reinvested in SQM stock. Albemarle's dividend on the other hand offers a 100% return over a roughly 35-year period if compounding is factored in. In other words, its stock price has to perform significantly better than SQM's stock if it is to provide investors with similar returns.

Between the far more generous dividend and the slightly lower P/E ratio, SQM offers investors arguably better long-term return potential compared with Albemarle and most of its peers.

{kind=link}

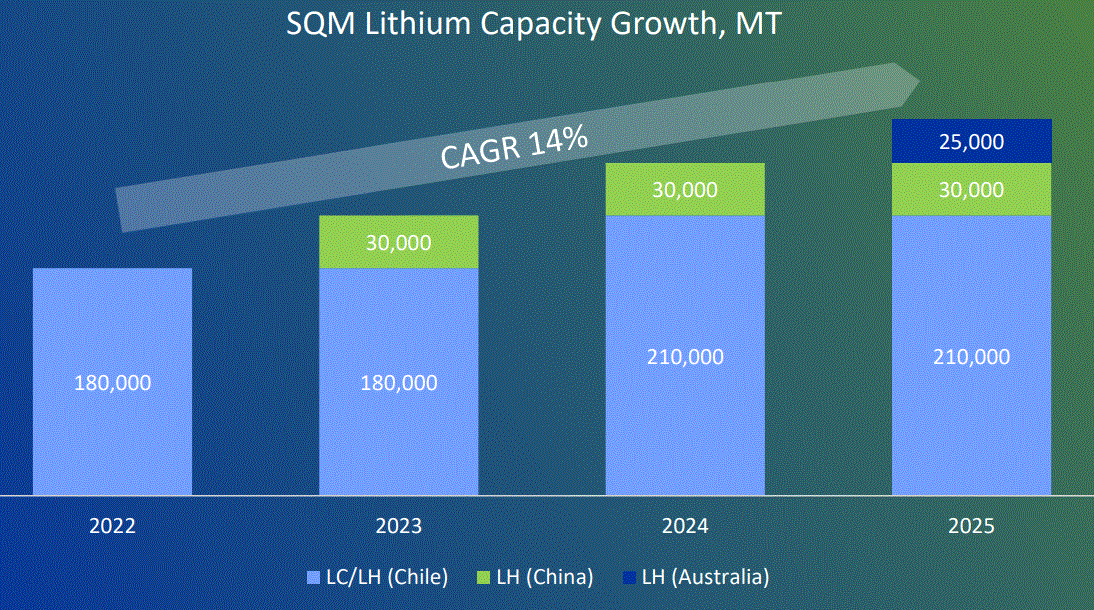

Its production growth profile is also very attractive with a roughly 50% increase in production expected by 2025, from 2022 levels. As we can see, the sources of production are also becoming more diversified, which is always a plus, especially in today's environment of growing geopolitical instability. The location of its sites is by no means low-risk from a geopolitical perspective. There is a rift between the US & China which could leave a company like SQM caught in the middle. Chile, like much of South America, has been prone to political instability in the past decades. it is stable now, but we never know what the future might bring.

Just like Albemarle , which I covered more extensively in the past, SQM also does have other business segments aside from lithium, which I find to be a desirable aspect of the company's profile. Production in its other segments may be largely stagnant, but the price has been trending largely higher.

{kind=link}

Its iodine segment makes up about 7% of its overall sales volumes as of 2022. The average sale price of iodine has been trending up, contributing to the stellar financial results that SQM saw last year. This year, it could potentially help to contribute in terms of some revenue and profits stability, in the face of what could end up becoming a challenging year for lithium producers.

{kind=link}

I am personally somewhat disappointed to see the declining trend in SQM's fertilizer production. It is a segment I feel that it has strong long-term potential for the rest of the decade, with factors such as the collapse of the EU fertilizer industry potentially benefiting producers elsewhere. It also has a potassium segment, which together with its specialized fertilizer segment presented in the above chart, makes up about 15% of revenues as of last year. SQM also has a specialty chemicals segment that makes up about 1-2% of revenues. These extra segments are a desirable feature in my view, which can provide the company with some extra stability, but clearly, its future is mostly tied to the lithium market and its future prospects.

The long-term lithium supply/demand outlook, without the hype

Given the exponential growth in global EV sales over the past decade, it is very easy to get caught up in the lithium market growth hype. While it is true that global lithium supplies and demand are both set to continue to grow exponentially for at least two more decades, it is important to nevertheless recognize any unrealistic assumptions that are baked into the forecasts.

For instance, there are still expectations for lithium to play a major role in renewable power storage for commercial grids. I personally see that as very unrealistic, because it lacks practical purpose. Such batteries can close the power generation gap for perhaps a day or a few days at most. As we have seen in the EU in 2021 , where there is already a growing reliance on intermittent sources of energy such as wind & solar, sometimes significant shortfalls may last for entire months. Green hydrogen, which will be stored and transported wherever it may be needed to feed hydrogen turbines is the more likely choice for green grid stabilization.

Some of the forecasts for EV sales also seem to be unreasonable. For instance, Goldman Sachs is forecasting 16 million EV sales per year in the EU by 2040. Total auto sales currently tend to never reach that level. Furthermore, if by 2040, only EVs will be available on the market, many Europeans will probably opt to give up on driving altogether, rather than purchase an EV that will only suffice for their city driving needs, given their lack of buying power needed to buy an EV with enough range to meet other needs.

We should also keep in mind that Europeans are becoming poorer compared with American consumers, as well as compared with others around the world. For instance, In Germany, the EU's largest auto market, average net monthly wages are about 70% that of average American monthly net wages. In France, the EU's second-largest market, wages are only about 59% of American Wages, with Italy's wages, which is the third-largest EU auto market, only reaching about 40% of average American wages. Auto sales per capita will probably continue to decline in Europe for the foreseeable future. Based on these factors, the 16 million EV sales per year expectations for the EU are likely a roughly 100% overstatement in terms of the volume of EV sales that is possible or probable in that particular market.

{kind=link}

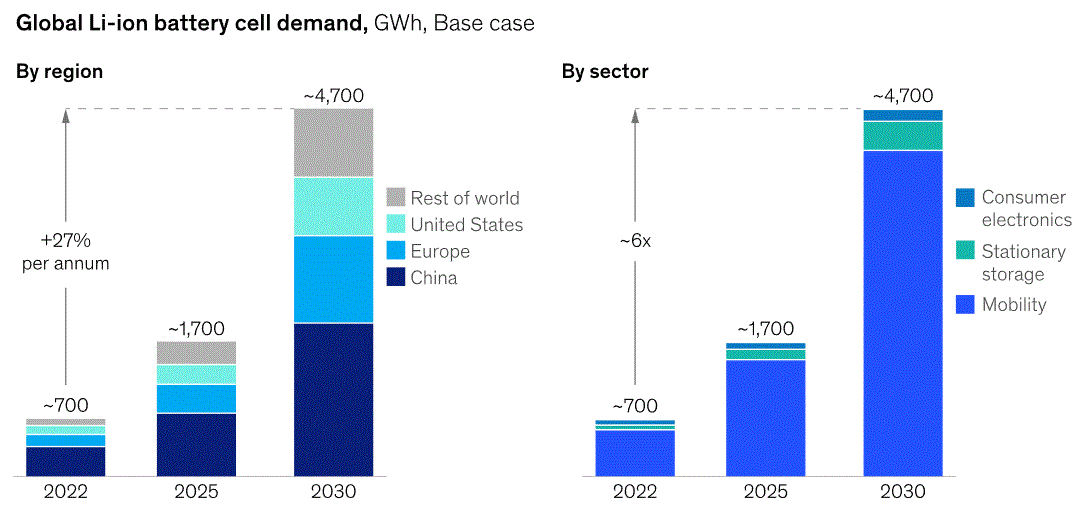

The market is currently expecting a roughly sevenfold increase in lithium battery cell demand between now and 2030. There are reasons to doubt such a robust rate of growth going forward, but even if the increase will be fivefold instead of sevenfold, it still makes this one of the most robust growth industries on the planet currently. It nevertheless helps to keep a realistic view of it all.

Investment implications

Given the fact that lithium mining might be one of the fastest-growing industries on the planet for the rest of this decade and perhaps beyond, the current decline in lithium stocks can only be seen as a great opportunity to invest in lithium producers, which only comes around perhaps a few times in a decade. It is possible that we will see another leg down in lithium prices, therefore also in lithium miner stock prices. For that reason, I bought lithium miner stocks with some constraints, keeping in mind that there may yet be an opportunity to add more at a more favorable price.

SQM & Albemarle, in particular, are attractive, because they have a solid proven track record of producing lithium carbonate at a profit, even in years when lithium prices were below current levels. I also bought some Lithium Americas stock recently, which is a startup on the verge of starting lithium production, with some potential. However, the lithium market, while overall I see it as mostly going strong this decade, will also be volatile, with wild price swings along the way. For this reason, Albemarle and SQM seem like the more conservative bets that I am personally more comfortable with building a long-term position in. SQM seems like the better bet, mostly on the higher dividend, but within the context of rising volatility, whether economic, financial or geopolitical, it is wiser to stay as diversified as possible.

For further details see:

SQM: Slight Dividend And P/E Advantage For Investors Vs. Albemarle