ET - SRV: This Midstream Energy Fund Fights Inflation And Yields Over 16%

2023-04-21 17:35:30 ET

Summary

- SRV trades at a -12% discount to NAV and offers a 16.5% yield based on a monthly distribution.

- The fund changed names after the employees of Cushing Asset Management bought out the company in 2022 and changed the name to NXG.

- The total return over the past 1-year period has exceeded other similar midstream/MLP funds and offers a much higher yield.

While many are now worried about a recession, the effects of rising inflation have not gone away. Although the pace of inflation has slowed somewhat to about 5% in March, the rising prices that impact everyday consumers are still going up, just not as quickly. In fact, in the post-pandemic economy higher prices are here to stay, at least according to one news source.

Analysts say some of the key drivers of the post-pandemic spike in inflation, like supply chain issues and the elevated food and energy prices spurred in part by the war in Ukraine, are abating. But the flames of inflation are nevertheless being fanned by a still-hot job market, which has added 1 million positions in 2023.

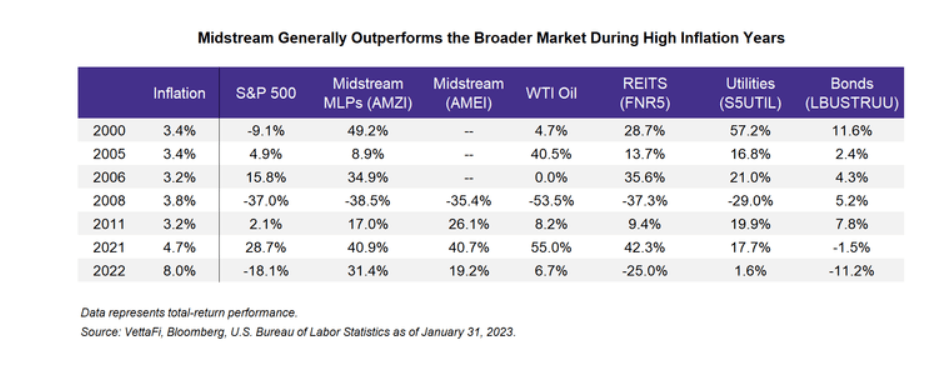

During inflationary times, one asset class that tends to outperform includes "real assets" such as energy infrastructure including pipelines and other midstream assets. In fact, inflation can provide tailwinds for midstream companies that transport energy such as oil and gas via pipelines. That is because midstream companies provide services for fees under long-term contracts which typically include annual inflation adjustments enabling them to raise their fees. Those increasing rates generally outpace the rising costs of operations generating higher profits.

{kind=link}

As I have discussed in other recent articles regarding real assets such as energy infrastructure, these companies generate consistent, recession-resistant high yield income as well from those increasing rates thereby offering investors an opportunity to participate in the passive income stream. One such opportunity to invest in high-yield midstream energy companies is available from the NXG Cushing Midstream Energy Fund (SRV). In January of this year, the fund announced that effective April 3 it would change its name from the Cushing MLP & Infrastructure Total Return fund. The change from MLP & Infrastructure to Midstream is a subtle change and further detail is included in the announcement.

Effective as of April 3, 2023, the Fund will pursue its investment objective by investing, under normal market conditions, at least 80% of its net assets, plus any borrowings for investment purposes, in a portfolio of midstream energy investments. The Fund considers midstream energy investments to be investments that offer economic exposure to securities of midstream energy companies, which are companies that engage provide midstream services in the energy infrastructure sector, including the gathering, transporting, processing, fractionation, storing, refining and distribution of natural resources, such as natural gas, natural gas liquids, crude oil refined petroleum products, biofuels, carbon sequestration, solar, and wind . The Fund considers a company to be a midstream energy company if at least 50% of its assets, income, sales or profits are committed to, derived from or otherwise related to midstream energy services.

NXG Investment Management

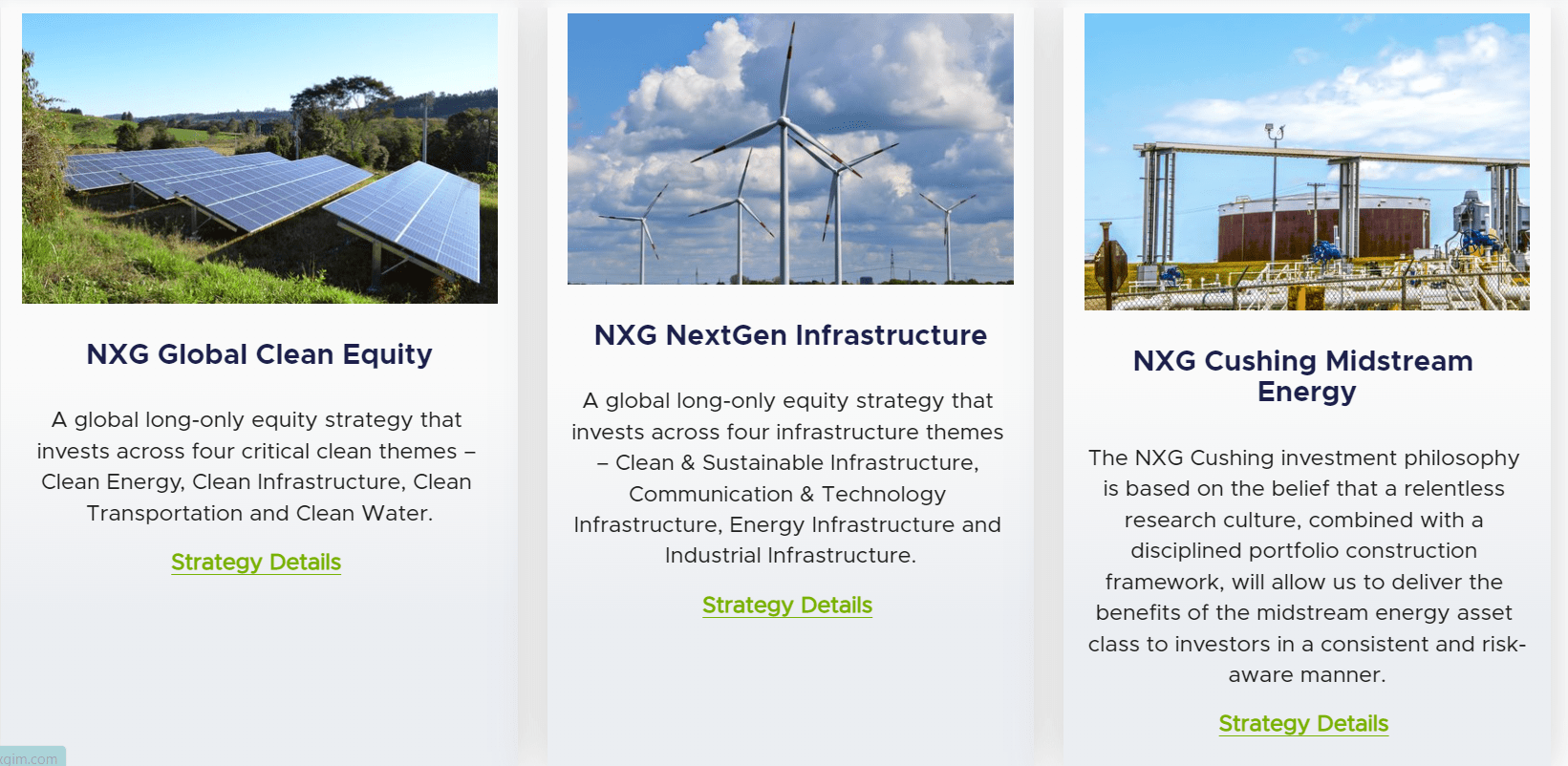

The other change in the name includes the addition of the NXG prefix. There is also a sibling fund called the NXG NextGen Infrastructure Fund (NXG), which formerly had the ticker SZC. I was curious about the change from Cushing to NXG Cushing. I learned that NXG Investment Management is a newly formed organization created in March 2022 when the employees decided to buy out the firm formerly known as Cushing Asset Management.

NXG Investment Management is an independent investment management firm managed by its employees. In March 2022 the employees agreed to purchase the firm from its founder and rebrand under "NXG Investment Management" to better reflect our focus and commitment to a "next generation" of investment ideals.

The focus of NXG Investment Management is to provide next generation investment strategies based on long-term growth in companies with a focus on sustainable and clean energy as well as traditional and transformational infrastructure companies.

{kind=link}

Apparently, the rebranding is still in the works because some of the links to web pages do not work and there is not a lot of information available about the company. I did find the LinkedIn page for the CEO of NXG, Mark Rhodes that shows he became CEO in July 2022. He has this to say on his profile page:

I am the CEO of NXG. We are a global asset manager with a 20 year history in managing energy assets in the public markets. Our three investment strategies focus on providing the investment community an experienced team with a deep commitment to fundamental research complemented by our proprietary Rmap technology. We invest in traditional, renewable and clean global energy public securities driven by a powerful secular theme.

From 2018 to 2020 there was a period of consolidation and conversion of MLPs followed by the Covid-19 pandemic which led to many midstream companies cutting way back on capex. Some midstream companies are not structured as partnerships and that may change the perception and the tax structure, but not necessarily the investment potential of the company, especially now that the cost of oil has risen dramatically in the last 3 years.

Cash flow generation for midstream operators and MLPs has grown substantially since 2020 due to the reduced capex followed by rising rates. The distribution coverage of many of these midstream energy companies has increased along with that cash flow growth as explained in this recent article :

Many MLPs still report distribution coverage each quarter, but it is easier to feel confident that MLPs can maintain or grow their distributions today than in the past. That largely stems from solid free cash flow generation in the space, which began in earnest in 2020 as capital spending fell meaningfully.

Furthermore, I noted that biofuels, carbon sequestration, solar, and wind are now included in the definition of midstream, whereas those types of companies would not have been considered previous to the NXG changeover. As of January 27, 2023, 92.42% of the fund's assets are invested in midstream energy investments, therefore, no substantial changes to the fund's holdings are expected. However, the changes do offer some leeway for fund advisors to look at investing in some alternative midstream opportunities in the future.

SRV Facts and Figures

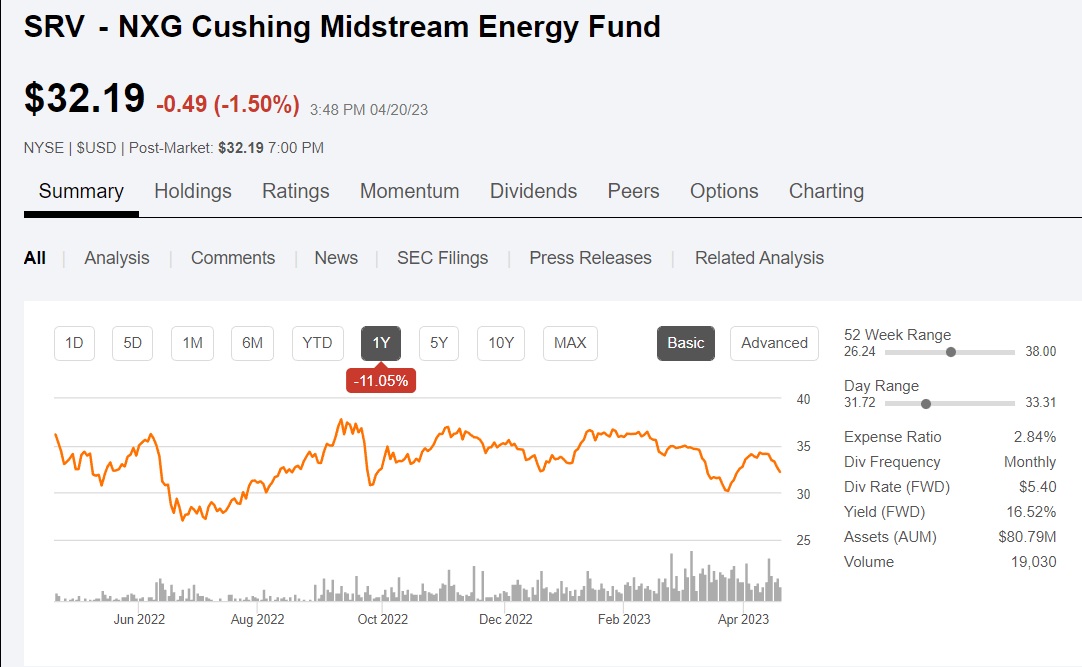

The fund is a relatively small CEF with only about $88 million in AUM, according to CEFconnect . One of my favorite fellow analysts on SA, Nick Ackerman, last wrote about SRV in February and he stated that the AUM was closer to $100 million at that time, while the SA summary page indicates that $80.8M is the current AUM.

{kind=link}

The most recent information available from the fund website is based on the Annual Report and is current as of November 2022. Therefore, most of the current information for this article is taken from CEFconnect, which states that the information is current as of 3/31/23. The fund basics indicate about 8% leverage and an expense ratio of 3.2% of which 1.65% is management fees.

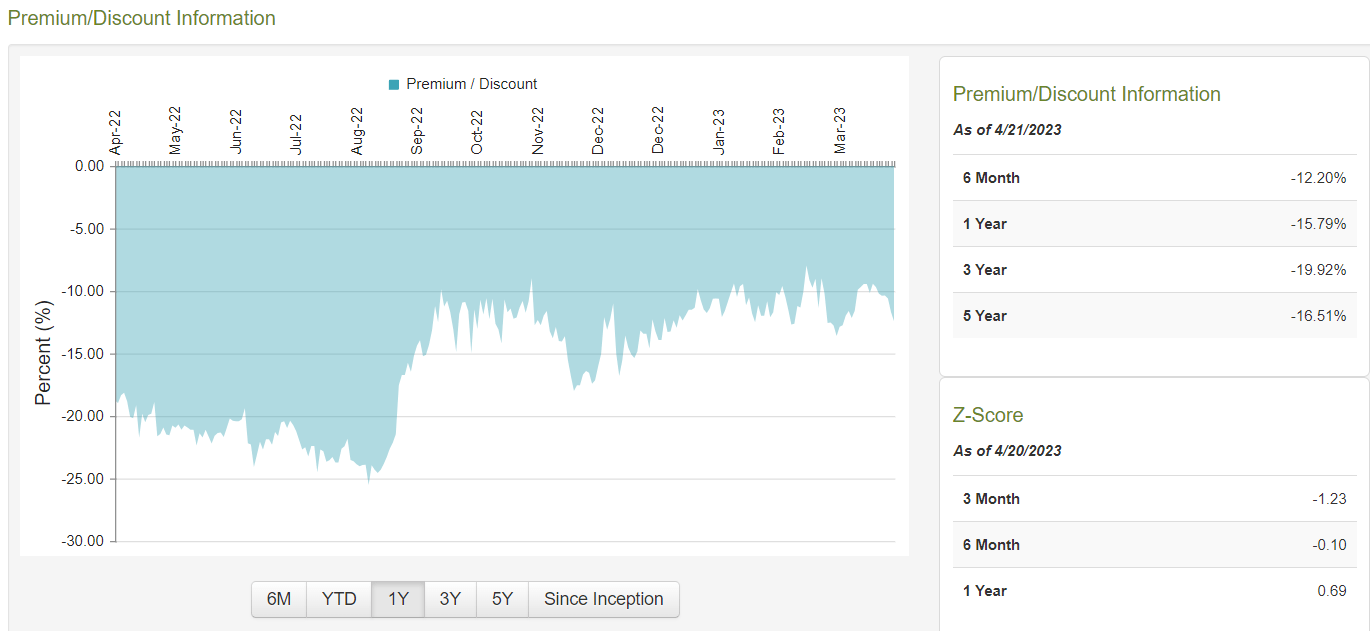

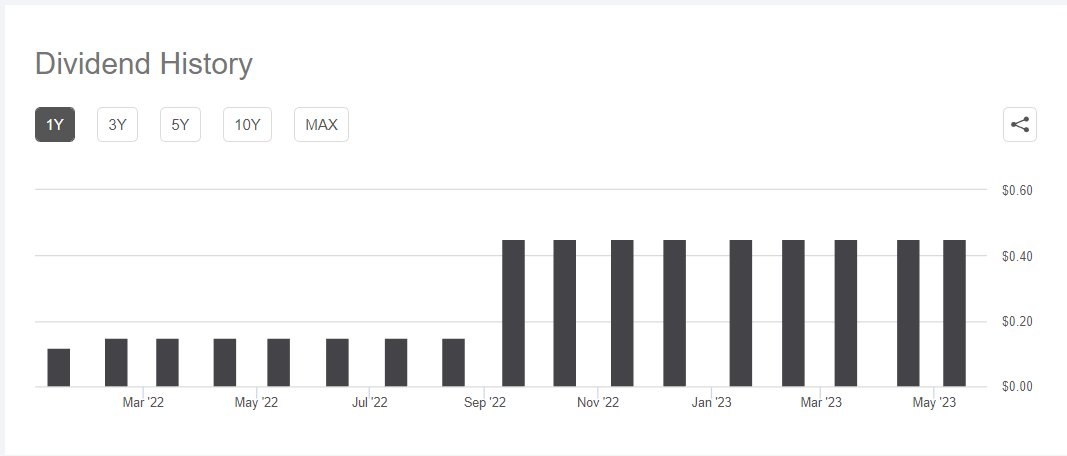

The fund currently trades at about a -12% discount to NAV, which is considerably less than the 3-year average discount of -20%. Back in September 2022, SRV announced a 200% increase in the distribution, from $0.15 per month to $0.45 per month. That caused the discount to narrow considerably, and the fund has traded essentially sideways for the past 6 months while paying out a 16.5% annual yield based on the current market price.

{kind=link}

In February, SRV announced further distribution payments of $0.45 per month for the months of February, March, April and May. The estimated ROC for each distribution is 86%. That may be beneficial to shareholders that hold SRV in a taxable account. It does not necessarily indicate that the fund is having trouble covering the distribution.

{kind=link}

The fund's top holdings as shown on CEFconnect still look a lot like an MLP fund. Many of these holdings are highly recommended for income-oriented investors. For example, Energy Transfer (ET) offers a 9.5% yield and has Strong Buy recommendations from 13 Wall St analysts. ET announced in March that they are buying another midstream company, Lotus Midstream for $1.45B.

Targa Resources (TRGP) has 14 Strong Buy recommendations from Wall St and recently raised the dividend by 42%. Cheniere Energy (LNG) has 15 Strong Buy recommendations from Wall St. Another top holding is Marathon Petroleum (MPC) which has provided investors with a total return of almost 500% in 3 years and nearly 600% since its Covid low. Williams Companies (WMB) is a natural gas pipeline company that has strong financials, a growing distribution, and potential for strong returns.

{kind=link}

Institutional Selling by Saba

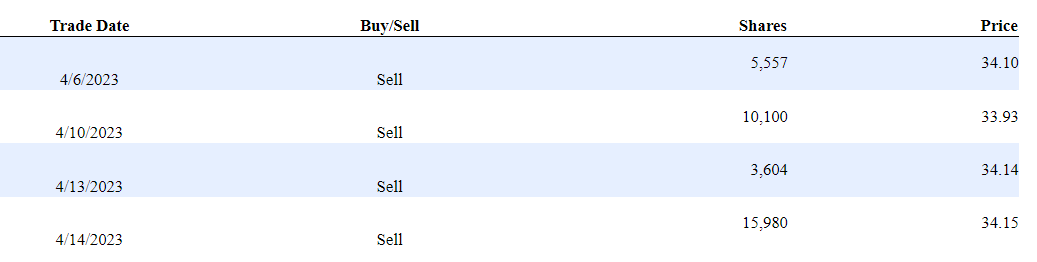

On April 14, 2023, form 13D/A was filed with the SEC indicating a change of ownership by Saba Capital Management. According to the form, Saba sold shares 4 different times during the month of April reducing their total holdings to 95,801 or about 4.4% of the total outstanding shares, which were 2,183,391 shares of outstanding common stock as of 11/30/22. The schedule of those transactions is shown on the form:

{kind=link}

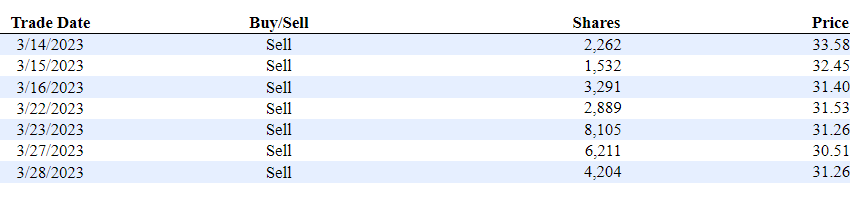

In a previously filed 13D/A on April 3, Saba sold shares based on the following schedule:

{kind=link}

On March 29, the form 13D/a showed more sales, and there were more sales previous to 3/14.

{kind=link}

For whatever reason, Saba has been systematically selling off shares and now owns less than 5% of the total outstanding shares of SRV. Perhaps they are using the capital gains from the sale of SRV shares to help cover the distribution in their Saba Capital Income & Opportunities Fund (BRW).

This could be interpreted as a potential negative for SRV, or it could simply be that Saba is adjusting their holdings to reduce exposure to midstream assets in 2023. Regardless, it is a data point worth considering if you are interested in an investment in SRV.

Comparison to Other Midstream CEFs

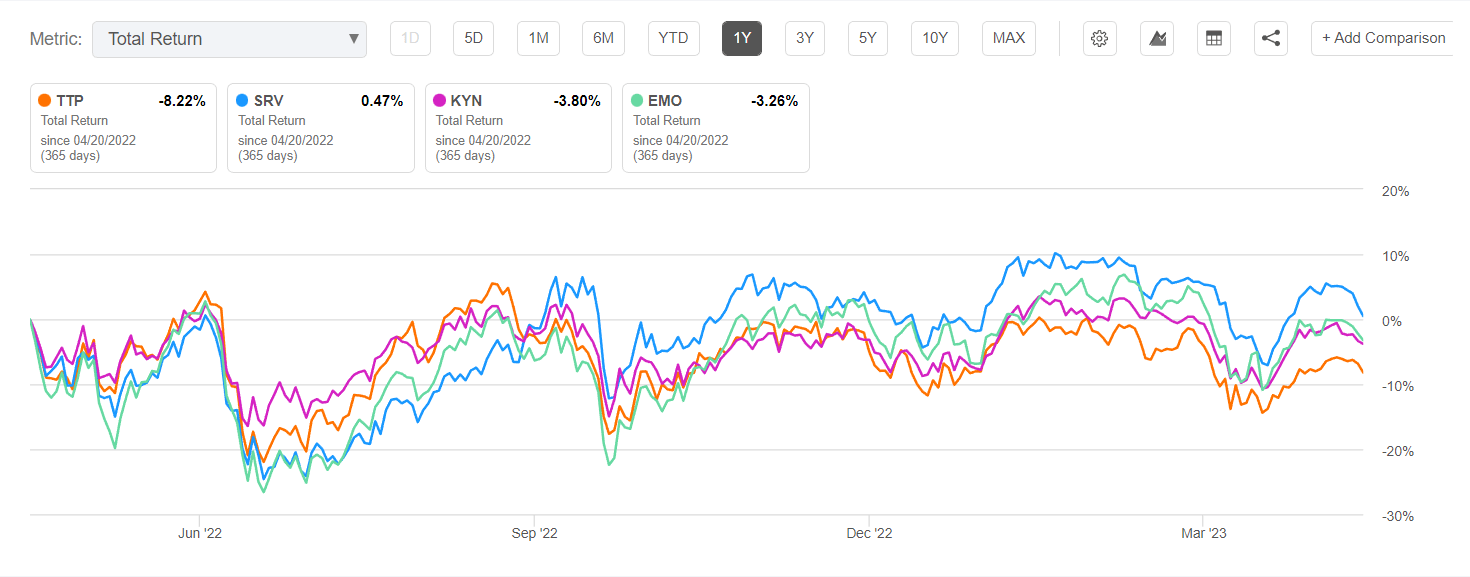

While the -12% discount to NAV and the 16.5% yield is attractive, SRV has a total return over the past 3-years, 1-year, and YTD that is comparable to several others in the category. For example, I have previously covered Tortoise Pipeline & Energy Fund (TTP), most recently in October 2022. At the time, they had announced a tender offer and I had expected that announcement to close the -14% discount that fund was trading at. Despite the tender offer, the shares of TTP now trade at an even wider discount of -18% and currently yields about 9% based on a quarterly distribution.

Another fund that holds midstream assets with similar holdings to SRV is the Kayne Anderson Energy Infrastructure Fund (KYN). That fund currently trades at a -15% discount to NAV and yields 10%, also paid quarterly. It uses about 27% leverage and has a fund expense ratio of 9.5% compared to SRV leverage of 8% and expenses of 3.2%.

And just to round out the comparison with one other midstream fund I have included ClearBridge Energy Midstream Opportunity (EMO). That CEF offers a yield of 7.5% paid quarterly and trades at a -15% discount to NAV. The fund expense ratio is similar to SRV at about 3.1% but uses over 32% leverage.

Comparing total returns over the past 1-year period shows SRV in the lead by a slight advantage over the other 3.

{kind=link}

Conclusion and Recommendations

If you are interested in an investment in midstream energy assets and, like me, are looking for a steady flow of high yield income for your retirement or just to cover everyday expenses, I suggest that you consider SRV. The fund has potentially more risk due to its smaller size and recent management changes, although the change to an internally managed fund could also be seen as a positive. SRV uses far less leverage than other similar funds and has a lower expense ratio than many of them. And it pays a much higher yield that is based on a monthly, rather than quarterly distribution.

{kind=link}

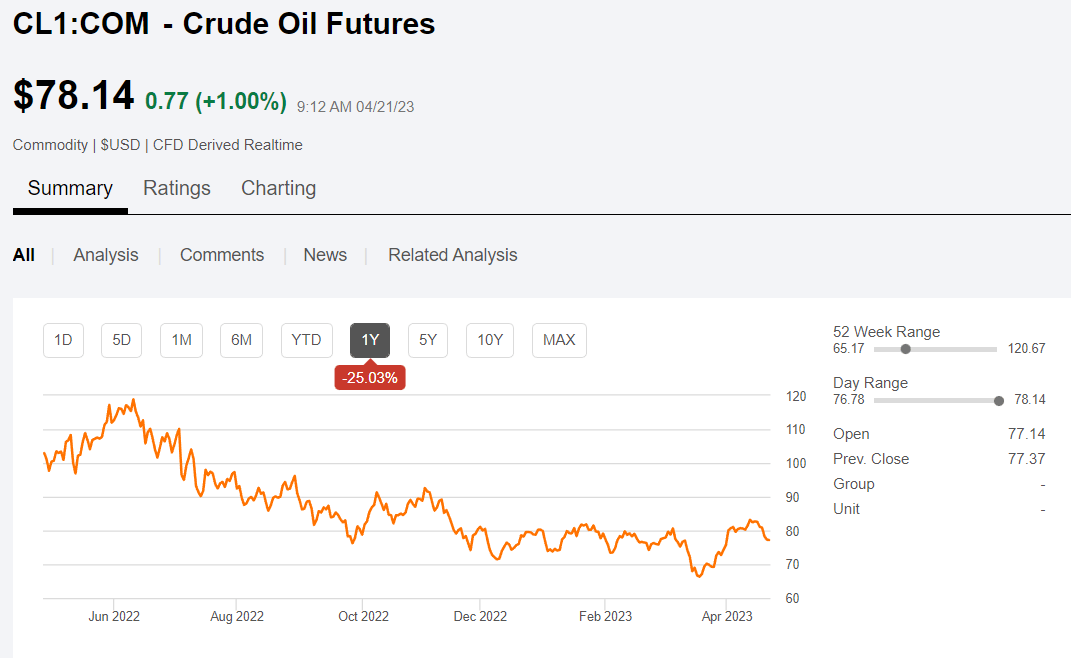

While the future is still very uncertain given the ongoing conflict in Ukraine and other geopolitical tensions, and the price of oil futures has declined over -25% in the past year, midstream energy assets still offer a reasonably low risk source of steady and even increasing income due to the reasons that I described earlier. At some point in the future the global economy is likely to recover and oil prices will most likely rise again.

{kind=link}

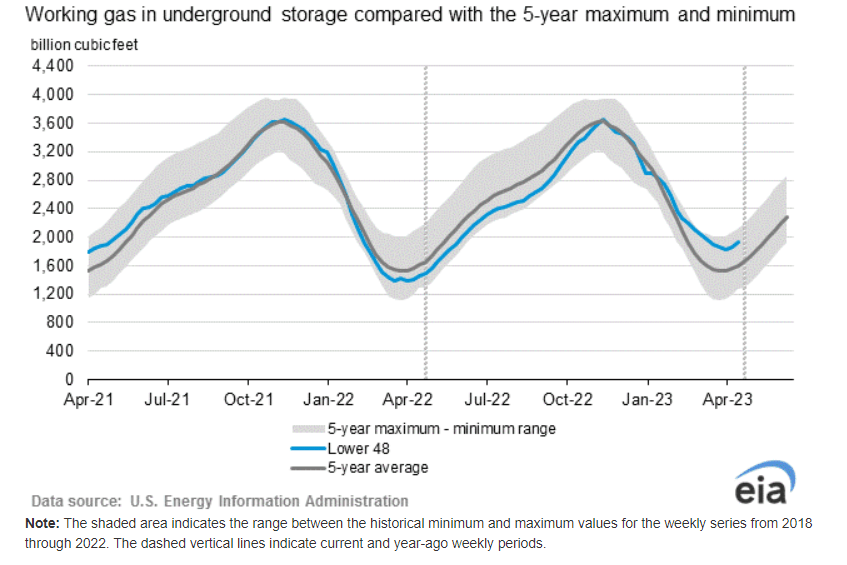

Natural gas prices have also seen an even more significant downward trend over the past year but may be close to bottoming out. Natural gas production is near all-time highs and according to the EIA natural gas storage is currently about 20% higher than the 5-year average. As the demand for electricity rises and natural gas continues to replace coal to power energy production the price is likely to rise again as demand evens out.

Renewable energy assets are also increasing as the demand for EVs, batteries, wind and solar, and carbon sequestration gain traction. At the Wells Fargo Midstream, Utilities, and Renewable Power Symposium in December 2022, the CEO of Magellan Midstream Partners, Aaron Milford, discussed how their company is positioned for the future and the opportunity it offers to investors:

We think we're going to be essential for a really long time. Even with the backdrop of energy transition, electric vehicles, batteries, alternative fuels of all varieties, we think that transition is going to continue. But as it continues, we're still going to be essential. We're still going to need crude oil, gasoline and jet fuel to run our economy.

So, as that happens, we think that the demand for the fuels that we deliver are going to -- is going to remain really steady for a really long time. And as the energy transition moves forward, whatever that may look like, we're still going to be essential even out in 2050 because we're still going to be needing the fuels that we deliver.

The long-term opportunity in income generation from real assets such as midstream energy infrastructure offers investors a steady flow of cash at lower risk relative to other asset classes, especially as inflation continues to impact pricing. The SRV fund offers an income stream of 16% annually paid in monthly distributions that have been declared at least through May. I rate SRV a Strong Buy.

For further details see:

SRV: This Midstream Energy Fund Fights Inflation And Yields Over 16%