CA - Stelco: More Free Cash Flow Coming +35% Net Cash

2023-11-28 07:00:00 ET

Summary

- Stelco boasts a forward free cash flow multiple of less than 5x, signaling an undervalued investment opportunity.

- The company's financial strength is underscored by a debt-free status and a substantial cash reserve, constituting +30% of its market cap.

- Stelco's commitment to shareholder returns is evident through consistent dividend payouts, including a recent special dividend.

Investment Thesis

Stelco (STZHF) is a Canadian steel company with a significant presence in the North American steel industry. As a key player, Stelco is known for its industry-leading low-cost structure, marked by operational efficiency. The company engages in the production of steel and has consistently demonstrated a strong financial performance, emphasizing shareholder returns through dividends and strategic initiatives.

An investment in STZHF is not a blemish-free investment thesis, given the innate cyclicality of the business, but there's still a lot to like from this very cheap stock.

According to my estimates, the stock is priced at less than 5x forward free cash flow. Also, the business holds no debt, and about 30% of its market cap is made up of cash.

And on top of all that, management has a strong predisposition towards returning significant capital back to shareholders. However, the capital return cycle is far from guaranteed.

There's a lot to like here, so let's get to it.

Rapid Recap,

Back in May, I said in my bullish analysis ,

I've assumed that Stelco's total EBITDA in 2023 will reach CAD$500 million. Meanwhile, assuming that the capex figure reaches CAD$180 million, this means that Stelco's free cash flow this year reaches CAD$320 million.

Author's work on Stelco

As it transpires, I was wrong to be bullish, since the share price is down 9% (including dividends). But the irony is that the free cash flow is actually going to end higher than my estimate of US$320 million, and closer to US$330 million.

We have a lot to get through, so let's get to it.

Stelco's Near-Term Prospects

Stelco is known for its industry-leading low-cost structure. Notably, the company has maintained the highest steel EBITDA margin in the entire North American reporting steel industry for 10 out of the last 12 quarters, underscoring its consistent performance since the completion of a crucial blast furnace upgrade project in 2020.

Furthermore, Stelco's management, led by Executive Chairman and CEO Alan Kestenbaum, emphasizes a shareholder-centric approach, exemplified by its very high dividend in the most recent quarter, but also, through its history of share repurchases.

For example, Stelco's return of capital to shareholders totals over $2 billion since the company's IPO in 2017, reflecting a robust track record that stands out in terms of market capitalization percentages among North American reporting peers. As a point of reference, it's interesting to note that Stelco's capital return is higher than its current market cap.

That being said, there are some blemishes to be mindful of. One notable concern is the adverse impact of a deteriorating price environment that persisted for a significant portion of the third quarter in 2023. This challenging pricing scenario is reflected in an 11% decline in the company's average selling price over the second quarter, contributing to an 8% decrease in revenue quarter-over-quarter. The fluctuations in pricing have presented obstacles to achieving robust financial performance.

Additionally, the guidance for shipping volume in the fourth quarter, ranging from 600,000 to 625,000 net tons, suggests potential challenges related to absorption issues and slightly higher fixed costs.

Looking further ahead, Stelco is positioned to capitalize on an upward trajectory in steel prices and stable market demand.

The recent positive trends in pricing and demand, combined with ongoing operational efficiencies, are expected to contribute to improved financial results starting in 2024.

Moreover, I believe this quote from the earnings call neatly encapsulates Stelco's near-term prospects,

And to your question about lead times, which is always a great indicator to us. So we're sold out for Q4, and we are well on our way to selling out Q1, not so much in the March period, but January and February are getting filled up pretty rapidly. I have to tell you, I looked at my records that I keep going back to 2021, I don't have the data right beforehand, but we have never been this far out during November 9, this far around on our order book as we are right now at this time of the year.

[...] Typically, in the fourth quarter, things tend to drop off and get a bit depressed. This fourth quarter, I think, driven by the resolution of the auto industry strikes is different. So the order book is strong. I think the good news, bad news here is that when you look at Q4 pricing -- realized Q4 pricing, we're not getting the current, whatever, I don't know the last price increases were quoted up to $1,000 or something, we're not getting that. But we are -- in Q1, in late December, we are definitely getting, starting to see better prices. So I think it's very indicative of a very, very healthy market.

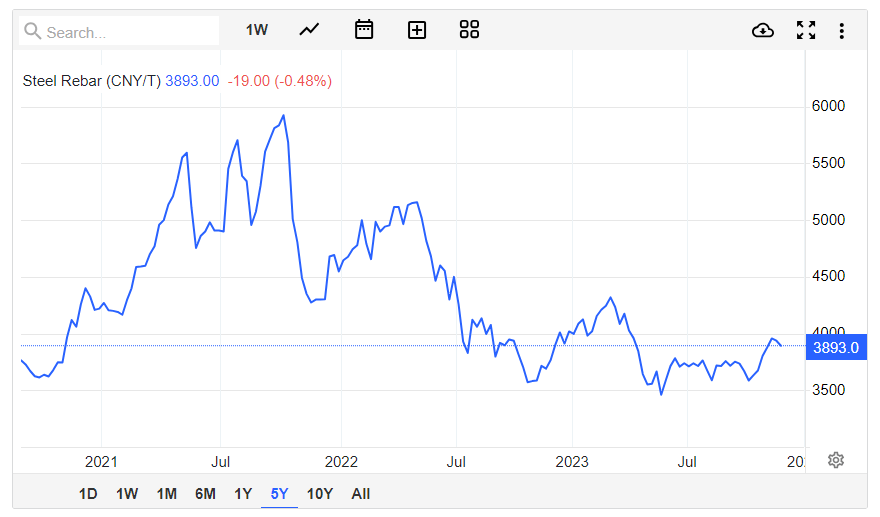

Similarly, the graphic that follows echoes that management's statement above.

{kind=link}

What you see above is shown in CNY per tonne rather than USD, but the overall take is the same. Steel prices have clearly stabilized and started to strengthen by late.

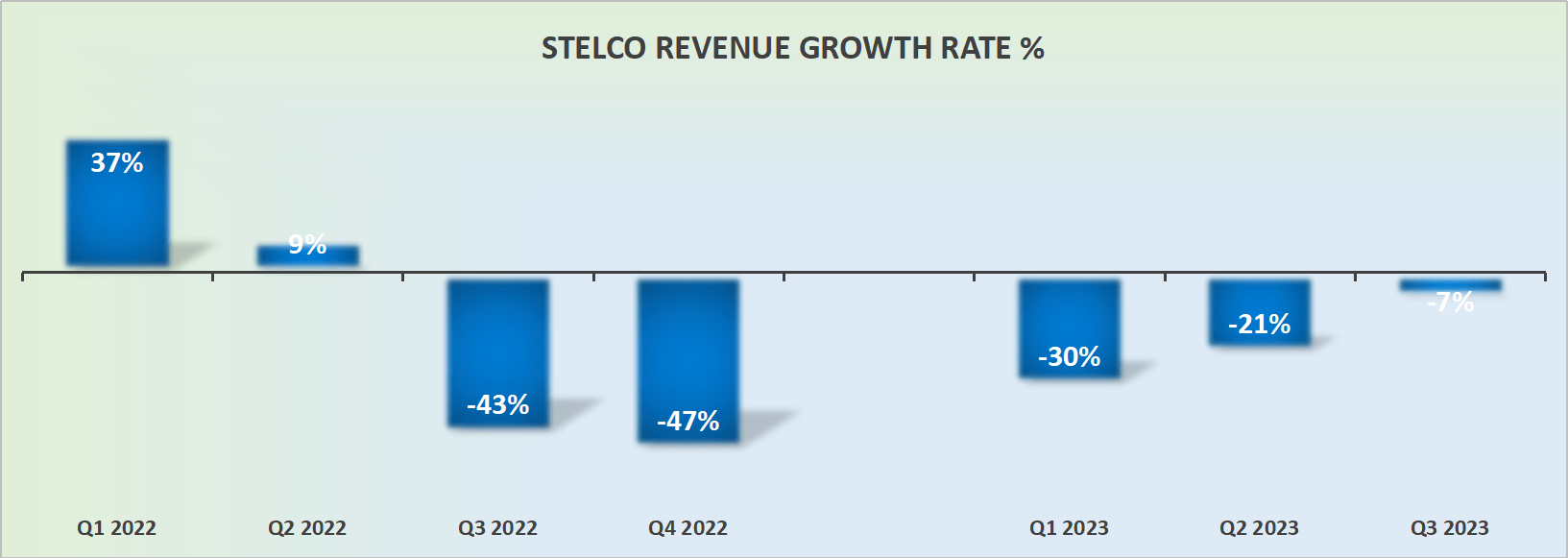

Revenue Growth Rates Should Stabilize

{kind=link}

Before we go further, keep in mind that Stelco's figures are reported in Canadian Dollars, while STZHF's market cap is reported in USD. Accordingly, the revenue growth rates shown above are reported in USD and will differ ever so slightly from Canadian figures.

For the trailing nine months of 2023, Stelco has reported negative y/y revenue growth rates. This will provide a much lower hurdle for Stelco to report positive revenue growth rates in 2024.

STZHF's Stock Valuation -- 5x Forward FCF

Anyone considering investing in a commodity company must spend some time to understand the strengths or weaknesses of a company's balance sheet. On this front, Stelco stands strong. Case in point, Stelco has no debt and substantial cash. More specifically, Stelco's market cap is made up of 30% cash, with CAD$840 million (approximately $615 million) of cash and no debt.

Furthermore, Stelco is in the process of paying out CAD$0.42 as a dividend, together with CAD$3.00 as a special dividend. Altogether, this meant that Stelco returned to investors CAD$3.42 (~$2.51 per share) this quarter, or a 7% total yield. Of course, the majority of this large dividend is a special dividend and investors shouldn't expect it to return again soon.

{kind=link}

According to my estimates, this year Stelco's free cash flow will be approximately CAD$450 million (approximately $330 million). This implies that Stelco is priced at about 5x this year's free cash flow. And if 2024 improves from this point, this multiple could fall to around 4x forward free cash flow.

Risk To Investing In Stelco?

Stelco is a lesser-known, modest-sized company, resulting in a relatively low trading volume.

As a result, there is restricted liquidity, deterring significant institutional participation in the stock.

Also, given its smaller size, Stelco's stock may be susceptible to substantial volatility.

The Bottom Line

In summary, Stelco presents a compelling investment case, particularly when evaluating its valuation metrics. With a forward free cash flow multiple of less than 5x, the company appears significantly undervalued. The absence of debt, a substantial cash reserve constituting +30% of its market cap, and a consistent dividend payout, including a recent special dividend, contribute to Stelco's strong financial standing.

As an investor, the attractive valuation coupled with the potential for improved free cash flow in 2024 positions Stelco as an intriguing opportunity. While acknowledging the risks associated with its smaller size and potential liquidity constraints, the company's valuation metrics underscore its potential for value appreciation, making it a noteworthy consideration in the investment landscape.

For further details see:

Stelco: More Free Cash Flow Coming, +35% Net Cash