PIPR - Stifel: Well-Rounded IB With Upside

2023-06-17 07:22:14 ET

Summary

- Stifel Financial Corp. is a financial services company that offers wealth management and investment banking services.

- AM fees and interest income have been a fantastic hedge against a decline in IB activities.

- Margins are good and stack up well relative to peers.

- Markets remain uncertain which will hold the business back, but once rates begin declining, we see rapid growth ahead.

- SF stock is trading at a discount to its peers despite what looks like a fundamentally superior business.

Investment thesis

Our current investment thesis is:

- Stifel's revenue stream is highly diversified, allowing the business to better ride the cyclical waves relative to its advisory-heavy peers.

- Margins are good, with a track record of sustainability. When compared to peers, the business looks strong.

- Stifel is trading at a discount to its peers despite the factors named, suggesting upside.

Company description

Stifel Financial Corp. (SF) is a financial services company that offers wealth management and investment banking services.

It operates in three segments, including Global Wealth Management, Institutional Group, and Other, providing private client services, institutional equity, and fixed income sales, trading and research, and investment banking services. Additionally, the company offers retail and commercial banking services.

Share price

Stifel's share price has performed well in the last decade, gaining over 150%. The business has done well to quietly grow its operations, generating improving returns for shareholders. The FY21 outlier year for transactions drove a large increase in share price, from which things look to have softened.

Financial analysis

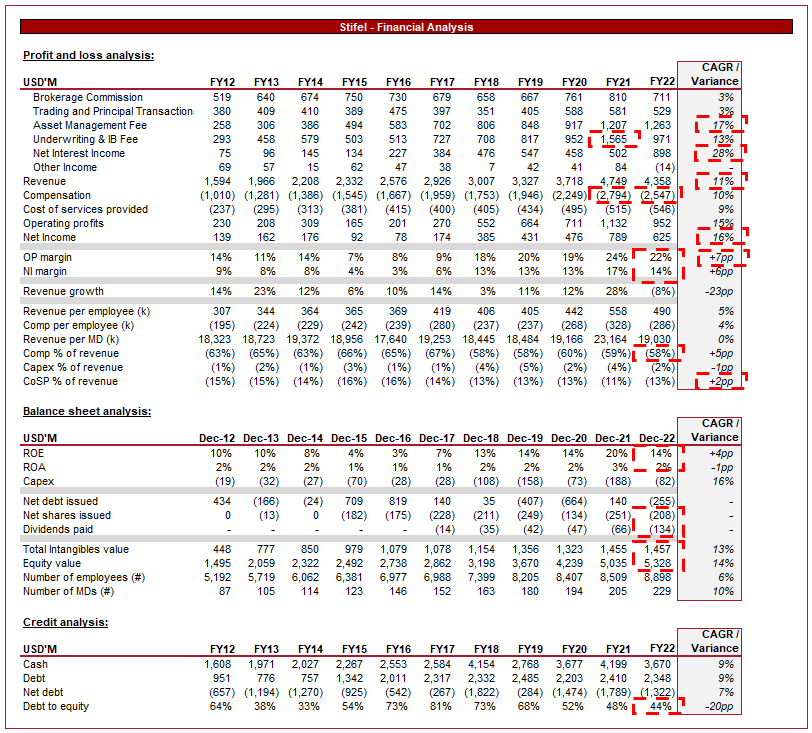

Stifel's financial performance (Tikr Terminal)

{kind=link}

Presented above is Stifel's financial performance for the last decade. The business has done a great job of growing across the board, reducing reliance on any one income stream.

Revenue

Revenue has grown at a CAGR of 11%, driven by growth across several of its revenue streams. Unlike many boutique investment banks, Stifel is highly diversified, with no single segment contributing more than 30% of total revenue.

This diversification is incredibly valuable for an investor as many parts of the investment banking industry are cyclical in nature. We are currently experiencing a bear market, driven in part by the heightened interest rates compared to the last decade. This has put pressure on the advisory business, which experienced a 38% decline in FY22. Despite this decline, Stifel's revenue only declined 8%, primarily become of growth in other areas, illustrating why diversification is so important.

Expanding further on the current bear market, interest rates increasing noticeably is a real issue for advisory. This is because as rates rise, the cost of capital increases. This leads to investors discounting a target's future cash flows at a larger rate, leading to a lower valuation. On the other side of the table, sellers are unwilling to sell their business at what they perceive to be a discount, knowing that rates will have to come down in the coming 12-24 months to avoid a serious economic downturn. This leads to a widening of the bid-ask spread in private markets, reducing the number of transactions. From speaking to PE professionals in the last few months, the impression I get is that the intention is to focus on improving their portfolio companies, only transacting if they see true value. Our view is that rates will likely remain heightened for another 6-12 months, during which time equity and debt activity could remain subdued.

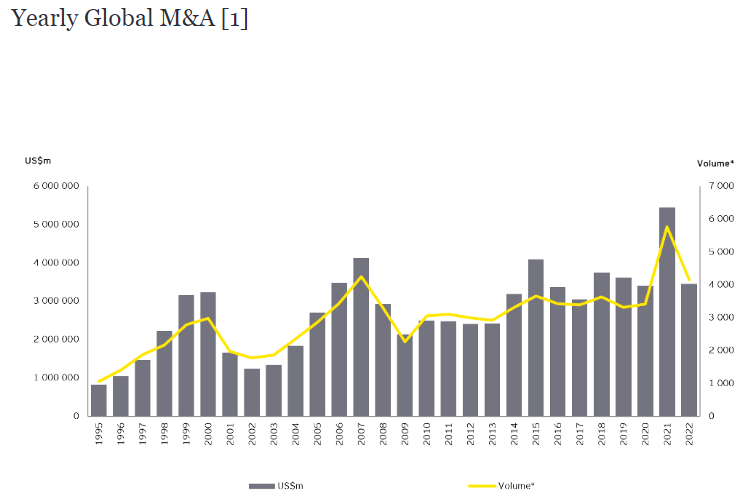

EY's view is that this market slowdown is attributable to uncertainty in the debt markets, as well as macroeconomic factors. As the following graph illustrates, the reduction in deal volume/value brought 2022 in line with pre-Covid years, suggesting we are not experiencing a capitulation but instead, as EY states, uncertainty.

{kind=link}

From Stifel's perspective, this likely means sideways trading during FY23, as we experience more of the same. If the business can achieve any growth, this would be quite impressive, as during such conditions, competition between banks increases.

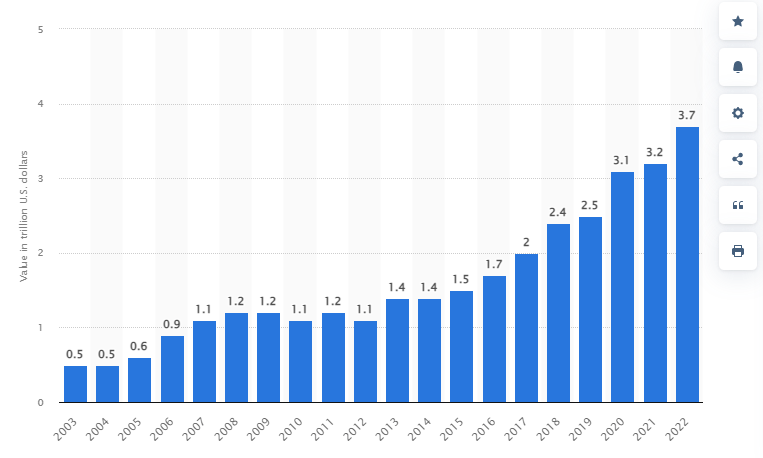

A factor that suggests we could see impressive long-term growth in advisory work is the level of dry powder currently in the market. Statista estimates the level of dry powder to be $3.7TN, a record level.

{kind=link}

The funds need to invest the money or face issues justifying fundraising while risking underperformance. This should act as a natural tailwind for the advisory business as a greater number of global transactions are made over time. Our view is that this will kick in once rates decline.

While on the topic of advisory, it may be worth touching on why revenues increased so dramatically during FY21. With a decade of lax monetary policy, and pent-up transaction demand during the initial pandemic period, corporates and PE firms came out in record numbers to transact, fueled by dry powder. The level of deal-making in the year was a record, as the graph above illustrates. Stifel did a good job of marketing its capabilities, partaking in the greater volume. A key value driver here was also deal size, which also trended up. This is because many within the bulge bracket and elite boutique cohort were unable to meet client demand, thus large deals were trickling down, benefiting the likes of Stifel.

Stifel's wealth management business is an important source of revenue for the firm, generating 29% of revenue in FY22. We like this revenue stream as it is recurring in nature while giving the business substantial cross-selling opportunities. Stifel has done a fantastic job in this segment, managing to grow revenue at an eyewatering 17%. A portion of this will be inorganic in nature but reflects the quality outperformance relative to its peers. Further, the recurring nature of the revenue allows the business to hedge against cyclical swings, as we note in FY22.

{kind=link}

What may be the most impressive of all is that revenue grew in FY22. With the bear market in mind, AUMs have declined across the board, even for the best asset managers. With fees linked to AUM, income growth must come from net inflows, which many have struggled with.

A segment of the banking industry that many IBs are arguably guilty of neglecting/avoiding is owning interest-bearing assets. This is understandable to an extent, as we've had a decade of record-low interest rates. Stifel, however, has quietly built its asset base, which is now bearing much fruit. Its current blended average interest rate is 5.43%, with a net interest margin of 3.57%. This has again helped to hedge the cyclical downturn we are experiencing.

Loan and NII growth (Stifel) Net interest income (Stifel)

As mentioned prior, our expectation is for rates to begin their decline in 6-12 months time. This means Stifel has a good runway to earn outsized interest and further build its loan book, with our view being that double-digit growth is possible from this segment.

Stifel's current loan and investment portfolio breakdown is as follows, with large exposure to real estate and CLOs. The valuation of both has trended up in the last year.

Loan and investment portfolio (Stifel)

With such exposure, credit risk is a continual factor. Stifel's reserve ratio remains flat across the period, all ACLs have trended up, especially for commercial real estate. There has been much talk in the news recently about large asset managers choosing to default on CRE , as the WFH culture reshapes the demand for CRE. This should be continually monitored.

Allowance for credit losses (Stifel)

One of the key drivers of revenue growth across its revenue streams is Management's focus on acquiring smaller firms to expand its service offerings and gain access to new markets / expertise. This is a fantastic growth strategy in the IB space as credentials are key, investors want to see that their advisors have the necessary track record to provide the best possible service. For this reason, acquiring successful sector-specific IBs allow Stifel to accelerate its penetration into key markets.

This factor is one of the reasons for the 10% growth rate in MDs during the period. The number of MDs is a key driver of revenue, as each member is essentially a P&L, responsible for contributing revenue and profits. In recent years, Stifel has done a good job of recruiting high-profile members from competing banks, winning their client book. This being said it is disappointing to see that revenue per MD has not materially increased, suggesting accretive gains are not being made.

MD numbers (Stifel)

Margins

Stifel has seen margin volatility in the historical period, primarily driven by changes in revenue mix and growth of the business. The general trend has been positive, however, with 5 successive years of OPM >15%.

The key cost for an investment bank is employees, as they are the drivers of revenue. Total costs have grown at a CAGR of 10%, which is dwarfed only marginally by revenue growth, suggesting the company's compensation packages are aggressive.

This said, revenue per employee has grown at a greater rate than compensation per employee, which is a key metric in our view as to whether Management is aligning compensation to shareholder interests. Overall, a compensation ratio of 58% is very good, our target would be anything under 63%.

Costs of services provided are all other cash costs to the business, which have also grown at a smaller rate to revenue, at 9%. This cost is not a substantial amount of the business and so finding efficiencies will naturally not be a priority for Management but there is scope for improvement here.

Overall, we like Stifel's commercial profile, as well as its margins.

Distributions

Management has achieved several years of consistent share buybacks and dividends. Our view is that this should be sustainable going forward, although the level will be dependent on financial performance.

Q1

Q1 (Stifel)

Presented above is Stifel's financial performance for Q1.

The company generated robust revenues, although NIM has slipped. This is due to the operational profile of the business. Stifel's Wealth Management division generated impressive growth, contributing to an expansion of margins. Conversely, its Advisory/IB business continues to decline as equity markets remain weak, leading to a sharp contraction in margins. As a large portion of costs are fixed in nature, margins will always swing with profitability.

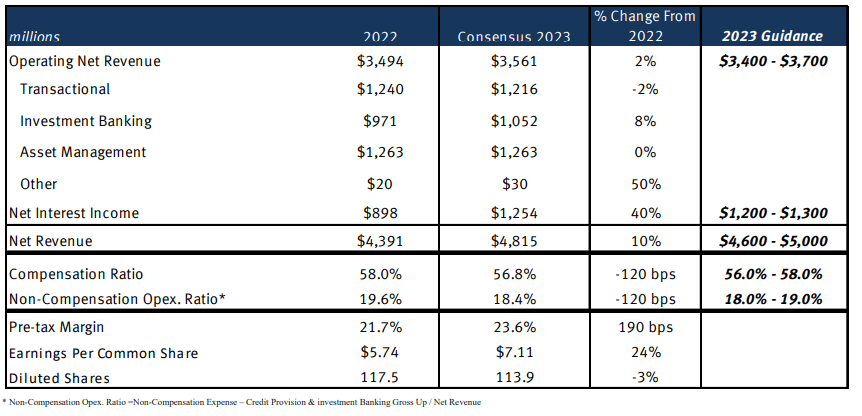

Outlook

{kind=link}

Presented above is the consensus Wall Street view of the business, alongside Management's guidance.

The company is expected to achieve c.10% revenue growth, primarily driven by NII. Further, costs are expected to trend downward, likely on the back of soft trading conditions.

Both assumptions look reasonable based on our analysis of the business. Stifel should do extremely well relative to its peers due to its exposure to interest income.

Peer comparison

Peer comparison (Tikr Terminal)

{kind=link}

Presented above is a comparison of Stifel to a cohort of other boutique investment banks.

Stifel performs quite well, generating a comparable OPM while outperforming on a NI basis. Further, it has grown at a faster rate, overall generating a greater return than average.

Valuation

Valuation (Tikr Terminal)

Despite the strong fundamental performance and outperformance of its peers, Stifel is trading at a discount to the average. We cannot see any clear reason for this, apart from that investors either do not see growth continuing or that future profitability is likely to be subpar.

Our view would be that there is a clear upside for investors and Wall St. analysts concur. Their consensus target price suggests a 9% upside from here.

Final thoughts

Stifel is a well-run business with a diversified revenue stream. Its margins are attractive and growth looks sustainable. When compared to a cohort of boutique investment banks, the company looks undervalued, trading at a forward discount to the likes of Piper Sandler despite better margins and similar growth.

The key risk for us is market conditions, which could act as a drag on growth. With a portion of costs being relatively fixed, namely salaries, margins could contract further if trading doesn't improve. We see net interest income as key to mitigating this.

We currently rate Stifel a buy, although a strong buy would be warranted should market conditions improve without price action.

For further details see:

Stifel: Well-Rounded IB With Upside