CA - Strathcona Resources Acquiring Pipestone Energy Creating A Possible Top-5 Canadian Oil Producer

2023-08-04 15:22:14 ET

Summary

- Pipestone Energy has reached an agreement to be acquired by Strathcona Resources, a serial acquirer and one of the largest private-equity owned E&P companies in North America.

- While Pipestone shareholders won't receive a premium, they are expected to reap the rewards of institutional investor interest and the unmatched growth potential offered by the large-cap Strathcona Resources.

- The transaction seems to undervalue the new Strathcona. Long-term investors might want to consider investing in Strathcona Resources by means of Pipestone Energy.

On August 1, 2023, Pipestone Energy Corp. ( OTCPK:BKBEF ) announced that it had reached an agreement to be acquired by the private company Strathcona Resources Ltd.

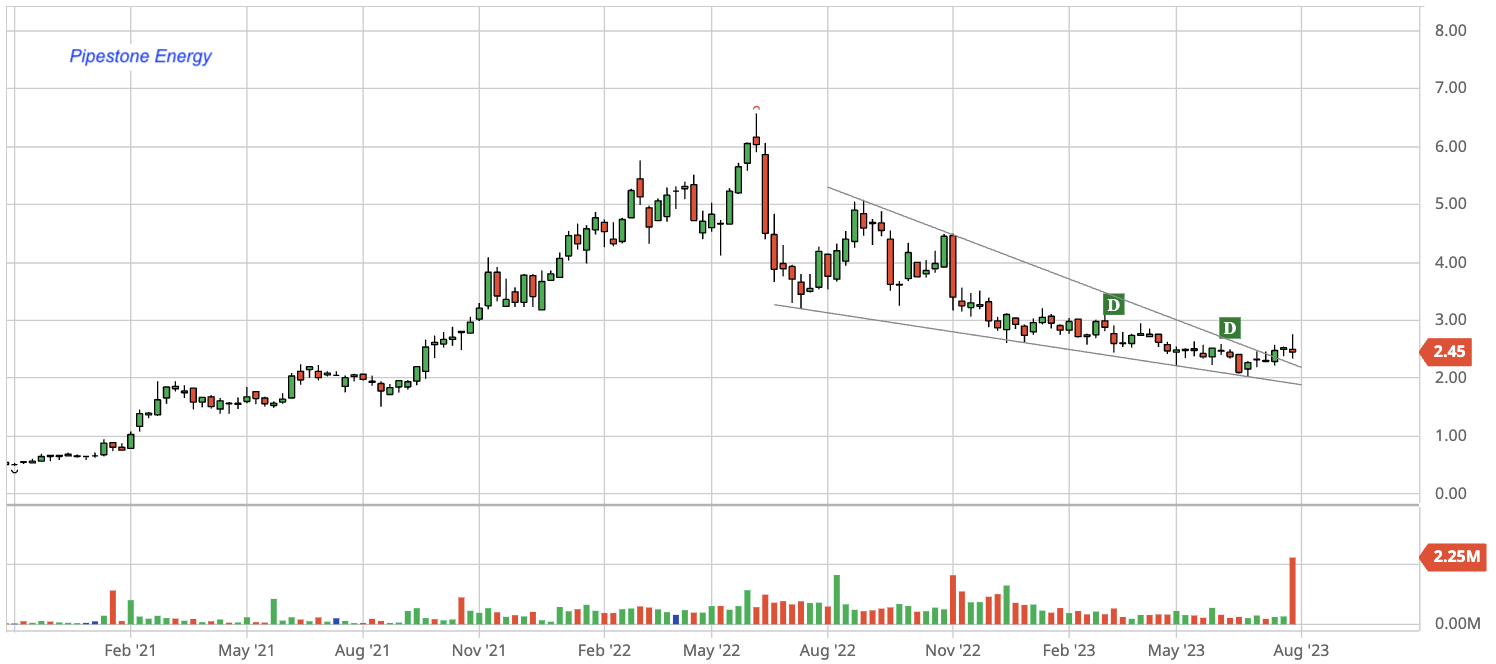

Pipestone is a growth-oriented, high-margin natural gas producer in the Montney play in Canada. The market has been anticipating a sale of Pipestone for some time. Strathcona Resources obviously timed the acquisition perfectly as Pipestone just recently broke out of a 12-month slump, as illustrated in Figure 1.

{kind=link}

Fig. 1. Stock chart of Pipestone Energy, dividend ( D ) back-adjusted (modified from Barchart and Seeking Alpha)

A number of questions arose from the transaction. What kind of company is Strathcona anyway? Is Strathcona worthy of an investment and how to make an entry? What should the existing Pipestone shareholders do now?

Strathcona Resources: A serial acquirer

Strathcona is a portfolio company of Waterous Energy Fund. From 2017 to 2019, Waterous carried out four transactions to form Cona Resources Ltd., including the acquisition of 67% of Northern Blizzard Resources on April 10, 2017 for C$244 million.

- On January 7, 2020, Cona Resources Ltd. acquired Pengrowth Energy Corporation for approximately C$740 million, with the Lindbergh thermal in-situ property near Cold Lake included in the deal. With the Pengrowth acquisition, Cona produced at 35,000 boe/d with a base decline rate below 10%. It was said that Pengrowth sold for pennies on the dollar as its access to capital dried up at the time.

- On August 14, 2020, Cona Resources Ltd. and Strath Resources Ltd. merged to form Strathcona Resources Ltd., for the benefit of Strath's condensate and natural gas production in the Kakwa region of the Montney play to complement its Pengrowth heavy oil operations. Both Cona and Strath are a portfolio company of Waterous Energy Fund. Strathcona produced at 60,000 boe/d, with a 67% oil and liquids cut, a 40-year reserve life index, and a base oil decline rate of approximately 10%.

- On June 11, 2021, Strathcona Resources Ltd. acquired Osum Oil Sands Corp. , along with Orion oilsands project, for approximately C$370 million.

- On November 30, 2021, Strathcona acquired Caltex Resources Ltd. Caltex produces 13,000 bo/d of heavy oil in Alberta and Saskatchewan through enhanced oil recovery (aka, EOR). There is the benefit of synergy to be gained by combining two immediately adjacent polymer flood projects in the Lloydminster heavy oil EOR play, i.e., Greater Bodo of Caltex and Cactus Lake of Strathcona.

- On January 31, 2022, Strathcona acquired the Tucker asset , a thermal oil field producing ~19,000 bo/d in the Cold Lake region of Alberta, near Strathcona’s existing Cold Lake thermal oil operations at the Orion and Lindbergh fields. Following the Tucker transaction, Strathcona had production capability of approximately 110,000 boe/d in Alberta and Saskatchewan.

- On August 29, 2022, Strathcona completed the acquisition of heavy oil producer Serafina Energy Ltd. for C$2.3 billion. Serafina produces 40,000 boe/d in Saskatchewan.

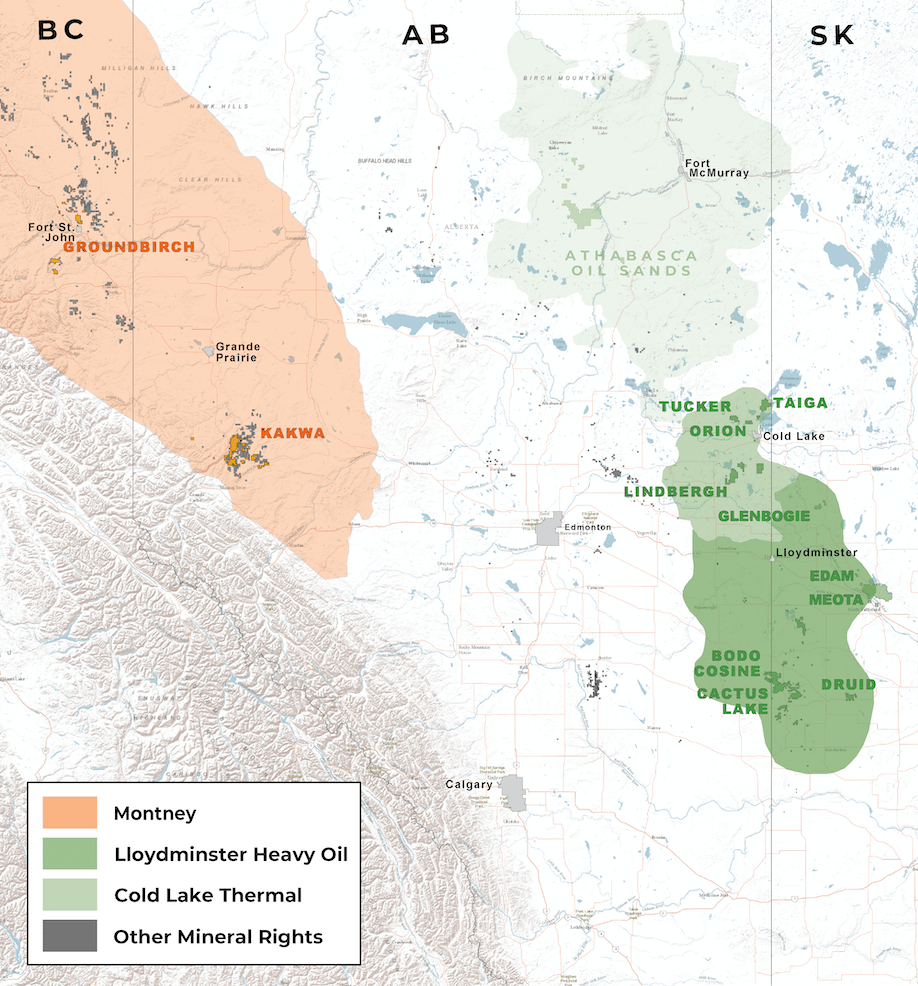

As a result of those acquisitions, Strathcona Resources has emerged as one of the largest private-equity owned E&P companies in North America. Strathcona operates a diversified portfolio of assets in Canada in three core areas, including the Cold Lake oil sands play, the Lloydminster heavy oil play, and the Montney natural gas play, as shown in Figure 2.

{kind=link}

Fig. 2. A map showing the assets owned by Strathcona Resources (Strathcona Resources)

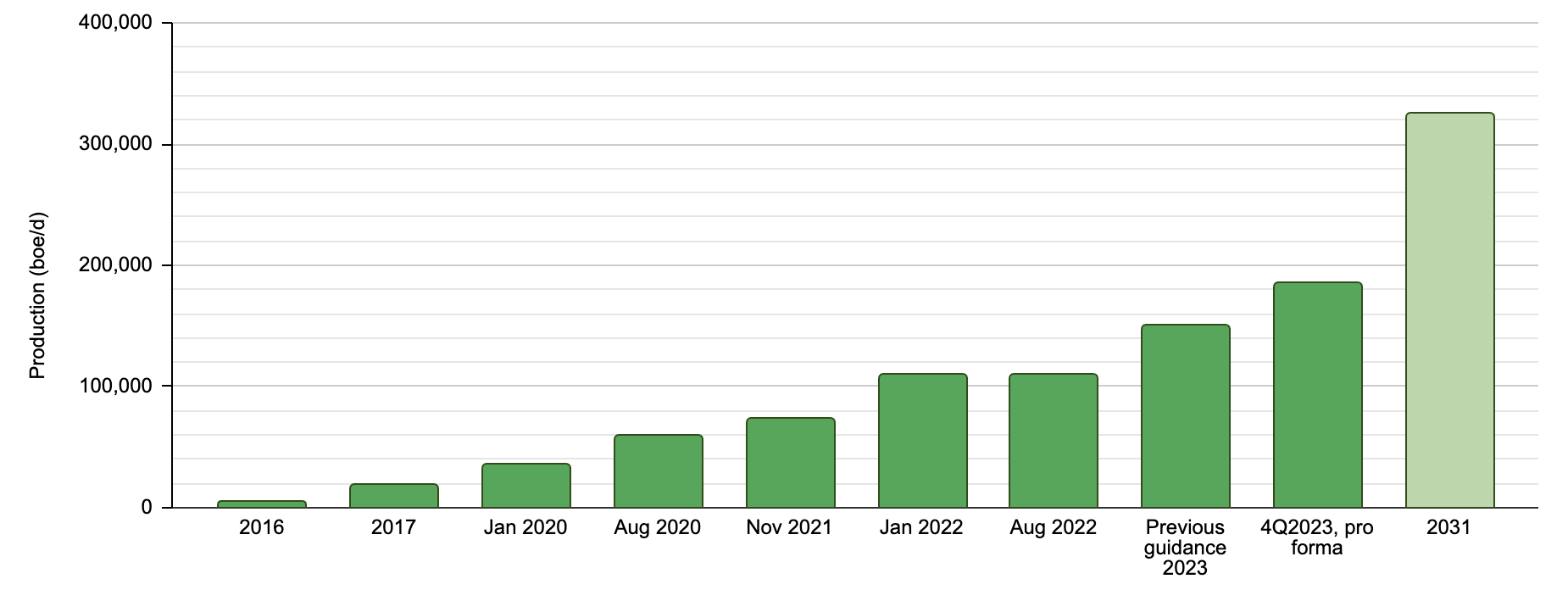

Prior to the announcement of the Pipestone transaction, Strathcona guided toward producing 148,000–154,000 boe/d in 2023 (Figure 3), with the output consisting of 85% of liquids and 15% natural gas. From 2016 to the end of 2023, without considering Pipestone, Strathcona will have grown production at an impressive CAGR of 62.7% through acquisitions and organically.

{kind=link}

Fig. 3. Estimated production profile of Strathcona Resources, historical and anticipated (Laurentian Research for The Natural Resources Hub based on various company news releases)

The acquisition of Pipestone

Transaction structure

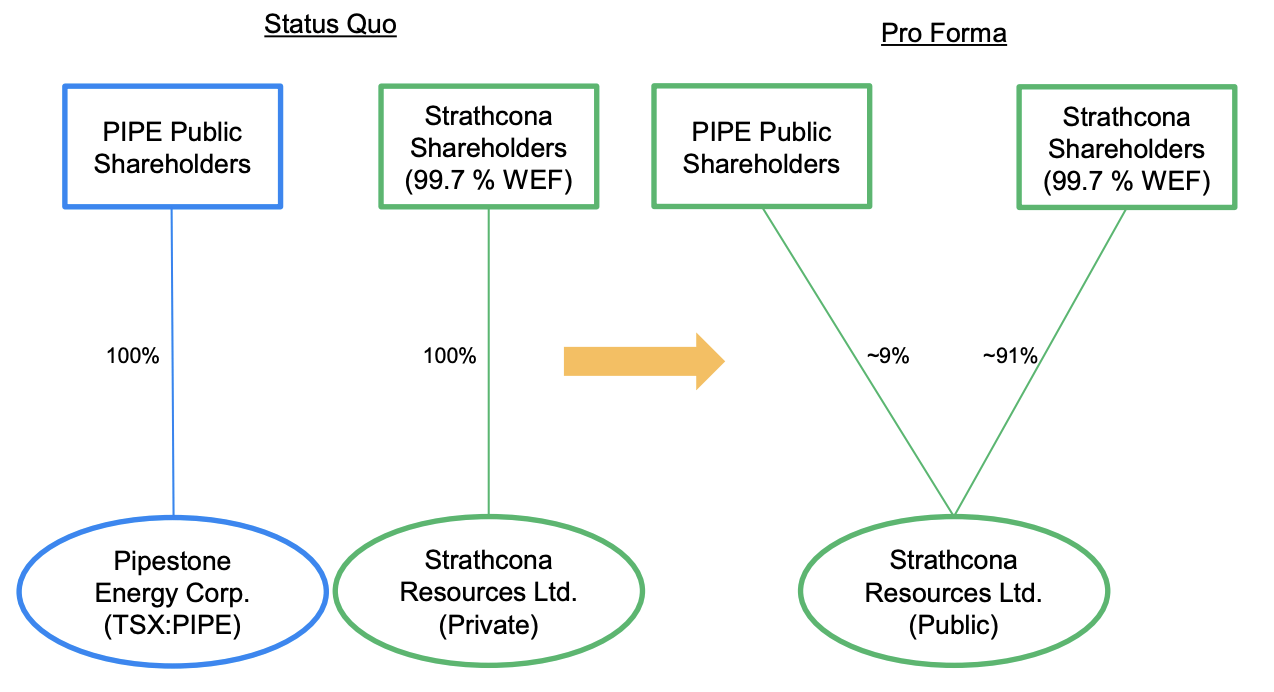

Following the all-share acquisition, the newly formed corporation will continue as "Strathcona Resources Ltd." Once the transaction is completed, the existing Pipestone shareholders will receive approximately 9.05% of the pro forma equity in the new Strathcona Resources on a fully-diluted basis or around 8.87% on a basic basis. In other words, every Pipestone share will exchange into 0.067967 new Strathcona shares, as detailed in Figure 4 and Figure 5.

{kind=link}

Fig. 4. The all-share acquisition of Pipestone Energy by Strathcona Resources (Pipestone)

Fig. 5. Pro forma share structure of the new Strathcona Resources (Pipestone)

The above exchange ratio implies an initial market capitalization of C$8.6 billion or an initial enterprise value of C$11.5 billion once the C$2.9 billion in pro forma debt outstanding on closing of the transaction is considered.

It is worth noting that the agreed transaction terms do not include any premium over the close price on July 31, 2023, the day before the announcement of the deal, for Pipestone shareholders. However, it is possible that some may have gotten wind of an upcoming transaction and caused the share price to surge on July 31, 2023. If that is the case, using last Friday's close as a reference point, the agreed terms may actually include an 11.9% premium, which evaporated entirely on August 1, 2023, as illustrated in Figure 6.

{kind=link}

Fig. 6. Share prices of Pipestone Energy before and after the announcement of its sale to Strathcona Resources (modified from CEO.com and Seeking Alpha)

Strategic rationale for the transaction

With this transaction, Strathcona Resources further strengthens its exposure to the Montney natural gas play and increases condensate-rich Montney production, which provides a natural hedge to its operations in the Cold Lake oil sands and Lloydminster heavy oil plays. After 6.5 years of building up the business as a private entity, Strathcona will finally become a publicly-traded company, as the oil bull market continues to swing higher.

Pipestone Energy, on the other hand, has struggled to attract institutional investors due to its humble size, even though it had grown production from 152 boe/d to 35,162 boe/d in four years. By joining forces with Strathcona to create the fifth largest liquids producer in Canada, Pipestone shareholders will likely benefit from an inflow of institutional money and, consequently, share price appreciation.

Some Pipestone investors might have hoped for a larger premium that would allow for a quick gain upon exiting. However, Strathcona probably thought that it would get sufficient shareholder support anyway. Importantly, from Strathcona's perspective, offering a seat on the bus to years of production growth managed by a highly-regarded management team that consists of Executive Chairman Adam Waterous, CEO and President Rob Morgan, and CFO Connor Waterous, as well as the potential for substantial capital appreciation, outweighs catering to a few short-term swing traders.

Pro forma asset portfolio

Once the transaction is completed by 4Q2023, Strathcona will have a diversified portfolio of assets that includes Cold Lake thermal oil (55,000 bbl/d), Lloydminster heavy oil (55,000 bbl/d), and Montney natural gas (75,000 boe/d). These assets combined will be capable of producing 185,000 boe/d, with 70% being oil, 8% condensate, and 22% natural gas. At 185,000 boe/d, Strathcona will be trailing liquids-weighted producers Canadian Natural Resources ( CNQ ), Cenovus Energy ( CVE ) , Suncor Energy ( SU ) , and Imperial Oil ( IMO ), but will be ahead of MEG Energy ( MEGEF ) in terms of total production.

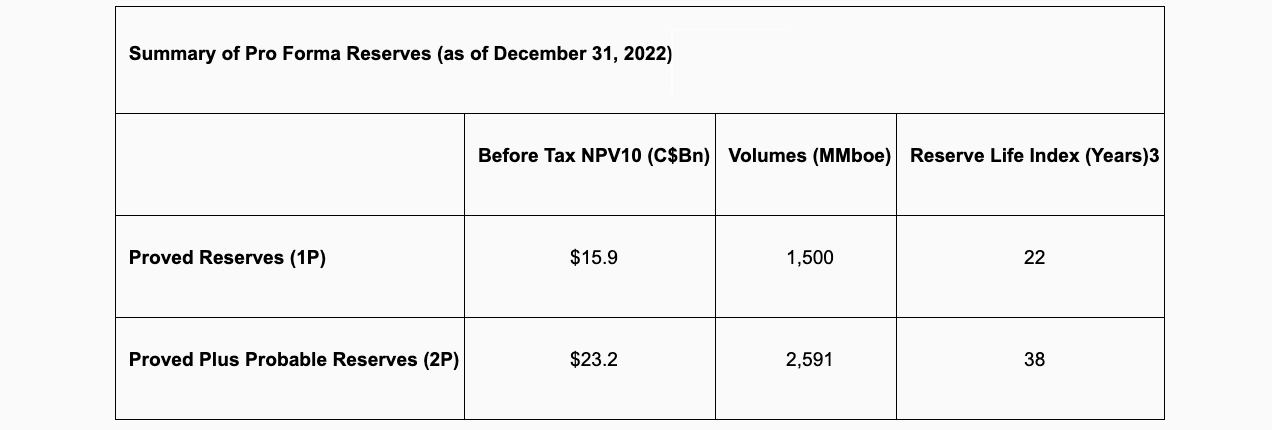

The new Strathcona Resources will have 1,500 MMboe of proved reserves and 2,591 MMboe of proved and probable reserves, supporting a 1P reserve life of 22.2 years and a 2P reserve life of 38.4 years, as shown in Figure 7.

{kind=link}

Fig. 7. Pro forma reserves of Strathcona Resources (Pipestone)

Future production growth

Backed by its ample reserves, Strathcona Resources envisions a future of aggressive organic growth. Over the next eight years, the company aims to increase production to 220,000 boe/d using its existing facility's capacity. With debottlenecking projects and brownfield expansions, that figure is set to rise to 285,000 boe/d. Furthermore, by developing greenfield areas, Strathcona may grow production to 325,000 boe/d, reflecting a robust CAGR of 7.3%, as depicted in Figure 3.

It's worth noting that additional acquisitions have the potential to accelerate this already promising growth trajectory.

How about profitability going forward?

Several factors are poised to drive Strathcona's profit margin:

- Firstly, with a long reserve life and a corporate decline rate of <25% (15% for oil), Strathcona does not need to allocate significant capital to finding and developing (F&D) reserves.

- Secondly, Strathcona enjoys premium realized pricing in Cold Lake over Athabasca oil sands due to higher crude oil quality, lower blending costs, and reduced transportation expenses. Strathcona's ownership and operation of the Hamlin rail terminal allow it to deliver up to 50,000 b/d of undiluted Lloydminster heavy oil to the U.S. Gulf coast.

- Thirdly, the liquids-rich Montney production complements its heavy oil production, which may need to be diluted for transportation.

- Lastly, Strathcona will have C$6.4 billion in pro forma tax pools, resulting in the company not expecting to pay cash taxes before 2026.

Strathcona is confident that its full-cycle breakeven will be less than US$40/bo WTI.

Upside and risks

According to my estimate, Strathcona Resources is valued at an EV/EBITDA of 3.0X immediately after completing the transaction, and it is valued at 2.8X of 2024 EBITDA. Given that it is an oil producer with a projected 7.3% annual production growth during an unfolding up-cycle, Strathcona appears undervalued compared to above industry peers, which capture an average EV/EBITDA of 5.6X. Furthermore, Strathcona's undervaluation is evident from its valuation metrics of US$5.75/boe for proved reserves and US$3.33/boe for proved and probable reserves.

In my view, purchasing Pipestone while impatient retail speculators head for the exit (Figure 6) presents an excellent opportunity for long-term investors to establish a position in Strathcona Resources.

There are a slew of risks associated with the newly-formed Strathcona Resources. The market will need time to learn about the management and the Strathcona story. Moreover, Waterous Energy Fund and its employees will own 90.95% of the new Strathcona Resources. Their more than 195 million shares could potentially overhang capital appreciation if unloaded without constraint. However, Strathcona management has indicated that they do not plan to sell a significant number of shares anytime soon. It is possible that the Waterous family may offload part of their shares in large blocks to various institutions, for example, for index purposes.

Investor takeaways

The acquisition of Pipestone Energy by Strathcona will create a publicly-traded large-cap oil producer in Canada. The new Strathcona Resources offers a compelling story of aggressive growth and high-margin profitability. Based on available information, the transaction appears to undervalue the new Strathcona Resources, leaving a significant upside for early investors, including those who choose to retain their positions in Pipestone.

For further details see:

Strathcona Resources Acquiring Pipestone Energy, Creating A Possible Top-5 Canadian Oil Producer