SPH - Suburban Propane Partners: Turning Waste Into Future Distribution Growth

Summary

- Suburban Propane Partners surprised and disappointed unitholders back in late 2022 when they failed to provide any distribution growth.

- Thankfully, their cash flow performance remains favorable and recently enjoyed a strong start to their fiscal year 2023.

- More so, it is now clearer why they skipped on distribution growth as they have recently announced a sizable $190m acquisition.

- This sees them move into renewable natural gas, which I view as a good fit for their partnership, although the profitability remains to be proven.

- At least their financial position can absorb the cost, and thus, I believe that maintaining my buy rating is appropriate.

Introduction

Despite the once-strong distribution growth outlook for Suburban Propane Partners (SPH), back in late 2022, it was both surprising and disappointing to see no distribution growth, as my previous article expressed. Following their recently announced sizable Equilibrium acquisition, thankfully the reasoning is clearer with management electing to double down on building out their clean energy business segment via renewable natural gas, which sees the potential of turning waste into future distribution growth.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

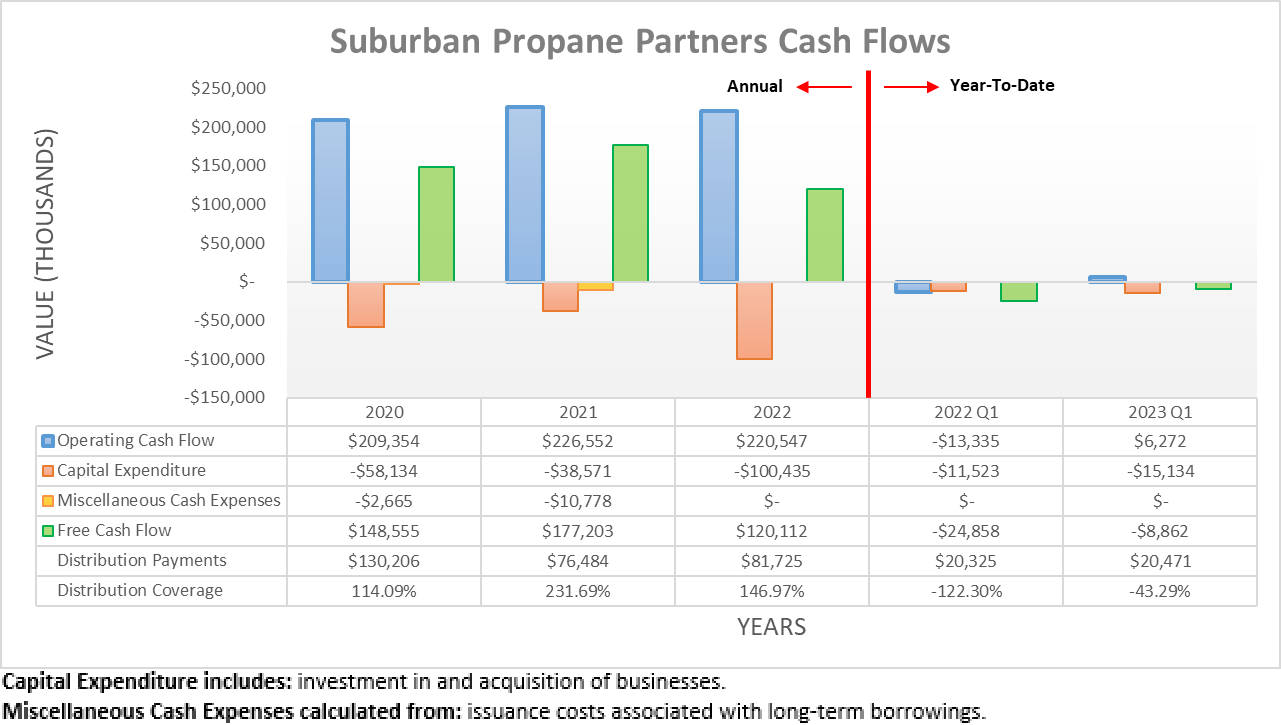

When it comes to their operating cash flow, it once again continued its steady performance, if looking annually and thus disregarding its typical seasonality. Since their fiscal year 2022 ended after conducting my previous analysis, it can now be seen their operating cash flow landed at $220.5m and thus is very similar to their previous results of $226.6m and $209.4m during their fiscal years 2021 and 2020, respectively. Even though they ramped up their capital expenditure building out their clean energy business segment during their fiscal year 2022, they still generated $120.1m of free cash flow that provided strong coverage of 146.97% to their accompanying distribution payments of $81.7m.

{kind=link}

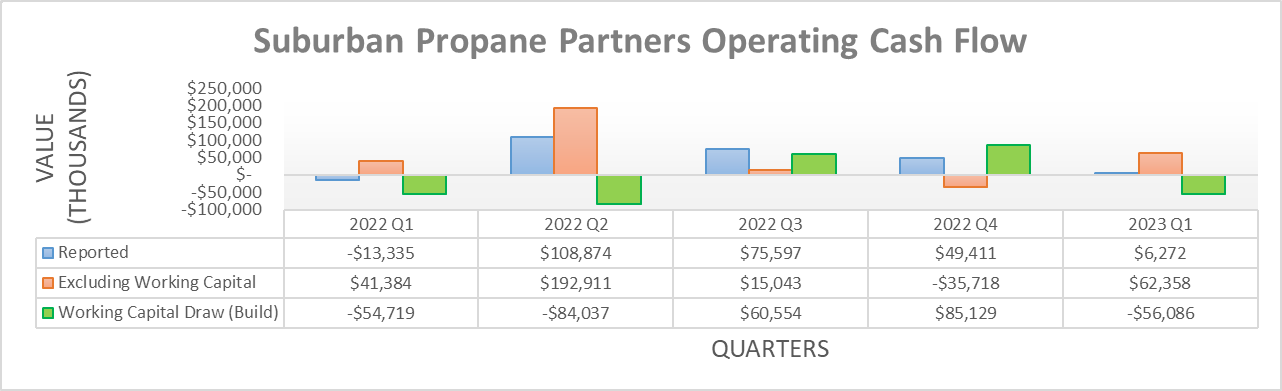

If viewing their cash flow performance on a quarterly basis, we can take a look into their most recent results for the first quarter of their fiscal year 2023. As for their reported results, their operating cash flow was barely visible at only $6.3m, although this is normal as one year prior, they saw a result of negative $13.3m. Upon removing their routine large working capital movements, their underlying results were much higher year-on-year with $62.4m versus $41.4m across these same two points in time, thereby seeing a strong start to their latest fiscal year.

Whilst their cash flow performance is important to monitor, the big news is actually the building out their clean energy business segment that recently took its most notable move so far, being their Equilibrium acquisition . This sees the partnership spending $190m to acquire renewable natural gas assets, which are expected to be accretive to their financial performance starting from their fiscal year 2024. Renewable natural gas is produced from waste and importantly, it is interchangeable with traditional natural gas, as per the quote included below.

"Renewable natural gas ((RNG)) is a pipeline-quality gas that is fully interchangeable with conventional natural gas and thus can be used in natural gas vehicles. RNG is essentially biogas (the gaseous product of the decomposition of organic matter) that has been processed to purity standards. Like conventional natural gas, RNG can be used as a transportation fuel in the form of compressed natural gas ((CNG)) or liquefied natural gas ((LNG))."

- Alternative Fuels Data Center .

In my eyes, this is a more suitable and lower-risk investment than their earlier hydrogen investments that were discussed within my previously linked article, mostly because natural gas already sees wide and extremely well-established demand. Since renewable natural gas is interchangeable but carries better environmental credentials, it lowers the risks versus hydrogen that is still more of an emerging fuel source and thus by extension, sees a less certain future.

If this pans out as hoped, it stands to build upon their existing free cash flow, thereby effectively turning waste into future distribution growth once they complete this growth era. That said, until the results hit their financial statements in the coming years, unitholders will have to sit back and wait because the extent of its profitability remains to be proven.

{kind=link}

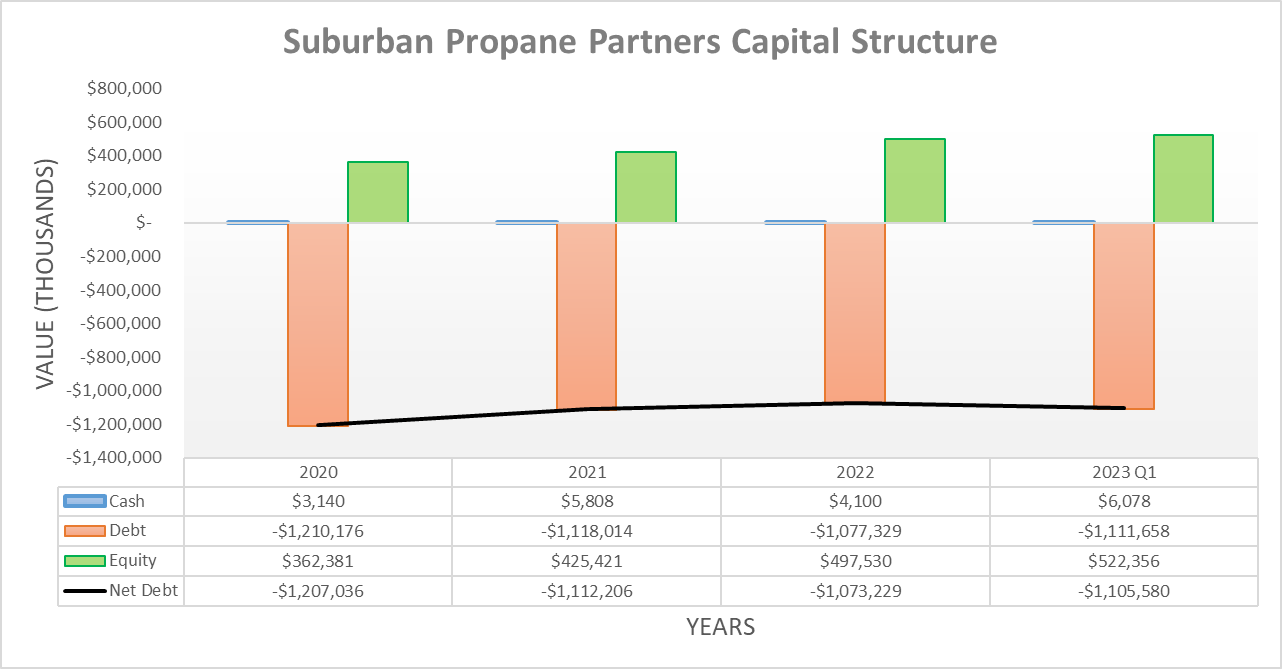

Since conducting the previous analysis, their subsequent two fiscal quarters saw their net debt broadly track sideways to $1.106b following the first quarter of their fiscal year 2023 versus its previous level of $1.072b following the third quarter of their fiscal year 2022. This is keeping in practice with the last couple of fiscal years but when looking ahead, the next report should see their net debt spike circa 17% as a result of their $190m Equilibrium acquisition.

{kind=link}

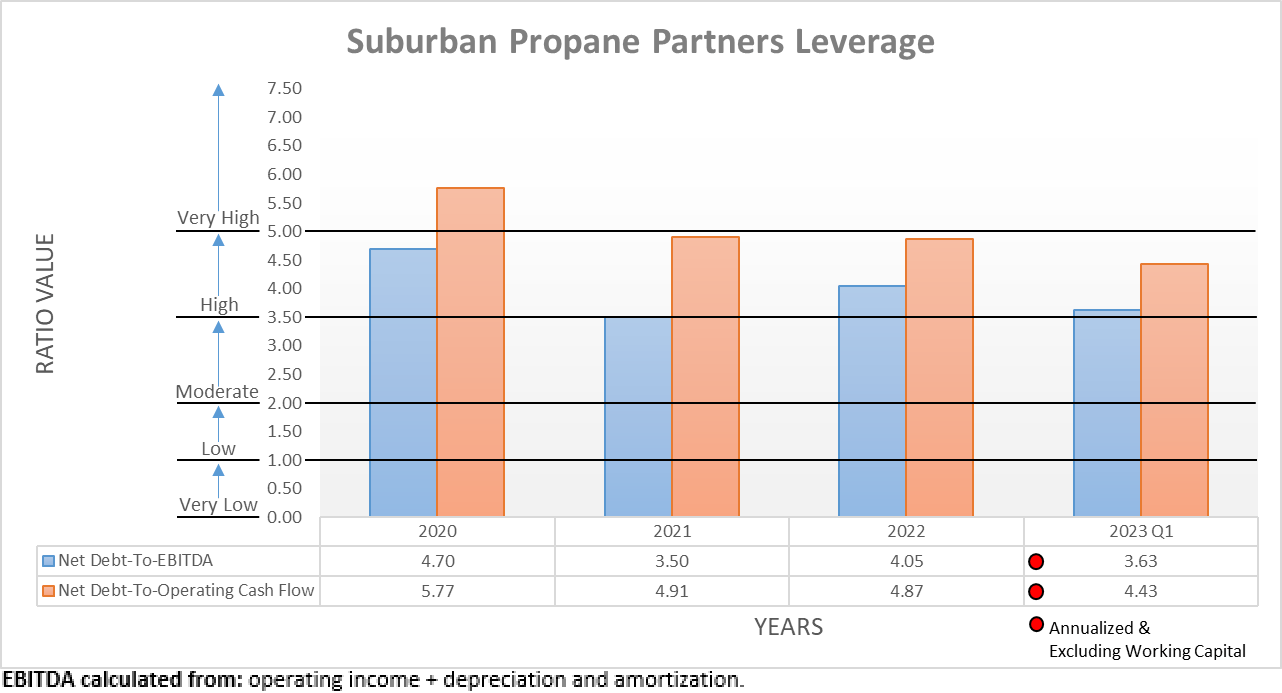

Due to the typical seasonality in their financial performance, there is no point in comparing their latest leverage ratios to those seen when conducting the previous analysis. More so, their full-year results paint an accurate picture and most recently, their fiscal year 2022 ended with a net debt-to-EBITDA of 4.05 and a net debt-to-operating cash flow of 4.87. Whilst these are in the high territory of between 3.51 and 5.00, they are certainly not crippling nor a reason for alarm given their reasonably stable and cash-generating propane business segment.

When looking ahead, in the short-term their Equilibrium acquisition is likely to push these towards the very high territory as their net debt spikes higher, mainly their net debt-to-operating cash flow. If this scales higher around 17% in tandem, its latest full-year result of 4.87 would increase to 5.70 and thus cross the threshold of 5.01 the very high territory. Despite not being ideal, in the medium to long-term the additional earnings expected to flow from their fiscal year 2024 onwards should help revert this lower. That said, whether these are sufficient remains to be seen and thus, it is now becoming clearer why management previously elected to halt their distribution growth whilst they integrate this sizeable acquisition.

{kind=link}

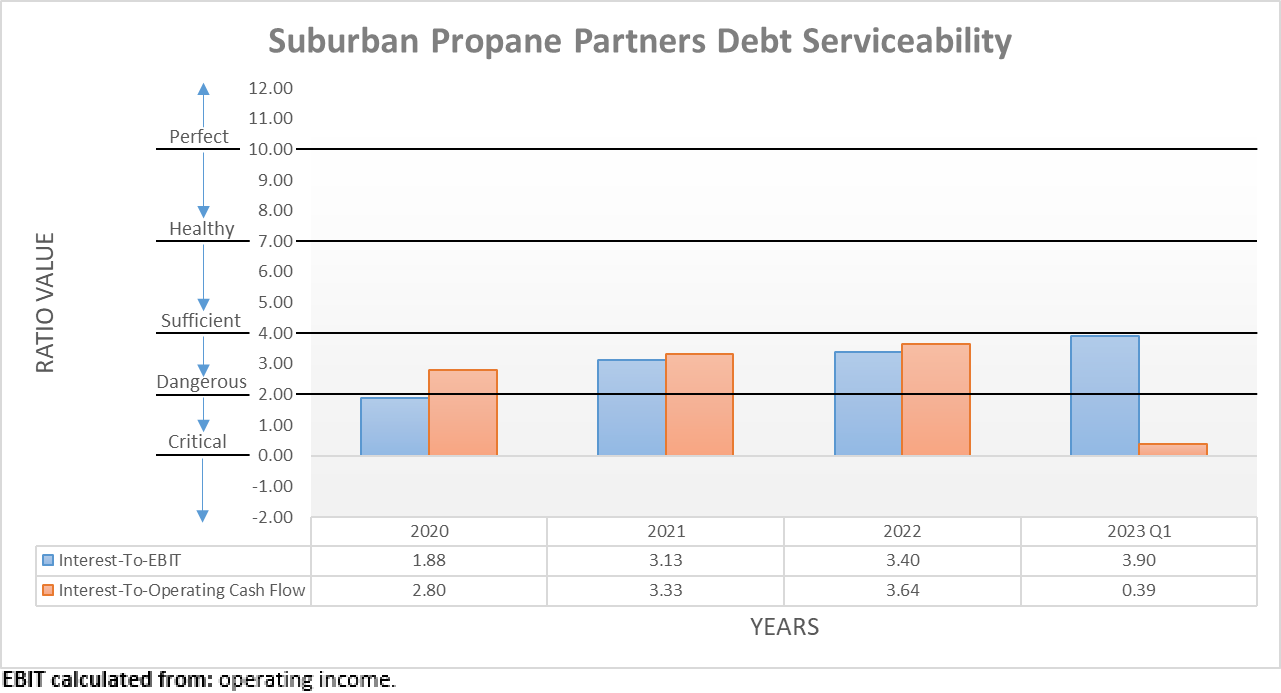

Similar to their leverage, their debt serviceability is also affected by the seasonality in their financial performance, thereby rendering anything but full-year results useless. Thankfully, they have routinely sported sufficient interest coverage across both fiscal years 2021 and 2022 with the latter seeing results of 3.40 and 3.64 when compared against their EBIT and operating cash flow, respectively. Even though higher net debt will weigh on their interest coverage in the short-term, this means it should be manageable until the earnings begin flowing from their new renewable natural gas assets in 2024.

{kind=link}

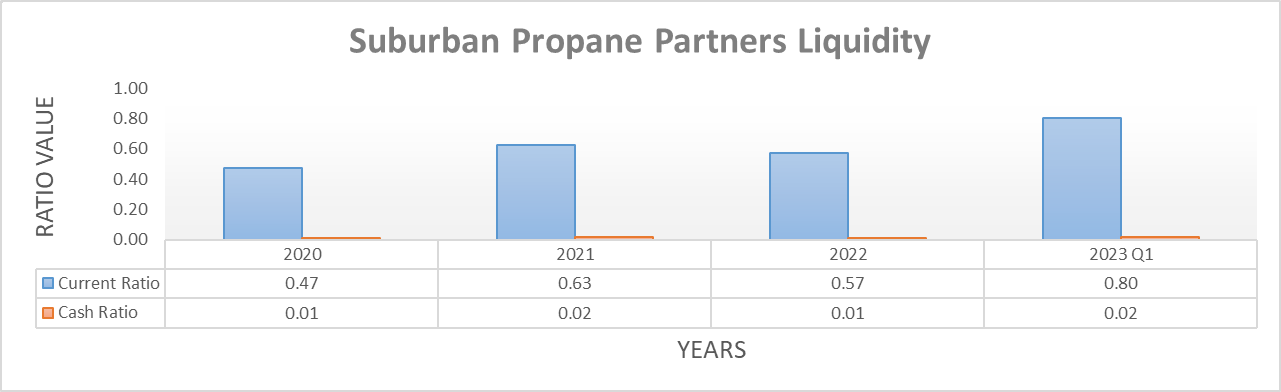

Quite unsurprisingly, their liquidity was uneventful during their two fiscal quarters following my previous analysis. Their current ratio is now 0.80 following the first quarter of their fiscal year 2023 versus its previous result of 0.89 following the third quarter of their fiscal year 2022, thereby representing a routine minor change. Meanwhile, their accompanying cash ratio sees results of 0.02 and 0.03 across these same points in time, which is obviously an immaterial change.

When looking ahead, the funding of their Equilibrium acquisition will lean upon their credit facility in the short-term, as I see no news of debt issuances apart from the $80m assumption of debt as part of the $190m transaction. Thankfully, their credit facility should still retain availability of $376.5m and does not mature until March 2025, thereby providing both scope and time to absorb the remaining cost and thus, ensuring they still retain adequate liquidity. Elsewhere, the remainder of their debt is not on the radar for maturity until March 2027 at the earliest, thereby easing pressure in the next few years.

Suburban Propane Partners Q1 2023 10-Q

Conclusion

Once again, their financial performance continues ticking along well with a strong start to their fiscal year 2023 and thus leaving their recently announced Equilibrium acquisition as the big news. Despite being a sizeable acquisition relative to the size of their partnership, they can absorb the cost whilst they await the additional earnings to flow in their fiscal year 2024. After seeing this acquisition, I can also now see why management skipped on distribution growth back last year when conducting my previous analysis and when all is said and done, I still believe that my buy rating is appropriate given my favorable view of their renewable natural gas assets.

Notes: Unless specified otherwise, all figures in this article were taken from Suburban Propane Partners' SEC filings , all calculated figures were performed by the author.

For further details see:

Suburban Propane Partners: Turning Waste Into Future Distribution Growth