SPH - Suburban Propane Partners: What! No Distribution Growth?

Summary

- Suburban Propane Partners started growing their distributions again during 2021 after having cut them amidst the turmoil of 2020.

- Thus far into their fiscal year 2022, their steady cash flow performance continued to generate ample free cash flow, even with their higher capital expenditure.

- Despite this otherwise positive backdrop, management did not increase their distributions with little explanation.

- Nor did they detail the continued costs to build out their clean energy business segment, which is now seemingly their focus.

- Since this lowers the appeal of their units, I now only believe that a buy rating is appropriate versus my previous strong buy rating.

Introduction

After cutting their distributions amidst the turmoil of 2020, Suburban Propane Partners ( SPH ) was seemingly entering a new age of distribution growth one year later with 2021 seeing a solid increase and plenty of scope for more to come, as my previous article highlighted. Since they are a steady partnership, their high distribution yield of 8.06% was effectively on autopilot during the subsequent twelve months and thus after this wait, it now seems timely to provide a refreshed analysis that disappointingly, leaves me thinking, what! No distribution growth?

Executive Summary & Ratings

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Author

*Instead of simply assessing distribution coverage through distributable cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact upon their financial position.

Detailed Analysis

{kind=link}

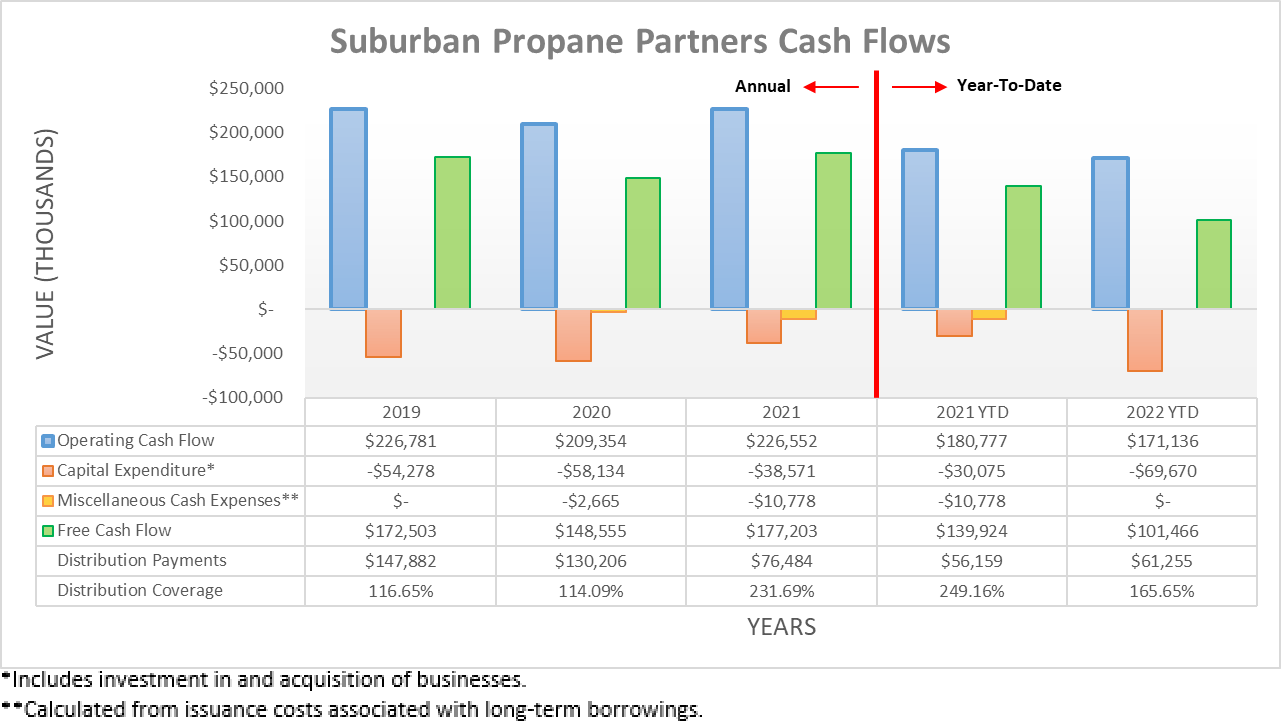

Following their resilient cash flow performance during the last two turbulent years, the first nine months of their fiscal year 2022 saw their operating cash flow land at $171.1m and thus down a slight 5.33% year-on-year versus the first nine of their fiscal year 2021 that saw a result of $180.8m. If removing the routine working capital builds arising as part of the typical seasonality in their financial performance, these two results would be $249.3m and $248.8m respectively, thereby unchanged year-on-year as their steady cash flow performance continues, unsurprisingly. Notwithstanding their working capital builds during the first nine months of their fiscal years, their underlying financial performance sees little to nothing attributable during the fourth quarter, as the bulk of the operating cash flow arises from these working capital builds reversing.

Even after the first nine months of their fiscal year 2022 seeing their capital expenditure ramp up to $69.7m as they build out their clean energy business segment, they still generated $101.5m of free cash flow to provide strong distribution coverage of 165.65% to their payments of $61.3m. Normally this would be a dream for income investors given their prospects to balance growth investments whilst leaving room for distribution growth but alas, they have now declared the same quarterly distribution of $0.325 per unit for five consecutive quarters, thereby missing the mark for a once a year increase, as is normally the case for most companies and partnerships. When asked about the outlook for distribution growth earlier in the year, they were vague as they instead focused on building out their new clean energy business segment, as per the commentary from management included below.

“I think what we've said all along is we obviously take a very hard look every quarter as to how to allocate capital. I think what we're excited about right now is the opportunities that we see in front of us with respect to deploying capital towards the build-out of our renewable platform. We have a number of exciting things that we're continuing to look at in continuing to support that effort and as well as propane opportunities…”

- Suburban Propane Partners Q2 2022 Conference Call.

Sadly, their subsequent conference call for the third quarter of their fiscal year 2022 did not shed any light on their lack of distribution growth. Furthermore, it would have been helpful if they at least provide guidance regarding how much these clean energy investments are going to cost but unfortunately, we are left guessing.

Whilst I am certainly not against the fundamental idea of growing their partnership into new areas that see stronger long-term demand, such as their hydrogen investment , it does not change the fact that their unitholders are somewhat left in the dark. Furthermore, unlike other fossil fuels along the lines of thermal coal, propane does not face nearly as big of a threat from the clean energy transition due to its end uses, as discussed within one of my earlier articles . Not to mention, following the now problematic global energy shortage, the threats to future propane demand seem even less severe than in prior years and thus makes their hesitation to grow their distributions even more perplexing.

Furthermore, even without knowing the extent of their future clean energy investments, their distributions are still relatively low versus their operating cash flow at circa one-third on a full-year basis. Whilst free cash flow is a better lens across time, the comparison to operating cash flow can be useful to assess distributions during years of particularly large capital expenditure, as it helps gauge the stress their distribution payments place upon their partnership, which is obviously quite low in this situation.

{kind=link}

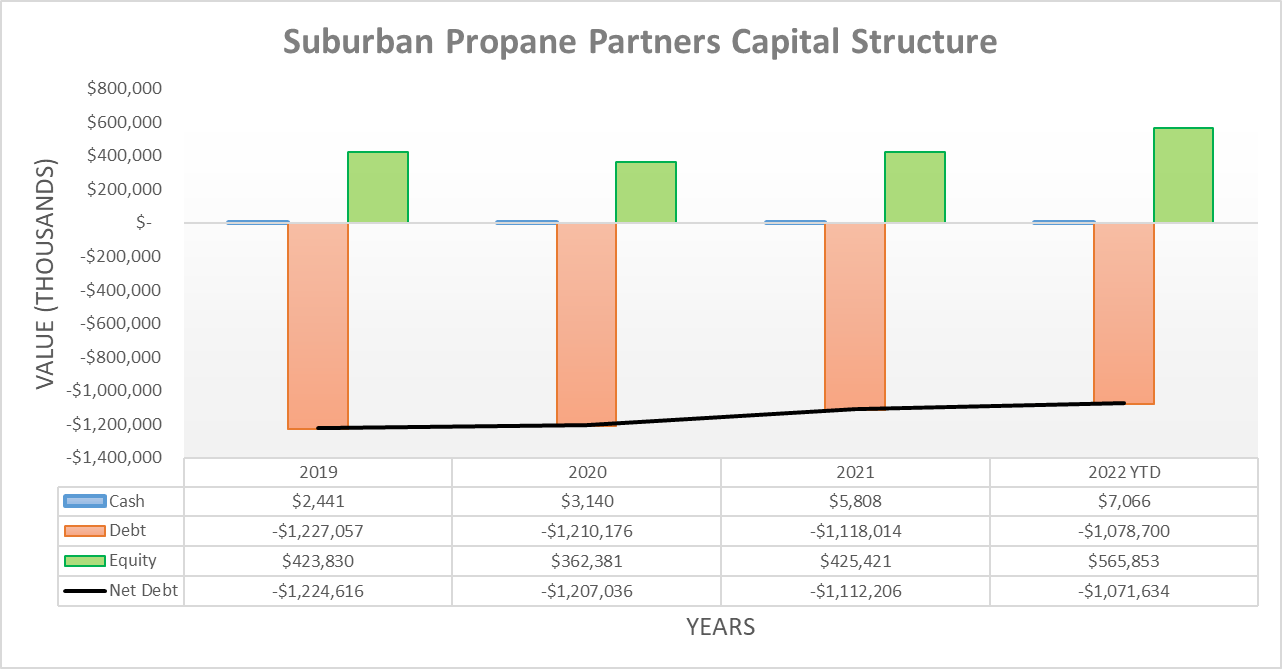

Thanks to the retained free cash flow provided by their continued steady cash flow performance, their net debt continues to trend lower, albeit at a rather slow pace. This now sees their net debt down to $1.072b, which is the lowest point in many years but conversely, only a modest 12.49% below its peak of $1.225b back at the end of 2019. Due to their lack of guidance for capital expenditure, going forwards it is difficult to assess where their net debt is heading but given their recent strong distribution coverage, it seems most likely to continue trending lower or if not, at least not increase significantly.

{kind=link}

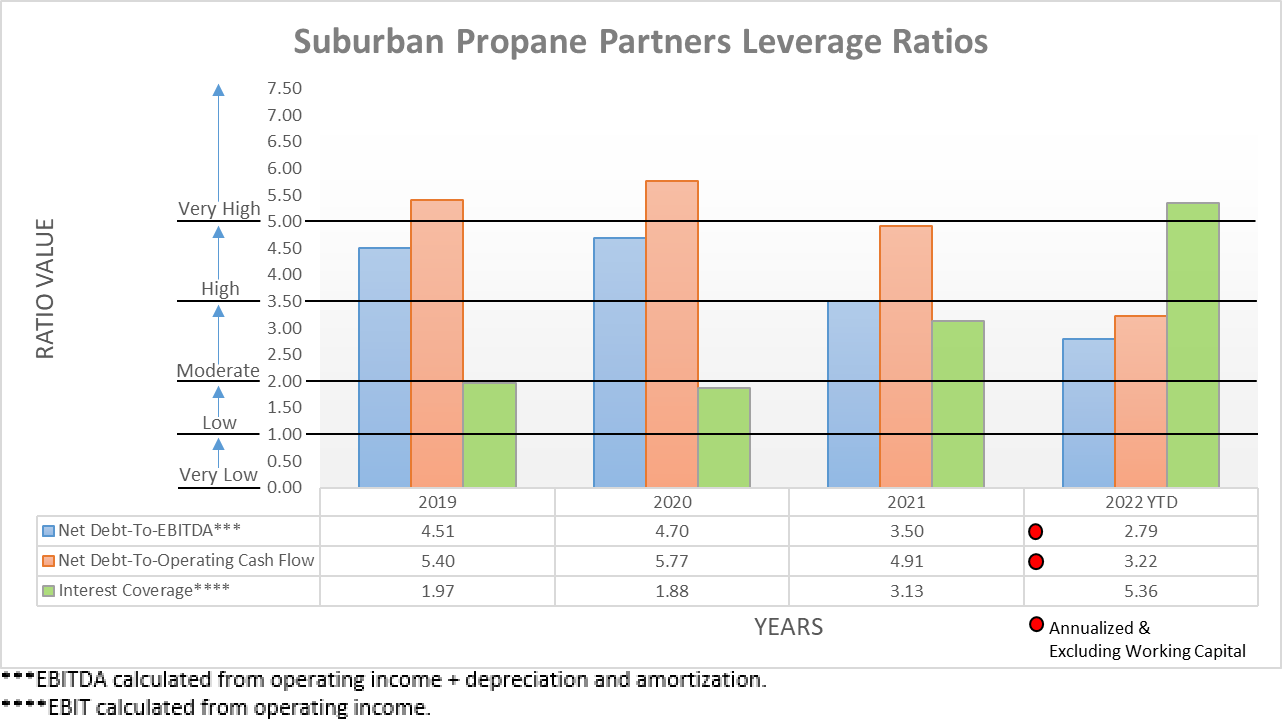

Due to the typical seasonality in their financial performance, it favorably skews their leverage ratios for the first nine months of their fiscal years, thereby rendering them pointless. Since their net debt is not materially different versus the end of their fiscal year 2021, we can utilize those results to assess their leverage with their net debt-to-EBITDA and net debt-to-operating cash flow posting results of 3.50 and 4.91 respectively. Whilst the former is sitting right on the crux between the moderate and high territories, the latter is towards the upper end of the high territory of 5.00. Despite sounding scary, this measurement is only generalized and thus still needs to be weighed against the nature of their partnership. Thankfully, they enjoy resilient financial performance that is seemingly not too affected by economic conditions, thereby meaning they can safely shoulder high leverage and thus they do not necessarily need to deleverage.

{kind=link}

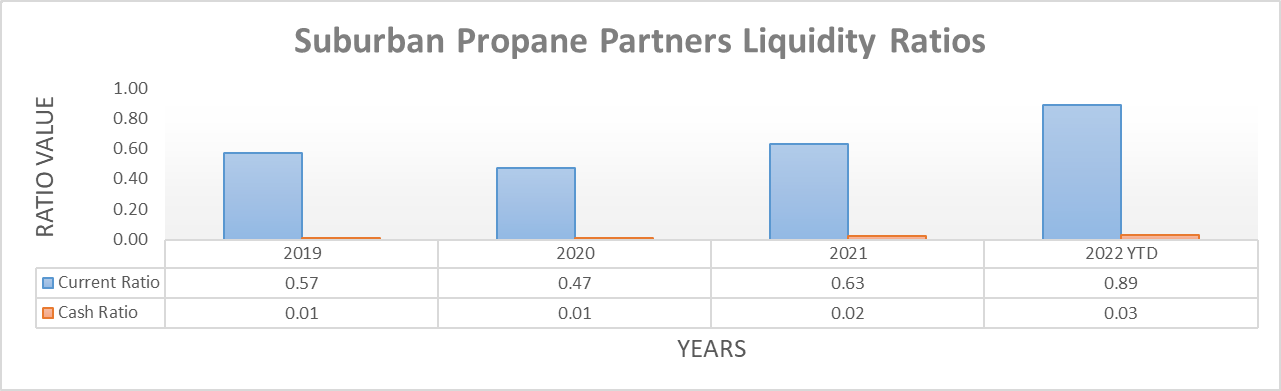

Following their continued steady cash flow performance, it was not surprising to see their liquidity remained adequate with their current ratio sitting at 0.89. Even though their low cash balance and resulting cash ratio of only 0.03 leaves room for improvement, it does not pose any material issues thanks to the $359.7m available under their credit facility, which should not change going forwards given their accompanying debt maturity profile that sees nothing until March 2025, as table included below displays.

Suburban Propane Partners Q3 2022 10-Q

Conclusion

It was disappointing to seemingly see their distribution growth now on pause, despite their solid fundamentals that most notably, include ample free cash flow. Whilst their focus on building out their clean energy business segment sees long-term potential, they have not released firm details regarding the costs and therefore, it leaves their unitholders somewhat in the dark. Whilst they still provide a desirable source of income given their high circa 8% yield, what was previously making their units very desirable and thus worthy of a strong buy rating was their accompanying growth prospects and thus as a result, I now believe that downgrading to a buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Suburban Propane Partners’ SEC filings , all calculated figures were performed by the author.

For further details see:

Suburban Propane Partners: What! No Distribution Growth?