JEF - Sumitomo Mitsui Financial Group: Potential Diversification Play Is Not Attractive Enough

2023-06-30 01:04:37 ET

Summary

- Sumitomo Mitsui Financial Group, a Japanese bank with over $2 trillion in assets, offers potential diversification due to its high exposure to Japan, but its lower than average dividend yield and fair valuation make it less attractive for investment.

- The bank has a conservative lending approach and a low-risk balance sheet, with a sizable equity portfolio of Japanese equities that it plans to reduce to decrease earnings volatility.

- Despite its stable profile and conservative risk culture, Sumitomo's financial performance has been relatively stable over the past few years due to low growth prospects. Its return on equity ratio is only 6.5%, a relatively low level of profitability.

- However, SMFG has a good dividend history and its dividend is expected to grow gradually in the coming years.

Sumitomo Mitsui Financial Group ( SMFG ) is a potential diversification play compared to U.S. or European banks, due to its high exposure to Japan, but its lower than average dividend yield and fair valuation aren't attractive enough to start a position.

Company Overview

Sumitomo is a Japanese bank and one of the largest banks around the world, given that at the end of last March it had more than $2 trillion in assets. Due to its large size, it's one of the Global Systemically Important Banks (G-SIB), implying an additional capital buffer of 1%. Its current market value is about $55 billion, and trades in the U.S. on the New York Stock Exchange .

One of its largest shareholder is the Government Pension Fund of Japan, with a stake of almost 10%, and due to the bank's size and importance within the Japanese banking system as a top three financial institution in the country there is a high likelihood of government support in case of need. This means that during tough periods, the bank may receive liquidity or capital injections from the government, but this doesn't necessarily mean that shareholders will be bailed out.

The bank is headquartered in Tokyo and operates under several segments of the financial industry, including retail and commercial banking, capital markets, plus other financial services. While the bank has a great exposure to its domestic market, its strategy has been to diversify its business profile in overseas markets, especially in Asia-Pacific and the Americas.

Its loan book is highly exposed to Japan (62% of total loans), while international markets with great weight are the Americas (39% of total international loans), Asia-Pacific (34%), while Europe, Middle East, and Africa account or the rest. Even though its loan book has a good diversification, Sumitomo has a conservative lending approach and has not seek growth at the expense of risk, thus its balance sheet risk profile is quite low and this trend is likely to be maintained over the coming years.

On the other hand, the bank has a sizable equity portfolio of Japanese equities, which it intends to reduce to have less exposure to capital markets and decrease its earnings volatility. From 2015-2020, Sumitomo sold about $3.5 billion from its equities portfolio, aiming to reduce a further $2 billion by the end of 2025. Its goal is to reduce the bank's domestic equities portfolio to less than 10% of its common equity tier 1 (CET1) ratio, compared to about 12% nowadays.

Despite this strategy, Sumitomo has recently made a strategic alliance with Jefferies Financial Group ( JEF ) to combine its U.S equities and M&A business, and also bought an equity stake in the U.S. investment firm. Sumitomo currently holds about 5% of Jefferies, but wants to increase its stake if regulator approves, aiming potentially to grow its stake above 20% in the coming years. Given that Jefferies has a market value of about $7.6 billion, this means Sumitomo still aims to reduce its net equity exposure over the next couple of years.

Contrary to what is usual in the banking sector, that is to hold a sizable bond portfolio for liquidity purposes, Sumitomo's domestic bond portfolio is relatively small taking into account that it only represents about 5% of total assets. This means that Sumitomo is not much exposed to potential losses of higher interest rates in Japan, plus its portfolio also has low duration, thus it's not much exposed to rising rates. Nevertheless, while inflationary pressures have led to higher rates across many developed economies, interest rates in Japan remain at very low levels and the prospects of higher rates are quite low in the near future.

Additionally, its bond portfolio is comprised mainly of government, municipal, and other low-risk entities, thus credit risk is quite low and potential credit losses from this portfolio aren't a reason of concern.

Beyond its domestic bond portfolio, the bank also holds a foreign bond portfolio mainly in US dollar, which represent about 4.5% of its total assets. This portfolio is also relatively low risk and well diversified, but has a higher duration that is domestic bond portfolio (4.4 years vs. 2.9 years), thus it's more exposed to interest rate risk. Like has happened to U.S. banks in recent quarters, rising interest rates is negative for the bank's Other Comprehensive Income (unrealized losses on bonds), but due to the relatively small size in its balance sheet, this isn't also a major concern regarding Sumitomo's risk profile.

Regarding growth prospects, they are relatively muted as the bank is heavily exposed to its domestic market, which is characterized by low levels of economic growth and ultralow interest rates, while in foreign markets it may have better growth prospects. However, the bank's conservative risk culture is a clear limitation on growth, given that is priority is to have a sound financial profile over the long term, rather than seeking growth at the cost of lower loan underwriting criteria.

Financial target (Sumitomo)

Financial Overview

Regarding its financial performance, Sumitomo's track record is not properly impressive given that the bank's financial results have been rather stable over the past few years, reflecting its low-growth prospects. This situation is not expected to change much in the near future, as the bank is heavily exposed to its domestic market, which has low growth projections for the foreseeable future.

In its last fiscal year 2023 , which ends in March, Sumitomo's revenues increased due to higher loan volumes and interest rates, especially in its foreign operations. Total revenues amounted to nearly $27 billion, an increase of 6.3% YoY. Beyond positive growth at its core banking business, Sumitomo also reported strong results in its payments segment, and reported equity gains on affiliates, namely related to gains in its stake in Bank of East Asia.

Regarding costs, despite the inflationary environment the bank was able to report lower costs in the last fiscal year, which together with higher revenues led to better efficiency. Despite that, its cost-to-income ratio was 63% in FY 2023, and has been consistently between 60-68% over the past nine years, which is an acceptable efficiency ratio but higher than compared to the most efficient banks in the world. This is justified in large part by the ultralow interest rate environment in Japan, thus it's not expected that Sumitomo will be able to improve much its cost-to-income ratio over the coming years.

Regarding loan loss provisions, due to its good credit quality and conservative loan underwriting criteria, its credit risk ratio has remained at relatively low levels in the recent past, even though in FY 20222 it reported a slight increase due to its exposure to Russia, to a total of $1.9 billion. In FY 2023, loan loss provisions declined to $1.5 billion, with most provisions being related to corporate exposures. Its guidance is to increase slightly provisions related to FY 2024, to $1.6 billion as higher interest rates in international markets is expected to negatively impact credit quality.

Its total profit for the year was nearly $6.3 billion and its return on equity (ROE) ratio, a key measure of profitability in the banking sector, was only 6.5%. This is a relatively low level of profitability and below the bank's cost of capital, a level that is justified by the bank's structural profile and issues. Indeed, over the past eight fiscal years, its ROE has been between 4.5%-7%, showing that low profitability is a feature of its business profile.

On the other hand, its stable profile and conservative risk culture lead to low capital requirements, which is positive to distribute a good part of its earnings to shareholders. Its capital requirement at the end of last March was only 8%, while its CET1 ratio was above 10%, thus the bank has a comfortable capital buffer and does not need to retain much earnings to build out its capital ratio in the coming years.

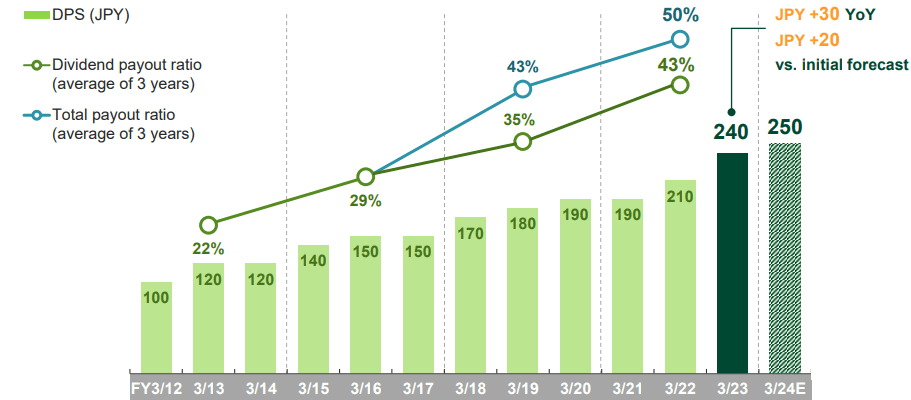

Taking into account this background, it's not surprising that Sumitomo has taken a more aggressive approach regarding shareholder remuneration, increasing at annual dividend by 30% YoY. The bank has a very good dividend history, even though its dividend payout ratio was quite conservative, and has been gradually increased over the past few years. Its current payout ratio is currently about 50% of annual earnings, a level that is quite good and may be further increased in the near future, providing a strong backdrop for a sustainable dividend over the long term.

{kind=link}

Indeed, according to analysts' estimates and the bank's own guidance, its dividend is expected to maintain an upward trajectory over the next three years, expected to increase at about 5% annually during this period. At its current share price, Sumitomo offers a dividend yield of about 3.9%, and has some prospects of improvement ahead, given that is dividend is expected to grow gradually in coming years. On the other hand, there are other banks in higher dividend yield both in the U.S. and Europe, as I've covered in previous articles , thus Sumitomo's yield doesn't seem to be currently high enough to attract income investors.

Conclusion

As I mainly cover the financial sector and my personal income portfolio is highly geared to this sector, I decided to analyze Sumitomo has a potential diversification play due to its exposure to a different region (Asia-Japan), as my portfolio is invested mainly in U.S. and European plays.

However, its dividend yield is not attractive enough and its current valuation (price-to-book value ratio of 0.65x) seems fair taking into account its fundamentals, thus Sumitomo is a pass for me for the time being.

For further details see:

Sumitomo Mitsui Financial Group: Potential Diversification Play Is Not Attractive Enough