SUN - Sunoco: After Years Of Waiting Higher Distributions Should Be Coming

Summary

- Despite growing larger, Sunoco has not increased their distributions since 2016.

- They enjoyed surprisingly strong cash flow performance during 2022 and given their guidance for 2023, this appears set to continue.

- They should be able to balance higher growth capital expenditure whilst still generating ample free cash flow to fund their existing distribution payments.

- This in turn makes higher distributions more likely than any other time in recent history.

- Whilst their unit price is trading around five-year highs, I nevertheless still believe that upgrading to a buy rating is now appropriate.

Introduction

When last reviewing Sunoco ( SUN ), they had enjoyed a surprisingly strong start to 2022, but alas, still only the same distributions were being declared, as my previous article discussed. Now that the calendar has rolled around to a new year, it feels timely to provide an update for what sits ahead in 2023 and thankfully, after years of waiting, it finally seems that higher distributions should be coming in the not-too-distant future.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

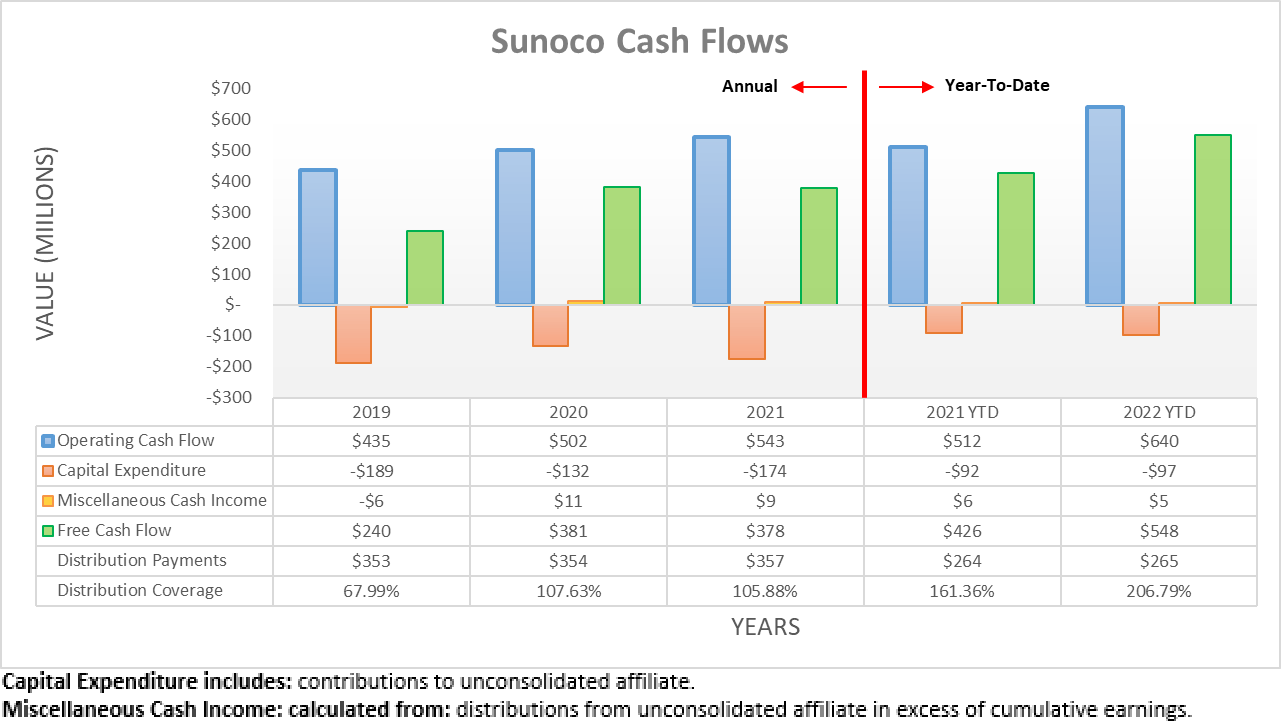

After seeing a surprisingly strong start to 2022, their cash flow performance continued powering onwards throughout the third quarter. When it comes to their operating cash flow, it landed at $640m and thus exactly 25% higher year-on-year versus their previous result of $512m during the first nine months of 2021. Thanks to their capital expenditure remaining restrained, this resulted in their free cash flow surging to $548m versus $426m across these same two periods of time, respectively.

{kind=link}

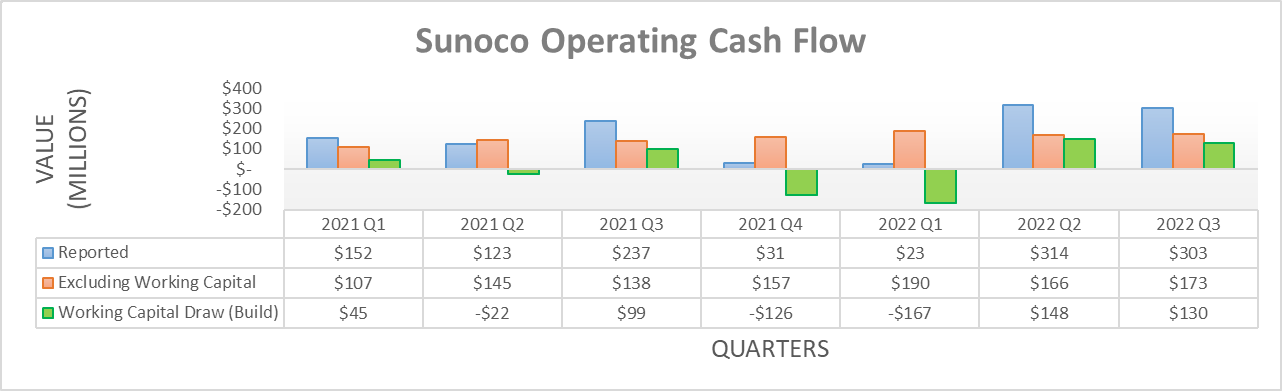

Admittedly, when viewed on a quarterly basis, some of their cash generation during 2022 stemmed from working capital movements. To this point, the second and third quarters saw draws of $148m and $130m respectively, which were sizeable and more than offset the build of $167m during the first quarter. Although even if excluded, their underlying operating cash flow during the first nine months was $529m and thus actually an even stronger 35.64% higher year-on-year versus their previous equivalent result of $390m during the first nine months of 2021. Whilst very impressive and once again better than many would have envisioned, the bigger and more important topic right now is their outlook for 2023.

Sunoco December 2022 Investor Presentation

{kind=link}

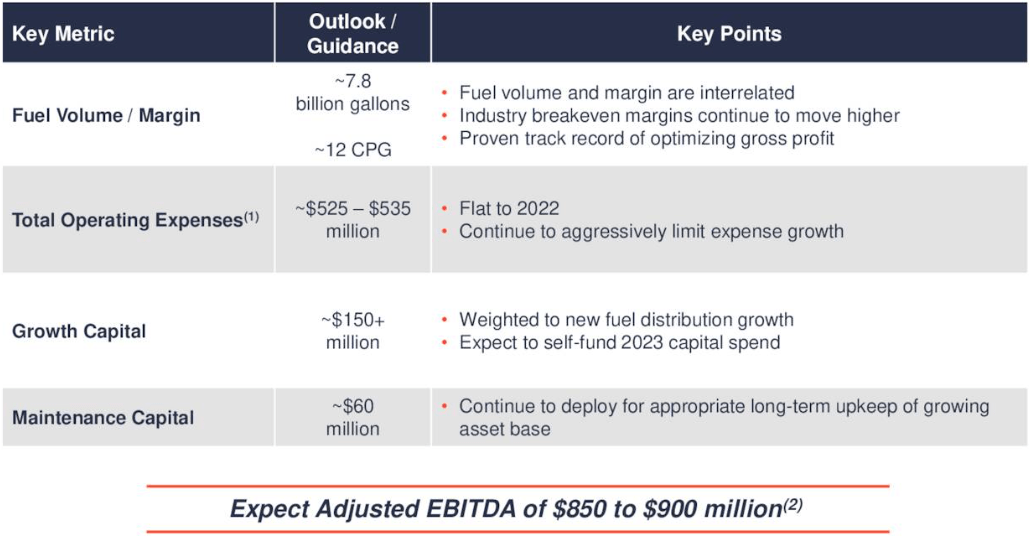

When reviewing their guidance for 2023, the most important aspect is their adjusted EBITDA forecast of $875m at the midpoint, which is ever-so-slightly above their guidance for 2022 of $855m at the midpoint, as per their third quarter of 2022 results announcement . Given its closeness, it stands to reason their operating cash flow during 2023 should be very similar to 2022 given their positive correlations, excluding working capital movements. Since their underlying operating cash flow of $529m during the first nine months of 2022 annualizes to circa $700m, this makes for a reasonable basis expectation, not just for their upcoming 2022 results but also those for 2023.

Elsewhere, they see growth capital expenditure of $150m+ and accompanying maintenance capital expenditure of circa $60m, thereby making for total capital expenditure of circa $210m+. If looking backwards, this would mark the highest level in recent history, with 2019-2021 seeing a high point of $189m with an average of only $165m. On one hand, higher capital expenditure consumes more of the cash they generate, but on the other hand, it also should lead to growth, thereby generating more cash in future years.

Thankfully, even with this higher capital expenditure and no additional growth, this guidance indicates they should still generate around $500m of free cash flow during 2023. In turn, this should make way for strong distribution coverage of circa 140% given their payments cost $357m during full-year 2021 and remain unchanged to date.

Even though they have not formally issued guidance for higher distributions, I suspect that after years of waiting, the day is finally approaching. Largely because they clearly have the spare capacity within their free cash flow, thereby meaning they can fund any increase without leaning further upon debt markets. Equally as important, this is running in conjunction with their higher capital expenditure that largely relates to growth, which in turn creates another reason to expect higher distributions are finally just around the corner, proverbially speaking. If this comes to pass, it will be the first time since 2016 their distributions have been increased and whilst I am not necessarily expecting a big increase, it nevertheless is a positive change for unitholders.

{kind=link}

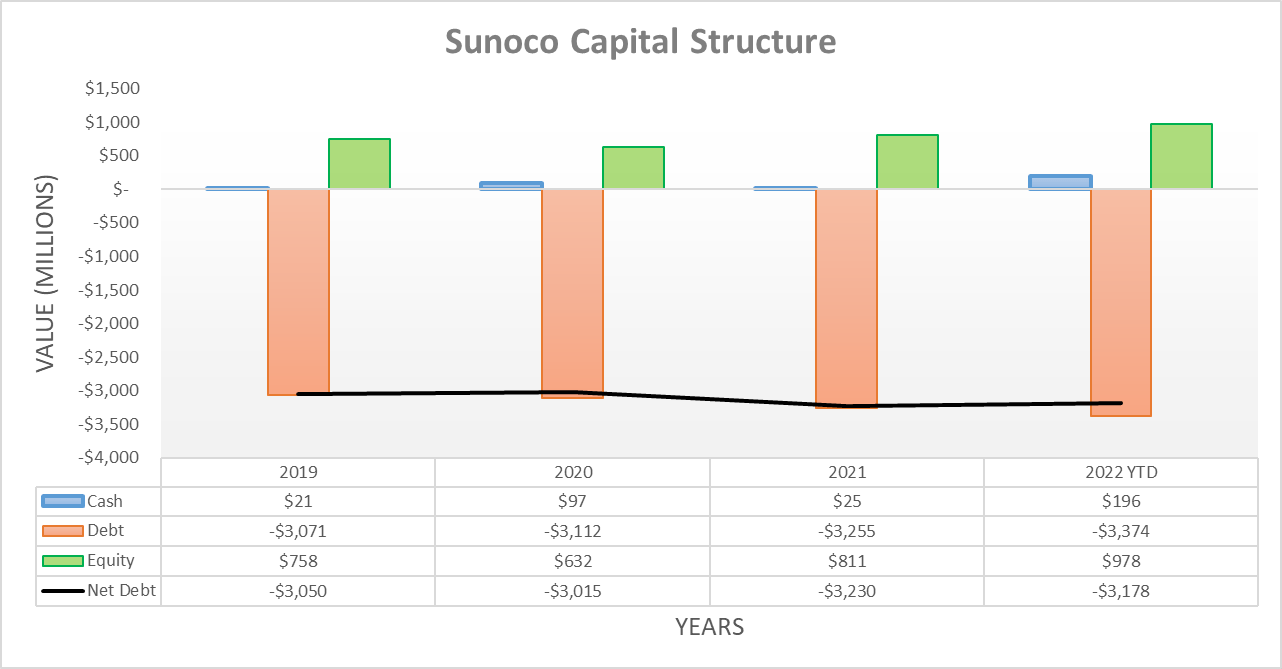

Thanks to their ample cash generation during the third quarter of 2022, their net debt edged lower to $3.178b versus its previous level of $3.37b following the second quarter. As for the recently ended fourth quarter, it should broadly track sideways, give or take a little depending upon working capital movements. As for 2023, it should continue heading lower given their prospects to generate excess free cash flow after distribution payments, barring any presently unknown acquisitions.

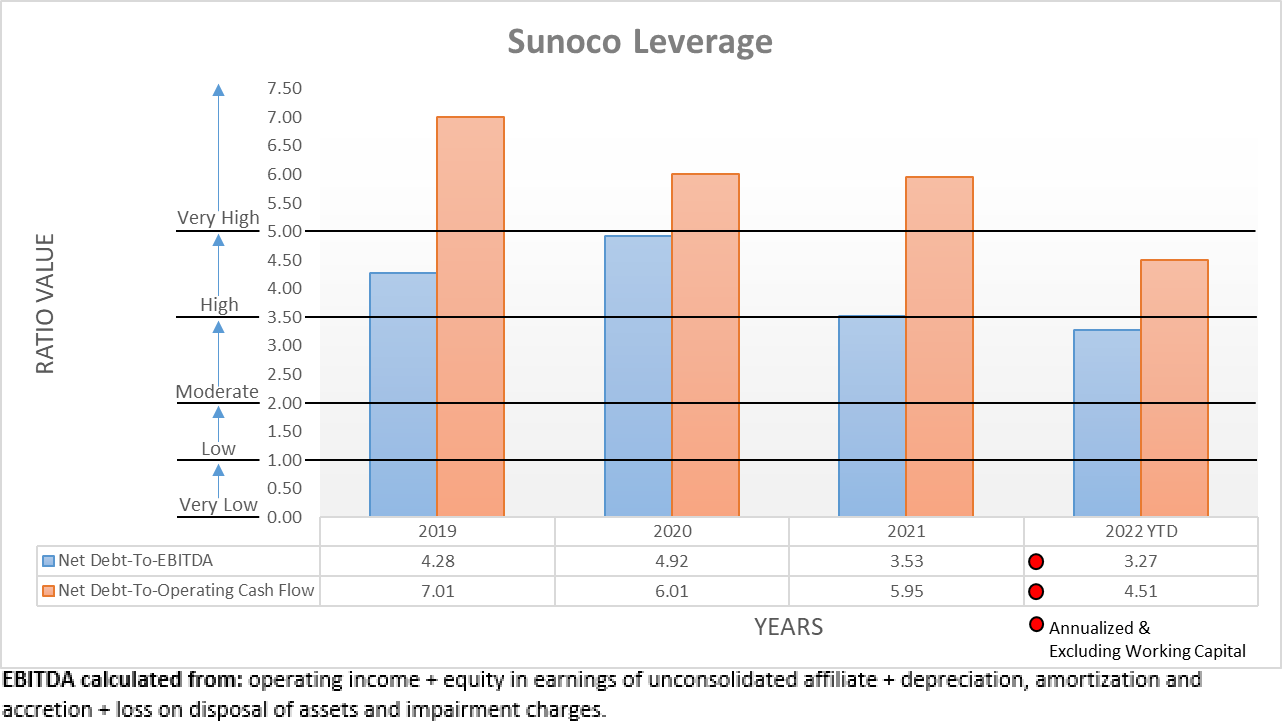

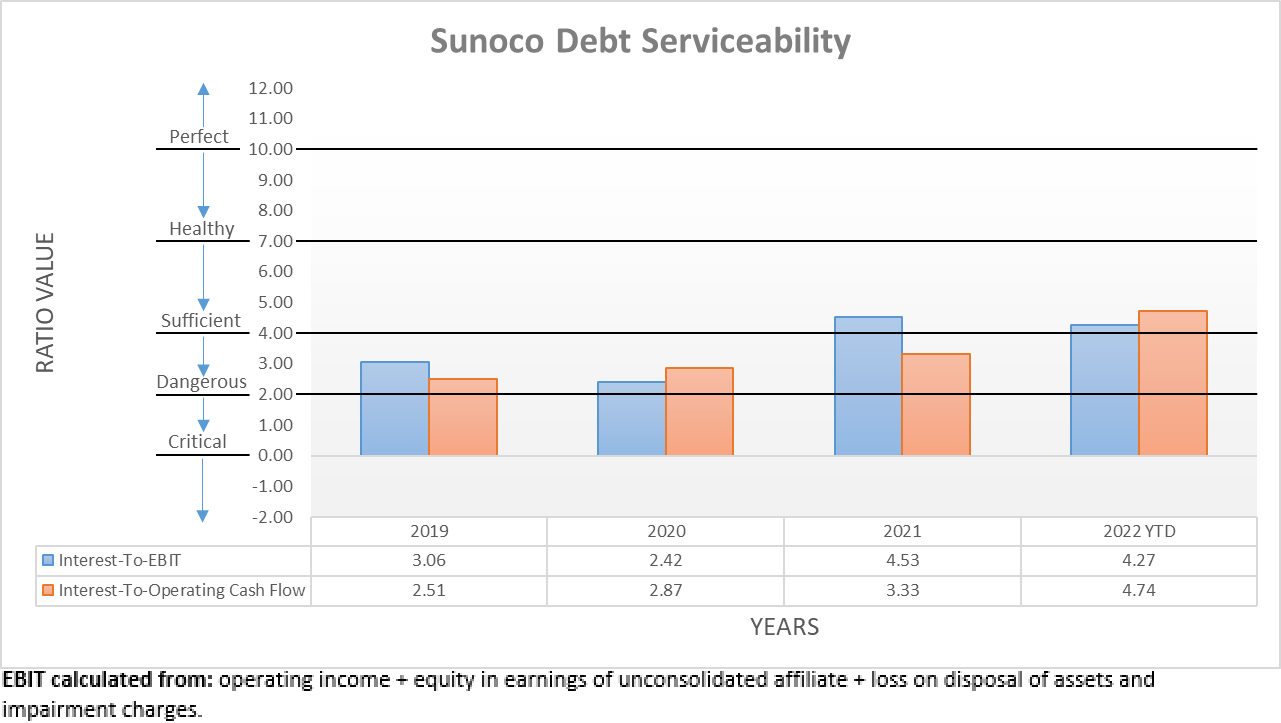

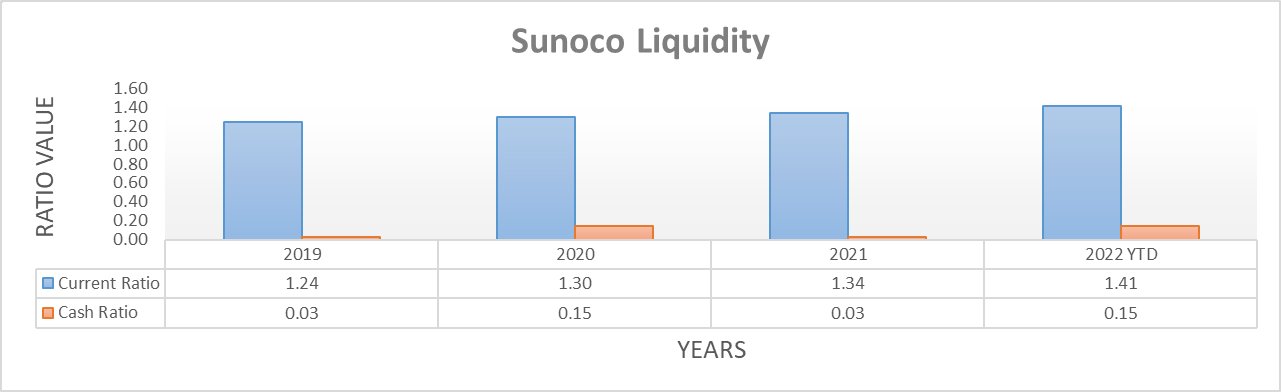

Since their net debt is only slightly lower, it would be redundant to reassess their leverage or debt serviceability in detail, as this was done when conducting the previous analysis and the focus of this update was their outlook for 2023. The same also applies to their liquidity, as their cash balance of $196m following the third quarter of 2022 remains immaterially different to their previous balance of $168m following the second quarter.

The three relevant graphs are still included below to provide context for any new readers that show their leverage sees a net debt-to-EBITDA of 3.27 and a net debt-to-operating cash flow of 4.51. Whilst the latter resides within the high territory of between 3.51 and 5.00, their stable financial performance keeps risks under wraps and thus does not inhibit providing higher distributions. Plus, their debt serviceability remains healthy with interest coverage of 4.27 and 4.74 when compared against their EBIT and operating cash flow, respectively. Concurrently, their strong liquidity persists, with a current ratio of 1.41 and a cash ratio of 0.15. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

Conclusion

After years of waiting, it finally seems that higher distributions should be coming with solid guidance for 2023 that encompasses an outlook for both ample free cash flow and higher growth investments in conjunction with each other. On one hand, their unit price is trading for a five-year high, but on the other hand, they still offer a desirable high single-digit distribution yield that I now expect to resume growing. When balanced, I believe that upgrading my previous hold rating is appropriate but only marginally to a buy rating and thus not a strong buy rating.

Notes: Unless specified otherwise, all figures in this article were taken from Sunoco’s SEC filings , all calculated figures were performed by the author.

For further details see:

Sunoco: After Years Of Waiting, Higher Distributions Should Be Coming