SUN - Sunoco Is A Solid Income Option But IDRs Are Burdensome

2023-09-01 13:05:26 ET

Summary

- Sunoco has been growing its EBITDA and is a potential option for income-oriented investors.

- The transition from combustible engine vehicles to electric vehicles (EVs) poses a risk to Sunoco.

- Sunoco's opportunities lie in margins, volumes, and acquisitions.

While Sunoco ( SUN ) will have to navigate the EV transition, the company has been doing a solid job growing its EBITDA the past few years and looks like an option for income-oriented investors to consider. However, I consider its IDRs as a big negative.

Company Profile

SUN markets and distributes motor fuel in 40 states across the East Coast, Midwest, South Central and Southeast, as well as in Hawaii and Puerto Rico. The company distributes its fuel under long-term contracts to about 7,400 dealer, distributor, and commission agent customers and approximately 1,600 commercial customers. It is the exclusive wholesale supplier of the Sunoco-branded and EcoMaxx-branded motor fuels, but it also distributes branded motor fuel under the Aloha, Chevron, Citgo, Conoco, Exxon, Mahalo, Mobil, Phillips 66, Shamrock, Shell, Texaco, and Valero brands.

7-Eleven is its largest customer and only dealer or distributor that accounts for 10% or more of revenue, and the company has a long-term take-or-pay supply agreement with the company. It also has 76 company-operated locations in Hawaii and in New Jersey along the Turnpike.

The company owns 42 refined product terminals that have about 20 million barrels of storage capacity. It also operates four transmix facilities. The company also controls around 950 real estate locations and owns around 600 of them, where it derives ratable lease income.

Energy Transfer ( ET ) owns just over 28% of the company, as well as its GP and incentive distribution rights (IDRs).

Opportunities and Risks

When looking at risks, the biggest is the ongoing transition from combustible engine vehicles that use motor fuel to electric vehicles (EVs) that use charging stations. While Telsa ( TSLA ) has carved out a niche as the leading EV maker, traditional automakers are also moving more production towards EVs. Earlier this week, it was reported that Ford ( F ) will discontinue three gas model vehicles to focus on its second-generation EV platform. General Motors ( GM ) is also in the midst of a big EV push as well through its Ultium platform , while European and Asian automakers also have EV offerings.

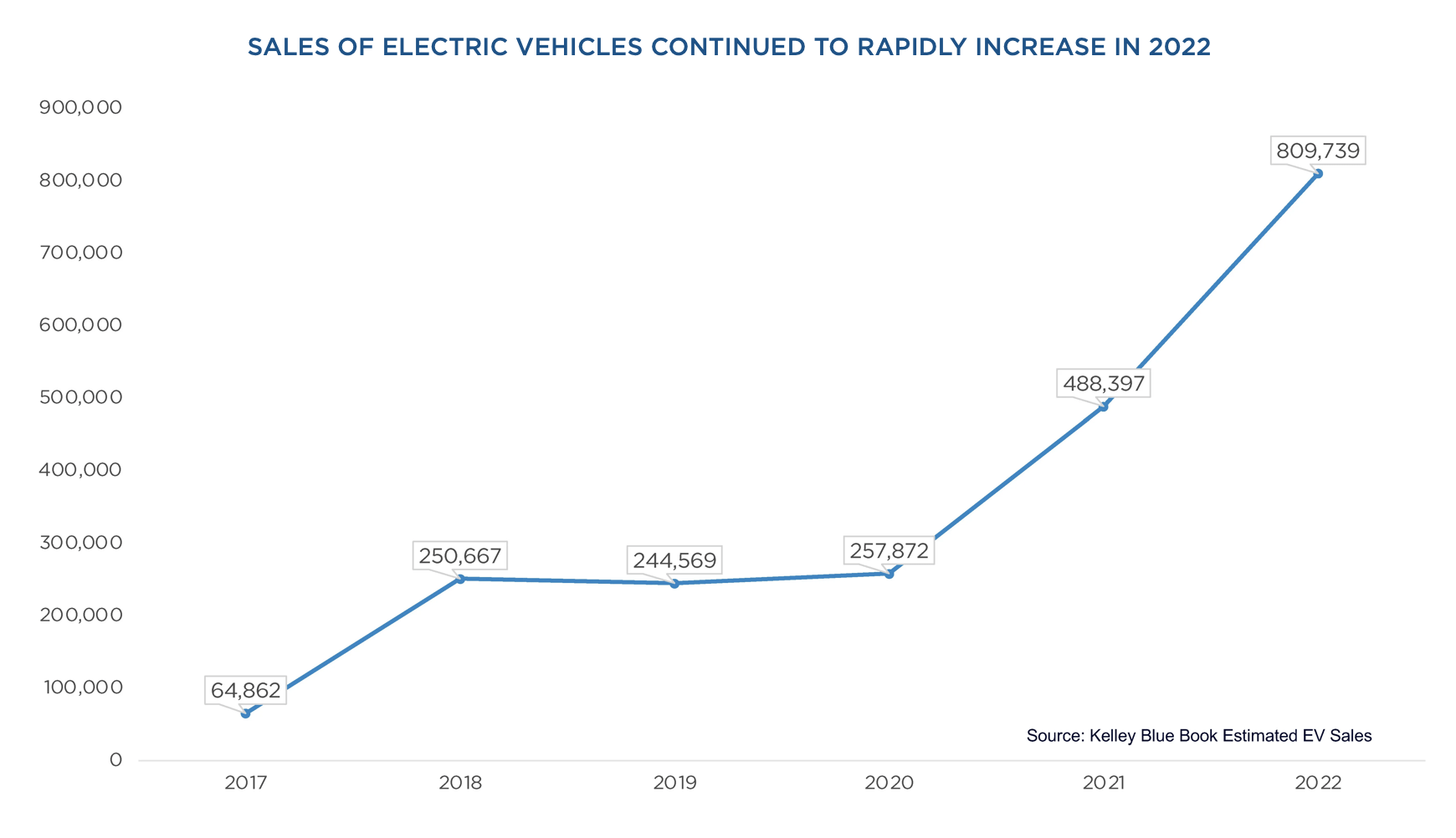

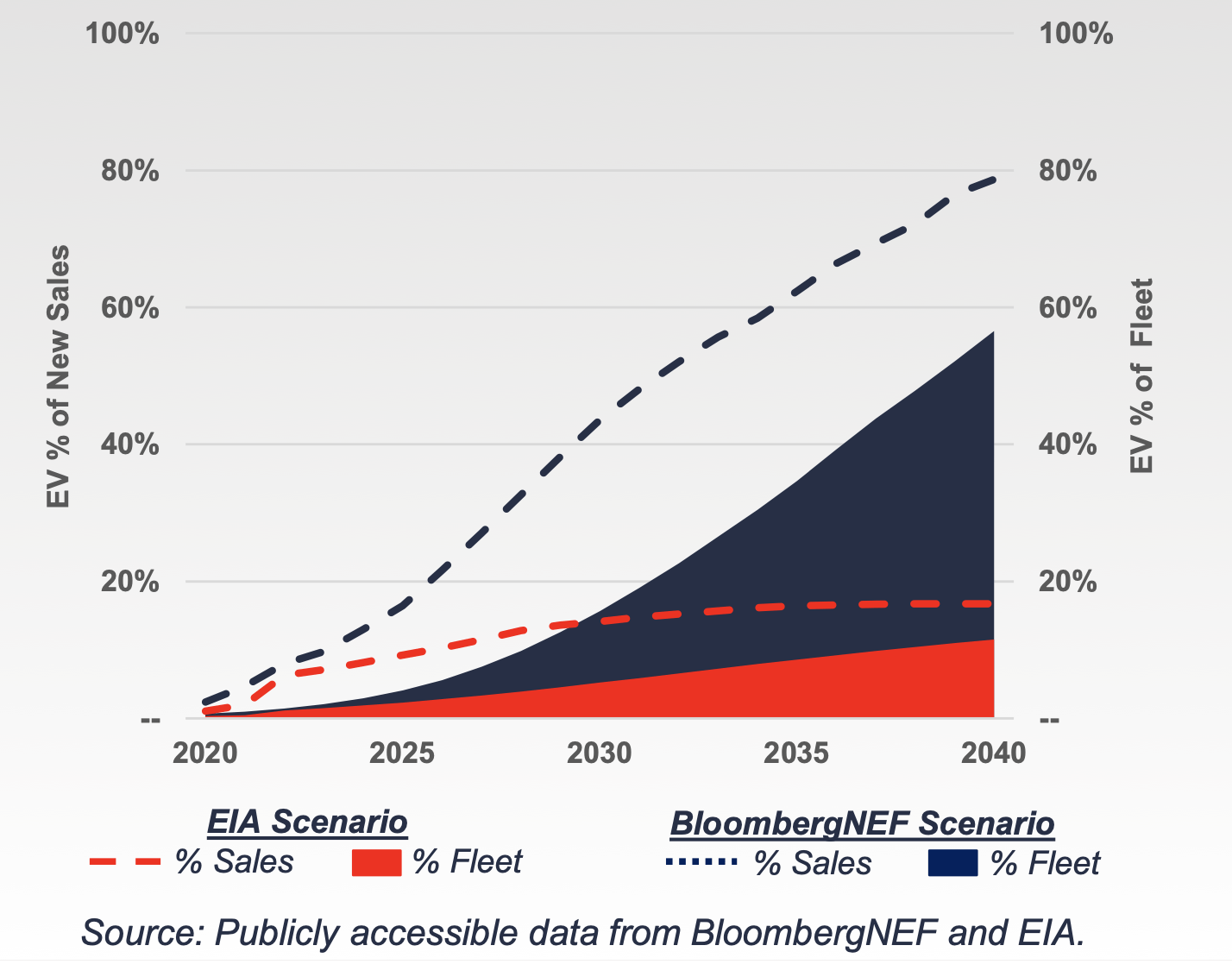

The Biden Administration, meanwhile, set a goal to have 50% of new car sales to be EVs by 2030. EVs were 5.8% of new U.S. vehicle sales in 2022, up from 3.2% in 2021, and rose to nearly 7% in Q1 of this year. Still there are approximately 285 million vehicles registered in the U.S., of which only 1 .7 million are EVs . At a goal of 50% new car sales being EVs, that would put around 7 million new EVs on the road per year.

{kind=link}

One issue with that goal, however, also comes from the amount of lithium, nickel, cobalt and other materials needed to make the batteries for EVs, and who controls these materials. About 70% of global lithium mined comes from Australia and Chile, while Bolivia is sitting on a lot of deposits. China, meanwhile, refines about 60% of the lithium that is extracted. To meet net-zero goals by 2040, lithium demand would grow 40x. The Congo, meanwhile, controls 75% of cobalt extraction. The ramp-up of EV market share, thus might not be quite as smooth as some government goals, as the EIA sees a much slower transition.

{kind=link}

Nonetheless, the EV transition and its pace is the biggest risk to SUN. When it comes to opportunities, margins, volumes and acquisitions are three of the big areas for SUN.

SUN's results are largely based on its gross margins and the volumes it distributes. On the margin front, its take-or-pay supply agreement with 7-Eleven, as well as its terminal storage and throughput fees indexed to inflation, and rental income help add a little stability. It divested most of its more volatile retail network over 5 years ago, selling it to 7-Eleven and locking in that take-or-pay agreement in the process.

Over the past several years, the company has really focused on a gross margin optimization program, and looks at volumes and margins holistically, trying to optimize the best balance. One example of this is the company developing individual location-by-location elasticity curves so that when it sets a price on a daily basis, it takes into account what the anticipated volume impact of that is.

SUN's margins have benefited from a trend of increasing industry breakeven margins. Margins can also benefit from volatile fuel prices, and the company's margins typically benefit whenever RBOB prices decrease.

On the volume front, SUN's volumes still remain below pre-Covid levels of 8.2 billion gallons. However, volumes have grown steadily from 2020 when its volumes were 7.1 billion gallons to 7.7 billion gallons in 2022, as households emerged from Covid and began to travel more. The company is projecting around 7.8 billion gallons this year. With more companies in the U.S. demanding its employees return to work in the office full time or more often, this should continue to drive fuel demand.

Acquisitions have also been a driver for SUN. Its most recent deal was the acquisition of 16 terminals from Zenith Energy. Earlier, it bought Peerless Oil & Chemicals to expand its distribution and terminal business in Puerto Rico and the Caribbean. It has also added terminal assets in deals with NuStar ( NS ) and Gladieux over the past few years. These deals have allowed the company to both expand its market, as well as realize synergies through vertical integration to help improve results.

When it comes to risks outside of the EV transition, declining volumes due to things like the economy is one. While driving is a necessity, people do tend to drive less during a recession. And while margins can benefit from lower or volatile prices, steadily rising prices can negatively impact them.

It is also worth noting that SUN is one of the few master limited partnerships (MLPs) that still have IDRs. IDRs are like a large tax on distribution increases, and something I view negatively. The company is in the high splits, which means that ET is nicely benefiting every time SUN raises its distribution.

Distribution

SUN currently has a yield of about 7.4%, paying out a distribution of 84.2 cents. The company increased its payout earlier this year from 82.55 cents. It was its first distribution raise since 2016.

With a Q2 coverage ratio of 1.9x, the distribution was well covered. Its leverage was 3.6x at the end of Q2, which is also solid for an MLP, and down from 4.5x from Q2 2018.

The one knock on SUN's distribution is that the MLP still has IDRs, which are currently in the high splits. For any incremental payment above 65.6 cents, the company essentially forks over a 50% "tax" to its GP owned by ET. That limits distribution increases and essentially makes increasing the distribution a poor use of capital allocation.

{kind=link}

Valuation

SUN trades at 8.4x the 2023 EBITDA consensus of $918.2 million. Based on the 2024 EBITDA consensus of $924.3 million, it is valued at 8.3x.

The stock has an attractive free cash flow yield of about 13% based on my 2023 projections calling for $500 million in FCF.

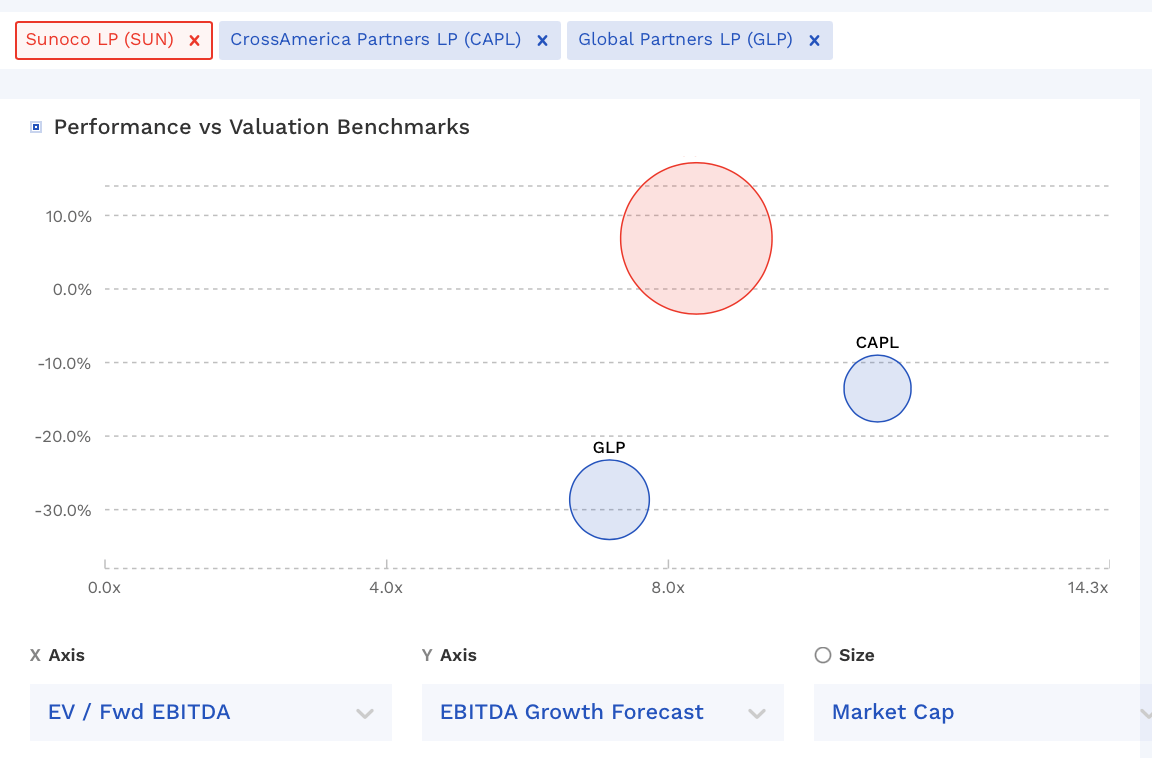

SUN trades between CrossAmerica ( CAPL ) and Global Partners ( GLP ), but analysts are expecting stronger growth for it.

SUN Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

SUN has done a solid job growing its EBITDA and paying down debt over the past few years, despite having to deal with the impacts of the pandemic and a big drop in driving. Leverage has gone from 4.5x in Q2 2018 to 3.6x in the most recent quarter.

The EV transition is a long-term risk, but given the supply chain challenges to extract the materials to make the batteries, the transition could take longer than many are expecting.

Overall, SUN has been a solid investment the past few years and management has done a nice job to re-position a company that was highly leveraged several years ago.

That said, I don't like the IDR structure and don't think it is unitholder-friendly. I think the stock is a solid "Hold" for income-oriented investors that currently own the name, but I would not put new money towards into the stock as long as it has IDRs.

For further details see:

Sunoco Is A Solid Income Option, But IDRs Are Burdensome