SUN - Sunoco: Near-8% Yield Should Hold Up During A Potential Recession

2023-03-29 16:58:48 ET

Summary

- When the calendar flicked over to 2023, it seemed that higher distributions should be coming soon for Sunoco.

- Subsequently, capital markets have endured turbulence, with talk of a banking crisis that could lead to a recession.

- The company's resilient cash flow performance endured the severe downturn of 2020 and thus can endure whatever 2023 might hold, in my view.

- Most importantly, their cash inflows should outpace their accompanying outflows, which isolates the partnership from a banking crisis as much as possible.

- Even without higher distributions, they still offer a high near-8% yield that can survive, and thus, I believe that maintaining my buy rating is appropriate.

Introduction

Following Sunoco ( SUN ) posting solid guidance for 2023 that built upon their already surprisingly strong results for 2022, my previous article highlighted how after years of waiting, it seemed that higher distributions should be coming in the not-too-distant future. Subsequently, capital markets have endured turbulence with talk of a bank crisis, but thankfully, their high near-8% distribution yield should hold up during a potential recession.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

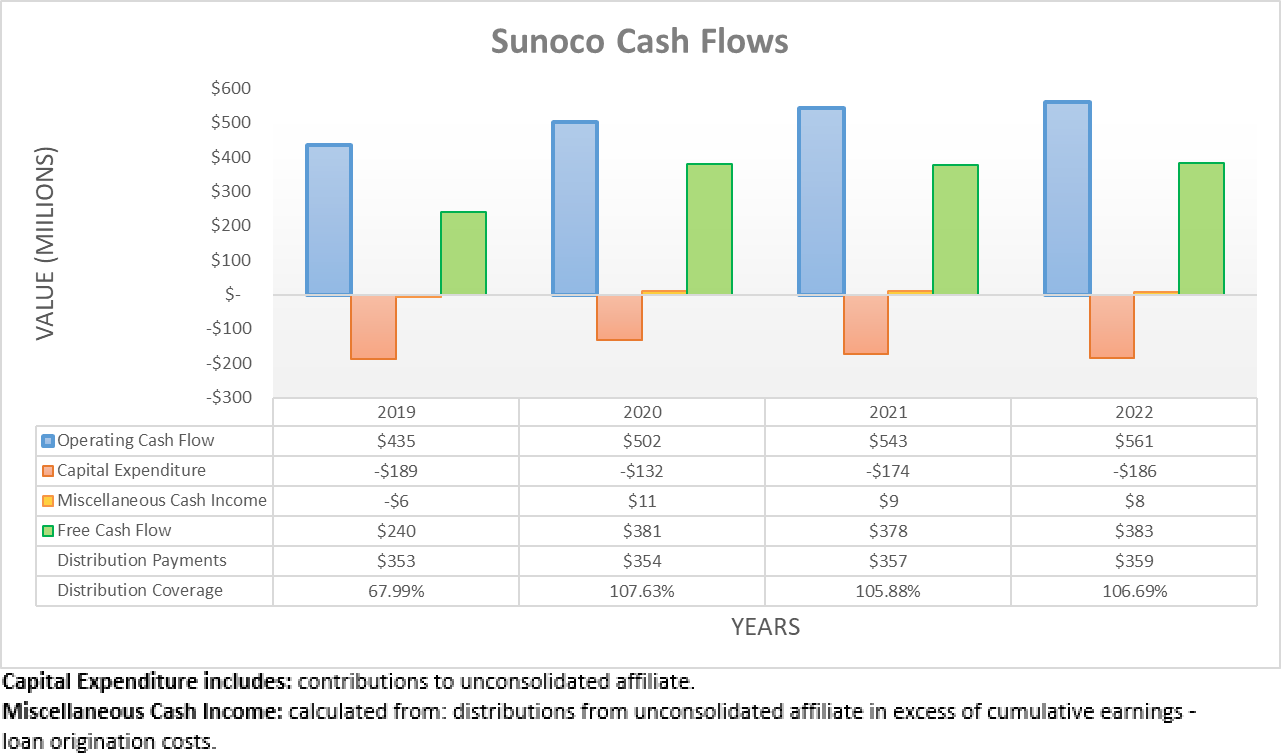

Earlier in 2022, their cash flow performance saw a surprisingly strong start that continued powering onwards throughout the third quarter but alas, this was not continued during the fourth quarter, at least on the surface. In fact, their operating cash flow actually ended the year lower than where it was following the first nine months at $561m and $640m, respectively. Nevertheless, it was quite impressive to see their free cash flow still reached $383m during the full year and thus was provided adequate coverage of 106.69% to their accompanying distribution payments of $359m.

{kind=link}

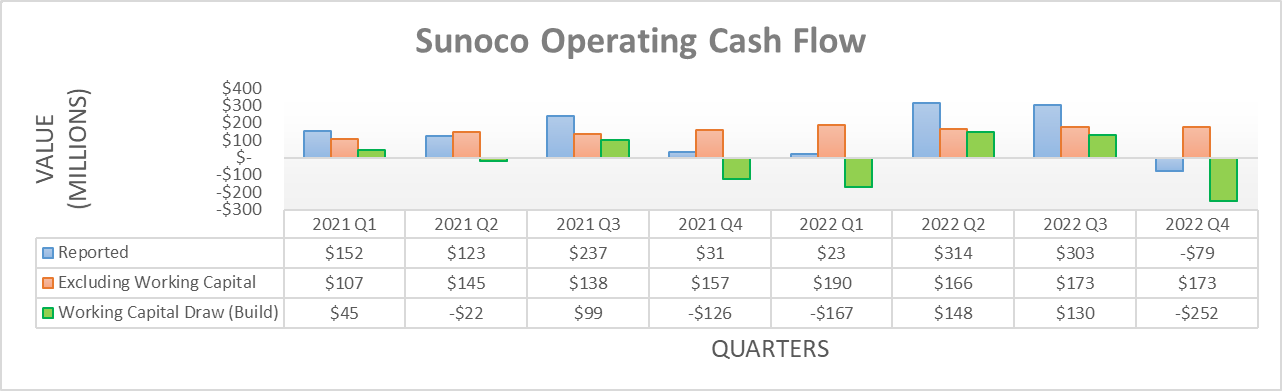

Thankfully, when looking at their quarterly cash flow performance, it shows the problem stemmed from an abnormally large working capital build of $252m during the fourth quarter of 2022, which is far larger than any other build or draw in recent history, at least since the beginning of 2021. If this were excluded, their underlying result during the fourth quarter of 2022 would have otherwise been $173m and thus on par with their result during the third quarter, which actually was the second-highest quarterly result in recent history.

Whilst their underlying cash flow performance made for a solid end to 2022 and thus created momentum going forwards into 2023, the recent weeks have seen turbulence in capital markets as a banking crisis emerged following the collapse of several regional banks in the United States. As of the time of writing, it seems that a fragile stability is returning to markets following the takeover of Credit Suisse ( CS ) but that said, it remains to be seen whether this is merely an intermission before it continues amplifying. In light of this concerning outlook that could foretell capital market turbulence on the horizon alongside a recession, it seems timely to assess their ability to navigate such an outcome and importantly, whether their distributions are at risk of being cut.

After reviewing their guidance for the year ahead when conducting the previous analysis, I estimated they should generate around $500m of free cash flow during 2023. In turn, this should see strong distribution coverage of circa 140% given their payments cost $357m during full-year 2021, unless they declare higher distributions in the coming quarters.

Naturally, the prospects of a recession on the horizon might see some investors worry about their ability to meet their guidance going forwards into 2023. Although, thankfully, their fuel distribution business enjoys remarkable resilient cash flow performance because most of their costs are variable and thus scale accordingly with their revenue. The best example was during the severe downturn of 2020 when Covid-19 lockdowns saw fuel demand plunge as people were literally not allowed to travel in many cases. Despite this headwind, their operating cash flow still clocked a result of $502m that, surprisingly, actually increased year-on-year versus their previous result of $435m during 2019.

If they can achieve this impressive feat throughout what was likely the worst operating condition possible, even a recession during 2023 should not cause any significant impact to their cash flow performance nor derail their guidance. Whilst this is very important, a solid financial position is still required for unitholders to sleep easy at night knowing their distributions are not at risk of being cut.

{kind=link}

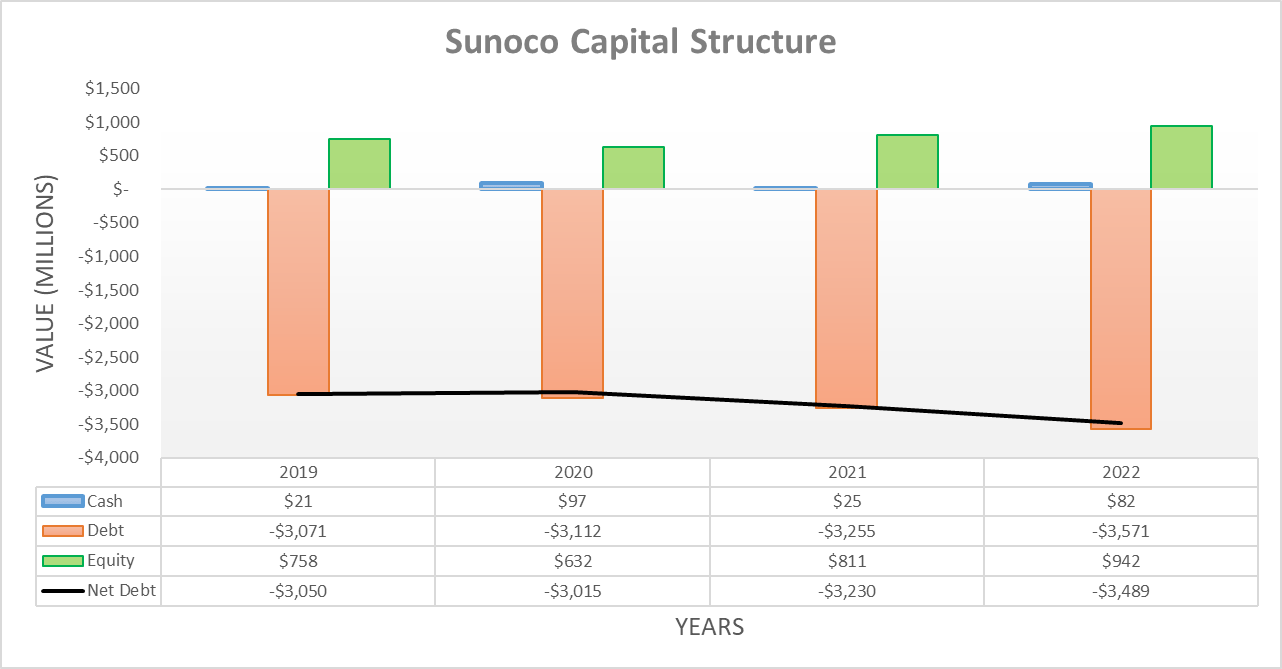

Due to their abnormally large working capital build during the fourth quarter of 2022, their net debt actually increased to $3.489b versus its previous level of $3.178b following the third quarter. Whilst not necessarily ideal, at least this should only be a mere blip on the radar, and going forwards into 2023, their prospects to generate excess free cash flow after distribution payments should see it heading lower, regardless of whether the banking crisis continues amplifying.

{kind=link}

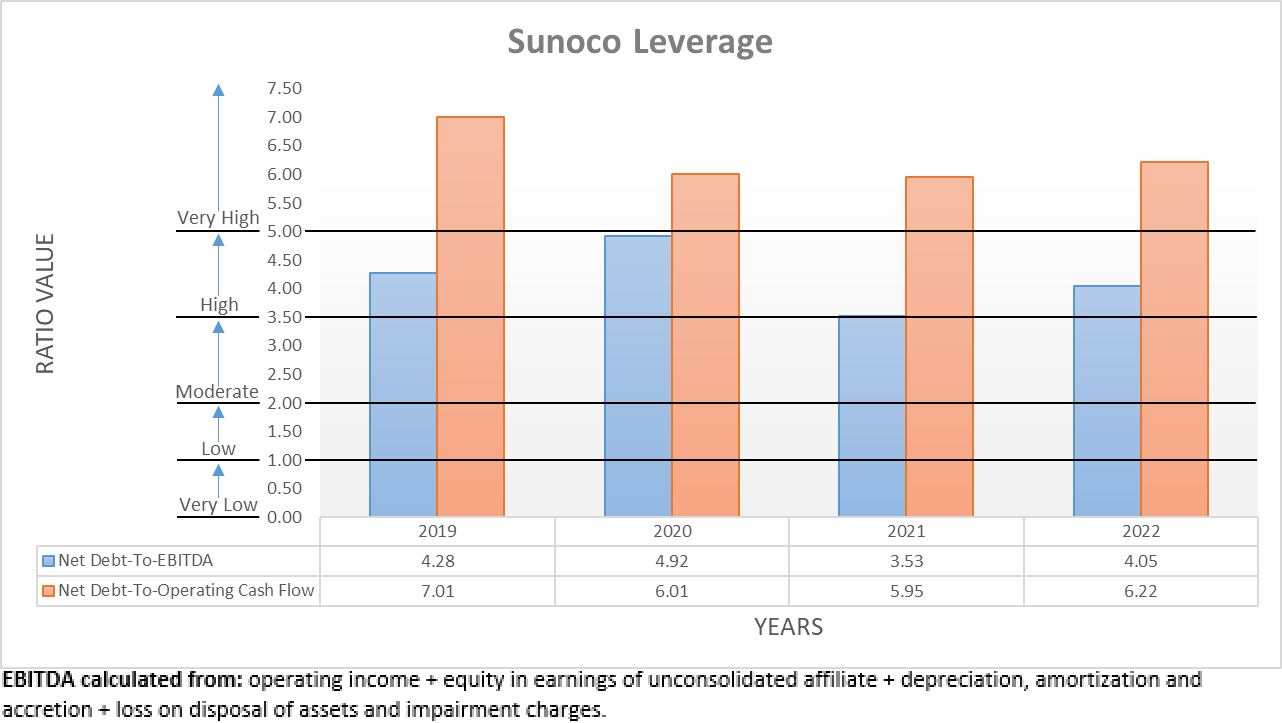

Unsurprisingly, their leverage was also impacted during the fourth quarter of 2022 as their net debt increased, but thankfully, it is not as bad as it seems on the surface. Whilst their net debt-to-EBITDA increased to 4.05 versus its previous result of 3.27 following the third quarter, the far bigger increase was their net debt-to-operating cash flow that soared to 6.22 versus 4.51 across these same two points in time, respectively. This was another impact of their abnormally large working capital build and whilst normally including these for full-year results, I feel that it should be excluded in this instance given its sheer size. If excluded along with their smaller builds and draws earlier in the year, it would have otherwise only seen a result of 4.95.

Whilst still representing an increase, at least it nevertheless sees both their net debt-to-EBITDA and net debt-to-operating cash flow remaining beneath the threshold of 5.01 for the very high territory and thus by extension within the high territory. Even though this might still sound concerning on the surface, thankfully their resilient cash flow performance largely removes the risk of their leverage becoming untenable, especially as their net debt should decrease going forwards into 2023.

{kind=link}

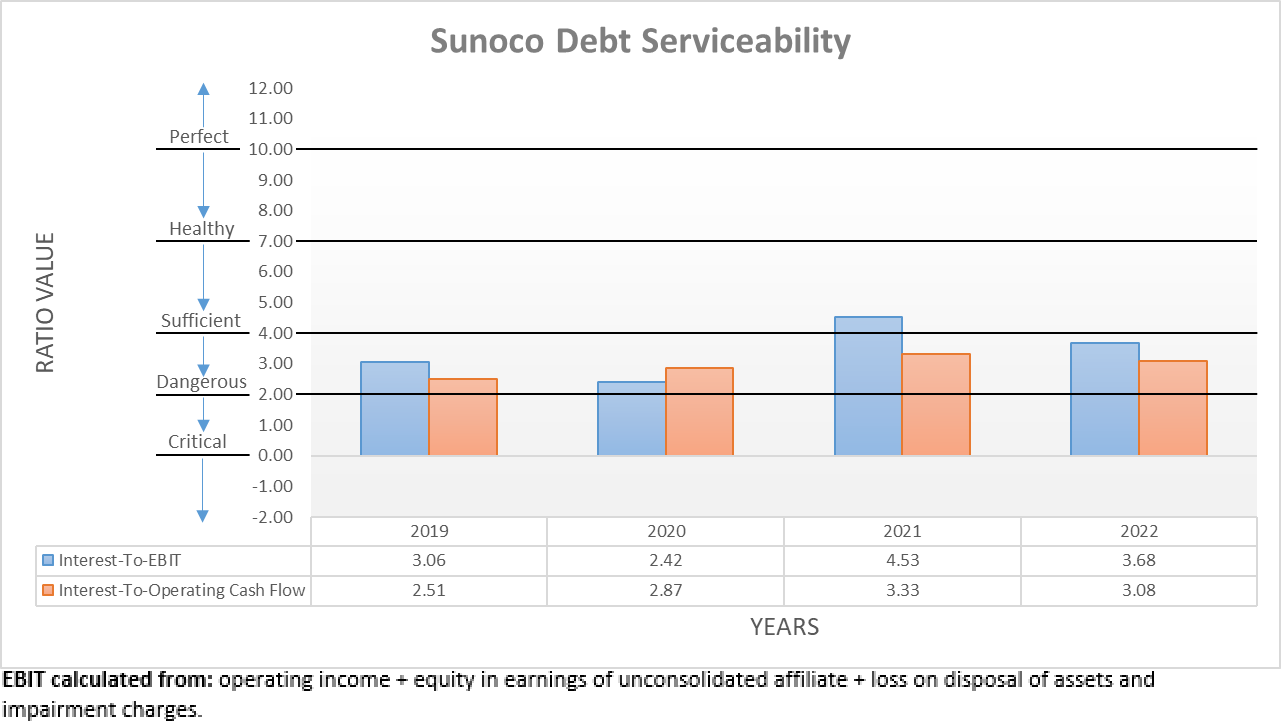

Similar to their leverage, their debt serviceability saw a similar impact during the fourth quarter of 2022. Although thankfully, their interest coverage is still sufficient with respective results of 3.68 and 3.08 when compared against their EBIT and operating cash flow, despite having decreased versus their previous respective results of 4.27 and 4.74 following the third quarter. Since only $900m of their total debt of $3.571b pertains to their credit facility and thus carries a variable interest rate, it should not create risks for their distributions, regardless of where monetary policy heads going forward into 2023.

{kind=link}

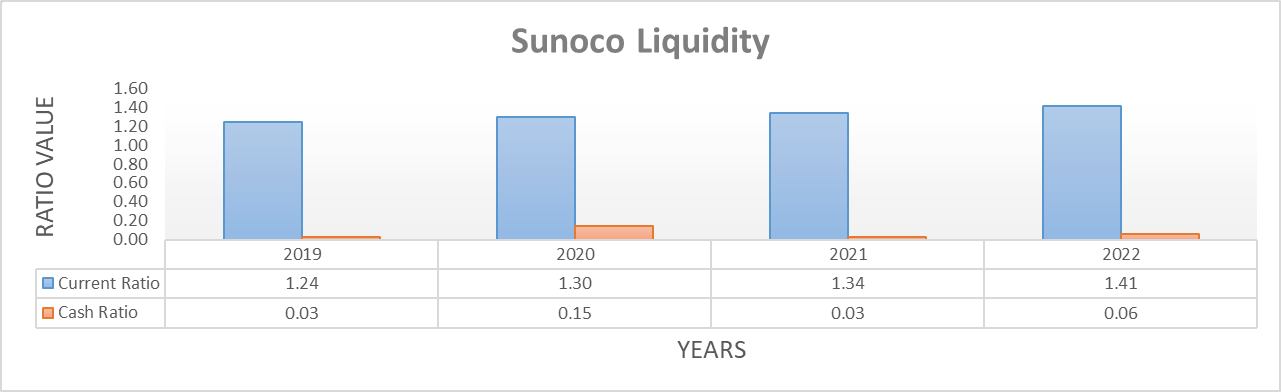

Whilst their leverage and debt serviceability are important, when a banking crisis arises, I feel their liquidity is actually more important. On this front, the fourth quarter of 2022 saw their current ratio unchanged at 1.41 versus its previous result following the third quarter, although their accompanying cash ratio decreased to 0.06 versus 0.15 across these same two points in time, respectively. Despite not necessarily being ideal per se, at least their liquidity remains adequate, and going forward into 2023, their prospects to generate excess free cash flow after distribution payments mostly remove reliance upon their credit facility.

This last aspect is arguably the most important consideration for the safety of their distributions because it means the partnership is a net contributor into capital markets, as their cash inflows outpace their accompanying outflows. Since they also do not see any debt maturities until as far away as April 2027, their lack of need to access capital markets effectively isolates the company from the banking crisis as much as possible. In normal times, requiring access to capital markets is not necessarily problematic, but if the banking crisis continues amplifying, it could make this difficult, and thus by extension, it could have otherwise created risks for their distributions.

Conclusion

Right now, it feels like the market is sitting in a state of limbo with a fragile stability waiting to see whether this banking crisis is over or continues amplifying. Even if the latter more painful path is forthcoming, at least their resilient cash flow performance and solid financial position ensure their distributions can survive, especially as they are a net contributor to capital markets going forwards into 2023. Although as a precautionary step, it would not be too surprising to see management hold off from declaring higher distributions that my previous analysis flagged until the turbulence in capital markets is definitely over. At least their high near-8% distribution yield remains desirable, and thus I believe that maintaining my buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Sunoco's SEC filings , all calculated figures were performed by the author.

For further details see:

Sunoco: Near-8% Yield Should Hold Up During A Potential Recession