SUN - Sunoco Q3: Operational Performance Has Been Strong But Stock Looks Fairly Valued

2023-11-17 16:15:09 ET

Summary

- SUN reported solid Q3 results, with strong volume growth.

- The company raised its full-year adjusted EBITDA outlook for the second time this year.

- While its operational performance has been strong, the stock looks fairly valued at the moment.

In my initial write-up on Sunoc o ( SUN ) from September, I said the company is a solid option for income-oriented investors but I viewed its incentive distribution rights (IDRs) as a negative. The stock has returned over 17% since then versus a slight decline in the S&P. With the company recently reporting earnings, let’s take a closer look at the stock.

Company Profile

As a refresher, SUN markets and distributes motor fuels across the U.S. and Puerto Rico under long-term contracts. It owns 42 refined product terminals with about 20 million barrels of storage capacity and operates four transmix facilities.

Its largest customer is 7-Eleven, with whom it has a long-term take-or-pay supply agreement. It also has 76 company-operated locations in New Jersey along the Turnpike, as well as in Hawaii. It also derives ratable lease income from the approximately 950 real estate locations its controls.

Q3 Results

For Q3, SUN saw revenue fall -4% to $6.3 billion. Motor fuel sales dropped nearly -8% to $5.8 billion. Non-motor fuel sales rose 21% to $109 million, while lease income increased nearly 6% to $38 million.

Gallons sold rose 7% to 2.124 billion. This was a record volume quarter for the company, which it contributed to organic growth and acquisitions, as well as increased demand in some markets. Its acquisition of Peerless at year-end 2022 played a big role in the year-over-year volume increase

Profit per gallon fell nearly -7% to 13 cents from 13.9 cents.

On its Q3 earnings call , COO Karl Fails said:

“ With respect to margins. The strong margin performance over the last few years continued in the third quarter as we delivered margins of $0.13 per gallon. There is no extraordinary story to share for this quarter. The continued combination of increased market volatility, higher breakeven margins and our gross profit optimization strategies delivered strong margins even with some rising prices of first half of the quarter. Looking forward to the fourth quarter, we expect the same fundamental factors to remain in place. However, just like with volume, our margins are often seasonally lower when compared to the third quarter. Even with some variability quarter-to-quarter, as we have said many times, when you look at our business over a full year period, we continue to deliver strong and growing results. ”

Adjusted EBITDA dropped -7% to $257 million from $276 million a year earlier. Adjusted distributable cash flow ((DCF)) slipped nearly -8% to $181 million. The company paid out a distribution of 84.2 cents, good for a coverage ratio of nearly 2x. Its trailing 12-month coverage ratio was 1.9x.

Turning to the balance sheet, SUN ended the quarter with $3.8 billion in debt and $256 million in cash and equivalents. Leverage was 3.9x.

Looking ahead, the company raised its full-year adjusted EBITDA outlook. It now expects adjusted EBITDA to be above $935 million. At the start of the year, the SUN originally projected EBITDA of between $850-900 million for 2023 and then raised it to between $865-915 million after its acquisition of Zenith, which brought with it 16 refined product terminals.

For Q4, the company is expecting to see a normal seasonal slowdown in volumes, as well as seasonally lower margins.

Discussing the current environment on its earnings call, CEO Joseph Kim said:

“ On a macro level, fuel distribution has remained highly attractive within the energy sector. The combination of higher breakeven margins and commodity volatility has supported strong earnings for select companies that can optimize gross profit and manage expenses. Obviously, this is what Sunoco does well. In addition, our growth in the terminal business has enhanced our overall portfolio, providing further stability and growth opportunities. … I'd like to preview a few key themes. We expect to grow and have another strong year in 2024. We expect industry fundamentals to remain supportive, and we expect the continuation of our proven track record of optimizing our business in various macro environments. Regardless of one's outlook on fuel demand, inflation recession risk and geopolitical uncertainty, we expect our stable portfolio to deliver strong results in various environments. With our increasing cash flow, we expect to grow both organically and through acquisition, the opportunity set remains ample and attractive. And finally, we're in a position to increase our distribution again next year. All of this while maintaining strong coverage and leverage ratios. ”

SUN reported solid Q3 results and nicely increased its full-year guidance by a meaningful amount. Margin and volume are typically in a seesaw type of relationship for fuel distribution companies, where higher margins lead to lower volumes and vice versa. However, SUN has been able to both be pretty robust this year, as the overall demand market has been flattish to down, supporting margins, and SUN has been able to grow volumes both organically and through acquisitions.

Acquisitions will likely continue to be a driver for the company moving forward. The company said it sees robust opportunities in both the fuel distribution and midstream space, and as one of the largest operators in the space, and backed by parent Energy Transfer ( ET ), it has both the financing and scale to be the natural consolidator in the space.

Valuation

SUN trades at 9.0x the 2023 EBITDA consensus of $942 million. Based on the 2024 EBITDA consensus of $930.4 million, it is valued at 9.1x.

The stock has an attractive free cash flow yield of about 11% based on my 2023 projections calling for just over $500 million in FCF.

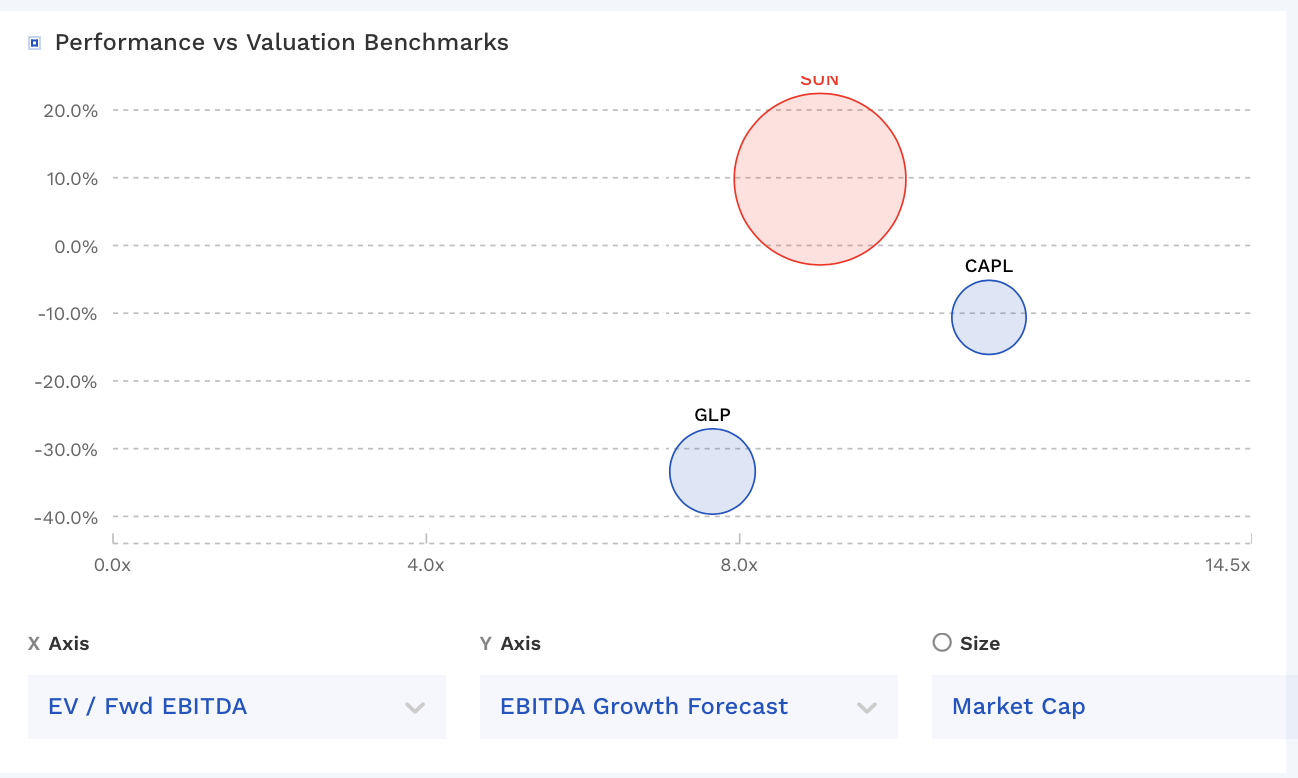

SUN trades between CrossAmerica ( CAPL ) and Global Partners ( GLP ), but analysts are expecting stronger growth for it, due to its ability to execute growth projects and make accretive acquisitions. I think fair value is right around current levels, and that a 9x EBITDA multiple is appropriate for the name given that is where most midstream companies currently trade.

{kind=link}

SUN Valuation Vs Peers (FinBox)

Conclusion

SUN has had strong year operationally so far, with solid margins and volumes. Now margins and volumes will both ultimately fluctuate, but they often do tend to balance each other out somewhat. At the same time, the company is growing its business both organically and through bolt-on acquisitions. The stock currently yields over 6% and I’d expect a distribution increase next year given its robust coverage ratio.

Overall, SUN’s stock looks close to fairly valued in my view, trading in between its two closest peers as well as in a similar range to many midstream stocks. If the economy weakens, the company could certainly see volumes take a hit, although I’d expect another accretive acquisition next year. I also continue to not be a fan of its IDRs.

I’ve owned SUN for a long time, but I would not be a new money buyer at current levels. I continue to rate the stock a “Hold.”

For further details see:

Sunoco Q3: Operational Performance Has Been Strong, But Stock Looks Fairly Valued