ET - Sunoco: Steady Q3 Results With Shares At Fair Value

2023-11-01 11:37:55 ET

Summary

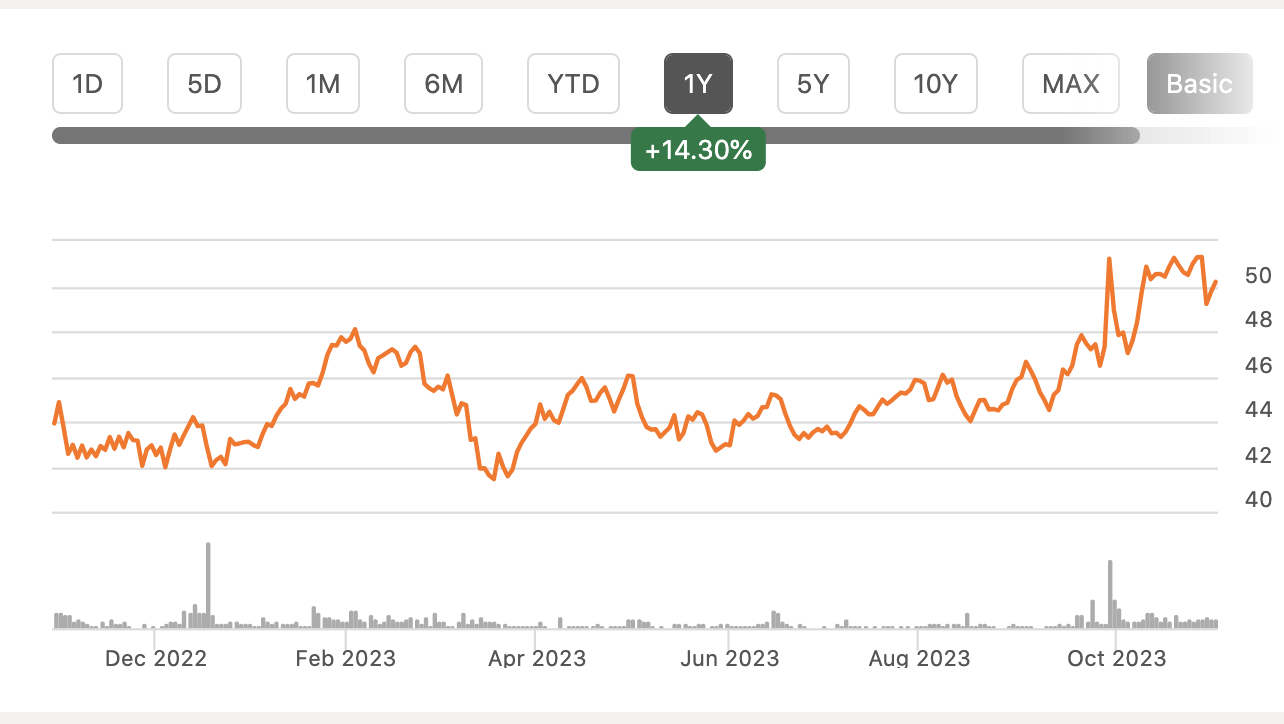

- Sunoco LP's stock has performed well over the past year, rising nearly 15% and responding positively to Q3 earnings.

- The company generates steady distributable cash flow and has healthy distribution coverage.

- However, Sunoco has limited growth prospects, making it a hold for income-oriented investors.

Shares of Sunoco LP ( SUN ) have been a solid performer over the past year, rising nearly 15%, and the stock responded positively to its Q3 earnings, rising about 1.5% in response. The company generates very steady distributable cash flow and has healthy distribution coverage. Against this, it has limited growth prospects. Following its rally, I view shares as broadly at fair value, making it a hold for income-oriented investors.

{kind=link}

In the company’s third quarter , Sunoco earned $2.95 in GAAP EPS from $0.75 last year. However, this is not indicative of underlying operating results. Sunoco revalues inventory to market, which can cause accounting fluctuations without shifting cash flow. There was a $141 million benefit this quarter vs a $40 million drag last year. That drove essentially all of the EPS variance. Revenue of $6.32 billion fell 4% from last year due to lower commodity prices.

Sunoco distributes about 8 billion gallons of fuels per year across its 7,400 dealer and distributor network. It also has 42 refined product terminals with the capacity to store 20 million barrels. While it owns gas stations in New Jersey and Hawaii, it primarily acts as just a distributor. It earns a profit by collecting a spread on what it pays for gasoline and diesel and what it sells it for. As a consequence, while revenue moves significantly with gas prices, its EBITDA and cash flow is relatively immune to commodity prices.

This is evidenced by the fact that fuel sales were down by $270 million from last year. Excluding inventory adjustments, cost of fuel sales fell by $288 million, essentially moving in lockstep. During the quarter, its fuel sales rose 7% to 2.1 billion gallons. The spread it earns on fuel declined to 13 from 13.9 cents last year. Last year, diesel margins in particular were quite strong as that market became very tight in the wake of Russian sanctions. While the diesel market is still quite tight, it has normalized to some degree, lessening margins.

Due to that 0.9 cent decline in fuel margins, adjusted EBITDA of $257 million was down from $276 million last year. Fuel EBITDA was $226 million from $250 million last year. Other EBITDA (primarily rent of gas station real estate it owns) rose to $31 million from $26 million. Alongside lower EBITDA, its distributable cash flow ((DCF)) declined to $181 million from $196 million. This is the key metric for income-seeking investors. DCF is operating cash flow less maintenance (but not growth) cap-ex, which can in turn be paid out to partners via distributions. During the quarter, SUN spent $45 million on cap-ex. $31 million on growth projects and $14 million on maintenance.

With its $0.842 distribution, SUN pays out $90 million in distributions; $71 million to SUN holders and $19 million to Energy Transfer ( ET ), its general partner. That still leaves $91 million of excess distribution, more than covering growth cap-ex. That remaining $60 million provides ability to pay down debt and potentially gradually increase the dividend. Coverage ran at 2x in the quarter.

Now, I would note that cash flow is somewhat seasonal as there is the “summer driving season” as people take vacations and road trips in July and August. As a consequence, Q3 can be stronger than average, meaning one would expect SUN to have a higher coverage ratio in this quarter, all else equal. Still, it has generated $516 million in year-to-date distributable cash flow for about 1.91x coverage. For the full year, it should generate about $680-690 million in distributable cash flow for about 1.89x coverage. SUN targets a minimum distribution coverage of 1.4x, so SUN is running with ample cushion even beyond this level.

With the $320 million of excess cash, SUN is able to fully fund its growth spending. Now, SUN is not engaged in massive growth cap-ex; these are primarily incremental projects, providing a modest boost to its long-term growth profile. With a $150 million growth cap-ex budget, it is only growing its total asset base about 2% per year. SUN is able to fund these growth projects entirely out of retained cash flow, which I view as a positive in today’s interest rate environment.

Higher rates can erode the economics and feasibility of some projects, which investors in NextEra Energy Partners ( NEP ) have realized, forcing companies to trim growth ambitions. When borrowing at 7-8%, the hurdle rate to generate a positive return on investment for equity holders is much higher than when borrowing at 4%. Because SUN is spending just out of its own cash flow, it does not have these same pressures.

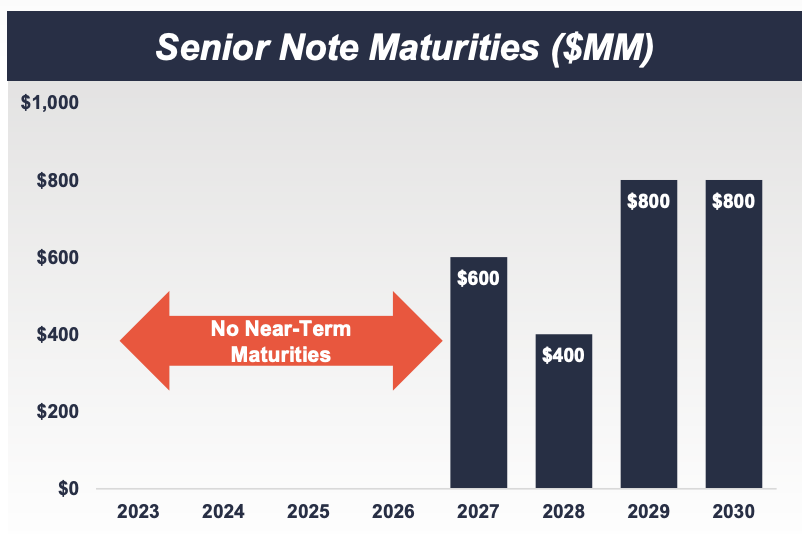

SUN has also been retaining cash beyond its growth cap-ex needs to bring down financial leverage and make its capital structure less dependent on debt financing. This is a positive insofar as helps to insulate the partnership better to some extent from higher rates. Debt to EBITDA has declined from 4.6x in 2019 to 3.9x today. In a higher rate environment, an optimal capital structure has less debt, all else equal. SUN began this de-leveraging journey ahead of the rise in rates but it has proven prudent. SUN also does not have near-term bond maturities, reducing its refinancing needs in this period of higher rates. By the time it has to roll over these bonds, rates could be lower again.

{kind=link}

With leverage below 4x, its balance sheet is now on a solid footing. This strategy of retaining capital rather than returning it all to partners works in limited partners’ interest. Because its quarterly distribution is at $0.842, any further increase is split 50/50 with the General Partner. Every dollar that is retained for cap-ex spending or debt reduction remains 100% within the limited partnership, but every new dollar it distributes has $0.50 of leakage away from limited partners to ET.

{kind=link}

After growth cap-ex, SUN has about $170 million of retained cash, if it chose to distribute all of that, it could raise its annual distribution level by about $1 (or $0.25/quarter), costing $85 million as it would also spend $85 million on distributions to ET. All else equal, investors will likely be better off in the long-run with SUN using that cash on continued balance sheet improvement or targeted growth projects, or even by buying back limited partner units.

Because it is in the highest IDR bracket, this is the strategy SUN has undertaken, only modestly growing its distribution, such as this year’s $0.01 increase . While the general partner is only getting about 20% of current distributions, it will be getting 50% of future ones, making increased distribution growth more burdensome.

Still with coverage at 1.9x, and with strong retained cash flow even after growth cap-ex, we can say that the current distribution is extremely safe and very well covered. As it collects a spread rather than having direct commodity exposure, its cash flow is fairly stable, but underlying growth is low single-digits given modest cap-ex spending. With leverage below 4x, we may see a modest acceleration in distribution growth, but I expect it to remain below 5% and more likely in the 1-3% range over the next several years.

Sunoco LP currently yields about 6.7%, which provides attractive and importantly secure income to investors. With this income rising 1-3%, medium-term potential is about 8%. I view that as fair value for a steady but slow growth company/partnership like Sunoco. Given the recent rally, SUN has converged to fair value. As such, I do not expect significant further capital appreciation potential, but for investors seeking stable income, SUN remains a suitable holding.

For further details see:

Sunoco: Steady Q3 Results With Shares At Fair Value