CA - SunOpta: Transformation Efforts Could Yield Results But Prospects Appear Baked In

2023-12-23 03:34:01 ET

Summary

- 9M 2023 revenues up 4% YoY, margins flat.

- SunOpta's transformation initiatives could drive medium-term growth and profitability however competitive and execution risks are significant.

- Valuation appears fair.

SunOpta's (STKL) transformation initiatives appear to be a step in the right direction and could positively support growth and profitability. Prospects appear baked into the stock.

Company Overview

SunOpta is a Canadian manufacturer of plant-based beverages and creamers, protein shakes, teas, and broths, as well as fruit snacks, and smoothie bowls for private label and national brands sold through retail and food service channels. SunOpta also produces products under their own brands including SOWN® (oat creamer), Dream® (plant milks including rice milk, coconut milk, almond milk, soymilk for retail and foodservice customers) and West Life™ (soymilk).

9M 2023 Performance

For the nine months ended September 2023, SunOpta's revenues increased 4% YoY to $448.7 million driven by pricing actions and volume growth, slightly offset by lower external sales of plant-based ingredients due to a customer transferring part of their business to a second-source supplier.

Gross margin amounted to 14% for the nine months of 2023 (17% after adjusting for a one-off increase in startup costs related to capital expansion projects). Operating margin amounted to under 1% for 9M 2023 (4% adjusted).

SunOpta Q3 2023, 10-Q

Looking ahead, the company is exploring a number of opportunities to drive growth, notably increasing acquiring new customers, TAM expansion (through new markets in the beverage space such as protein shakes), and market share gains with existing customers. Management is upbeat about the company's near term outlook with revenue growth expectations in the high single digit to double digit range for 2024. Medium term, management projects SunOpta's revenue potential at over $1.5 billion over the next 5-7 years, much of it in the plant-based business which in management's view could potentially grow into a billion dollar business, doubling from that generated in FY2022 (SunOpta generated revenues of $934 million in FY2022 of which plant based food and beverages generated $557 million, while fruit based foods and beverages, which includes their recently disposed frozen fruit business, generated the remainder). The recent opening of SunOpta's $125 million plant-based beverage facility in Texas "significantly expands" their production capacity, enabling them to meet this revenue target. Research reports project plant based beverage sales to grow in the double digits over the coming years in the U.S. where SunOpta generated most of its revenues.

SunOpta Q3 2023 Investor Presentation

Profitability could benefit from a number of strategic efforts as well. Following the disposal of their sunflower business last year and their lower-margin frozen fruit business this year, SunOpta is now a single segment company focused largely the plant-based space which is not only a fast-growing sector but has typically been a higher margin business as well (segment margins for SunOpta's fruit based food and beverage business have hovered in the low single digits or below break even over the past few years while plant based food and beverage segment margins are around the mid single digits). Share gains and capacity expansion in the plant-based space could potentially further improve margins through scale economies, while their switch from commodity manufacturing to value added manufacturing (through their growing portfolio of owned brands in plant foods and beverages) could be margin accretive as well. Management noted in their Q2 2023 earnings call that the company has transformed their portfolio from 70-30 commodity/value add to 30-70 and they remain committed to continued transformation. Management expects gross margins to improve to 20% going forward. Additionally, continued deleveraging could ease interest costs which due to rising interest rates have more than doubled in 9M 2023 compared to the same period last year, benefiting net margins.

SunOpta Q3 2023, 10-Q

About $75 million of the $141 million sales proceeds from the sale of their frozen fruit business in October 2023 was used to pay down debt which post-payment stood at over $240 million and leverage at 3.2x at the end of October 2023. Management made clear in their Q3 2023 earnings call that they intend on reducing leverage to a manageable sub-3x level by next year, partly using free cash flows (levered) which are expected to be around $35 million to $45 million in 2024.

SunOpta Q3 2023, 10-Q

Risks

Execution and competitive risks

The plant based space is saturated and highly competitive and SunOpta is up against bigger players like Silk (from Danone) ( OTCQX:DANOY ) and Nestle ( OTCPK:NSRGY ) who have financial and scale advantages against SunOpta. SunOpta management foresees intensifying competition and heightened promotion activity in 2024 , and competitive pressures may intensify longer term.

Moreover, SunOpta's focus on its own brands competes with their private label and co-manufacturing customers (who include players like Walmart ( WMT ) and Nestle), who may in turn shift their business to competing suppliers without an own brand portfolio. SunOpta's customers are quite concentrated with over 70% of revenues generated from their top 10 customers leaving them quite vulnerable to earnings volatility which may hinder growth projections, profitability, free cash flow generation, deleveraging targets and therefore potentially increasing solvency risks.

Conclusion

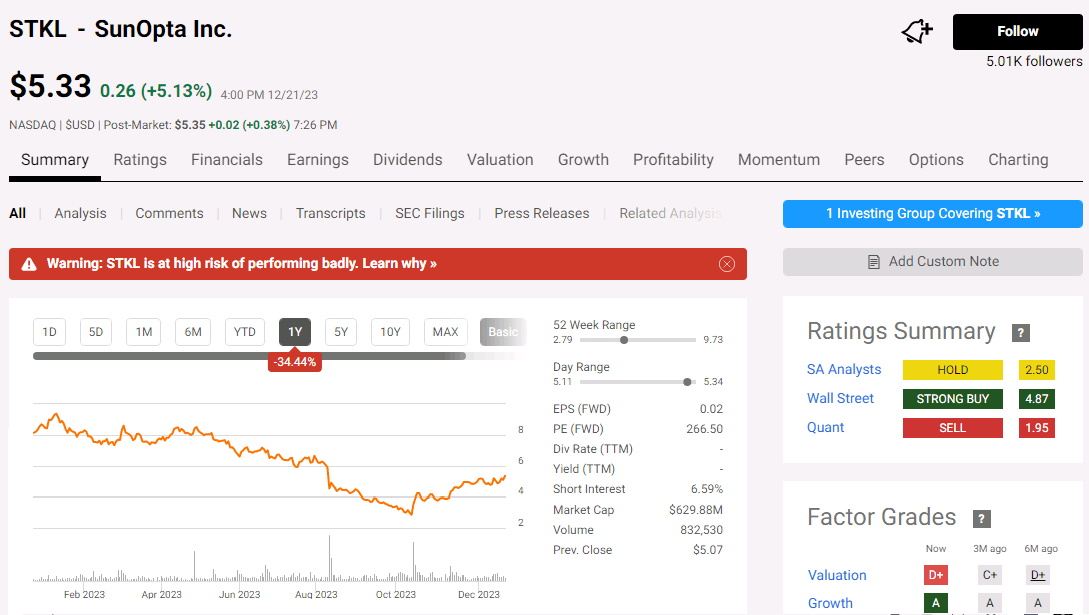

SunOpta has a 'Strong Buy' analyst consensus rating. Seeking Alpha's Quant system rates it a 'Sell'.

{kind=link}

Taking the following assumptions based on management's projections suggests SunOpta is worth under $700 million, suggesting a high single digit upside from their current market capitalization of around $630 million, however this scenario assumes the company successfully reaches a 16% growth rate annually which appears aggressive, may not materialize given competitive pressures in the plant-based space, and offers little margin for error for an investor. A more moderate growth assumption of 12% suggests the company is worth under $600 million.

| Revenue growth YoY % |

| 16% over the next seven years based on management's $1.5 billion goal in 5-7 years, which translates into an annual growth rate of around 16% annually over a seven-year period starting in 2023 when revenues are projected at around $600 million |

| Terminal growth rate % |

| 2% |

| Net margin % |

| 5% in 2024 (being their first full year as a mostly plant-based business) gradually improving to 7% due to scale economies, and an increasing share of value added manufacturing. For perspective, Nestle's powdered and liquid beverages segment has a segment margin of 20% |

| Depreciation % |

| 4% of revenues |

| CAPEX % |

| 4.5% of revenues annually maintenance CAPEX plus an assumed additional $100 million investment in capacity expansion in year 4 |

| Discount rate % |

| 10% |

For further details see:

SunOpta: Transformation Efforts Could Yield Results But Prospects Appear Baked In