CA - Superior Plus: Solid Start To 2023 - Warming Up To The Story

2023-06-21 09:21:09 ET

Summary

- Superior Plus reports solid Q1/23 results with record-high adj. EBITDA of $272 million, prompting an increase in 2023 annual adj. EBITDA guidance.

- The recent Certarus acquisition proves to be a success, with Q1/23 adj. EBITDA of $63 million, leading to an upward revision of full-year guidance.

- Despite positive results, Superior Plus' shares are fully valued at 8.0x pro-forma Fwd EV/EBITDA, with a stretched balance sheet.

- I recommend investors wait for a better buying opportunity.

A few months ago, I wrote a cautious update on Superior Plus ( SPB:CA ), warning that despite a transformative acquisition, SPB's shares are still expensive. Since my article, Superior Plus' stock price has declined by 12%, suggesting other investors agree with my assessment of the company (Figure 1).

Figure 1 - SPB has declined 12% since my last update (Seeking Alpha)

Recently, Superior Plus released its Q1/23 earnings report, the first under new CEO Allan MacDonald. Were the Q1 results any good and have the company's prospects improved enough to warrant another look?

(Author's note, all figures in this article are quoted in Canadian dollars unless otherwise specified)

Brief Company Background

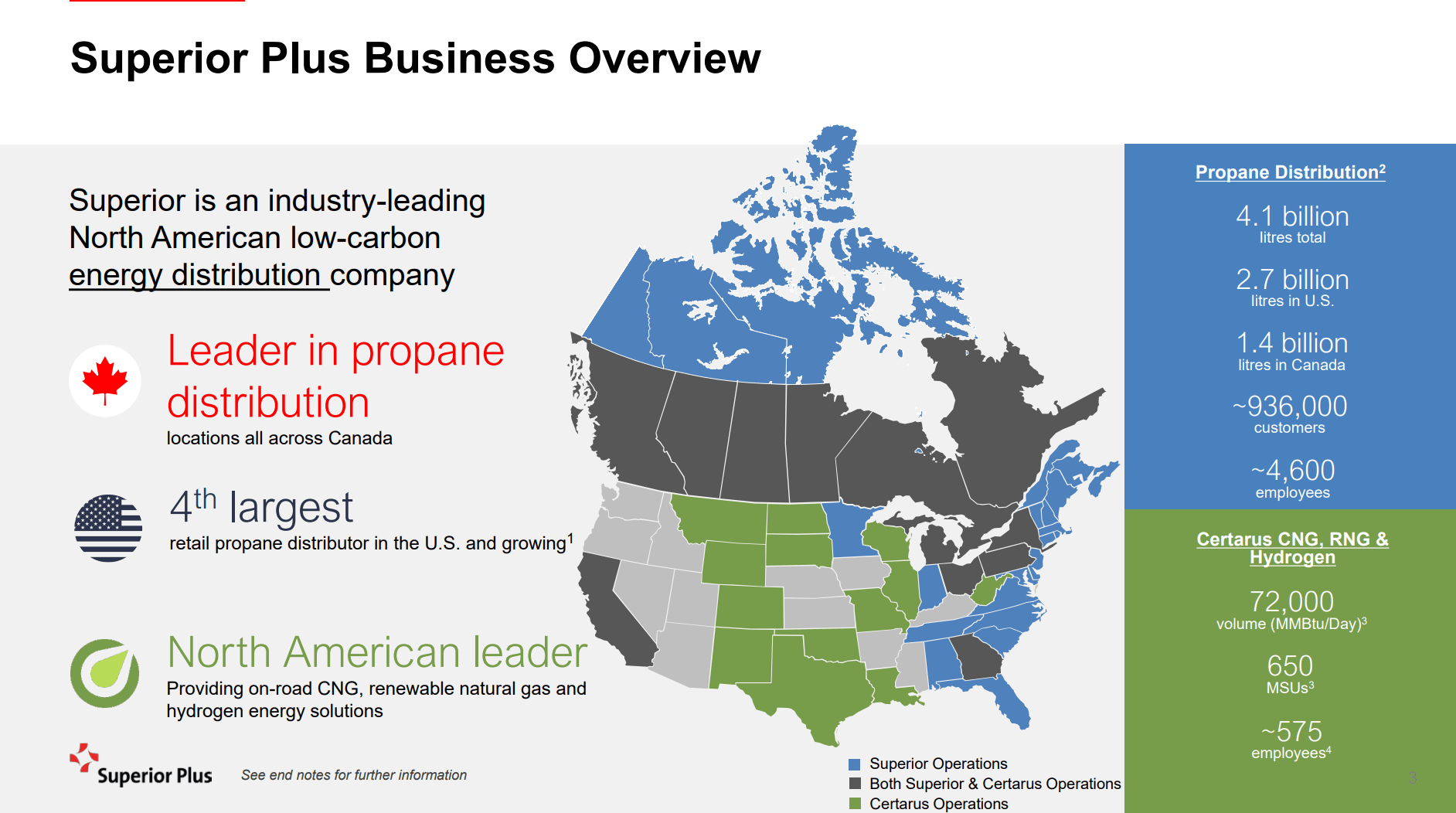

Superior Plus is a leading propane fuel distributor in North America, ranking # 1 in Canadian propane distribution and #4 by market share in the U.S., primarily on the U.S. East Coast (Figure 2).

{kind=link}

Figure 2 - Superior Plus overview (Company investor presentation)

Since the acquisition of Certarus (acquisition closed May 31st), approximately 45% of the company's EBITDA is derived from the U.S. propane distribution business, 21% from Canadian propane distribution, 10% from wholesale propane distribution, and 24% from the newly acquired CNG/RNG/Hydrogen distribution business (Figure 3).

{kind=link}

Figure 3 - SPB Financial overview (Company investor presentation)

Solid Start To 2023

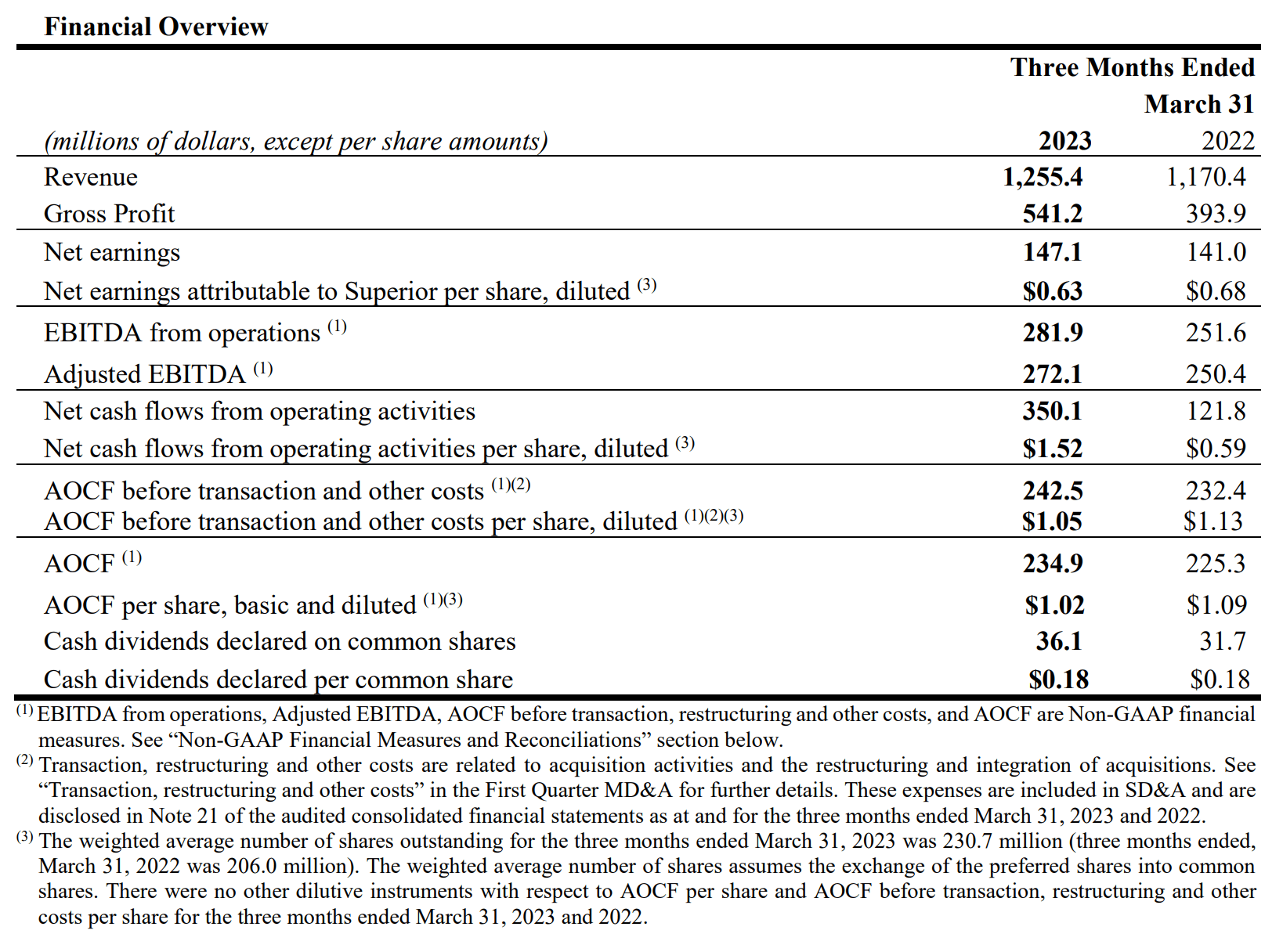

For Q1/23, Superior Plus recorded $1.26 billion in revenues and $272 million in adj. EBITDA, with adj. EBITDA being a record high for the company (Figure 4).

{kind=link}

Figure 4 - SPB Q1/23 financial summary (SPB Q1/23 financial report)

Importantly, Superior Plus increased its 2023 annual adj. EBITDA guidance from $585 - 635 million in February to $620 - 660 million based on strong performance from the newly acquired Certarus business.

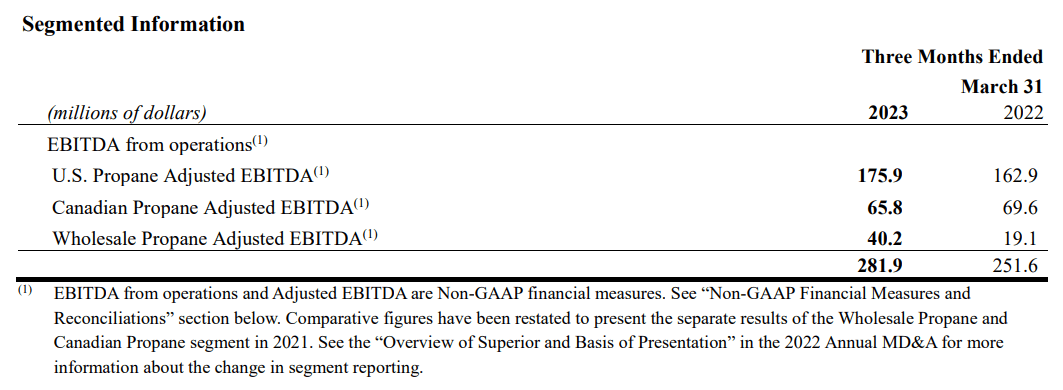

Operations-wise, the existing businesses mostly did well, as the U.S. Propane distribution business delivered $176 million in EBITDA, an 8.0% YoY increase, on the back of tuck-in acquisitions and higher margins from price increases partly offset by lower volumes. The U.S. business also benefited from a weaker Canadian dollar relative to the U.S. dollar (Figure 5).

Figure 5 - SPB Segmented EBITDA (SPB Q1/23 financial report)

{kind=link}

The Canadian Propane business saw a decline in EBITDA by 5.5% YoY to $66 million on the back of higher operating costs offset by higher gross profit. The prior year's quarter benefited from the Canadian government's COVID-related wage subsidies. Volumes were also lower in Canada due to warmer weather.

Finally, the Wholesale Propane business saw a doubling of EBITDA to $40 million from $19 million in the prior year primarily due to the acquisition of Kiva Energy Inc., a wholesale propane distributor in the U.S.

Positive First Look At Certarus

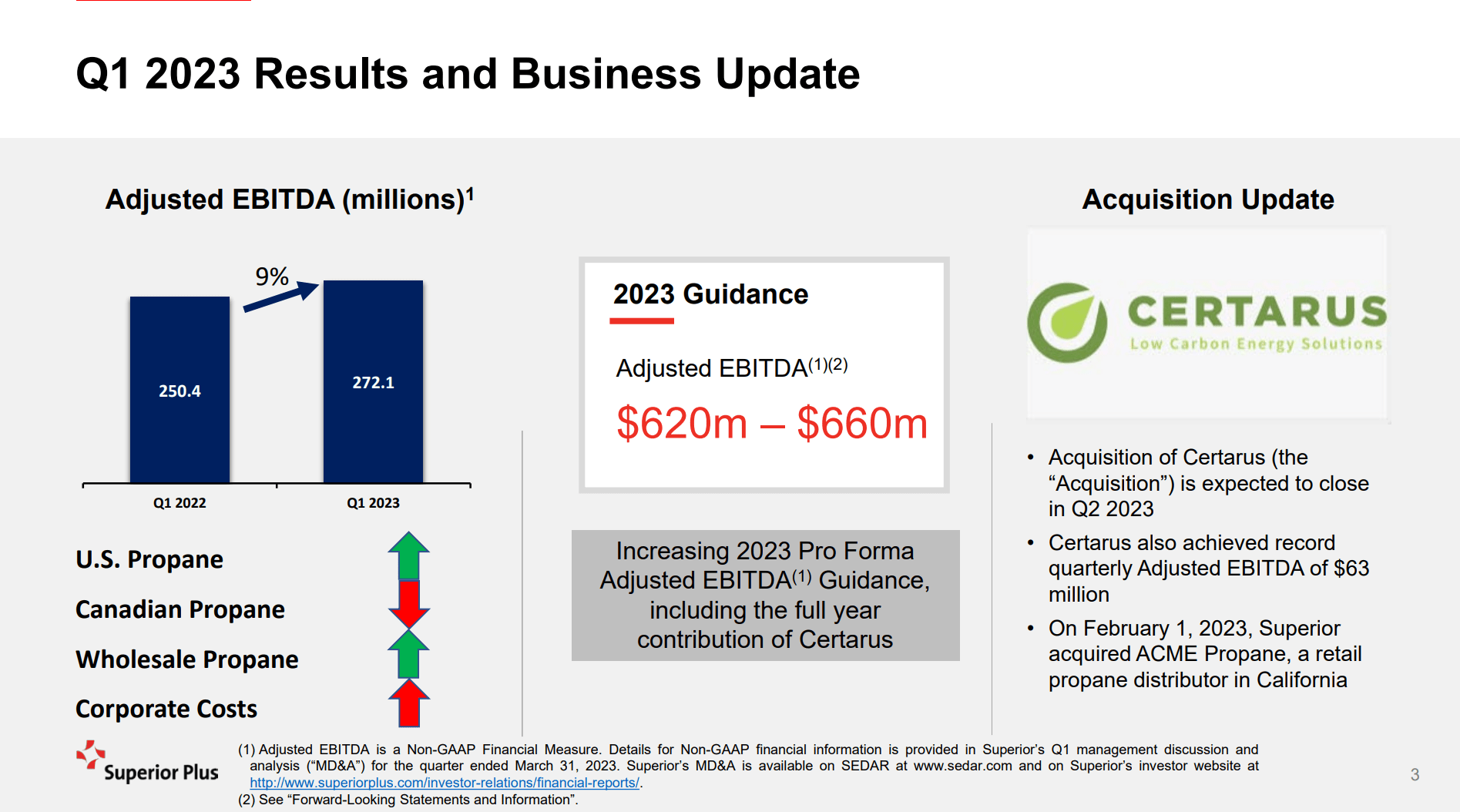

Back in February, Superior Plus was guiding to pro-forma annual adj. EBITDA of $140 - 150 million for Certarus, already a double digit increase to 2022 results. However, in Q1/23 alone, the Certarus business was able to achieve $63 million in adj. EBITDA (up 126% YoY), prompting an updated adj. EBITDA range of $175 - 185 million and the upward revision to Superior Plus' full year guidance (Figure 6).

Figure 6 - Q1/23 business update (Company investor presentation)

{kind=link}

As a reminder, Certarus is a leading distributor of low carbon fuels like compressed natural gas ("CNG"), renewable natural gas ("RNG"), and hydrogen, a fast growing market that SPB estimates to be worth $6-8 billion (Figure 7).

Figure 7 - Certarus business overview (Company investor presentation)

{kind=link}

The growth in adj. EBITDA at Certarus was driven by new contracts, improved pricing, lower production costs, and an increase in mobile storage units ("MSUs") deployed in the quarter, with average sales volumes of 72k MMBtu, a 17% YoY increase and average MSUs of 646, an 18% YoY increase.

Recall, SPB paid $1.05 billion in a combination of cash, shares, and assumption of debt for a business that generated $126 million in adj. EBITDA in 2022 or 8.5x trailing EV / EBITDA, in line with SPB's historical transaction multiples.

However, if we use the company's pro-forma adj. EBITDA guidance of $175 - 185 million ($180 million midpoint), then the Certarus transaction was completed at only 5.8x EV/EBITDA, a relative steal for a fast growing business like Certarus.

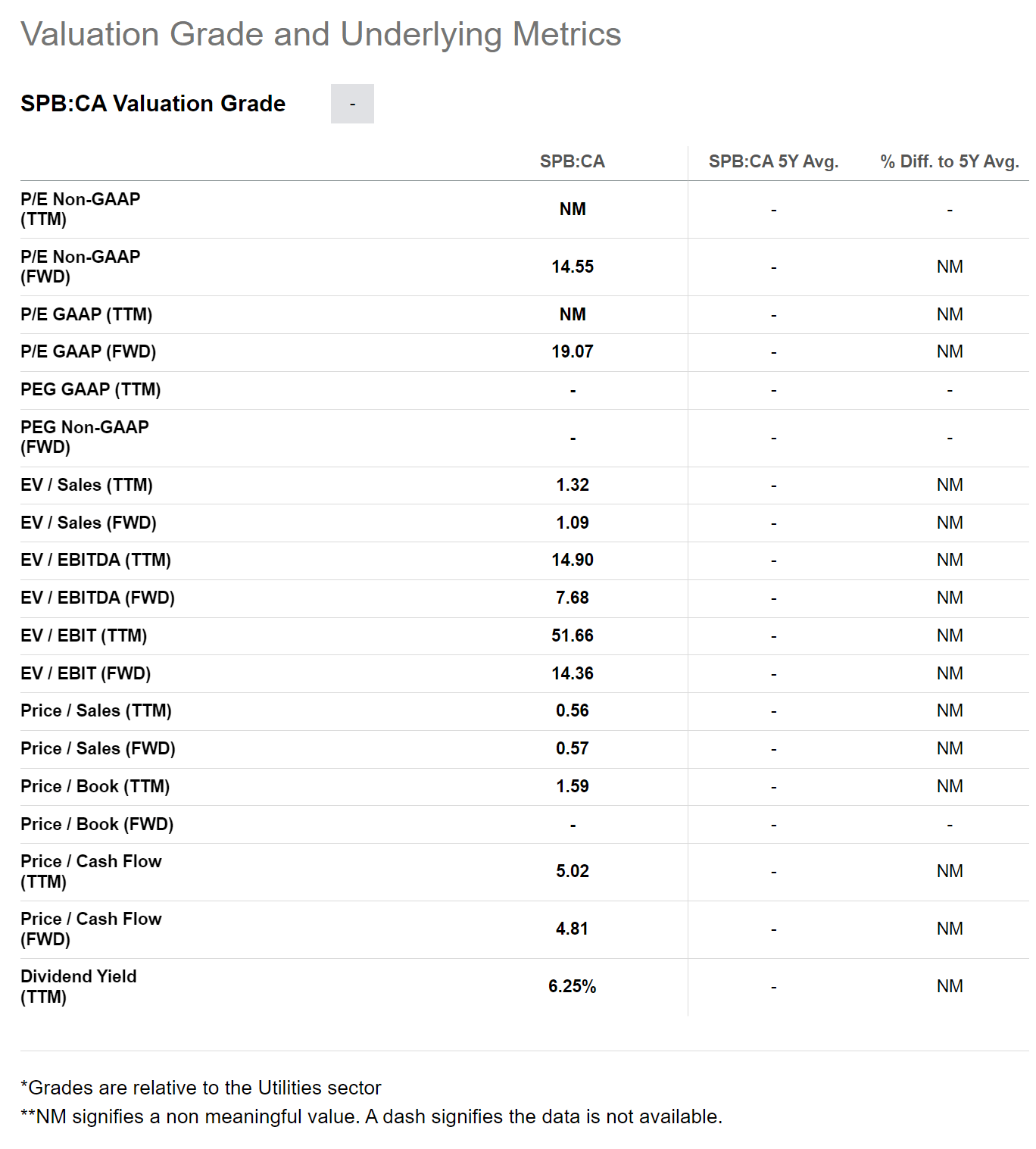

Valuation Improving But Still Not Cheap

With Superior Plus' positive start to 2023, I believe the company's valuation has improved significantly, as it is currently trading at 19.1x GAAP Fwd P/E and a reported Fwd EV/EBITDA multiple of 7.7x (Figure 8).

{kind=link}

Investors should note that SPB's valuation multiple remains understated on Seeking Alpha as its Enterprise Value is partly based on reported financials as of March 31, 2023, which does not include the assumed debt and cash payment for the Certarus transaction that closed on May 31, 2023 (Figure 9).

{kind=link}

Adjusting for ~$200 million in assumed debt plus the $353 million cash payment, I believe adj. Enterprise Value is actually $5.1 billion. Therefore, pro-forma EV/EBITDA is 8.0x (using management's midpoint guidance of $640 million).

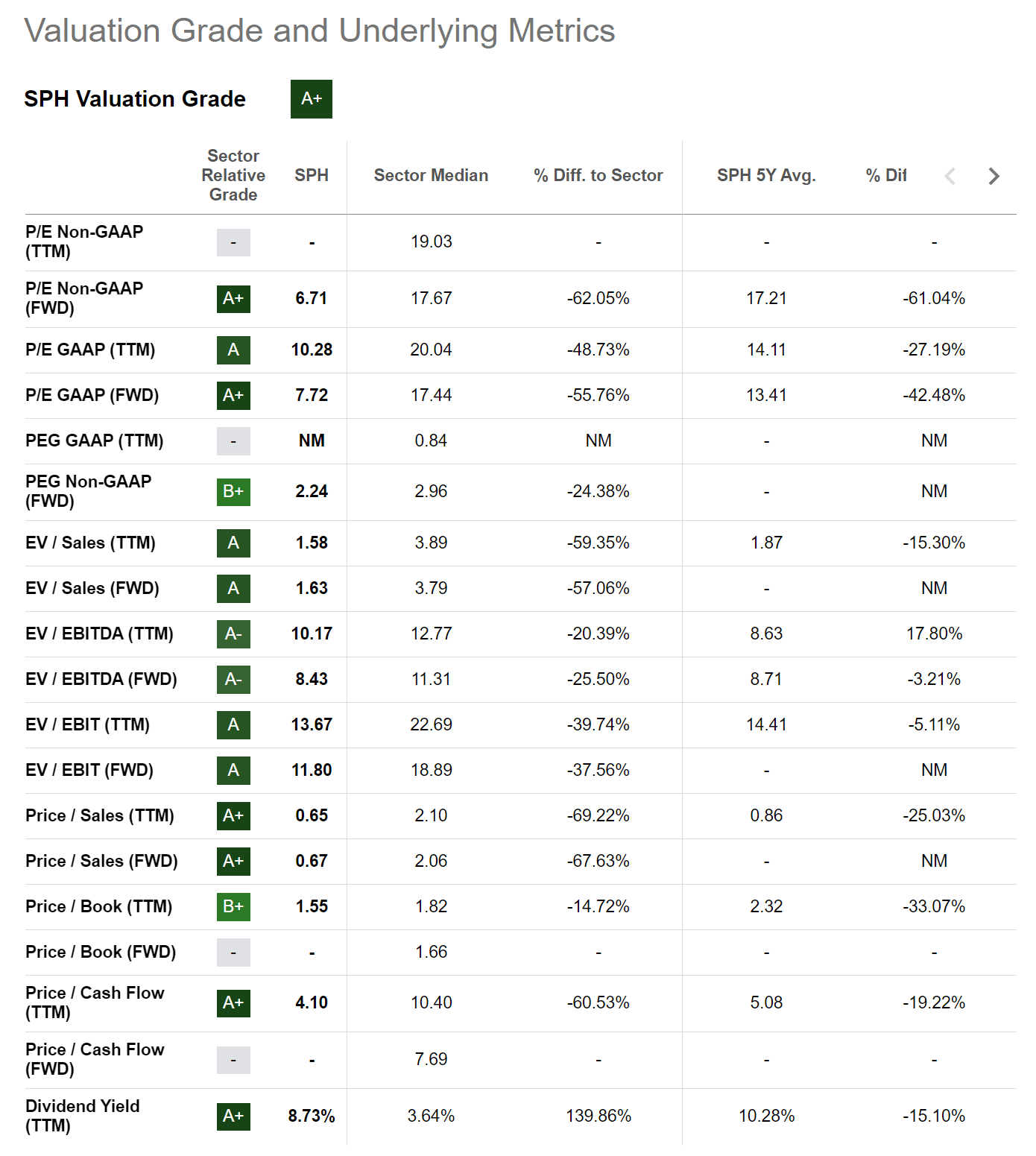

However, with a 12% decline in SPB's share price since March and an improvement in run-rate EBITDA, Superior Plus has closed the valuation gap against its closest competitor, Suburban Propane Partners ( SPH ), which currently trades at 8.4x Fwd EV/EBITDA (Figure 10).

Figure 10 - SPH is currently trading at 8.4x Fwd EV/EBITDA (Seeking Alpha)

{kind=link}

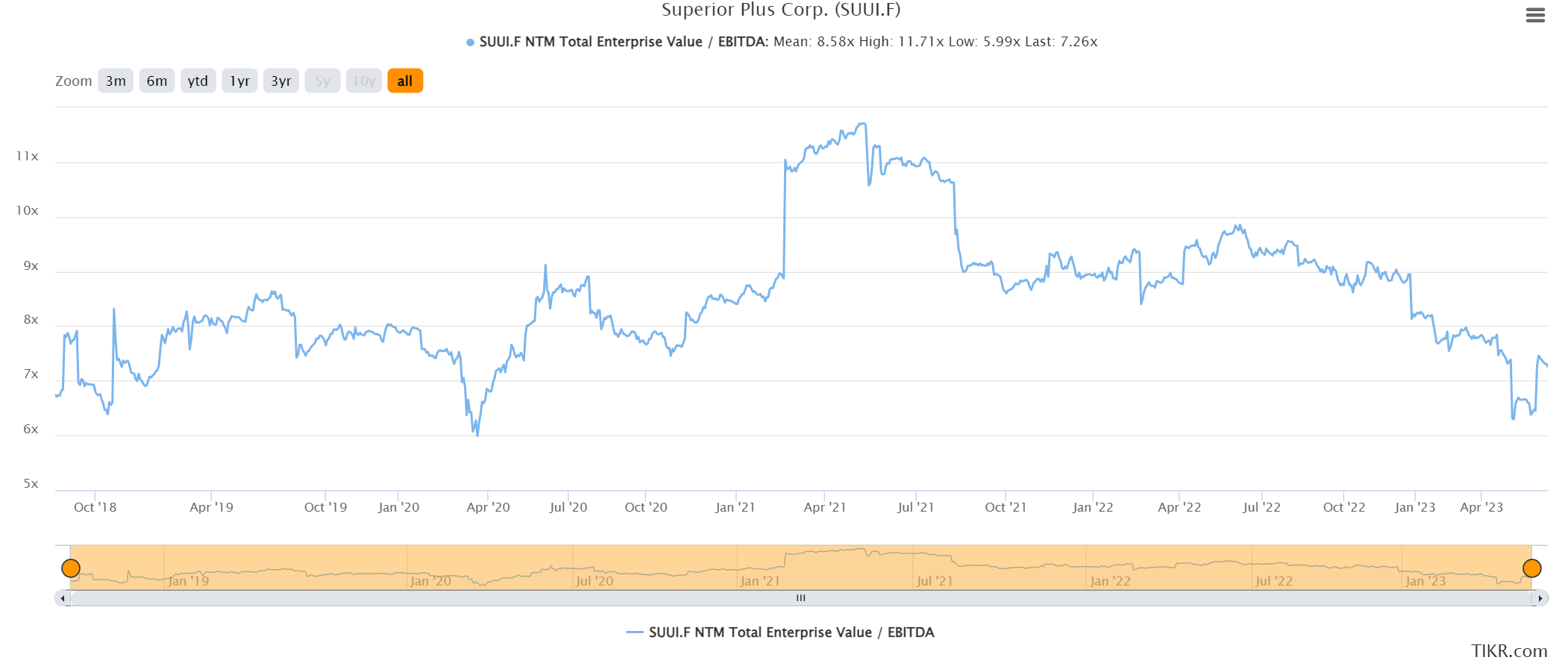

Historically, sub-7.0x Fwd EV/EBITDA have been good opportunities to buy shares of Superior Plus (Figure 11).

Figure 11 - Historical Fwd EV/EBITDA multiples on SPB (tikr.com)

{kind=link}

Attractive Dividend Should Be Well Funded

On a positive note, Superior Plus' $0.06 / month dividend (note, the company is switching to a quarterly $0.18 / share dividend beginning in June) should be well funded, as it only accounts for $45 million in quarterly cash payments vs. $640 million in adj. annual EBITDA. SPB's forward dividend yield is 7.5%.

Leverage Elevated But Manageable

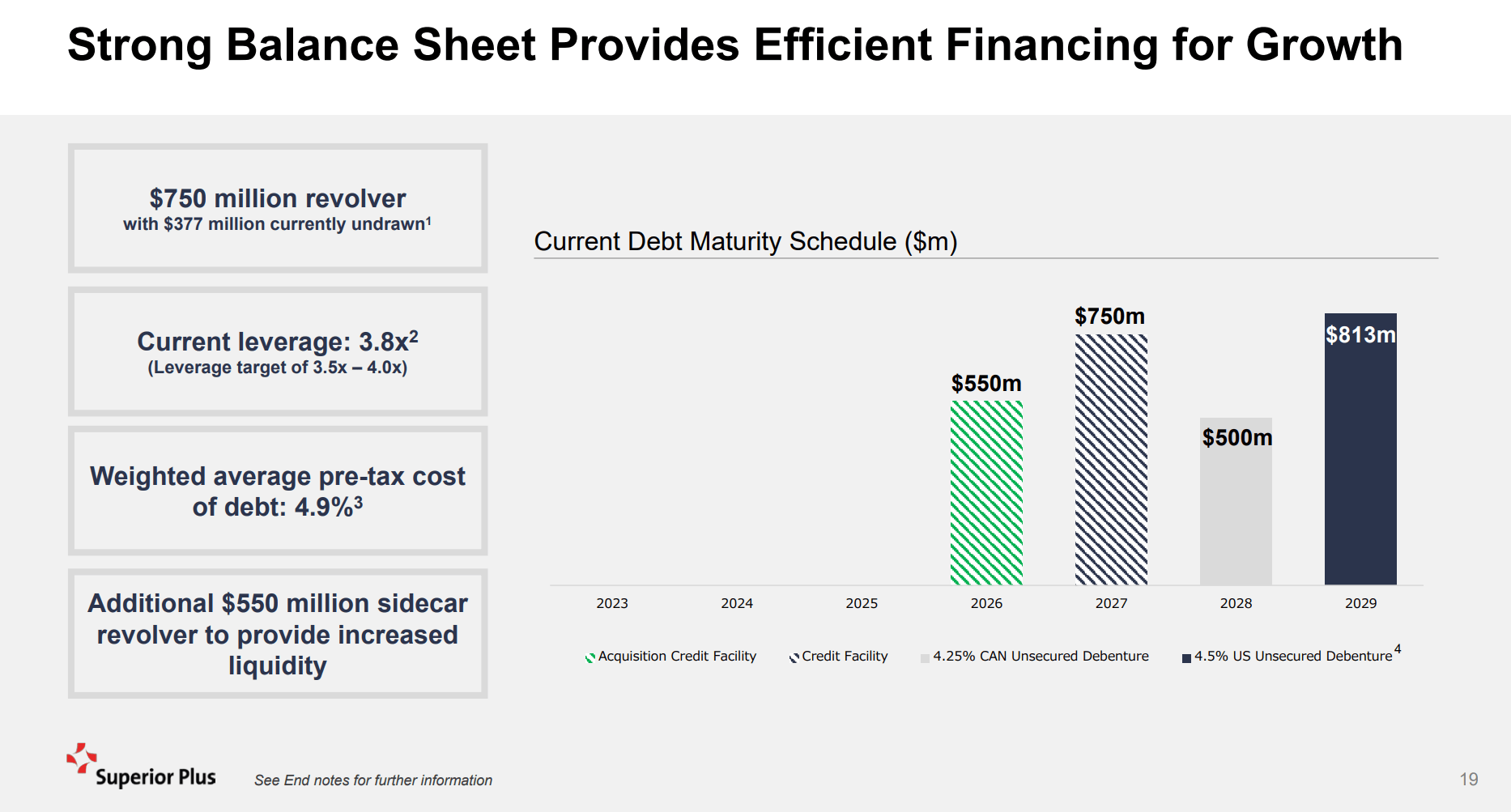

One concern I have with Superior Plus is the company's stretched balance sheet. Adjusting for the cash payments to complete the Certarus transaction plus the assumed debt, SPB currently has $2.4 billion in net debt outstanding or 3.8x leverage (Figure 12).

Figure 12 - SPB's balance sheet is stretched (Company investor presentation)

{kind=link}

However, Superior Plus does not have any near-term maturities and the weighted average cost of debt is relatively low at 4.9% pre-tax, so as long as the company is able to generate cash to service debt, Superior Plus' balance sheet should be manageable.

Additional Risks With Superior Plus

In addition to the stretched balance sheet, another risk with respect to Superior Plus is that historically, the company has been very acquisitive, as it tries to consolidate the propane distribution market. While acquisitions may be one way to grow, there is also the risk that Superior Plus overpays. For example, within the propane distribution market, there is a good counter-example, Ferrellgas ("FGP"). Ferrellgas grew quickly in the prior decade through debt-fueled acquisitions, becoming the #2 distributor in market share. However, the underlying businesses could not service the more than US$2.5 billion in debt that the company amassed and Ferrellgas was delisted from the NYSE in 2019.

Another longer-term risk to Superior Plus is that traditional propane distribution may be phased out as consumers and businesses look to low-carbon alternatives. To address this risk / opportunity, Superior made the Certarus acquisition as a launchpad into the low-carbon fuels distribution space.

Conclusion

Overall, I find Superior Plus' Q1 results to be a positive step in the right direction. The recently completed Certarus acquisition looks to be a winner, with adj. EBITDA exceeding expectations leading to an upgrade to the company's full year guidance.

However, trading at 8.0x pro-forma Fwd EV/EBITDA, SPB's shares are not particularly cheap. One upside to SPB is the company's dividend, currently at $0.18 / quarter, which annualizes to 7.5%.

I remain on the sidelines on SPB's shares, however, I am warming up to the company and may consider starting a position if valuation dips to sub-7.0x Fwd EV/EBITDA.

For further details see:

Superior Plus: Solid Start To 2023 - Warming Up To The Story