CA - Superior Plus: Transformative Acquisition But Still Expensive

2023-03-22 14:04:40 ET

Summary

- Superior Plus is the largest propane distributor in Canada and #4 in the U.S.

- Superior Plus has recently made a large acquisition in the nascent low-carbon fuels space. This brings forward management's guidance of $700-750 million in EBITDA by 2026.

- However, pro-forma the acquisition, I still find Superior Plus expensive relative to its U.S. peer, Suburban Propane.

- Furthermore, SPB has a stretched balance sheet and unattractive capital structure that makes me cautious.

About 6 months ago, I wrote a cautious article on Superior Plus ( SPB:CA ). I was concerned about the roll-up strategy being employed at Superior, as well as the company's heavy debt load. Furthermore, the company faces significant potential dilution from preferred shares sold to Brookfield.

Fast forward 6 months, have my views on Superior Plus changed?

(Author's note, all figures in this article are quoted in Canadian dollars unless otherwise specified)

Brief Company Overview

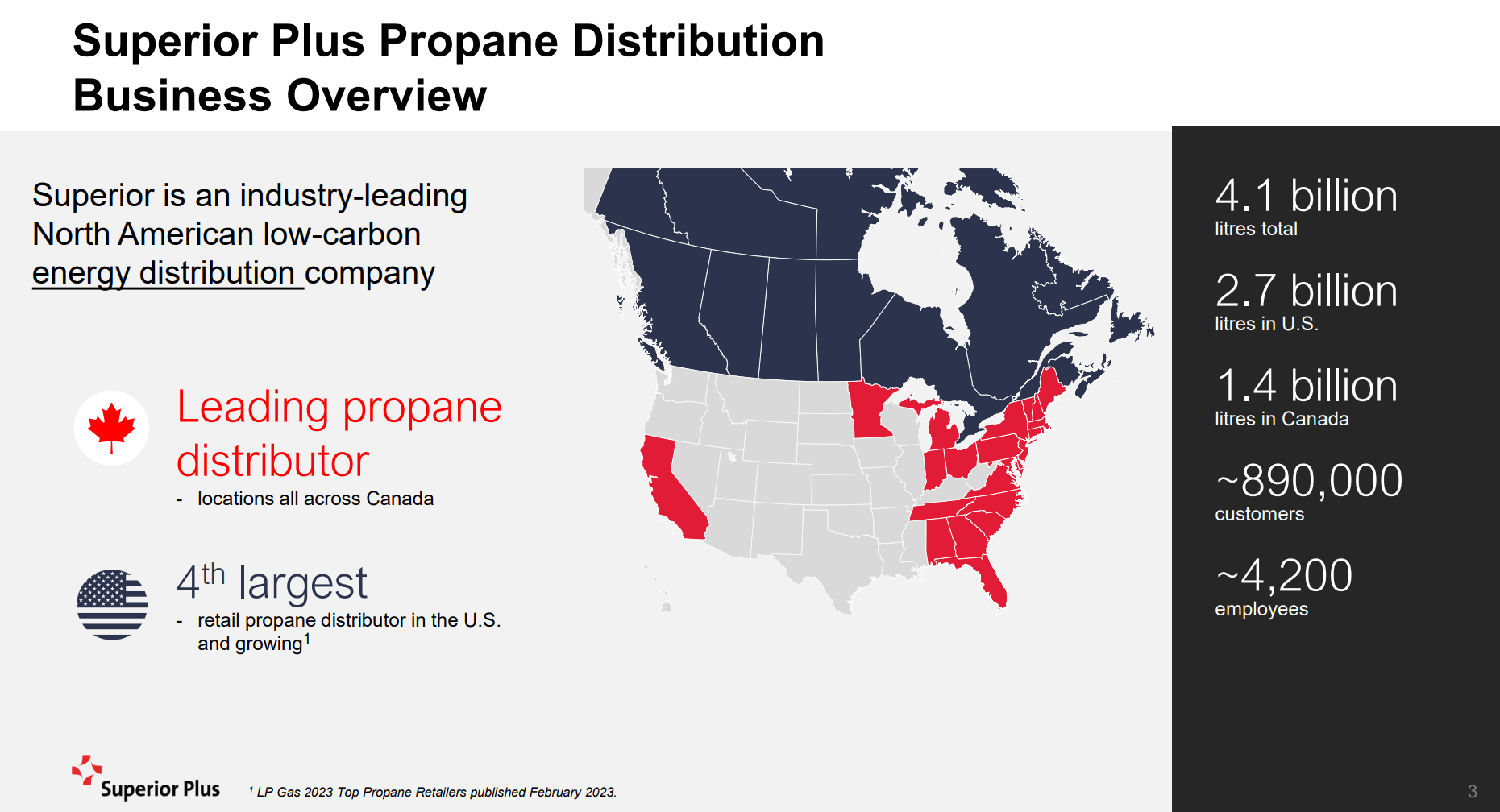

First, a brief overview of the company for readers who are unfamiliar with the company. Superior Plus is a leading propane fuel distributor in North America, with a #1 market share position in Canadian propane distribution and a #4 market share position in the U.S, primarily operating in the U.S. East Coast (Figure 1).

{kind=link}

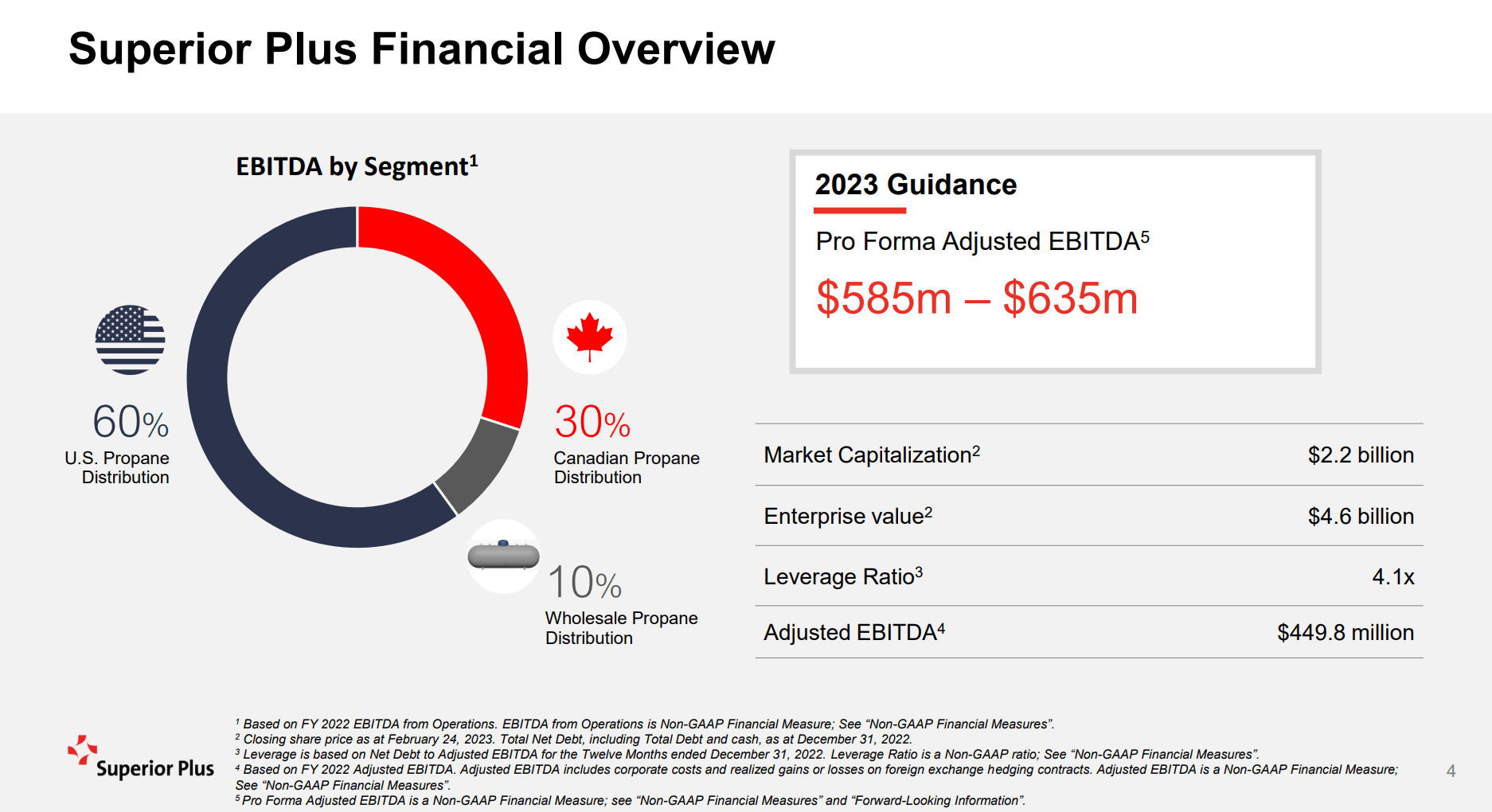

Approximately 60% of SPB's EBITDA is from its U.S. business and 40% is from its Canadian business. Pro-forma the recently announced $1.05 billion acquisition of Certarus Ltd., SPB is guiding to 2023 adjusted EBITDA of $585 - $635 million (Figure 2).

Figure 2 - SPB guiding to $585 to $635 million in 2023 EBITDA (SPB investor presentation)

{kind=link}

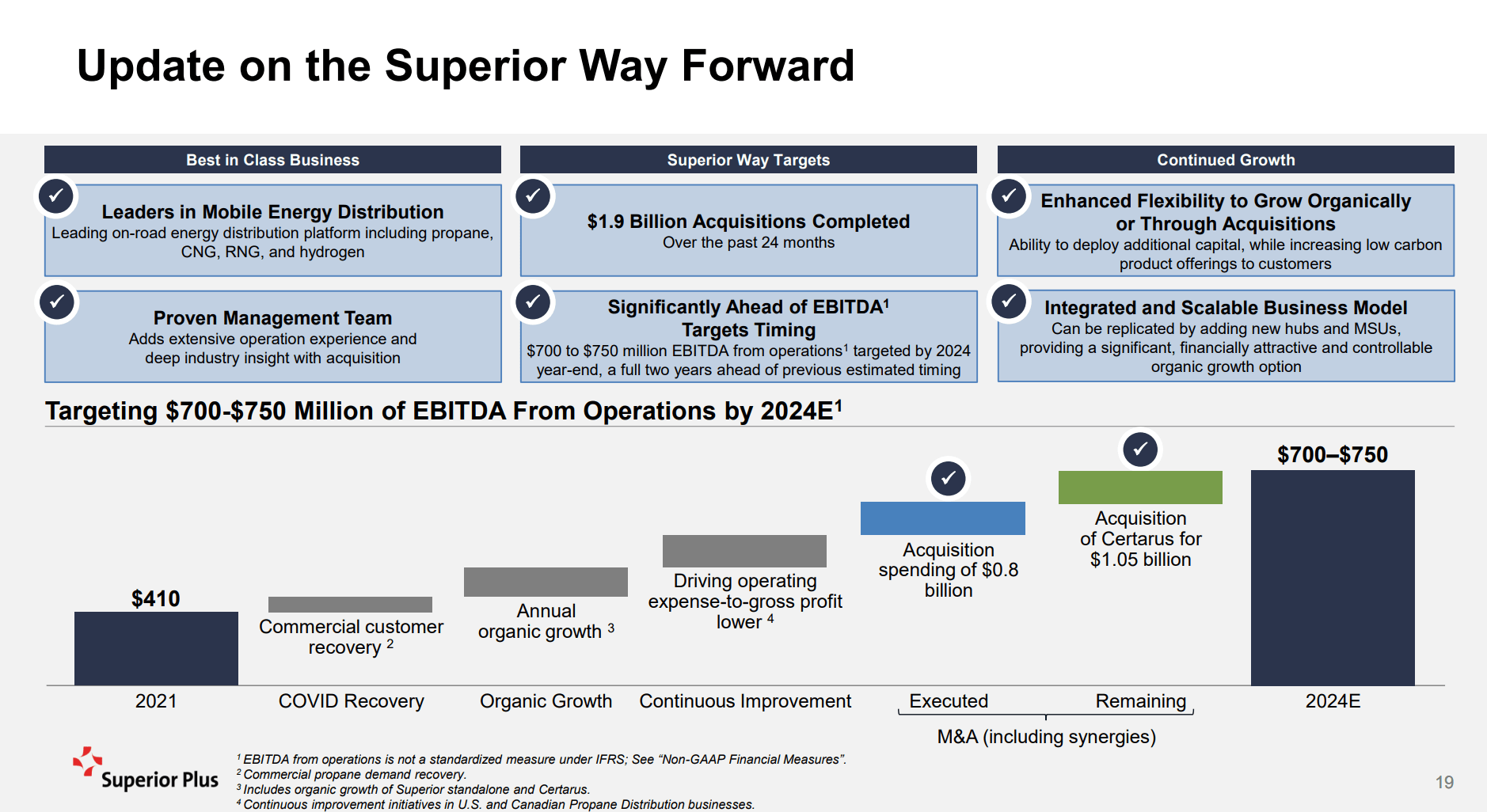

Since divesting its specialty chemicals business in 2021, Superior Plus has embarked on an ambitious growth strategy called 'Superior Way Forward' that calls for a 70-80% increase in EBITDA via organic growth and M&A transactions. So far, the company has spent $1.9 billion on acquisitions ($0.8 billion executed, $1.05 billion in process) (Figure 3).

Figure 3 - Superior Plus' Growth Strategy (SPB investor presentation)

{kind=link}

With the Certarus transaction, SPB has pulled forward its estimate of $700-$750 million in annualized EBITDA to fiscal 2024, from 2026 previously.

Certarus Is A Transformational Acquisition

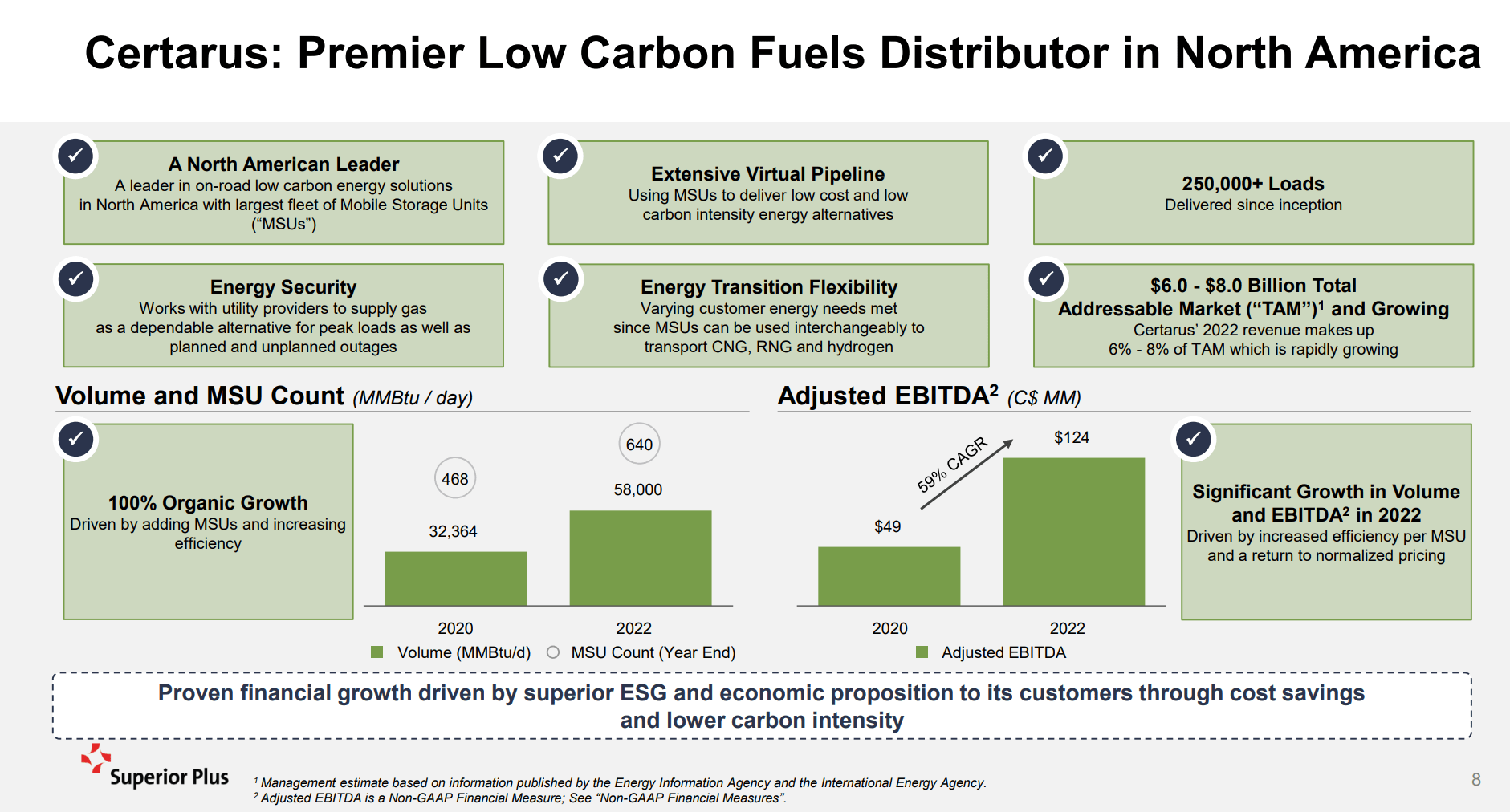

According to SPB's financial reports and presentations, Certarus is a transformational acquisition for the company as it positions Superior Plus to be a leading distributor of low carbon fuels like compressed natural gas ("CNG"), renewable natural gas ("RNG"), and hydrogen. Certarus has an estimated 6-8% market share of the fast growing $6-8 billion market (Figure 4).

{kind=link}

Financially, SPB is acquiring Certarus for $1.05 billion, comprised of $353 million in cash, $500 million of SPB shares (valued at $10.25 / share), and the assumption of $196 million in debt. On a pro-forma basis, Certarus shareholders will own approximately 17% of Superior Plus. Certarus had 2022 adjusted EBITDA of $124 million, so the transaction is valuing Certarus at 8.5x EV/EBITDA. Note, the acquisition multiple appears to be in line with historical SPB acquisitions, although the synergies from Certarus are unclear (Figure 5).

Figure 5 - Certarus transaction is in line with historical multiples paid (SPB investor presentation)

Like its propane distribution peer, Suburban Propane Partners ( SPH ), which recently spent US$190 million to acquire two RNG production facilities, Superior Plus appears to be preparing for a low carbon future by diversifying into CNG, RNG, and hydrogen generation and distribution.

Adjusting The Financials To Prosperity

As I wrote in my prior article, the challenge with analyzing acquisitive companies is that their financial statements are often riddled with adjustments and restructuring costs and it is hard to get a true picture of the underlying fundamentals.

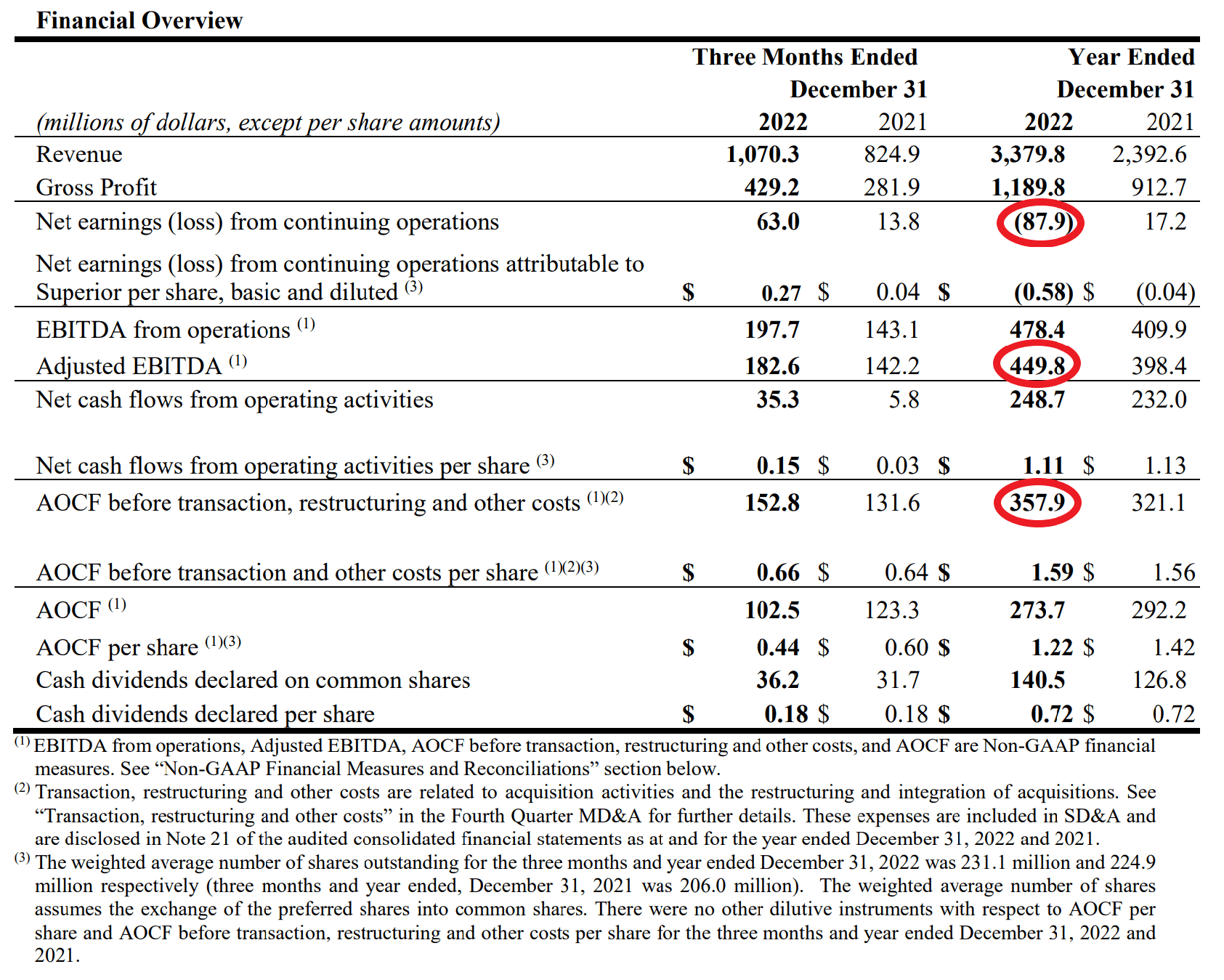

This was indeed the case with Superior Plus, as the company reported strong adjusted financial results to close out 2022, with adjusted EBITDA of $450 million (+12.9% YoY) and adjusted operating cash flow ("AOCF") before restructuring costs of $358 million (+11.5% YoY) (Figure 6).

Figure 6 - SPB 2022 financial overview (SPB Q4/2022 financial report)

{kind=link}

However, observant analysts will notice that net earnings from continuing operations actually fell to a loss of $88 million from $17 million in earnings in 2021. AOCF per share also fell 14.1% YoY to $1.22, suggesting shareholders were worse off despite the rosy headline adjusted figures.

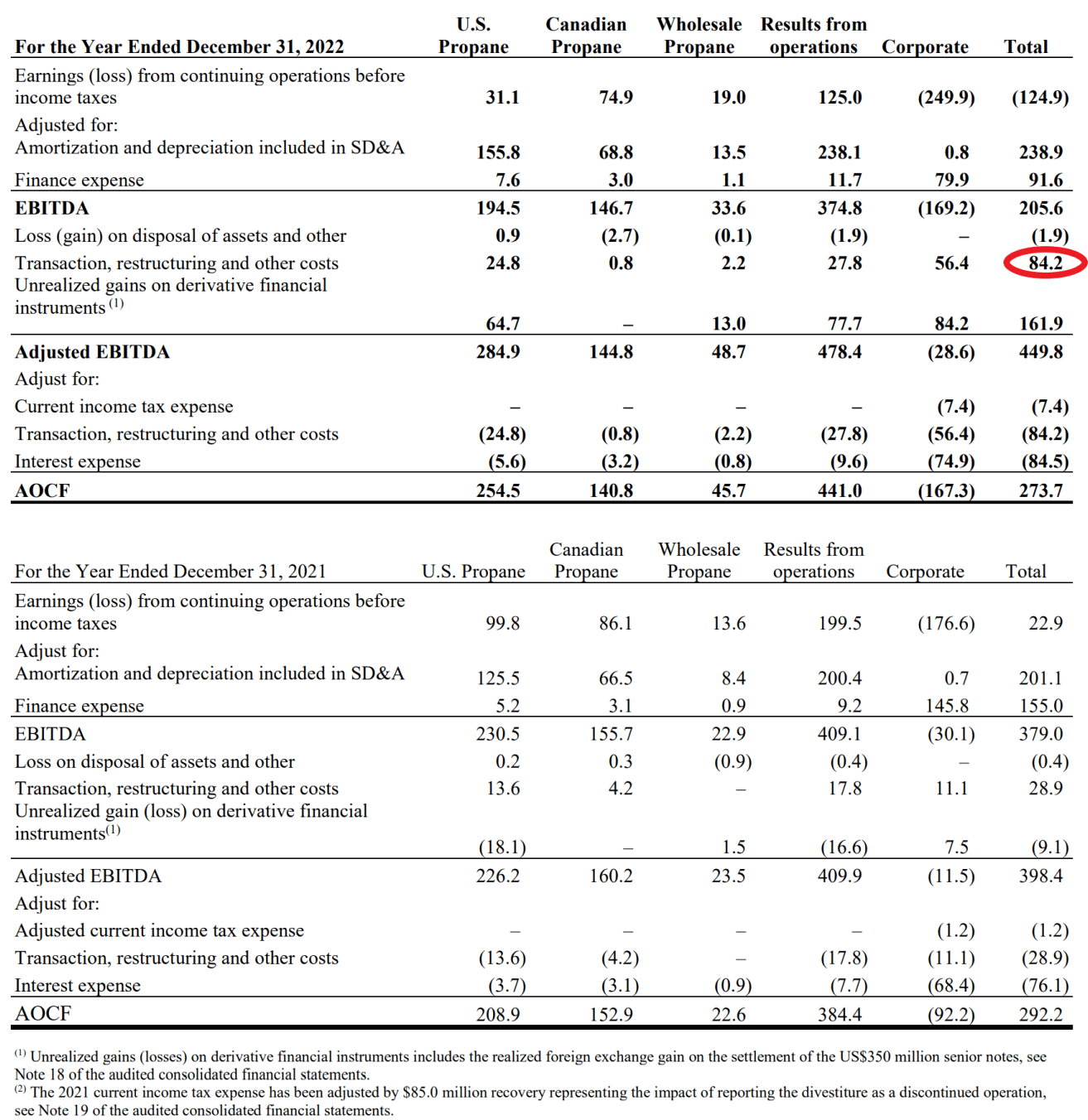

Analyzing the company's financials in more detail, we see Superior Plus recognized a worrisome $84 million in transaction, restructuring, and other costs in 2022. This figure appears excessively high and represents 18.7% of adjusted EBITDA (Figure 7).

Figure 7 - SPB segmented financial summary (SPB Q4/2022 financial report)

{kind=link}

Big Charges For A Deal Not Completed

Embedded in the $84 million in transaction costs for 2022 was $25 million plus interest related to a failed transaction from 2016. In late 2015, Superior Plus agreed to acquire Canexus, a Canadian chemicals business, out of bankruptcy. However, in mid-2016, Superior Plus backed out of the deal and was subsequently sued by Canexus for a $25 million termination fee. On December 22, 2022, the Alberta courts ruled against Superior and the company was required to pay the termination fee plus accrued interest to Chemtrade Logistics, which bought Canexus in 2017.

Although this appears to be a one-off case, the magnitude of the charge does highlight the inherent risk with Superior's growth by acquisition strategy.

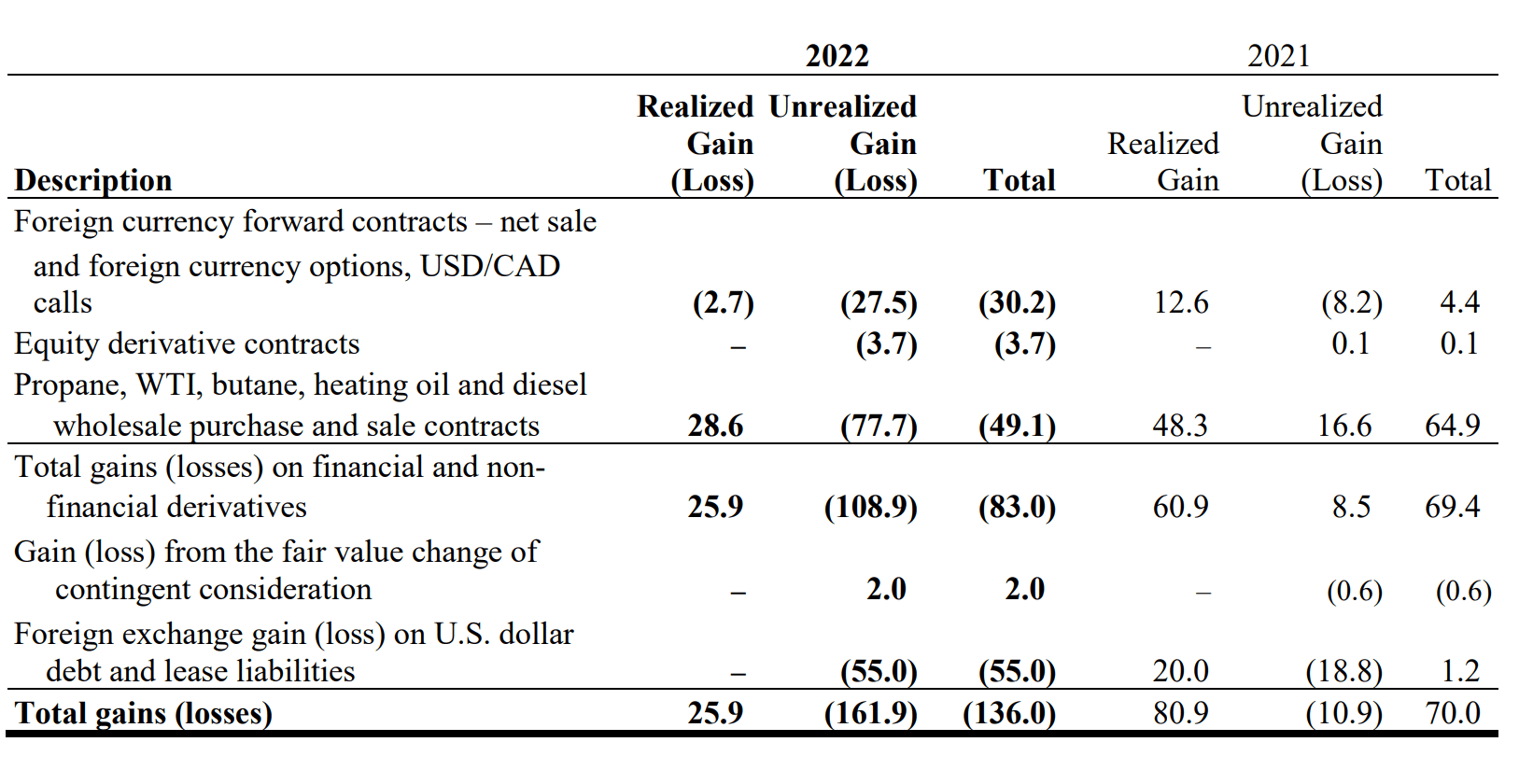

Large Hedging Losses

SPB's adjusted EBITDA also includes $162 million from unrealized losses on derivative financial instruments (Figure 8). As a commodity business, it is natural for SPB to hedge its commodity exposures and to experience gains and losses on those hedges. The key as analysts is to make sure that these gains and losses net out over time, so the company isn't making 'risky bets' via derivatives.

Figure 8 - Large unrealized hedging losses in 2022 (SPB Q4/2022 financial report)

{kind=link}

Decent Volumes Growth

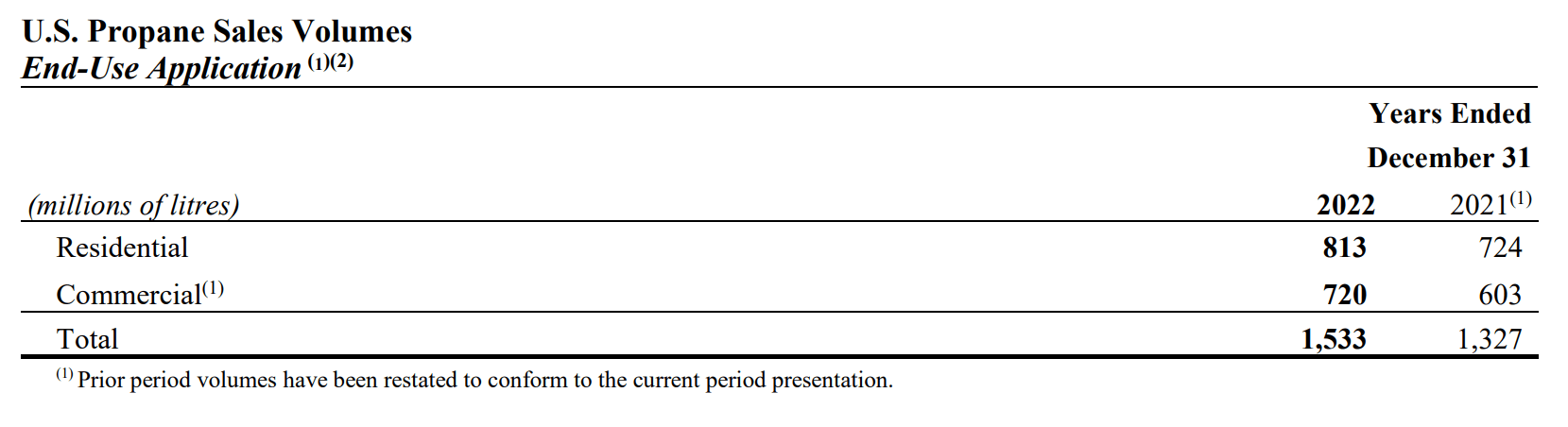

On the positive side, SPB's underlying businesses appear to be performing well, with U.S. propane volumes increasing 15.5% YoY to 1.5 billion liters in 2022, mostly on the back of acquisitions (Figure 9).

Figure 9 - U.S. propane volumes grew 15.5% YoY (SPB Q4/2022 financial report)

{kind=link}

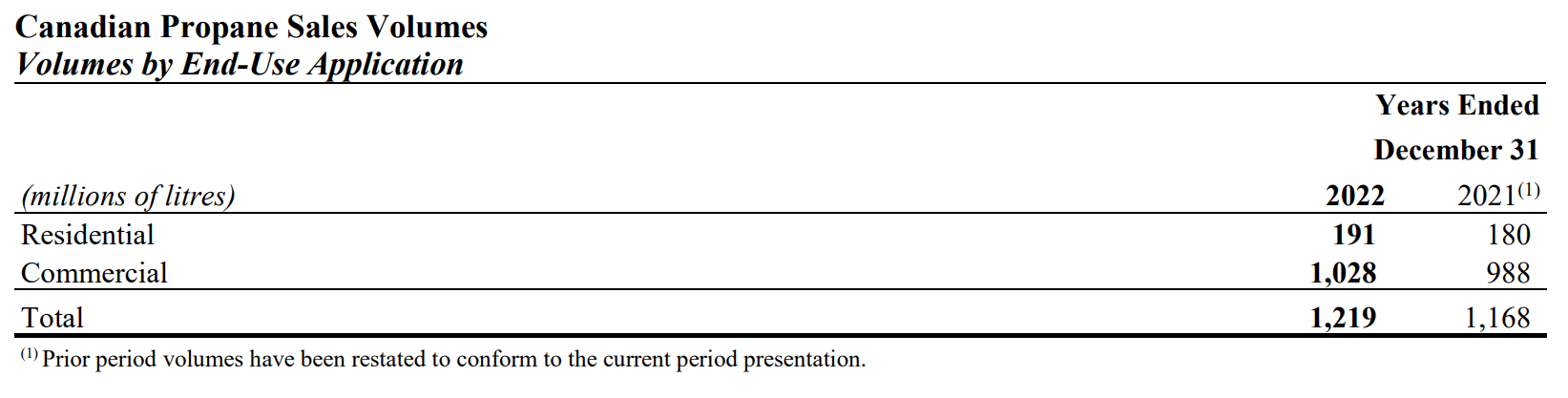

Canadian volume growth was more muted, rising only 4.4% YoY on the absence of acquisitions. (Figure 10).

Figure 10 - Canadian propane volumes grew 4.4% YoY (SPB Q4/2022 financial report)

{kind=link}

Stretched Balance Sheet

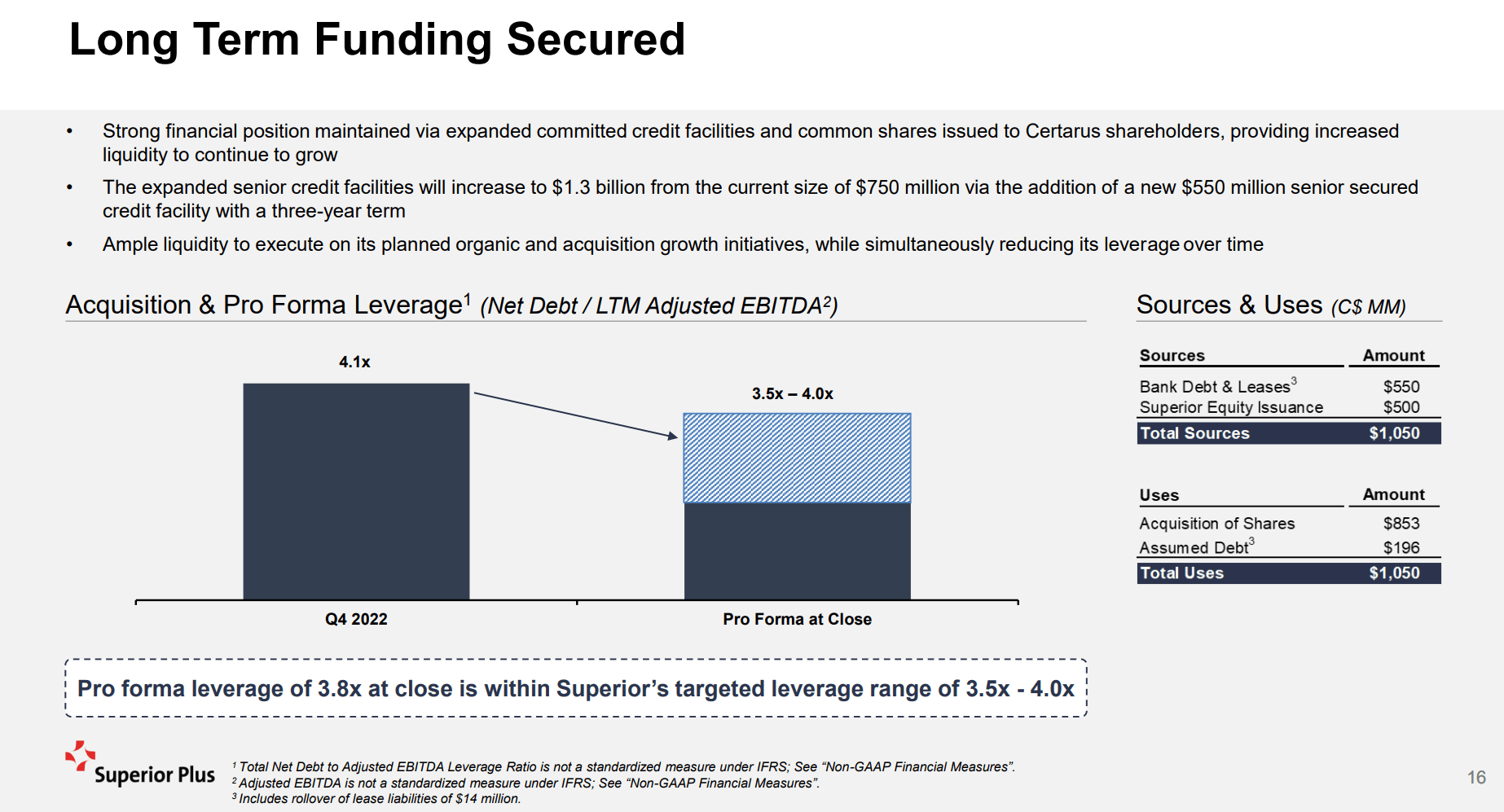

In order to consummate the Certarus acquisition, SPB also increased its senior credit facilities to $1.3 billion from the current $750 million. Pro-forma the funding of the Certarus transaction, Superior will have leverage of 3.8x EBITDA (Figure 11).

Figure 11 - SPB will take on more debt to complete Certarus transaction (SPB investor presentation)

{kind=link}

While Superior Plus has no near-term debt maturities, the high levels of debt outstanding is worrisome, particularly as we see long-term interest rates climb and the economy slow down.

Valuation

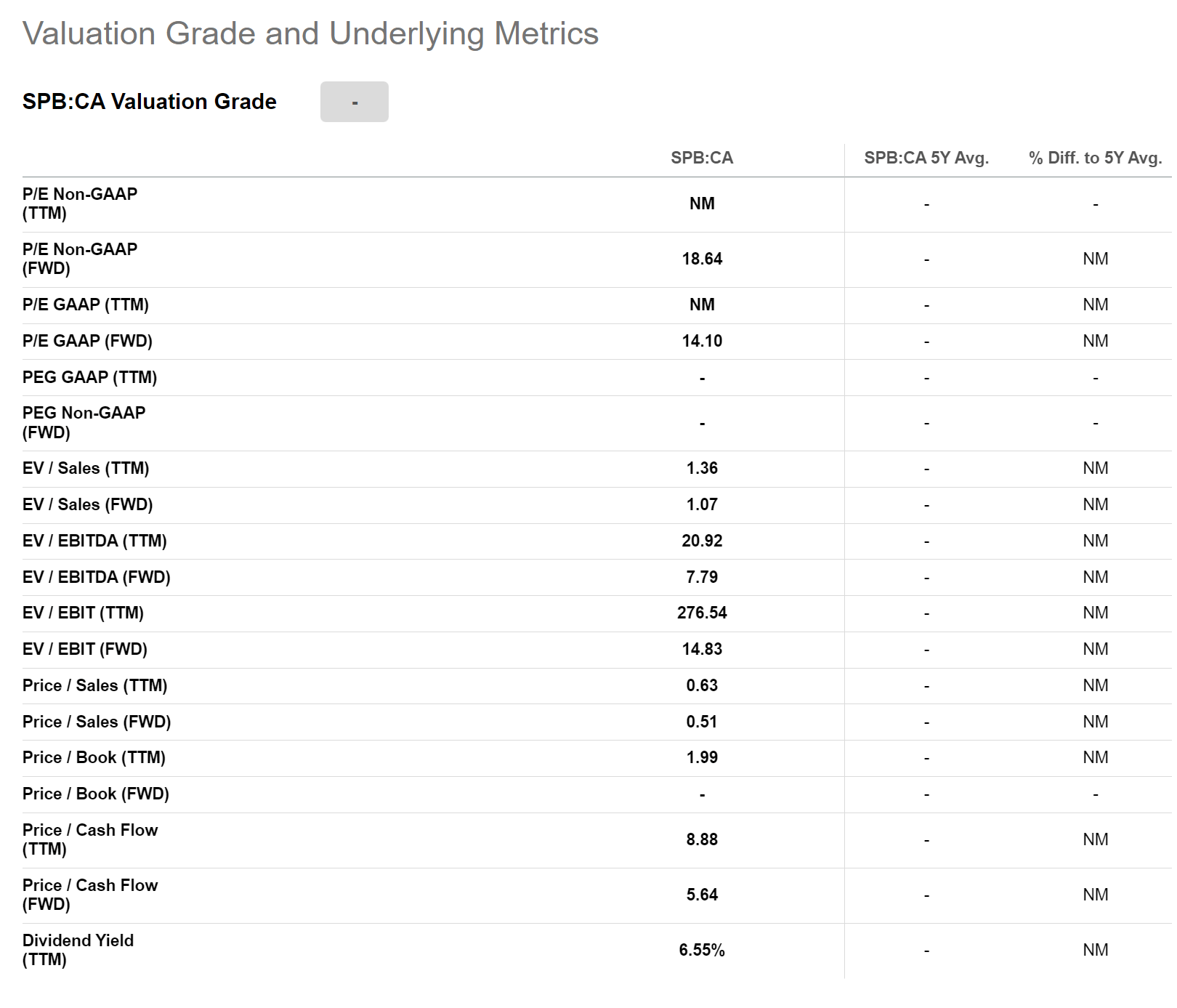

In terms of valuation, according to Seeking Alpha, Superior Plus currently trades at a forward P/E multiple of 18.6x, and forward EV/EBITDA multiple of 7.8x (Figure 12).

{kind=link}

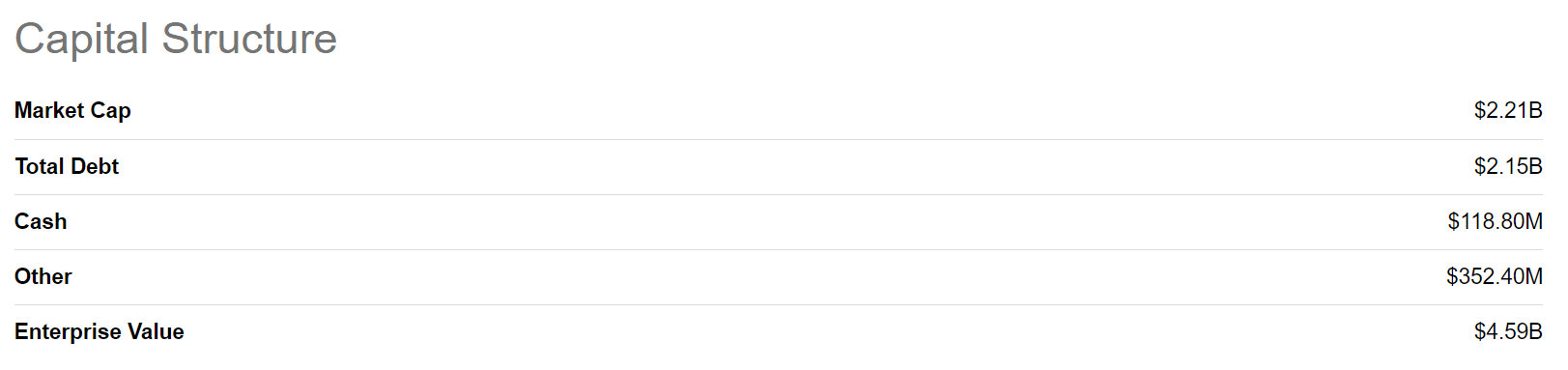

However, I believe the EV/EBITDA figures above are understated. Seeking Alpha's Enterprise Value ("EV") calculation is based on the latest financial reports and shows SPB with an EV of $4.6 billion (Figure 13).

{kind=link}

However, the EV figure does not include the in-process acquisition of Certarus which will add 48.8 million shares ($500 million issued at $10.25). On the other hand, the forward EBITDA of $590 million already includes the addition of Certarus, as per management's guidance from figure 2 above.

Therefore, to be accurate, SPB's pro-forma EV should be based on pro-forma 250 million shares (last reported 201 million shares plus 48.8 shares to be issued) outstanding, pro-forma debt of $2.35 billion ($2.15 billion in debt plus $196 million in assumed Certarus debt), less -$234 million in cash ($119 million in cash less $353 million in cash payment to Certarus), and other of $352 million. This works out to a pro-forma EV of $5.7 billion. Using pro-forma EV, Superior Plus is currently trading at a Fwd EV/EBITDA of 9.7x.

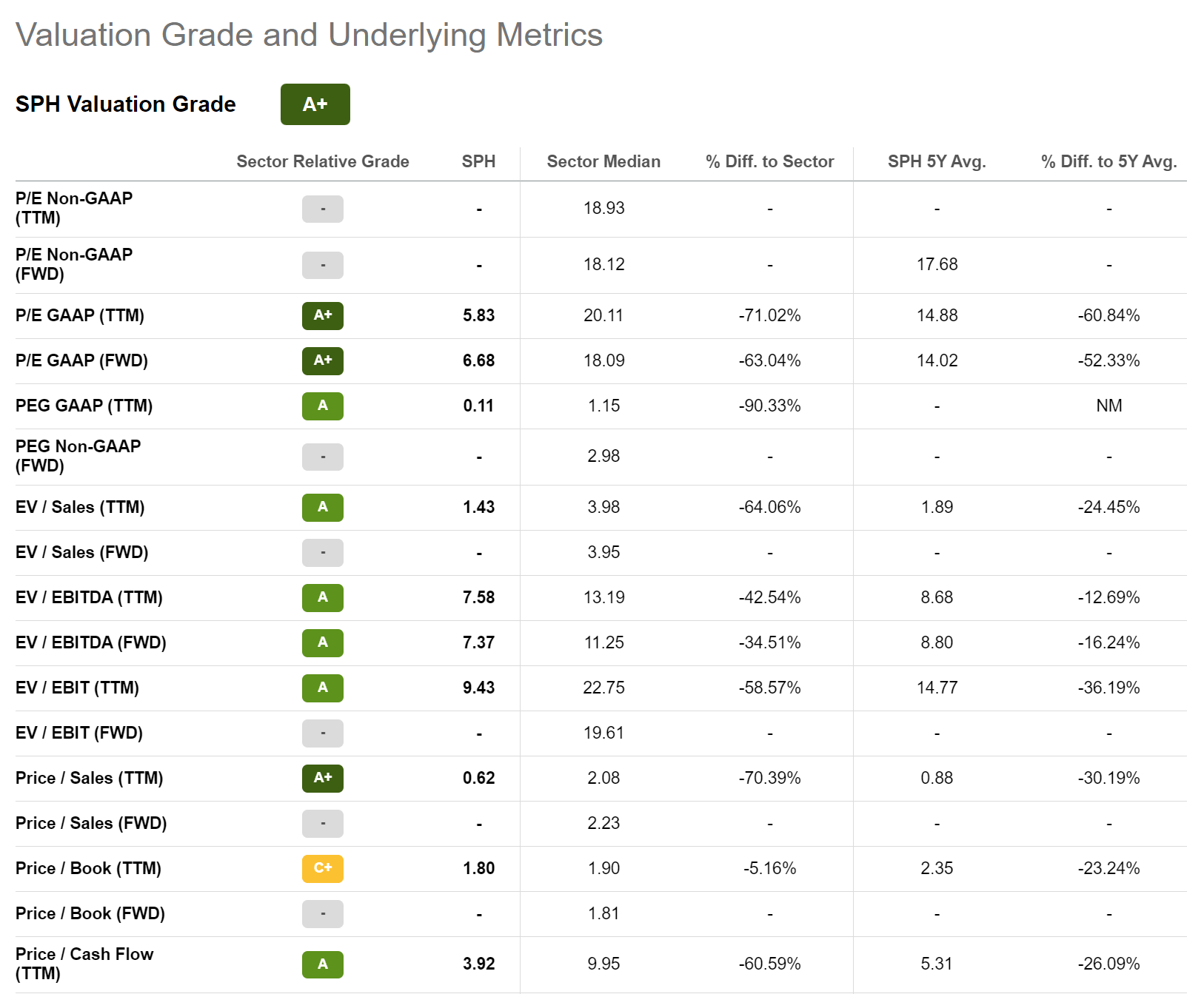

Comparing Superior Plus to its closest public peer, Suburban Propane, we find that Superior is almost 2.5x EV/EBITDA more expensive relative to SPH, which only trades at 7.4x Fwd EV/EBITDA (Figure 14). P/E ratios are not comparable as SPH is an MLP and pays no corporate taxes.

{kind=link}

Preferred Share Overhangs On Valuation

Furthermore, Superior Plus still has US$260 million in preferred stock outstanding that were issued to Brookfield Asset Management in 2020.

The preferred stock pays an annual 7.25% dividend and are exchangeable into 30.0 common shares. If the preferred shares are not redeemed by 2027, the dividend rate will increase by 0.75% per annum up to 10.25%.

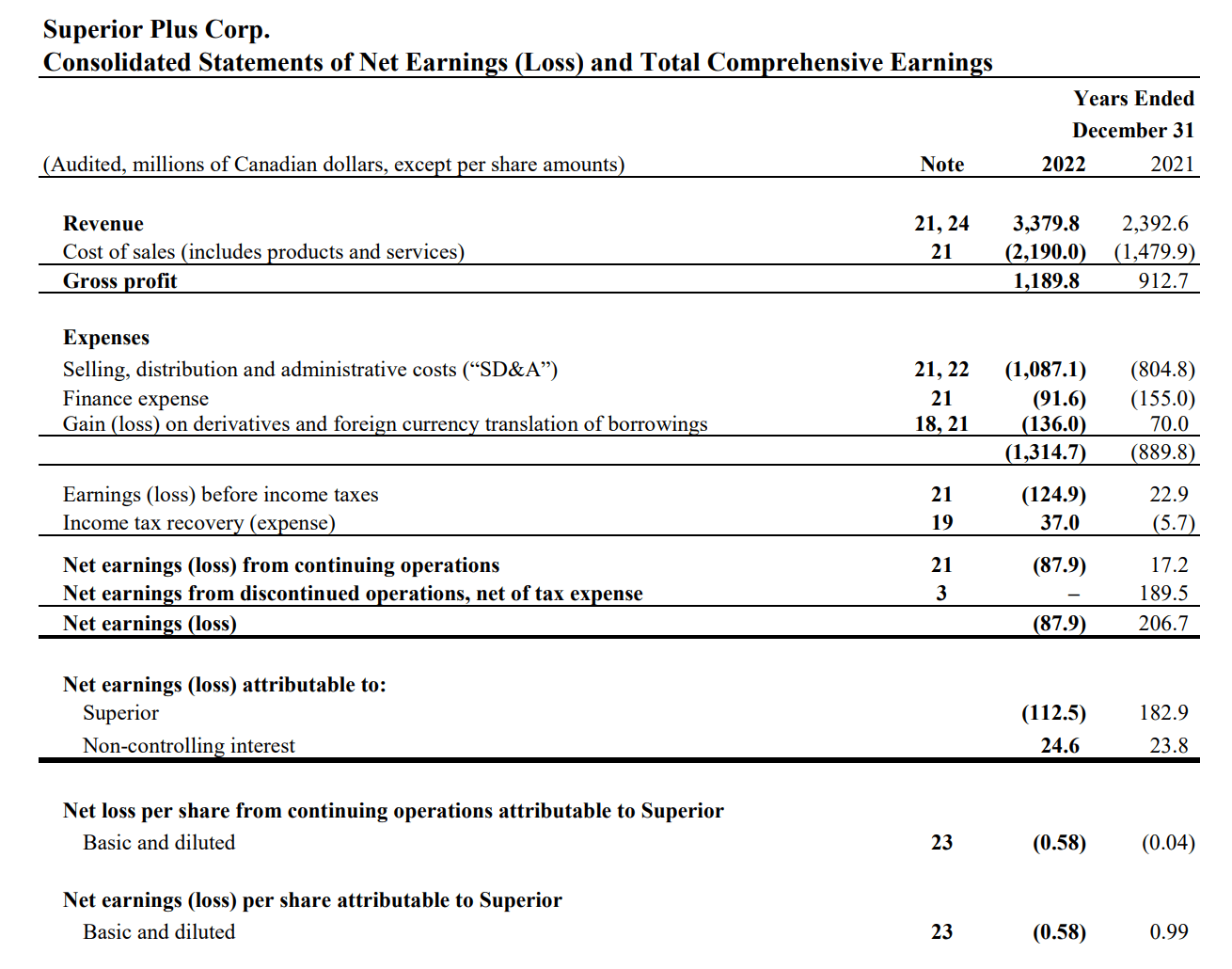

The preferred shares rank ahead of common shareholders, so even though Superior suffered a net loss of $88 million in 2022, the preferred shareholders were still allocated $25 million in net income while the common shareholders were allocated a $113 million net loss (Figure 15).

Figure 15 - SPB 2022 income statement (SPB Q4/2022 financials)

{kind=link}

In my opinion, this 'heads I win, tails you lose' structure is very unattractive for common shareholders.

Conclusion

Superior Plus has recently made a large acquisition in the nascent low-carbon fuels space, paying $1.05 billion to acquire Certarus Ltd. By management's estimates, this helps the company achieve its 2026 EBITDA goals by 2024. However, I am still concerned by Superior's financials, which continue to be heavily adjusted due to the company's acquisitive nature. Unadjusted, SPB appears to be a money-losing enterprise.

Furthermore, based on management's guidance of $585 - $635 million in adjusted 2024 EBITDA, the company is trading at a pro-forma Fwd EV/EBITDA multiple of 9.7x, far above its public comparable, Suburban Propane.

With a stretched balance sheet and unattractive preferred shares that sit ahead of common shareholders, I simply do not see the attractiveness of SPB's common shares.

For further details see:

Superior Plus: Transformative Acquisition But Still Expensive