CA - Supremex Continues To Grow Yet Trades At 4.8x TTM P/E

2023-08-16 10:43:28 ET

Summary

- Supremex's Q2 2023 results demonstrate successful execution of the diversification strategy into Packaging with total sales growth YoY of 27.3% for the YTD six-month period.

- Investors are not currently paying for this growth with the shares trading at only 4.8x TTM P/E or an estimated 9.9% FCF yield, including acquisition spending.

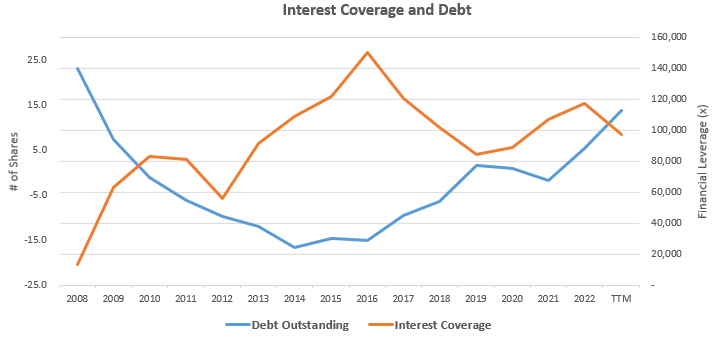

- Debt levels still look healthy with interest coverage at 8.5x and debt-to-EBITDA of 1.9x.

Supremex (SUMXF) is back on my radar after a sharp decline of 39.5% from 52-week highs. This drop leaves the company trading at 4.8x TTM P/E and a 2.8% dividend yield in addition to regular share repurchases which will be discussed later. Supremex's share price has had a great run in recent years as the company continues to perform well in its diversification strategy and is building cash flows and book value as this article will discuss.

Since I last wrote about Supremex back in November 2020 the stock has returned a whopping total return of 295.7% compared to the S&P 500 total return of 24.0%. Unfortunately, I did not fully participate in these great returns as I sold out my position around $4.05 in August 2022 for a +50% total return. A year later and with continued execution of its strategy, Supremex is back on my radar as a potential investment in an expensive equity market.

Latest Q2 Show Continued Growth through Acquisitions

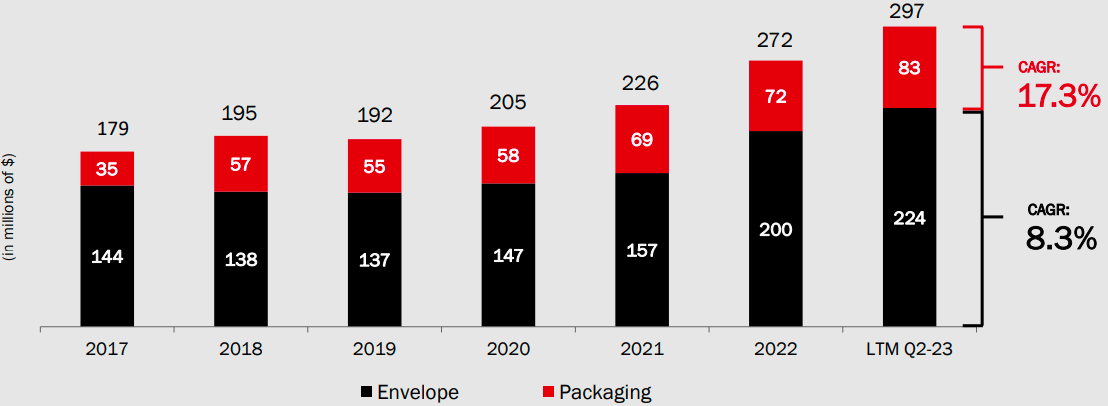

Supremex's latest results in Q2 2023 showed continued execution of the company's strategy to continue diversification into the growing Packaging segment while consolidating players in the shrinking Envelope market. Total revenues as of Q2 2023 for the company grew to $307 million for the trailing twelve-month period from $272 million in fiscal 2022. The company has made two sizable acquisitions recently with Impression Paragraphs acquired in January for $26.6 million and Graf-Pak Inc . in May for $6 million to continue their expansion into the packaging market.

The Envelope segment saw trailing twelve-month sales of $224 million which was 12% higher compared to $200 million for fiscal year 2023. The company's Packaging segment's TTM revenue grew 15% to $83 million from $72 million in 2022. This latest quarter leaves intact the trend of 17.3% and 8.3% annualized compounding revenue growth in the Envelope and Packaging segment respectfully since 2017. This can be seen in the below slide from management's Q2 presentation. Keep in mind when we discuss these growth rates for the TTM as of Q2 2023 that this twelve-month data only includes two new quarters compared to fiscal year 2022, so the annualized growth rate is much higher. For the six-month period ended Q2 2023, revenues are 27.3% higher at $160 million compared to $126 million for the six months ended Q2 2022.

Revenue Breakdown for Supremex (August 2023 Investor Presentation)

{kind=link}

An Old Cash Cow of a Business

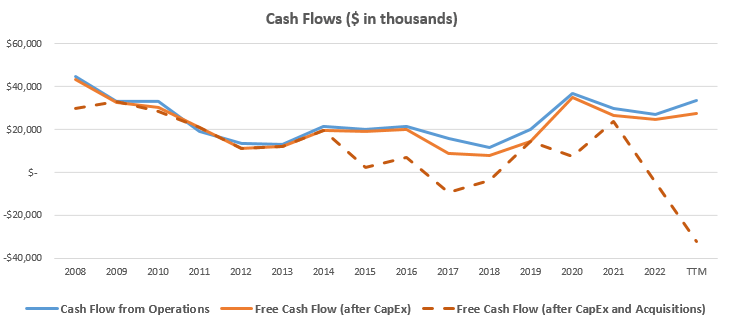

Supremex had a rough start to the past decade with the decline in its Envelope business leading to massive goodwill impairments in 2008, 2009, and 2012 of $148.3M, $43.0M, and $28.9M, respectively. That being said, the company continues to churn out free cash flow after capital expenditures in the high $25 to $27 million range the past couple of years. The company's Envelope business is an old cash cow helping the business not have a single year of negative free cash flow ((FCF)) after accounting for capital expenditures and only negative FCF when including acquisitions, as can be seen in the graph below.

Supremex Cash Flow Highlights (compiled by author from company financials)

{kind=link}

Supremex saw large declines in FCF after the 2008 financial crisis and continued secular decline in the Envelope business. However, management is looking able to navigate this trend as growth has stabilized since 2012 with the company plowing money into the packaging business. Much of the recent acquisitions have been sustainably financed by cash flow from operations, as indicated through the graph of FCF above only passing into the negative in 2017 due to its large $17.5 million acquisition of Stuart Packaging and again recently in the TTM period due to its $26.5 million acquisition of Impression Paragraph Inc . Given how important acquisitions have been in the recent business model of Supremex, any cash flow valuation would need to take these acquisitions into account.

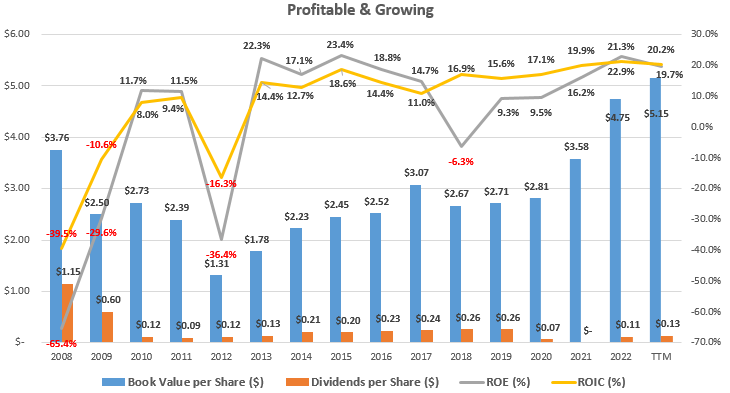

The secular decline in the envelope business has led to a rough early decade for Supremex's net income as noted earlier and as seen in the graph below. The company's continued acquisitions in recent years have left the balance sheet consisting of 20% goodwill which could be exposed to impairments if acquisitions do not work out as forecasted. For now, the healthy ROE and ROIC around 20% seem to support the growth in the balance sheet.

Historical Profitability & Growth of Supremex (compiled by author from company financials)

{kind=link}

Cash Flow Analysis

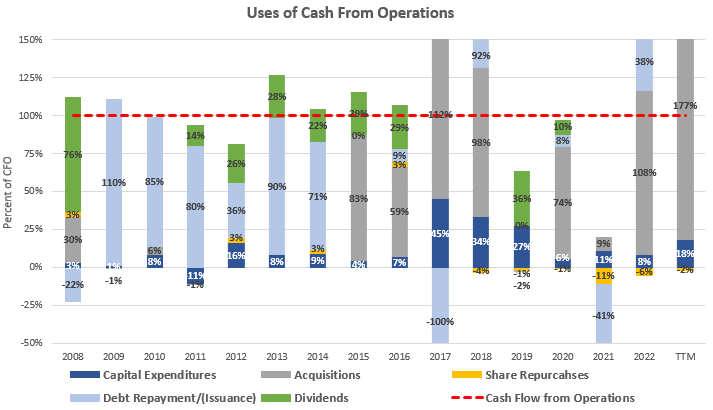

Supremex does a great job of generating cash and returns it to the shareholder through both dividends and share repurchases. To get an idea of the sustainability of dividends and share repurchases, we can take a look at what percent of cash flow from operations is available to be returned to shareholders after making the necessary capital expenditures.

As can be seen below, capital expenditures and acquisitions only used up on average only 59% of cash flow from operations over the past decade. This leaves approximately 41% to be returned to investors in the form of dividends and share repurchases. With an average cash flow from operations of $31.9 million over the past three-year period, this 41% would imply free cash flow to shareholders of $13.0 million for around a 9.9% free cash flow yield at the current $131.4 million market capitalization.

Cash Flow Analysis (compiled by author from company financials)

{kind=link}

How is the Leverage?

Supremex's acquisition strategy has led to the company building up debt on the balance sheet to the tune of $113 million as of the latest quarter. While the debt level has grown significantly as can be seen in the graph below, the latest results still leave interest coverage at a healthy 8.5x in the TTM period. In terms of debt-to-EBITDA, Supremex's $59.2 million adjusted EBITDA as shown in the latest investor presentation, give a reasonable debt-to-EBITDA of 1.9x sitting on the company's credit facility line which finances their acquisitions. This is a healthy level in my opinion and one Supremex's bankers seem comfortable with too; albeit from a different capital position as a creditor.

Interest Coverage and Debt at Supremex (compiled by author from company financials)

{kind=link}

Since 2008, Supremex has bought back an average of 0.8% of their outstanding shares. I always like to see share repurchases by management as it shows capital budget discipline and management's faith in the long-term prospects of the business, especially when done at favorable valuations. The opportunistic share repurchases done by management through COVID are hugely appreciated as a shareholder.

Here is how that story played out! During the beginning of COVID in Q1 2020, management cut the dividend but reinstated it in Q1 2021 and have already raised it twice since then to the current 3.5 cents per quarter ($0.14 annually). However, even though management cut the dividend, they opportunistically redirected those cash flows to repurchasing the company's shares while the stock valuation was suffering with $3.3 million worth of shares repurchased in 2021 and $1.5 million in 2022. This was up significantly (+200%) from pre-2020 share repurchase levels around $0.4 million annually. With the stock valuation higher now, management is switching its shareholder return strategy back over to dividends with the $3.3 million in the TTM or $0.14 dividend per year going forward already making up around half the $0.26 per year pre-COVID.

Risks

Supremex's acquisition strategy to navigate the secular declining envelope business is not without risks and has led to the company building up significant debt and goodwill on the balance sheet. The company had to write-down and impair assets in the years after 2008 leading to significant EPS losses. For now the company's acquisition strategy seems to be going successfully with high overall company ROE and ROIC remaining strong and supporting the acquisitions and growth of the balance sheet. If this trend were to reverse as acquisitions do not turn out as expected, or if the economy falls into a hard recession, there could be similar impairments to the goodwill sitting on the balance sheet.

Takeaway for Investors

Supremex is an interesting old cash cow that is currently only trading at 4.8x TTM P/E (20.8% earnings yield) or an estimated free cash flow yield including spending on acquisitions around 9.9%. The company continues to grow nicely into packaging as it navigates the secular decline in the envelope business with growth over the latest six-month period up 27.3%. The growth in debt at the company looks manageable for now with interest coverage still healthy around 8.5x. Supremex is back on my radar after its recent pullback and I will be watching for continued growth from the recent acquisitions.

For further details see:

Supremex Continues To Grow, Yet Trades At 4.8x TTM P/E