CA - Supremex: Supreme Q1 2023 Results But Orders Are Under Pressure

2023-05-27 06:32:22 ET

Summary

- The company’s revenues rose by 39.8% in Q1 2023 while adjusted EBITDA soared by 55.4% thanks to acquisitions, and high average selling prices in the envelope segment.

- The current annual revenue run rate is around C$350 million ($257 million) and Supremex is trading at an LTM EV/EBITDA ratio of just 3.5x.

- However, the company warned about a slowdown in new orders and revenues are likely to decline in Q2 2023.

- Yet, I think that annualized EBITDA is unlikely to drop below C$40 million ($29.4 million) this year and this would put the EV/EBITDA ratio at 5.6x which I still consider low.

Introduction

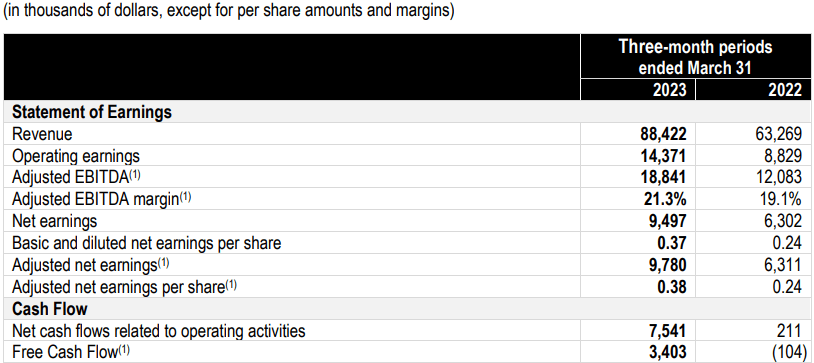

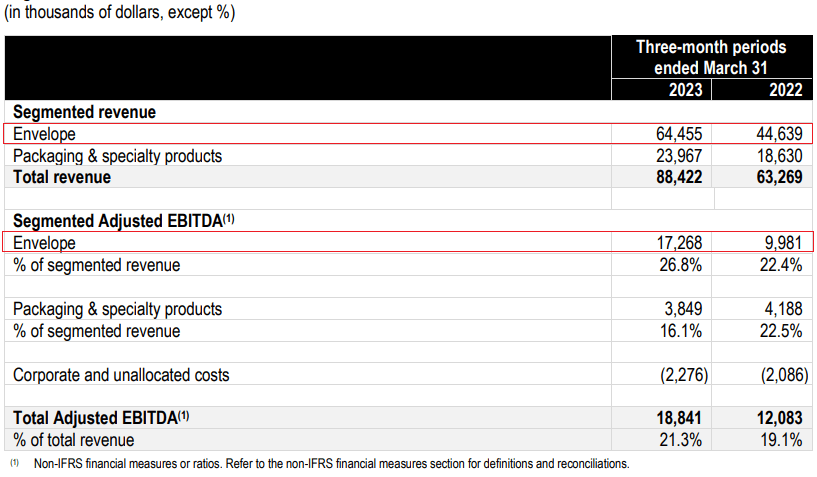

In March, I wrote an article on SA about Canadian envelope producer Supremex ( OTCPK:SUMXF ) ( SXP:CA ) in which I said that acquisitions should boost EBITDA in the near future and that I expected the dividend yield to increase significantly. Well, Q1 2023 revenues rose by 39.8% to C$88.4 million ($64.9 million) thanks to the consolidation of Royal Envelope, and Paragraph while adjusted EBITDA soared by 55.4% to C$18.8 million ($13.8 million) thanks to high average selling prices in the envelope segment. However, the quarterly dividend remained at C$0.035 ($0.026) per share as the net debt has increased significantly following the recent acquisitions. Looking ahead, it seems that new orders are slowing down and that revenues and margins could decline in Q2 2023. Yet, I think that the pivot to the packaging segment is going well and that annualized adjusted EBITDA should remain above C$40 million ($29.4 million) in 2023. Let's review.

Overview of the Q1 2023 results

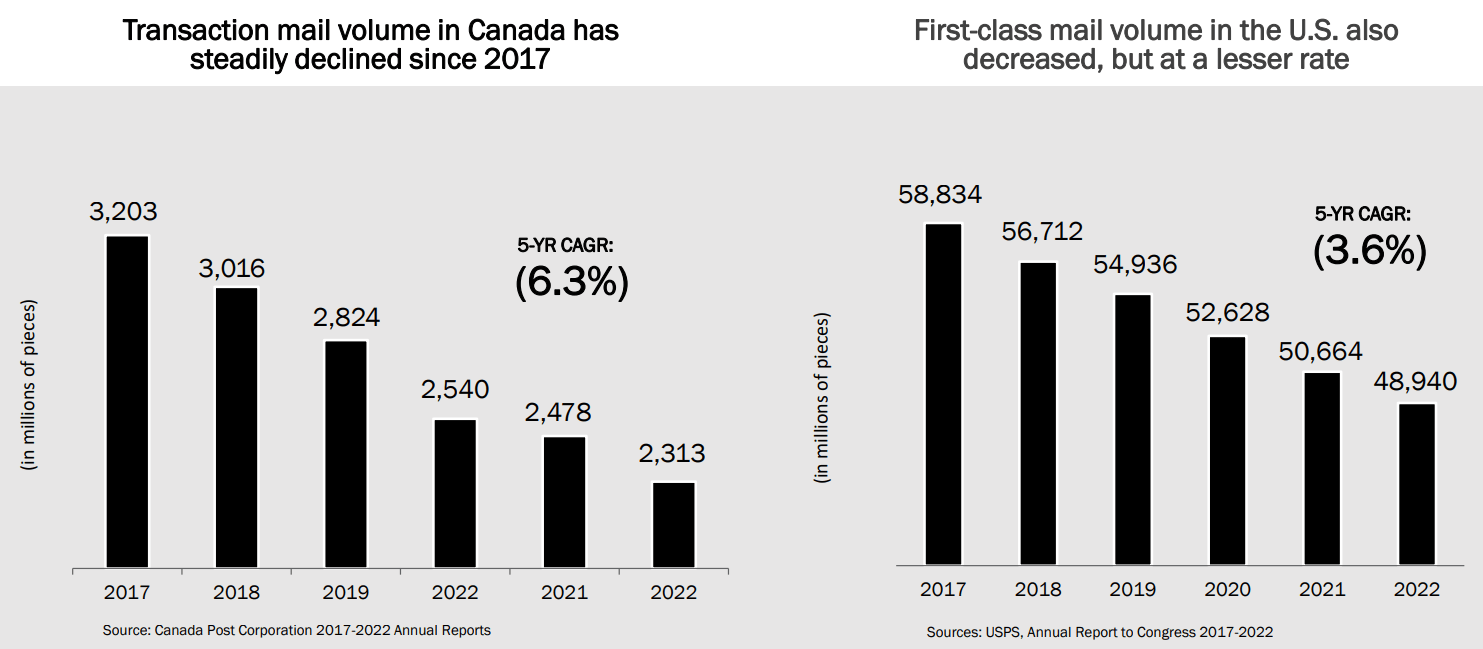

In case you're not familiar with Supremex or my earlier coverage, here's a quick description of the business. The company specializes in the manufacturing of stock and custom envelopes as well as paper-based packaging solutions and specialty products such as premium quality folding carton packaging, e-commerce solutions, and labels. Supremex is the largest envelope producer in Canada as well as the largest independent folding carton provider in Quebec and its business includes 17 manufacturing facilities and over 1,000 employees. The envelope segment accounts for about 70% of revenues but the issue here is that this market is shrinking rapidly as the transaction mail volume in Canada and the first-class mail volume in the USA has been shrinking over the past several years.

{kind=link}

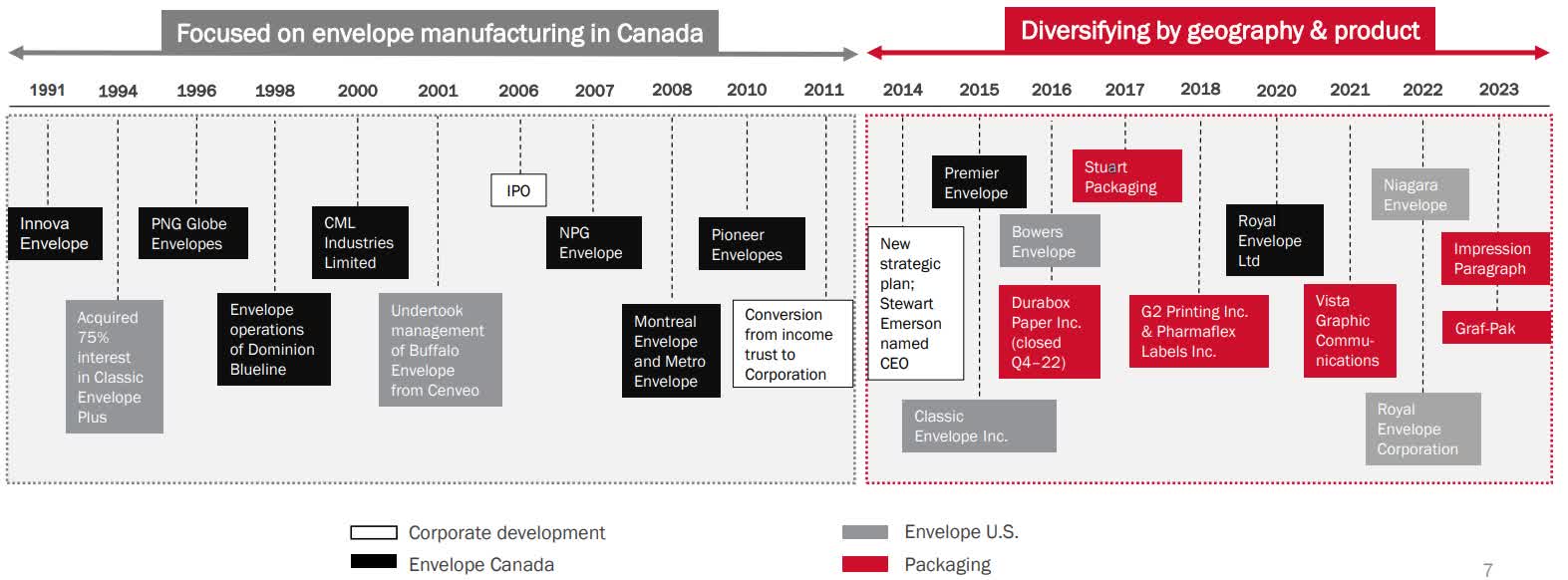

In view of this, Supremex has been shifting its focus to the packaging market and its aim is to grow the revenues of this segment to match its envelopes business by the end of 2025. It's an ambitious goal that requires about C$150 million ($110 million) in new packaging business but I think it's achievable if the company continues to bet on M&A to expand. As you can see from the chart below, Supremex has completed several acquisitions in the packaging sector over the past few years and I expect it to make several tuck-in purchases by 2025.

{kind=link}

The latest acquisition was announced on May 8, and it includes Canadian folding carton packaging solutions manufacturer Graf-Pak. This company has annual sales of around C$6.7 million ($4.9 million) and I think it should bring in decent synergies for the Greater Montreal area business of Supremex as its plant is located just 15 km away from the Lachine facility.

Turning our attention to the financial performance of Supremex, I think that the Q1 2023 results were strong as revenues soared by close to 40% while adjusted EBITDA increased year on year for the 13th consecutive quarter.

{kind=link}

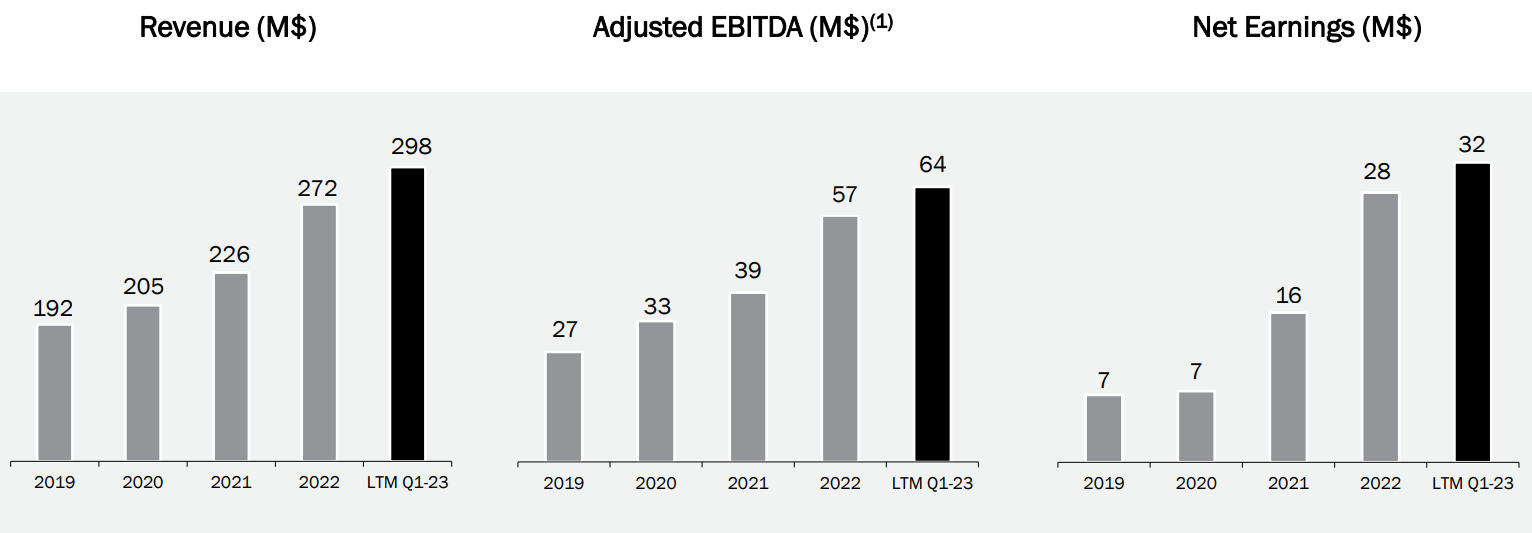

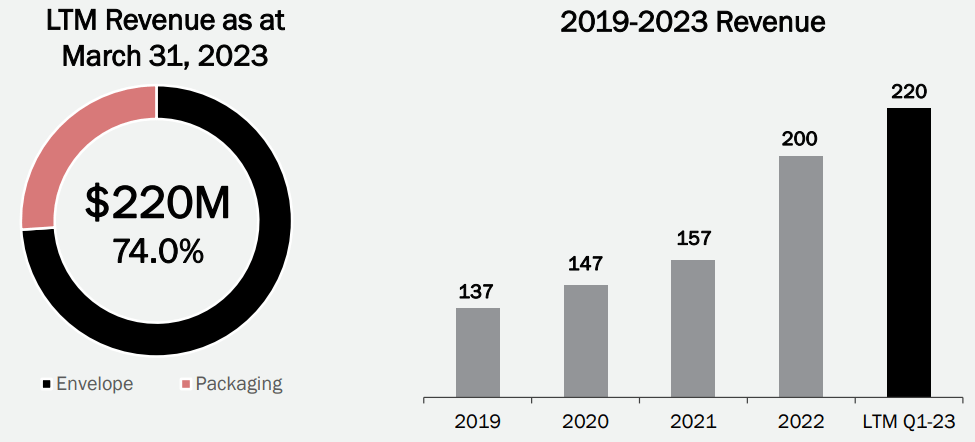

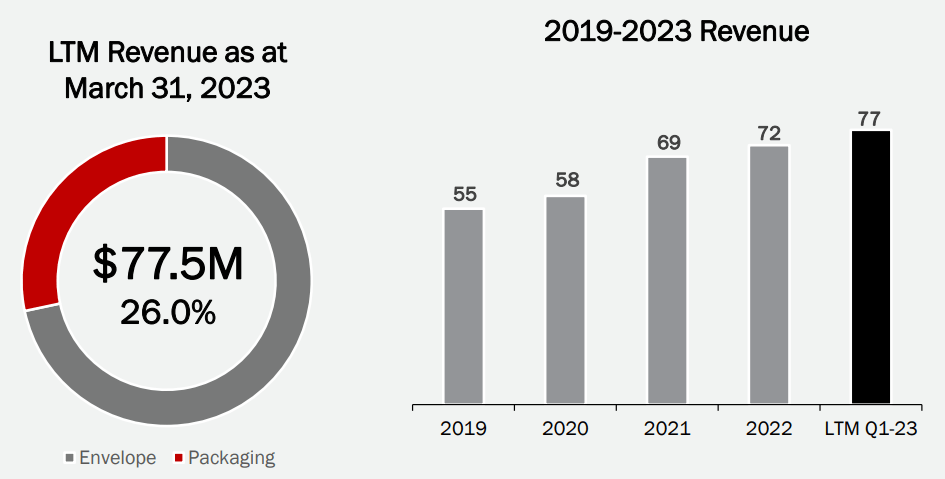

Looking at the LTM trends, we can see that all key financial metrics continued improving at a steady pace and the main reason behind this is the strong performance of the envelope segment. The current annual revenue run rate is around C$350 million ($257 million).

{kind=link}

The envelope business of Supremex has been getting a strong boost from high bookings due to strong demand following the end of COVID-19 lockdowns and the company saw a continuation of this trend in Q1 2023 as the average selling price increased by 40.1% year on year. In addition, this was the first full quarter with Royal Envelope, which added about C$12 million ($8.8 million) of revenues. Looking at the packaging segment, revenues grew by 28.7% in Q1 2023 thanks to a C$7.8 million ($5.7 million) contribution from Paragraph as well as higher e-commerce-related sales.

{kind=link}

{kind=link}

However, the envelope segment still accounts for the vast majority of EBITDA and Supremex will need to make several acquisitions over the next 18 months to pivot to the packaging business.

{kind=link}

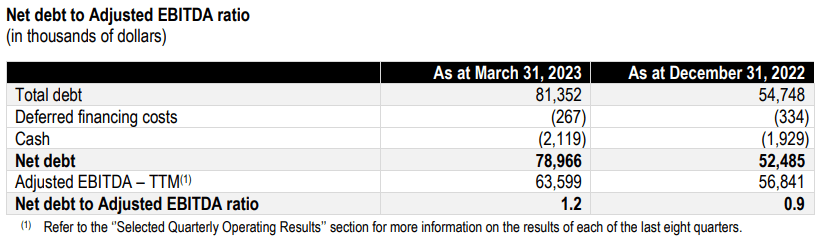

Turning our attention to the balance sheet, net debt rose to C$79 million ($58 million) in Q1 2023 as a result of the purchase of Paragraph for C$27.1 million ($19.9 million). Supremex is keeping its dividend unchanged and it has enough funds to pursue acquisition opportunities as it had C$39.9 million ($29.3 million) in available liquidity under its senior secured revolving credit facility of C$120 million ($88.1 million) as of the end of March 2023.

{kind=link}

Looking at what to expect in the future, Supremex warned during its Q1 2023 earnings call that both the envelope and packaging segments are seeing a slowdown in new orders as customers are now reducing inventory levels built during 2022. Revenues are likely to go down in Q2 and I think the decline could stretch into Q3 and Q4 as the average selling prices in the envelope segment gradually return to pre-pandemic levels. That being said, I expect annualized EBITDA to remain above C$40 million ($29.4 million) in Q4 as Supremex is now a much larger company compared to the time before the end of COVID-19 lockdowns as a result of several acquisitions.

Turning our attention to the valuation, Supremex has an enterprise value of C$223.2 million ($163.9 million) as of the time of writing and is trading at an LTM EV/EBITDA ratio of 3.5x. If we are conservative and assume that annualized EBITDA drops to C$40 million ($29.4 million), this ratio increases to 5.6x. Considering that Supremex has a leading market position in the envelope segment in Canada and has been steadily growing its business over the past several years, I think that it should be trading at above 6x EV/EBITDA. At an annual EBITDA of C$40 million ($29.4 million), this translates into C$6.20 ($4.55) per share.

Looking at the risks for the bull case, I think the major one is an economic slowdown in North America as this could accelerate the decline in the transaction mail volume in Canada and the first-class mail volume in the USA. It's also possible that Supremex doesn't manage to find enough suitable M&A targets over the coming 18 months and is thus unable to pivot to the packaging business. Also, the slowdown of orders from customers could be more severe than the company anticipates.

Investor takeaway

Supremex had a strong start to 2023 but there could be a significant decline in its revenues over the coming quarters as there is a slowdown in new orders. Yet, I think that the company looks cheap at the moment as it's trading at just 3.5x LTM EV/EBITDA. Even if annualized EBITDA drops to C$40 million ($29.4 million), Supremex doesn't look expensive, and I think that revenues and EBITDA could be higher by 2025 as the company continues to snap up small competitors over the coming months.

For further details see:

Supremex: Supreme Q1 2023 Results But Orders Are Under Pressure