MU - Synergy Investing: Cirrus Logic's Coming Story

2023-07-13 12:00:00 ET

Summary

- Cirrus Logic's stock has suffered due to the loss of an iPhone haptic product, but its prospects look promising due to potential synergies. These include growth vectors in Apple, Android, and a new PC business.

- Despite a bearish outlook in the short term, Cirrus has a history of buying significant shares during periods of low pricing. It increased the future SAM from $6.5 billion to almost $8.5 billion.

- Cirrus is developing new products for Apple and expanding into the PC market. It is also cutting costs by reducing physical facilities overhead and headcount.

The market spoke loudly and badly about Cirrus Logic ( CRUS ) after analysts and the company announced the loss of an iPhone haptic product even though the offending issue resided with another company. It ignored reasoning and tanked the price. Investors might consider moving on, but by doing so, long-term thinkers ignore its future of synergy . Defining synergy in conjunction with investing means a period when businesses simultaneously align toward growth. It appears that's exactly what is happening at Logic. The potential isn't small and may last more than a few years. The rowers are rowing in unison, listening to the coxswain's beat.

The Bad

Before beginning, let's get the bad news out of the way. Heading to the charts, when comparing the Philadelphia Semiconductor Index ( SOX ), Cirrus' sector index, with the Logic chart, the view isn't bullish; it's bearish, very bearish.

{kind=link}

Notice Cirrus' price collapse began while the SOX continued north. In general, this type of divergence predicts further weakness should the index turn south. The fact that Cirrus has already overcorrected doesn't insulate future movements against bearish sector trading. Buyers need to beware and vigilant. But again, if readers stop here, they miss the rest of the story.

The Good

Yet, strangely, the monthly chart included below illustrates a continued bullish stance with the long-term trend still magically intact. Strange!!!

{kind=link}

In addition, Cirrus has a lengthy history of buying significant shares of stock especially during periods of, in the belief of management, cheap pricing. In the March quarter, management purchased 350,000 shares of stock at prices above $100 followed by 275,000 shares in April at $87. With over $500 million in cash, expect larger purchases during the balance of the June quarter at prices in the $75 range. We expect the June quarter purchases to exceed a million shares (2% of the outstanding). It will likely continue for the balance of the year.

The Synergy

With good and bad discussed, it's appropriate to lay out the synergies. Cirrus' businesses consist of three primary growth vectors: Apple ( AAPL ), Android, mostly amplifiers and haptic devices followed by a new and budding PC business. Each of these are poised for growth after experiencing a level of weak or stagnate unit sales. A fourth vector, also aligning, controlled costs, will allow growth to directly fall to the bottom line, unhindered.

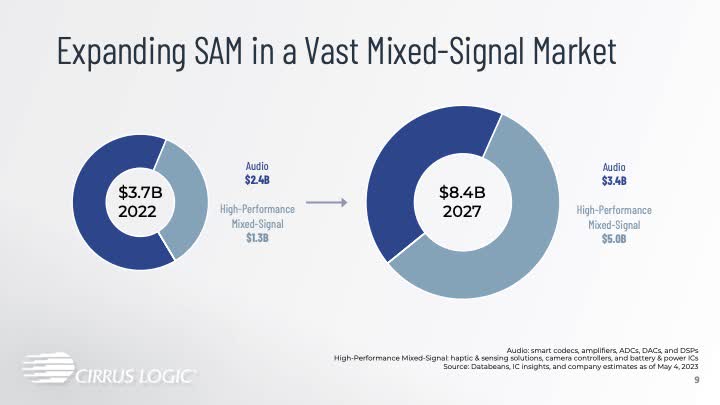

Beginning with the big picture, Cirrus always provides a SAM slide with its presentation shown next.

{kind=link}

Two observations from the past and present must be made. In the past few years, management increased the future SAM from $6.5 billion to almost $8.5 billion with the High-Performance Mixed Signal's SAM now greater than audio. Most recently, the value increased by $1 billion. Second, in the past, the company has consistently garnered approximately two-thirds of the SAM within a few years of the target. John Forsyth, Cirrus' CEO, summarized generally coming growth ,

"I think we talked about our total SAM as being about $3.4 billion, the majority of which was audio based. In 2027, we think our SAM will be around $8.4 billion and the majority of that would be in the high-performance mixed-signal space. And certainly, the high-performance mixed-signal space represents the bulk of the growth..."

From an historical overview perspective, Cirrus' revenue might grow to $5.5 billion in the 2027-2028-time frame, a 300%-fold increase.

Apple

Important details reside within a closer view. Let's start with Apple, which makes up approximately three-fourths of the total revenue. Mentioned above Cirrus lost a $1 product targeted at iPhone interfacing. But, in the Que and supplied only by Cirrus, the company is finishing the development of a new smaller nanometer codec plus new amplifiers targeted at Apple. Past management comments suggest an ASP increase for both products estimated in total at $2+. New amplifier functionality will eliminate more passive devices. The 22 nm codec will allow for major functional additions possibly including voice biometrics. Forsyth, at the Stifle Conference, stated, "So, we anticipate that shipping in the back half of next year and running on the same kind of timeline... " We expect in time an additional $400+ million with iPhone and eventually a migration over a few years into other Apple products, i.e., tablets adding approximately $100 million. In total, this upgrade likely adds $500 million.

Continuing with Apple, Cirrus' description of it headset product offering, added much detail essentially shadowing Apple's sound description for its latest product Vision Pro . The CEO described its products being with low latency, low power and high quality. A recent Apple News announcement for a new Beats product has Cirrus' technology written all over it. We don't have a crystal ball predicting unit sales for either of these, but Cirrus' content is likely huge, in the $8-$20 range, the high range for the Vision Pro with its 10 plus cameras. (Cirrus likely provides 2-4 CLCs for each Pro product camera at 40 cents apiece plus other products such as haptics, amplifiers and audio codecs.)

Cirrus always includes this statement in its shareholder letters , "Our relationship with our largest customer remains outstanding with continued strong design activity across a wide range of products." More undisclosed products are coming.

Android Intake

Next, discussing Android's increased intake was enabled with new manufacturing capacity added in the last year. This category isn't a huge adder but adds. For Android, Cirrus provides amplifier and haptic devices at ASPs of approximately $1.5-$3 per device. An analyst, a few years back, stated that the potential for amplifiers outside of Apple in smart phones was about 400 million per year or $200 million in revenue. This will add revenue possibly $100 million.

PCs - Battery Powered Laptops

Getting back to the coxswain's instructions, the big kahuna, the PC world, brings a twofold advantage, huge market size plus revenue outside of Apple. Cirrus entered this market during the chip capacity shortage era with former suppliers caught without capacity. Logic's CFO, at a recent investor conference, re-characterized its SAM upward to $1.3 billion.

Several factors are driving customers toward Cirrus products, some of which include pressures to reduce physical size and power consumption, two realms in the company's best of the best wheelhouse. To better serve the market, the company announced a new product family . Carl Albert at Cowen Technology, Media & Telecom Conference, added when answering who is driving the interest, "I would say that the major OEMs are pulling us into conversations." It isn't Cirrus trying to sell the customers.

The PC X Factor

Although PC physical size and power usage dynamics primarily drives Cirrus' strength, an additional driving force sits on the horizon, a PC X factor so to speak. A new approach with incredible new uses awaits creating for the 1st time in 50 years new power and market demand. Will Douglas Heaven from MIT Review, wrote,

"AI changes that on at least three fronts: how computers are made, how they're programmed, and how they're used. Ultimately, it will change what they are for."

AI or artificial intelligence adds "a type of [functionality] that learns how to solve a task through trial and error". The hard precise computational ability having driven the past decades, morphs into hardware working quickly on soft imprecise calculations. The need for quick access is now paramount. Hardware builders started developing this type of GPU technology in more recent time frames.

Programmers create neural networks which learn the rules for programming and then the programs program. Interaction technology with the device will change possibly eliminating the need for keyboards and mouses. What makes this whole direction different is that everything becomes a computer. Devices become a true intelligent assistant. Massive hanger-size opportunity doors open.

What Cirrus brings to the table is its expertise for small physical size, extremely low power usage and massive computational capabilities for interfacing through sound and possibly gesturing. Although, our research continually emphasizes new, powerful interfacing, in our view, this task can't fully be accomplished with one approach. Places and circumstances exist where audio or touch isn't possible. A third, suggested above, gesturing, adds to a fuller compliment. We will let our readers ponder this significance. Cirrus, either in full fashion or at an essential complement, adds state-of-the-art technology on all three of these approaches. This paradigm shift in technology isn't the primary driving force for Cirrus, as stated above, but the X factor juices the rowers maybe for a decade.

A couple of side notes seem important. From Micron's ( MU ) latest conference, " So next few months and quarters are going to be very exciting for all of our AI portfolio and the continued ramp of our business in support of the AI offerings." Second, from the Asian Investor's Micron: AI To The Rescue (Rating Upgrade) , "The size of the generative AI market, according to Precedence Research, is set to explode by a factor of 11 to $118B over the next decade, boosting the revenue potential of Micron." The enormous shift begins now.

Aligning Costs

Next, a discussion on the direction of costs follows. Under most circumstances for growing revenue, companies must hire thus increasing fixed cost. In the case of Cirrus Logic, the opposite at least for a while is in vogue. At the last conference, management cut both physical facilities overhead and set the stage for lower headcount. The reasoning makes sense with a little deeper dive. The company, stated above, lost a resource-intensive socket with Apple and is at the tail end of developing new codec/amplifier technology both of which frees up significant resource size. With this reallocation, the company also cut new hiring to levels that bleed employees though natural attrition .

The next chart from the last shareholder letter shows the significant drop in costs now in place from these changes.

Cirrus' Shareholder Letter

If the employment openings remain under 50, the number will taper off followed by lower costs. On July 12th, the company announced a small employee reduction. In the above graph, another important observation shows itself. Over the prior two-year period, Cirrus' hiring endeavor only managed to gain 200 employees at an approximate cost of $40 million a year shadowing out a meager $80 million in revenue. Clearly, costs are now labeled tailwinds for at least the next few years. We should also note that this isn't the first time Cirrus cut headcount successfully without product development disruption.

Undisclosed Products

Forsyth, again at the Stifle Conference, added,

"And so, that's a whole range of [HPMS] areas there from cameras, power, haptics, and other areas beyond that that we haven't necessarily spoken about yet, but a very significant broadening of the SAM that initially has relevance in the smartphone market."

Details aren't known, but likely explain revenue gaps missing in our above discussion.

Risk & Summary

The business is aligned with strength. Cost seems in check with still enough resources to produce new technology. The biggest risk remains collapsing unit volume sales inside of a severe recession. Yet, calculating earnings from revenue projections for a few cases seems in order. Cirrus continually repurchases stock. The number of fully diluted shares now equals 55 million lower by 4 million from a year ago is one example. With the price incredibly weak, we expect shares to be under 50 million in a year or two. In four years, it is likely nearer 45 million. Margins have been guided at 50% long-term. Taxes with the full depreciation effect of the law change likely sit long-term at 17-18%. June non-GAAP cash costs were guided at $115 million or a base level of $460 million a year. Slightly lower headcount will lower the level even more. Over the next few years, it seems that near $500 million is the maximum. Note: Our comment above concerning hiring rates. Using the 65% rule from SAM, earnings equal $40 per share. In this article, we identified approximately $2 billion in revenue to add to the appropriate $2 billion we estimated in our last article, Cirrus Logic's Crazy Revenue Signature Just Got Crazier , for the coming FY-2024. The total earnings at $4 billion might equal $30. The coxswain has the team in unison; synergy is in place. The question isn't whether; it's when. We continue our hold until the earnings date draws closer. We added options buying and selling strikes between $90-$100 a few days ago.

For further details see:

Synergy Investing: Cirrus Logic's Coming Story