TTOO - T2 Biosystems' Survival Riddle

Summary

- T2's ongoing survival is a marvel to behold.

- T2's products fill key niches but have yet to show any viable commercial appeal.

- The elephant in the room for T2 shareholders is whether it will ever participate in any upside that may reside in its intellectual property.

T2 Biosystems ( TTOO ) is a bygone favorite of mine that has bumped along on the fringes. I last discussed it in 08/2020's "COVID-19 Opportunity Knocks, T2 Answers". At the time, T2 was hoping to use interest in its rapid COVID diagnostics to place its T2Dx diagnostic device in hospitals.

T2's strategy has been successful, but at an insufficient scale to turn it around.

Placing devices is an important focus of T2's business development strategy. During T2's Q2 2022 earnings call (the "Call"), CEO Sperzel advised that its strategy was playing out as planned. It was gradually transitioning instruments that had been used for processing T2SARS-CoV-2 panels to use for sepsis testing.

As a result, T2 has been experiencing an expected decline in COVID testing.

[It] view[s] this development as a positive because it allows [it] to convert COVID-driven instruments to sepsis testing. As a reminder, [it] sold 47 T2Dx instruments to hospital microbiology labs during 2020, initially for COVID-19 testing, with the expectation that approximately 80% would convert to ... sepsis test panels over time.

Selling instruments is an important driver of revenues for T2. Once an instrument is placed, it generates ongoing revenues. During the Call Sperzel explained:

From an instrument pull-through perspective, in the United States, we achieved annualized sepsis tests utilization of $106,000 for legacy instruments. We continue to believe that annualized US sepsis test utilization will reach $200,000 per instrument and we have a number of customers that have already surpassed that target. We believe there is a significant market opportunity for our products, and we're excited to expand our presence in new and existing customers.

During the Call, he also advised that T2's installed base of instruments includes a total of 155, 94 in the US and 61 internationally. When you consider that the instrument was FDA approved in 09/2014, this is a discouraging total.

T2 has gone from troubled to extremely troubled, but somehow it keeps on ticking.

My first (11/2019) T2 article , "T2: Navigating The Danger Zone", presented a cautiously optimistic view of this company. T2 had snagged its FDA approval back in 2014 for its instrument, but was, and still is, wallowing in the danger zone as it works to commercialize its T2Dx diagnostic device.

It's hard to believe that T2, which currently (08/25/2022) trades for ~$0.13 went public in 08/2014 at ~$11.00 and subsequently traded >$20.00. Cheap does not a bargain make. T2's current down and nearly out share price reflects some very real problems that are dogging this company.

Its rapid diagnostic products are quite attractive from any patient's point of view. The problem is that T2 has yet to figure out how to market them in commercially sufficient quantities to meet its expenses, much less earn a profit. T2's long-fought efforts for commercial viability have decimated the company's shares.

It is struggling to maintain its NASDAQ listing. It currently anticipates a reverse stock split of somewhere between 1-for-10 and 1-for-50. If it would elect the 1 for 50 ratio, a shareholder who currently owns 50 shares trading at $0.13 would instead own 1 share worth $6.50; if it elects the 1 for 10 ratio, then shareholder would own 5 shares worth $1.30, still aggregating $6.50.

T2 has an outstanding debt financing, originally for $40 million, with CRG. This financing has long been a concern of mine as I discuss at length in " T2: A Catch With A Catch ". This concern is only exacerbated by T2's ongoing losses.

The CRG loan is secured by a lien on substantially all of T2's assets, including its intellectual property. The loan requires T2 to maintain a minimum cash balance of $5 million along with other covenants. It is prepayable. In its latest 10-K , T2 advises:

...[It] intend[s] to continue to evaluate options to refinance the Term Loan Agreement, which becomes due on December 30, 2023. There can be no assurances that we will be able to refinance on terms favorable or at all. The amounts involved in any such transactions, individually or in the aggregate, may be material.

Because the loan and its covenants are so important, T2 advised during the Call that it was then in compliance with all its loan covenants. As I recall from past review, this is a common bit of assurance that T2 has so far been able to provide during its quarterly earnings calls.

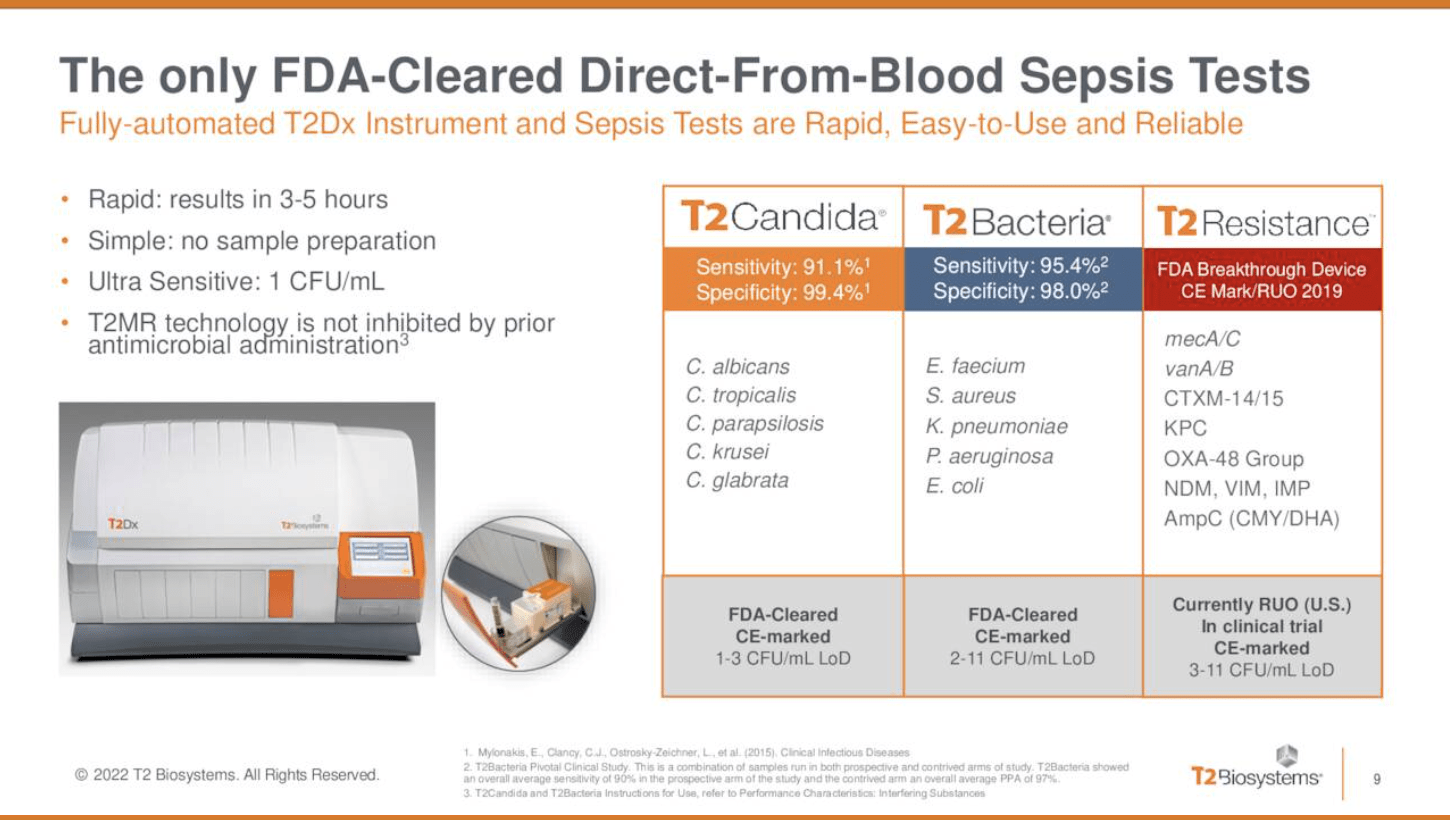

T2 has a bevy of highly attractive products which have not proven financially viable.

The issue with T2 that is especially frustrating relates to the extreme appeal of its products from a patient's point of view. Its current products are shown on its Q2 2022 presentation slide below:

{kind=link}

T2's rapid results are a godsend for patients who need to get a health screening, but who can ill afford long delays that are prevalent in the industry.

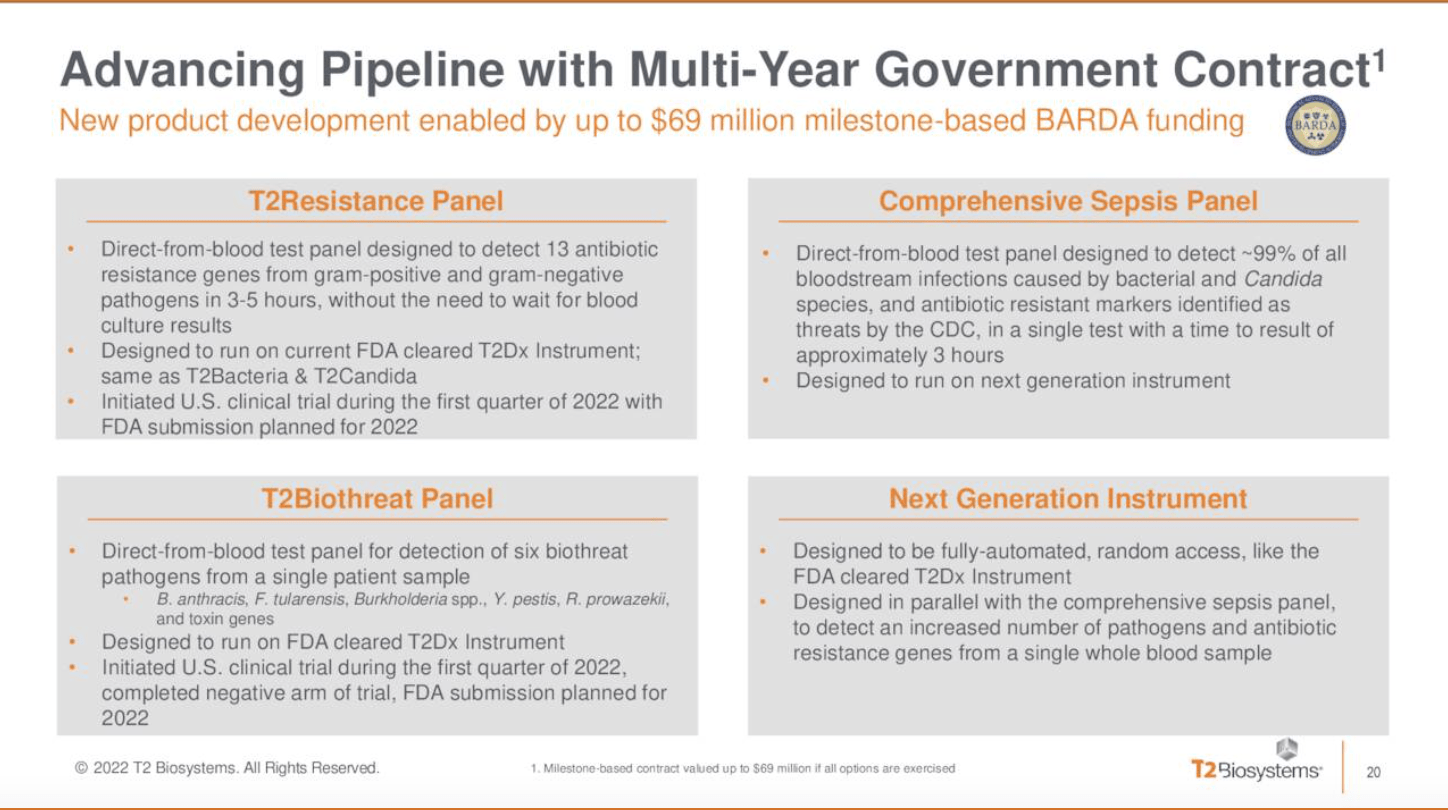

T2's vision and its pipeline are even more exciting. It is working on significant projects that could dramatically improve rapid diagnostics as shown by its slide below:

Q2 2022 earnings slide (seekingalpha.com)

{kind=link}

Additional pipeline products include its Lyme disease and its T2Cauris panels, described in its Q2 2022 earnings presentation slides 20-21. From a T2 shareholder standpoint, its technology is stirring. Its pipeline products are even better. It has proven ability to expand into new areas. Unfortunately, its technical prowess is overmatched by its ineptitude at selling its products at scale.

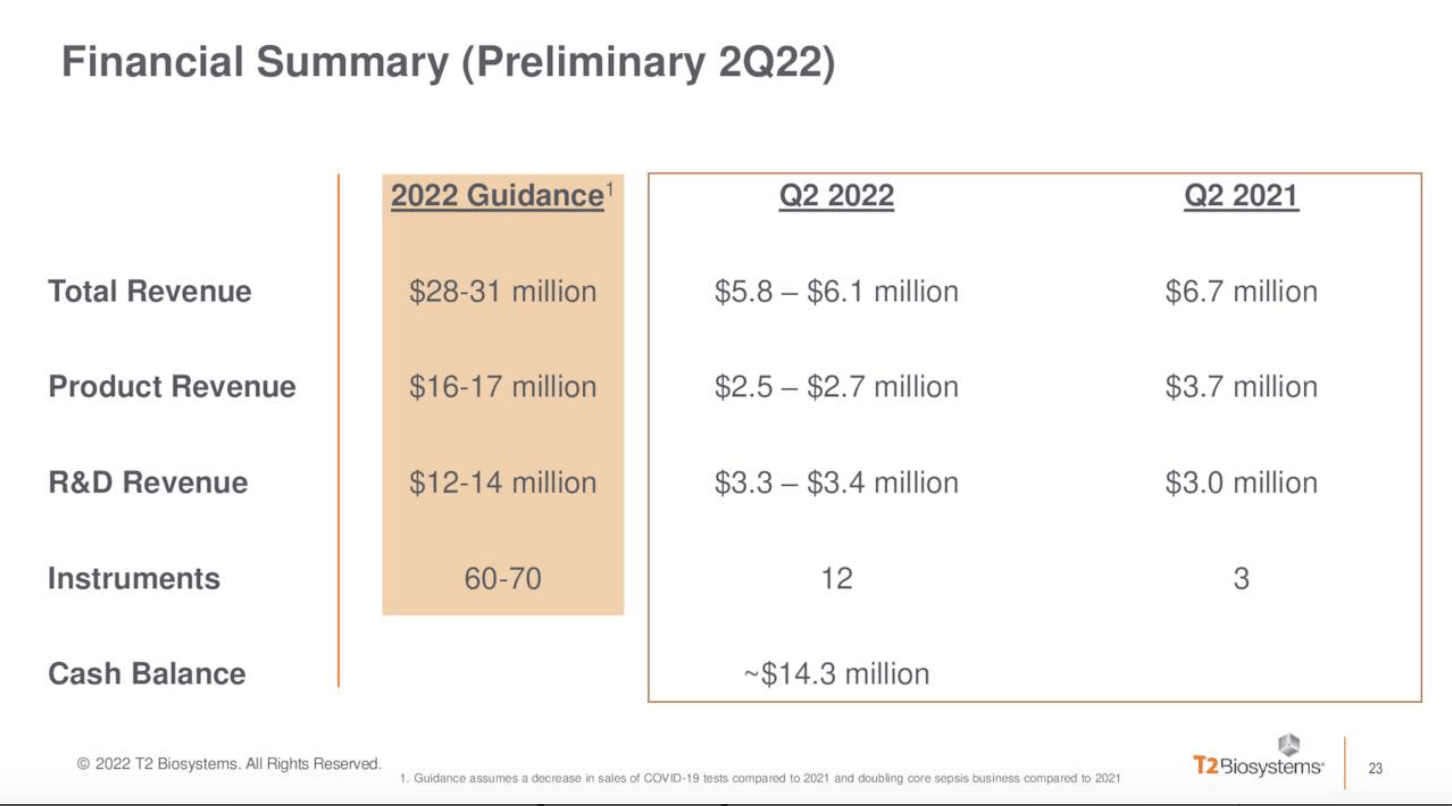

Great products and a great pipeline, but revenues are disappointing. Its Q2 2022 financial summary slide below pretty well tells half the story:

{kind=link}

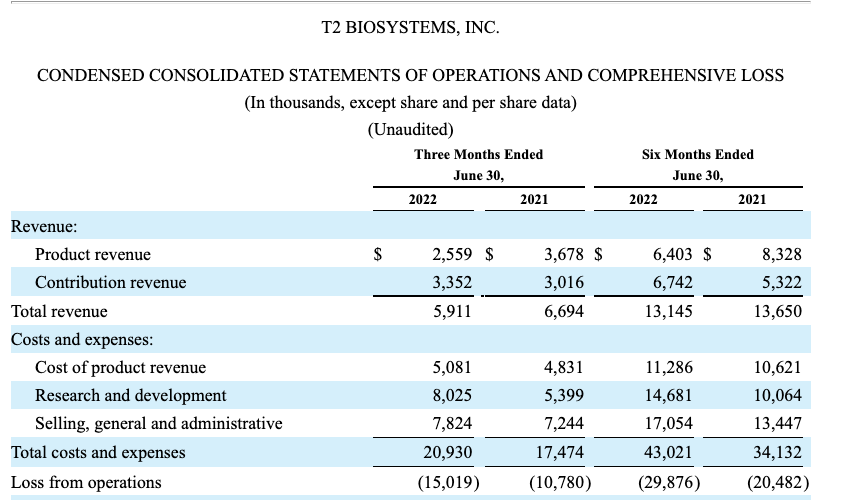

Note that this summary is hopelessly careless in one regard. It provides no input on expenses. Its Q2 2022 10-Q provides a more complete, albeit far more dismal, rounding of the situation:

{kind=link}

These latest quarterly losses are nothing new for T2. Its 2022 10-K sets out its full annual loss from operations at $49.2 million and $46.8 million for the years ended December 31, 2021 and 2020, respectively.

Conclusion

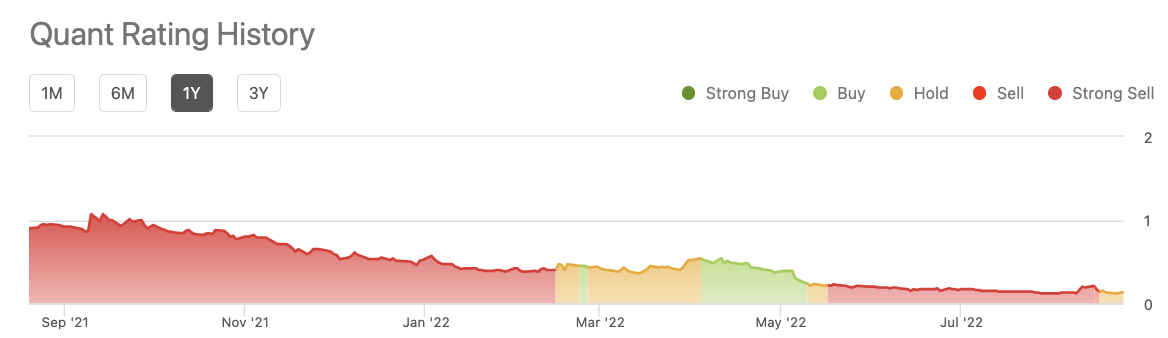

I often look to Seeking Alpha's quant ratings system for a shorthand read on a stock's underlying metrics. In T2's case, the picture has been dire over the long haul, as reflected by the one-year summary graph of its quant ratings shown below:

{kind=link}

It has gyrated back and forth; its overall reddish hue points to poor prognoses for T2's shares, even as its shares trade deeply in penny stock territory.

T2 is drenched in accumulated losses. Can it turn things around? Surely it can. However, its efforts to date have been hopelessly inadequate. Its term loan comes due at the end of 2023, a mere ~16 months from my current writing. T2's shareholders will be at particular risk until this loan is addressed in a shareholder-friendly way.

A shareholder-unfriendly refinancing would involve a refinancing which takes out the current shareholders completely. Typically, such a deal might take place as part of a prepackaged bankruptcy.

Current shareholders need to recognize that $0.13 is not an impenetrable floor for T2. It can certainly go all the way to zero, as described in a reorganization. On the plus side, the average of three Wall Street analysts have the stock at $0.20; hardly a ton of upside from a typically optimistic bunch.

I have labelled T2 a hold. I can understand those who sell out completely. There are no apparent compelling reasons to buy this hapless failure.

For further details see:

T2 Biosystems' Survival Riddle