LMT - Tailwinds For Airpower Mean Lockheed Martin Is A Buy After Q2 Earnings

2023-07-19 10:25:36 ET

Summary

- Lockheed Martin, the largest US Defense contractor, enjoys a stable revenue stream due to its separation from the economic cycle and steady US defense budgets.

- The company's work can be opaque due to its secretive nature, but the general evolution of the threat environment and warfare itself favors Lockheed's impressive airpower-focused product mix.

- The firm has a track record of delivering to shareholders and the positive secular catalysts on the demand side pair very nicely with an industry-leading capital return policy.

Lockheed Martin (LMT) is the largest US Defense contractor, and as such, it holds an exalted and protected competitive position. One attractive feature of Defense contractors is that they have primary catalysts relatively divorced from the economic cycle. This doesn't mean their primary drivers are necessarily less volatile, but they are different.

- Geopolitical environment

- Upgrade cycles in alliances like NATO

- Fortunes on the battlefield

- Changing threat environment

- Inflation

- Domestic political situation

These drivers, among many others, guide the level of the US defense budget. When the threat environment and geopolitical situation only seem like they can move in one direction, it's an excellent time to buy big Defense. The ongoing war between Ukraine and Russia, our allies' desire to upgrade their armed forces rapidly, and an increasingly urgent potential global showdown with China are three secular factors that will drive great demand for Lockheed's products in my view.

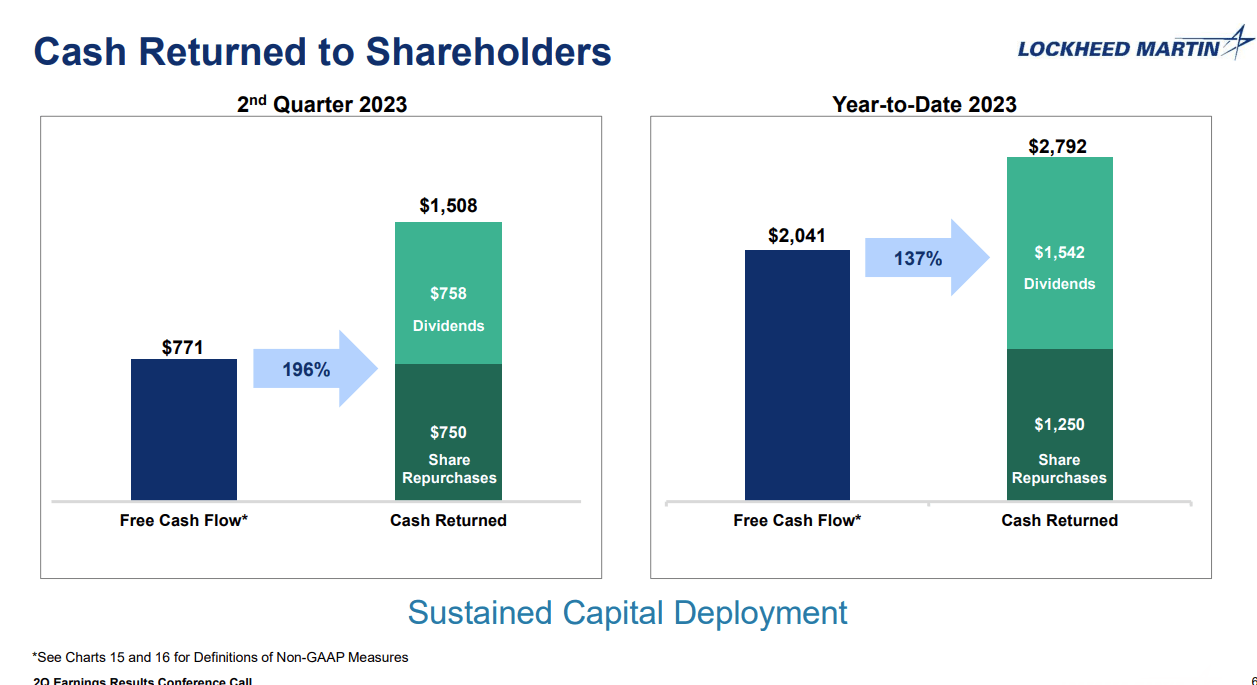

Of course, despite the incredible profit drivers, the business is very stable since its principal benefactor is the largest and most prosperous financial entity on the planet. However, management is also firmly dedicated to returning capital to shareholders, and despite not quite being a dividend aristocrat, this company should be on every significant dividend growth investor's list.

{kind=link}

The firm has a culture of innovation that harkens back to the days of the infamous "Skunkworks," it also has a lot of intangible value in coveted relationships with Uncle Sam as the nation's largest Defense Contractor.

While there were some bumbles and inefficiencies on the F-35 project, few other companies could hope to handle a project of such a prodigious scale. There was also a political genius in its meticulous planning that assures it survival. The plane was also built with the Russian military in mind .

These unique industry characteristics make large defense contractors with steady backlogs good candidates for compounding. Their dividend payments help investors achieve compounding over time, and in the case of Lockheed, the firm is currently intrinsically undervalued. I believe the steady nature of Lockheed's revenue being pared with it being intrinsically undervalued makes it an optimal time to enter the stock.

{kind=link}

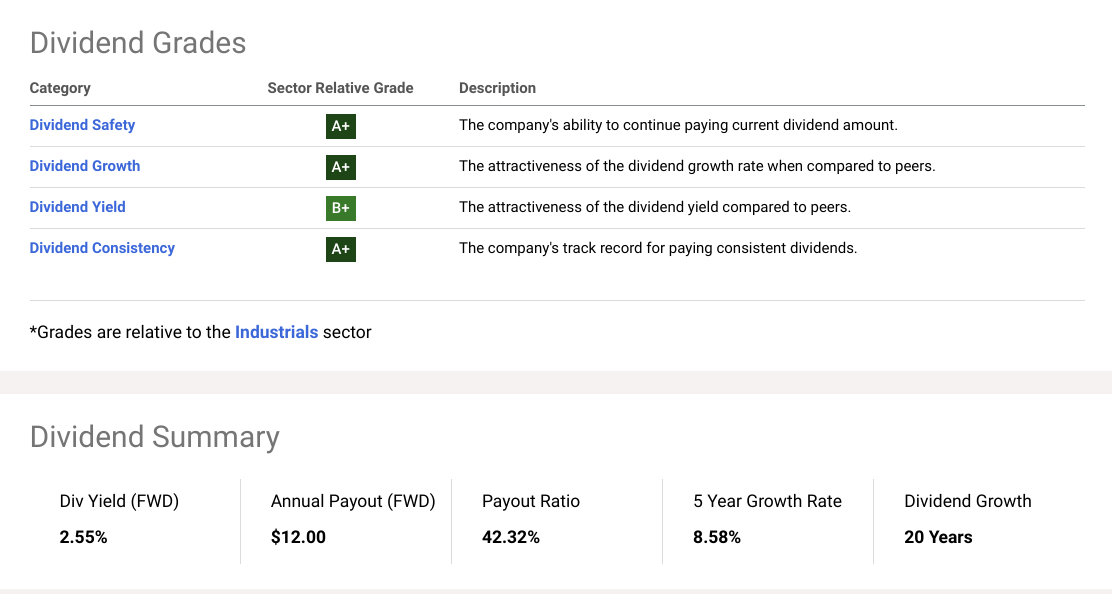

It can be easy to forget that Lockheed has a solid dividend track record and has raised dividends for twenty consecutive years. The firm's pristine financial condition and record high backlog are two reasons you can consider the dividend safe with a high prospect for further growth.

But after Lockheed's strong 2nd Quarter results, it seems that the benefits from the elevated threat environment and diminishing headwinds in areas like the supply chain have improved the risk/reward for this stalwart name. The earnings showed that the company is firing on all cylinders.

Second Quarter Earnings Were Positive

The firm reversed a prediction made earlier this year that growth would contract. It raised expectations and beat analyst expectations on both revenue and EPS. This was a strong quarter for the firm that showed notable strength across the business and a record backlog.

- Sales rose significantly, driven by the F-35, HIMARS missiles, and other missile systems.

- Lockheed rose full-year sales forecasts and now expects to earn more than it did in 2022.

- The firm beat expectations on EPS by 4.3% and revenue by 5%.

- The backlog hit a record high level of $158 billion.

- Earnings per share are expected to be 35 cents higher than expected for 2023.

There was some apprehension about an issue with the F-35 Program that might continue to delay sales. The firm must update a routine technology refresh upgrade before the US government can accept further deliveries. This could cause a shortage of aircraft deliveries that creates nearly a half billion headwind to free cash flow, which makes the quarter's strength all the more impressive.

{kind=link}

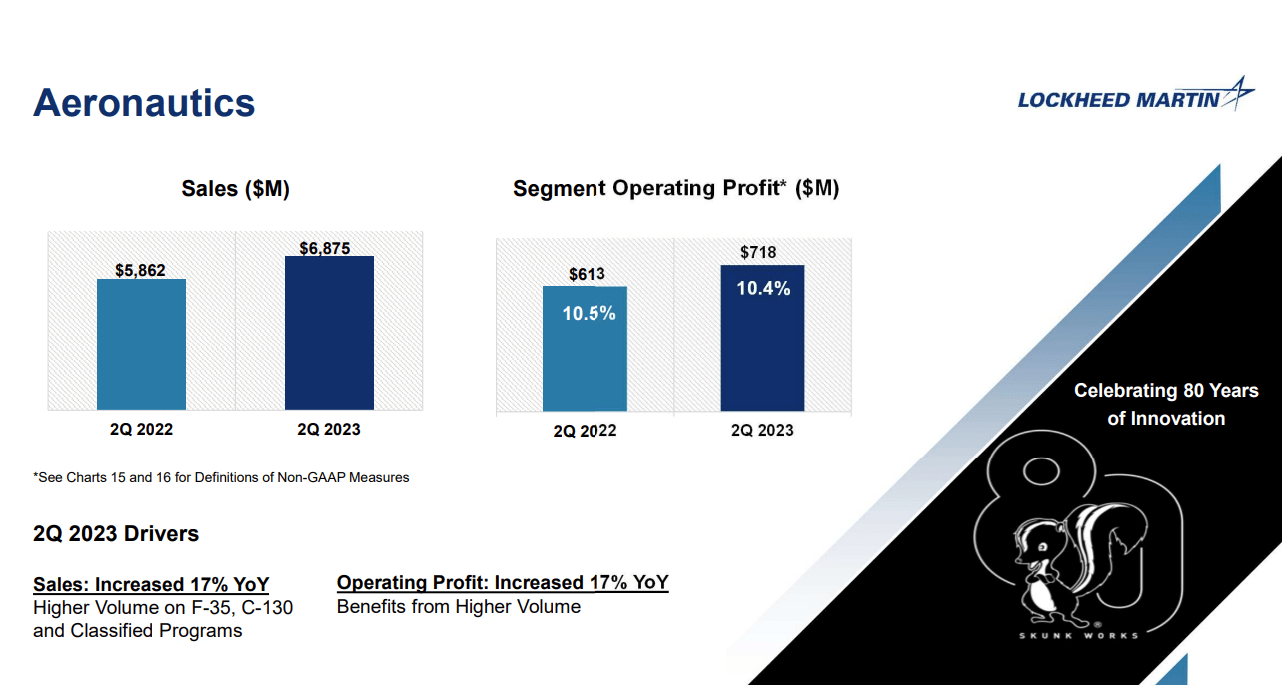

Lockheed's current weakness is also its current strength. While there are currently questions about the F-35 program that have some investors skeptical, I also think this system will outperform expectations regarding orders. If you have a long enough time horizon, delays shouldn't matter. Strength in the aeronautics department is a significant reason to continue owning this stock, as I will elaborate on in the conclusion.

Developments in Ukraine Suggest Future Airpower Purchases by Allies

The deterioration in the geopolitical landscape that has occurred since Russia's invasion of Ukraine has been somewhat favorable to US Defense contractors since it boosts demand for their wares. The early part of the conflict was defined by ground systems that checked the Russian advantage, like the Stinger and Javelin anti-tank missiles. But still, Lockheed has dominated Defense contracts involving Ukraine for a reason.

However, the conflict shows the importance of airpower and combined arms operations, a lesson not lost on NATO's eastern and Western members alike. Advanced ground systems could thwart Russia's initial invasion mainly because they didn't have advanced combined arms capability either.

The drive for F-16s will deplete the stocks of allies when they are becoming increasingly conscious of the importance of airpower. Lockheed also provides the most cutting-edge air defense missiles (PAC-3), selling like hotcakes for apparent reasons. The firm's THAAD missile defense will also likely be on many foreign purchasers' wish lists.

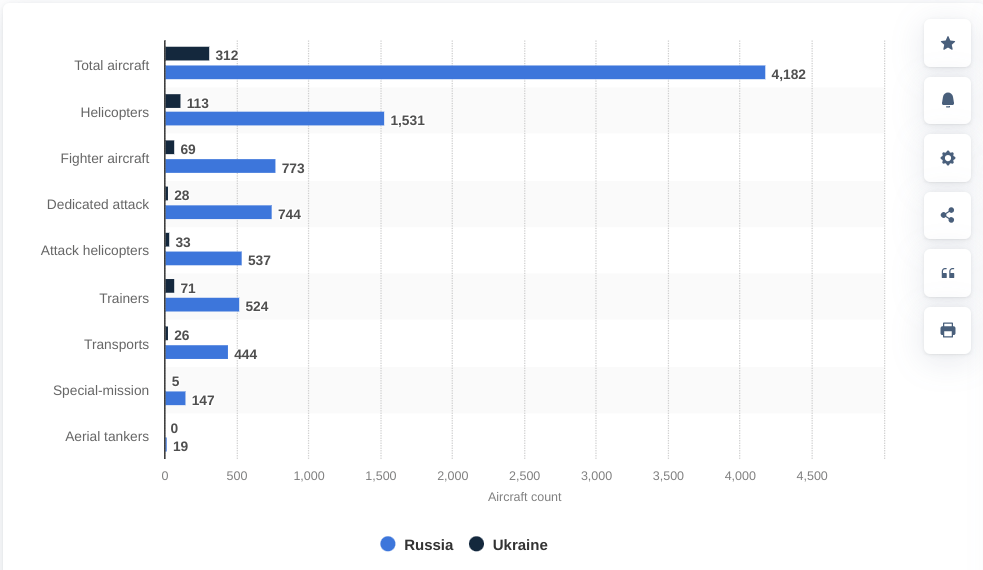

This is incredibly important for Ukraine's survival as their Russian adversary possess more than 13 times as many aircraft. The success of air defense against a brutal Russian onslaught is a better advertisement for global defense purchasers than could be contrived.

{kind=link}

So, as the Ukrainian offensive has not met initial optimistic expectations for lack of sufficient air support and the lack of an ability to achieve localized air superiority with reliability, the premium on what Lockheed Martin does best (airpower) is rising. It's likely difficult to dislodge a defensively competent military like Russia's without overwhelming airpower unless mass casualties are acceptable in my opinion.

Visual Capitalist

Another opportunity emerging for Lockheed and its peers is to boost foreign sales at the expense of their primary competitor, Russia's arms industry. For obvious reasons, Russia's arms industry is wholly inundated by sanctions and replacing combat losses. Of course, many former purchasers would prefer US weaponry after seeing the dismal performance of so many integral Russian combat systems.

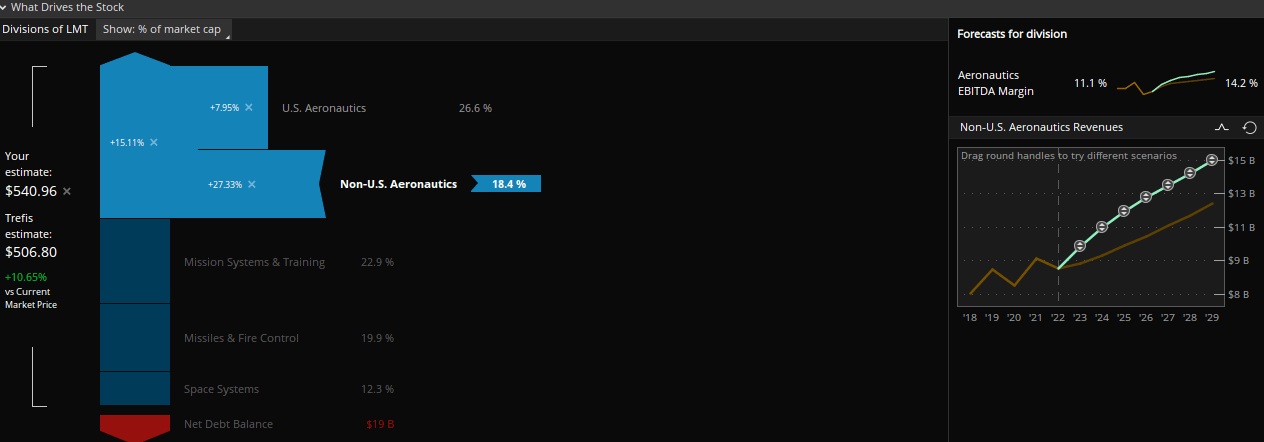

Lockheed Martin Valuation

This firm is the largest within the US Defense & Aerospace complex, which already has some very appealing competitive characteristics. Being the biggest and running crucial projects like the F-35 and having some of the essential air defense products of the future should merit a premium valuation.

{kind=link}

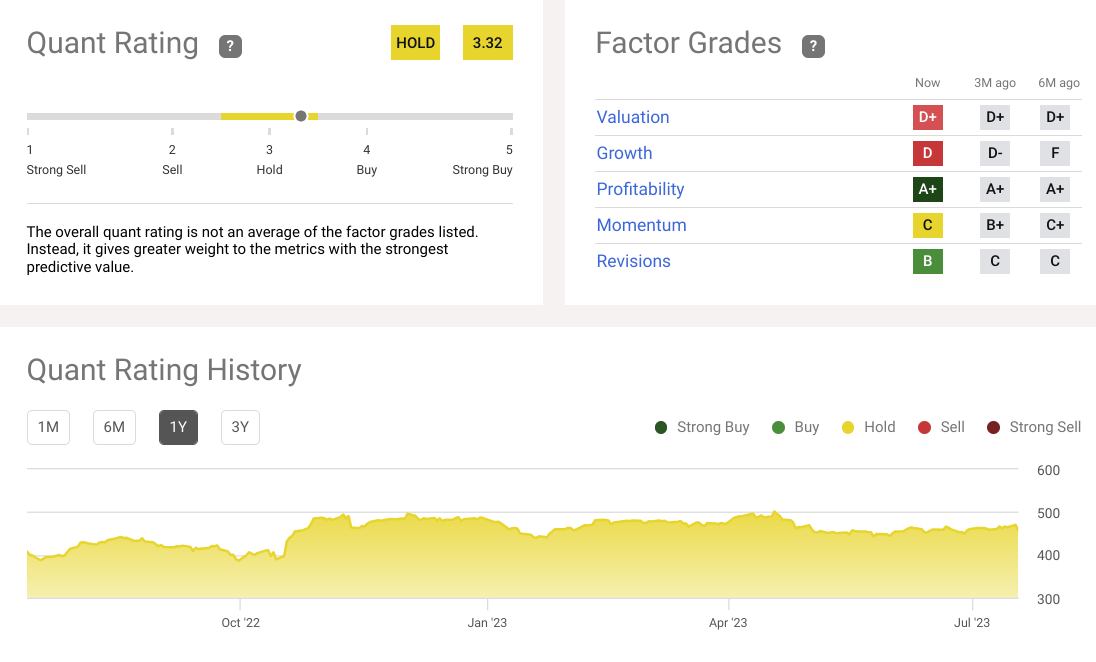

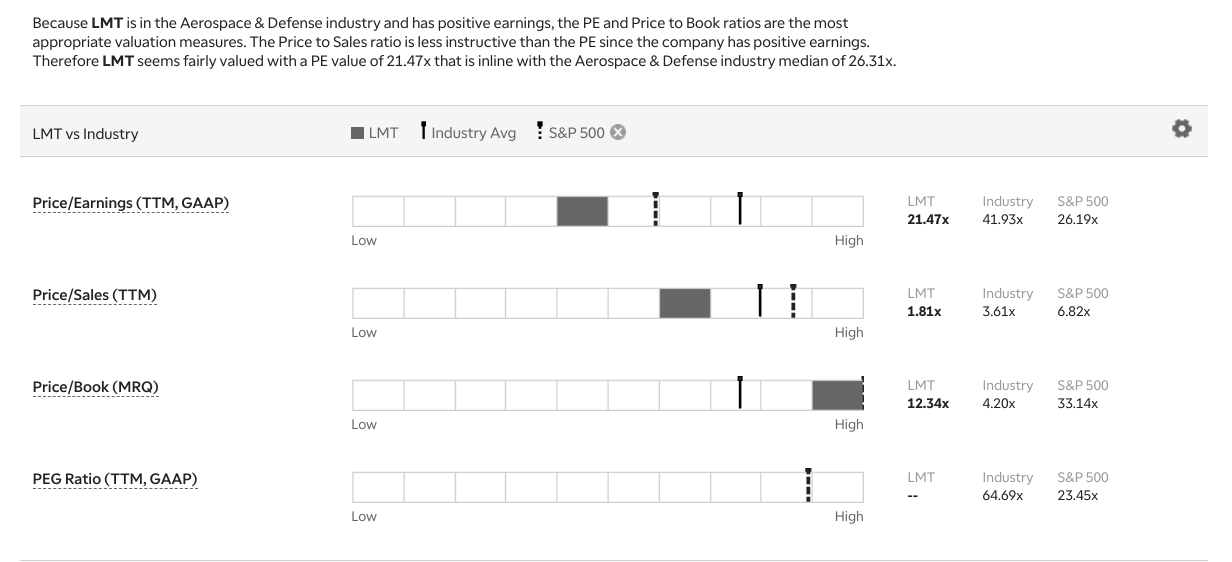

This is undoubtedly true by some measures, and you can see that the Seeking Alpha Factor Grade significantly penalizes the company for a stretched valuation. However, the company seems like a bargain at these levels based on many different methods for assessing intrinsic value. For example, when you look at Lockheed on the two metrics most relevant for peer comparison (P/E and P/S), the firm is undervalued relative to industry peers.

{kind=link}

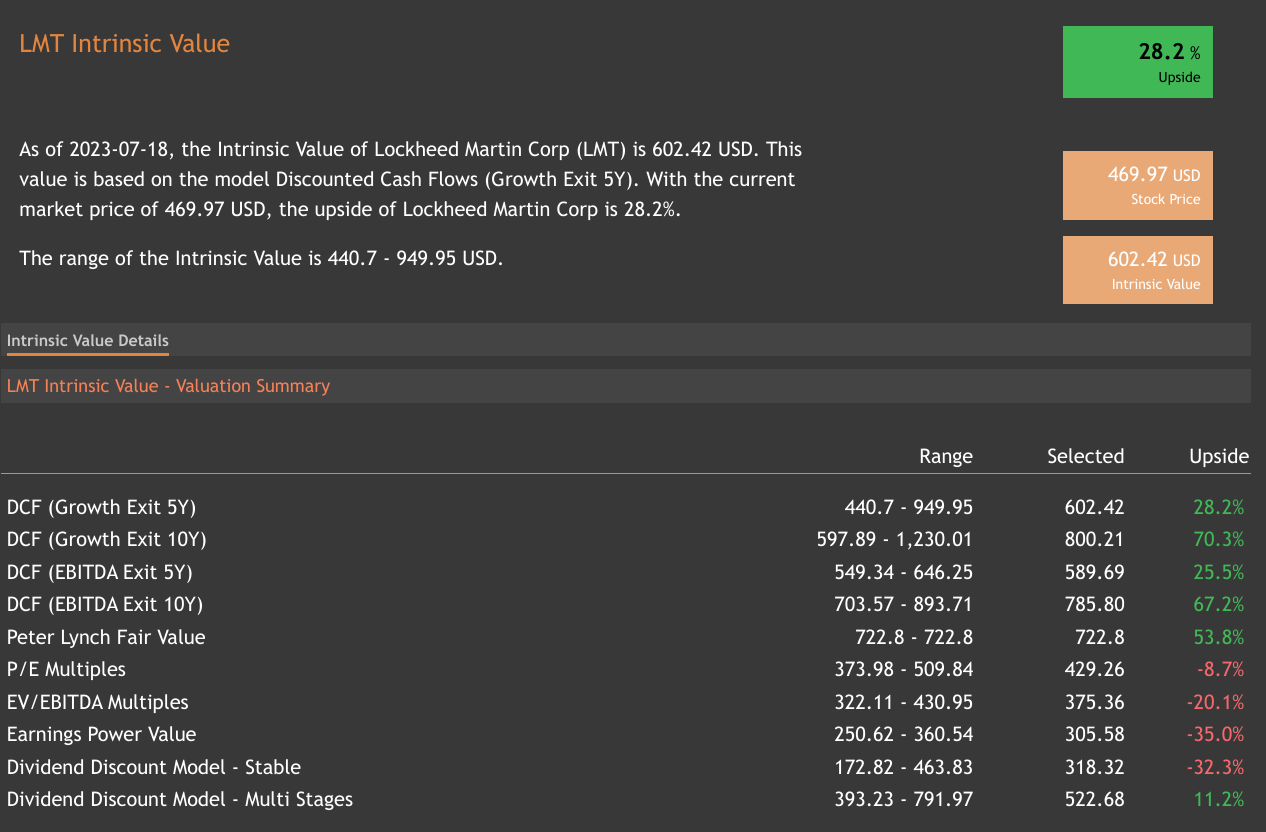

When you get to intrinsic valuation, it is a mixed picture. Still, as you can see below, most valuation methodologies show Lockheed as being significantly intrinsically undervalued. I'm a big fan of Peter Lynch's Fair Value methodology, and as you can see, it suggests a significant upside in this Defense & Aerospace leader.

{kind=link}

So, despite the natural premium valuation compared to some peers, given its size and the intangible value of being the most significant player in the US Defense Industry, the firm is still attractively valued at a time when secular drivers suggest there could be some significant upside to current earnings projections.

{kind=link}

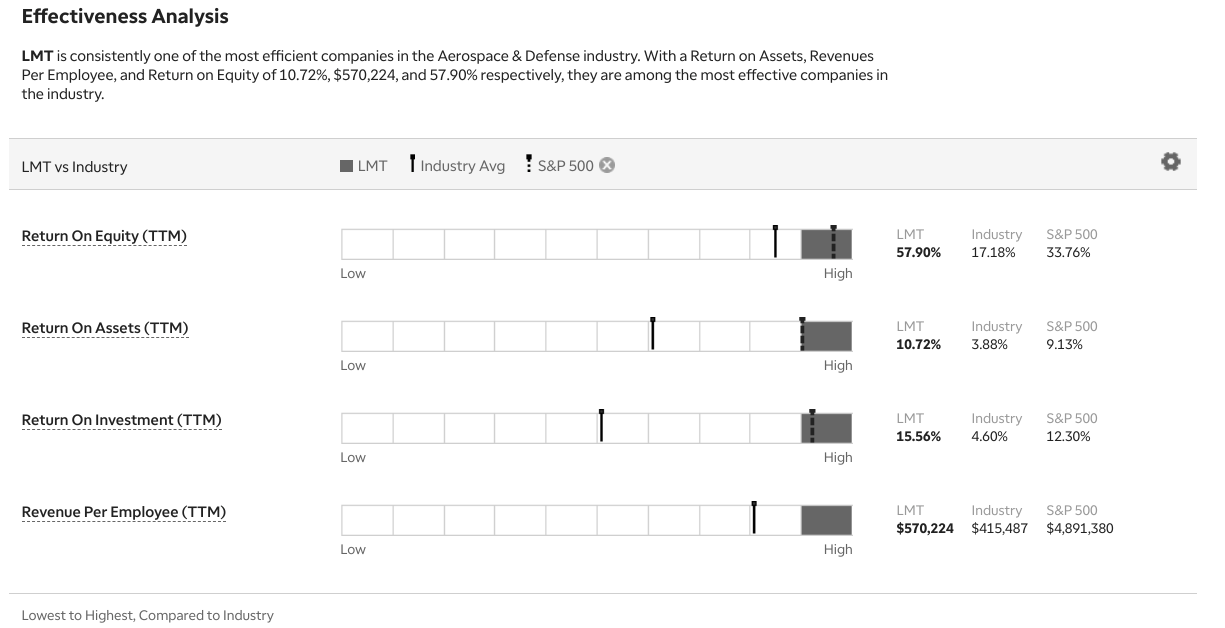

Here's the other thing about valuation. You might be a pure value investor and think that 6/10 valuation methods showing the firm is undervalued is good but not great. However, I think the case for the firm being undervalued is significantly bolstered when you consider that the firm's effectiveness with shareholder capital is significantly superior to industry peers and the wider market.

Risks and Where I Could Be Wrong

There are always plenty of risks when building some of the most complicated and controversial products on the planet. Of course, there are many tailwinds for the Defense Industry. Still, as the growing bipartisan consensus on increasing Defense spending has been positive, this consensus can also be a double-edged sword.

As the threat environment and Defense needs increase, there can also be pushback from Congress on Defense Contractors for inefficiency. As the largest Defense Contractor, Lockheed is exposed to this risk. Legislative initiatives are currently aimed at curtailing "price gouging" that could negatively affect earnings and margins. Of course, there is also a vocal minority increasingly opposed to US aid to Ukraine.

The three most persistent risk drivers to any significant Defense & Aerospace company remain the "Big Three."

- Inflation is a particularly pernicious risk for Defense contractors as the length of contracts goes many years, and contract structures can leave the producer eating costs.

- Supply chain issues are particular snags for defense contractors. Making weapons for Uncle Sam is subject to some of the most exacting standards on Earth, so labor interruption in minor components can cause massive delays.

- Labor is also a massive consideration for Defense. Given the security clearances needed and specialization needed to work on covert projects, the demographic changes in the labor force can make filling the place of retirees or dealing with labor issues, particularly problematic.

The current concerns about the F-35 program should not concern investors who plan to own this stock for at least three years, which is the time horizon I would recommend. The nature of how defense revenue is realized means that the benefits of current spending increases will show up in earnings in a couple of years. However, the company's revenues are concentrated in the F-35 program so that any program setbacks could be a significant negative for the share price.

A final risk has to do with the increasing debt obligation of the United States government. As the most significant part of discretionary spending, the Defense Budget may become too juicy a target for cuts if the financial condition of the United States government declines significantly.

Conclusion: Airpower Premium

Lockheed Martin is a leader in the US Defense Industry. Aside from being intrinsically undervalued along many metrics, the company enjoys the benefits of a generational increase in demand for many of its core products. The bloody stalemate in Ukraine highlights the importance of advanced airpower capability in a military engaged in a high-intensity conflict. This increasing focus and attractiveness of offensive and defensive airpower options will likely continue to benefit.

Lockheed gets a significant portion of its revenue from aeronautics and profitability tends to increase with volumes despite the bespoke nature of the product. The increased interest in the F-16 and its imminent deployment to Ukraine, where it will likely have a significant effect given the performance of Russia's air force, will only increase international interest in bulking up in airpower in my view.

{kind=link}

As you can see, when making more generous assumptions to domestic and international aeronautics, the intrinsic value of the stock increases significantly. Not only is it a safe assumption that defense spending will increase in real terms over the next decade, but it doesn't even have to increase significantly in terms of proportional GDP for the defense companies to majorly benefit.

Most of the militaries in the western world have become leaner volunteer based organizations that aren't subject to the "cost disease" that occurs in labor intensive industries like healthcare. Instead a lot of the technological trends, including Lockheed's vital Mission Systems segment, is reducing the need for personnel by using automation and other efficiencies

NATO and the US spend relatively meager amounts on labor increases, and the shortfalls in military spending aren't going to be filled by drafting more recruits, they'll be filled by buying more equipment and nothing is more desirable for the ramshackle state of much of our allies armed forces than premier air assets, offensive and defensive.

The F-35 program constitutes a significant portion of the company's revenue, and the new spirit injected into the NATO alliance bodes well for purchases of this product exceeding current projections. Of course, air defense products are being proven more essential and effective than any advertisement could convey daily.

{kind=link}

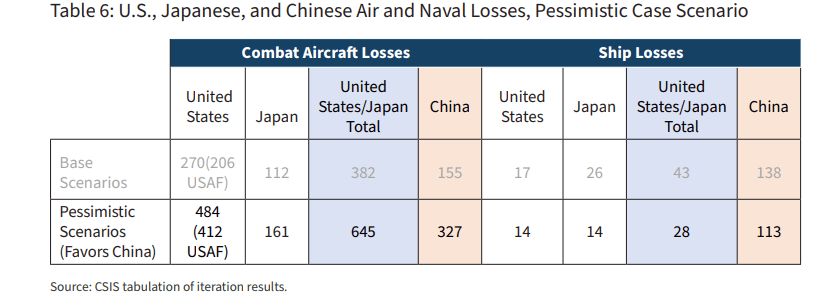

The Center for Strategic International Studies recently conducted a wargame exercise simulating a Chinese Invasion of Taiwan. While the United States is able to come out on top in most scenarios and Taiwan remains an independent country, such an outcome is attained at an incomprehensible cost in blood and cutting edge equipment. You might find it hard to believe, of all the things the dollar can buy less of since the 1980s, airpower isn't one of them.

The basic conclusion from the war game, and from the current fighting in Ukraine, is that there is a massive premium on having modern combat aircraft and the highly trained crews necessary to attain air superiority. The US will need more aircraft and missiles, and air defense like THAAD, going forward. Furthermore, what has been proven even more essential is that air defense can be the difference between life and death. I believe these realizations firmly favor Lockheed Martin's current and future weapons platforms.

For further details see:

Tailwinds For Airpower Mean Lockheed Martin Is A Buy After Q2 Earnings