CA - Tamarack Valley Energy: A Narrower WCS Discount On The Horizon

2023-05-16 07:00:00 ET

Summary

- Tamarack Valley Energy Ltd. is misunderstood by the market and deserves to trade at higher than current levels.

- At WTI $70 and above, Tamarack Valley Energy is positioned to be a cash flow monster with long-life, low-cost wells.

- A number of the headwinds for Q1 are set to decline, putting more money on the company's bottom line.

- We think Tamarack Valley Energy is attractively priced for new investors and those wishing to add at lower levels for growth and income.

Introduction

Tamarack Valley Energy Ltd. ( OTCPK:TNEYF ) reported its Q1 earnings the other day. Consistent with other energy producers, the market looked past a so-so Q1 report to focus solely on the negatives - lower production than forecast, a revenue miss, and uncertain guidance for the rest of the year. It's like we entered a time-warp and are back in Q2 2020. That turned out to be a great entry point for everything energy, and we could be headed there again.

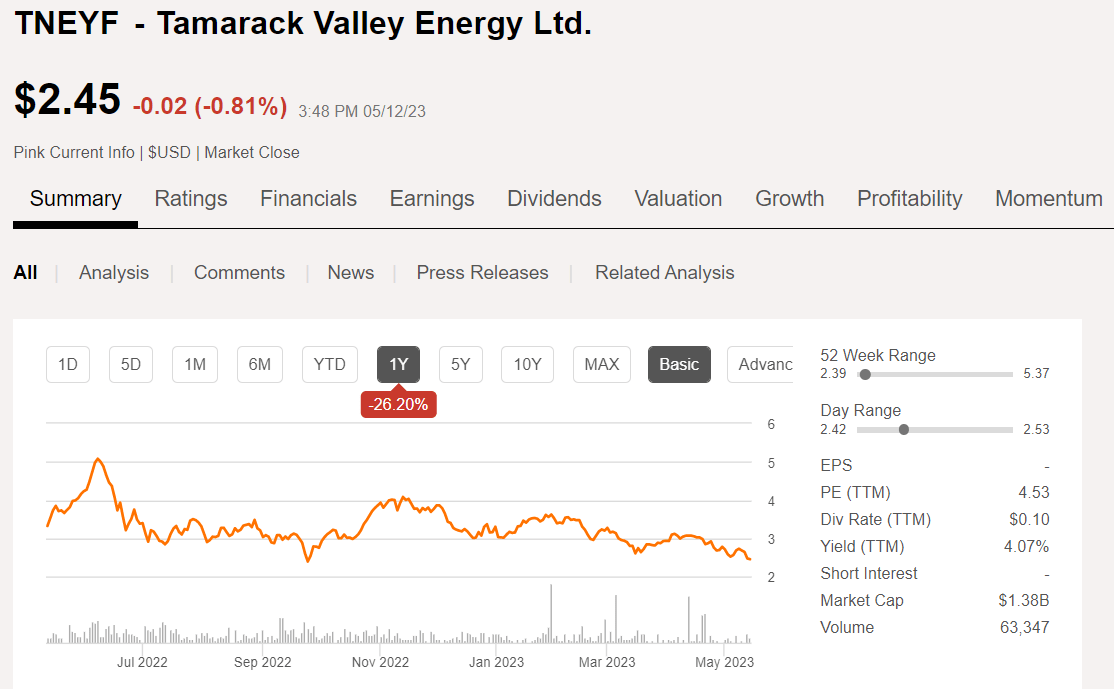

Tamarack Valley Energy Price chart (Seeking Alpha)

{kind=link}

Since my last, admittedly "bullish" article on the company, TVE stock is down 30%. Conditions are changing, though, and that could be good for the company.

In this review we will recap how the company did in Q-1, and see how we feel about TVE at current levels. Let's take a quick look at the macro picture for Canadian E&P's in the year ahead, first.

The macro picture

I will admit to having been caught off-guard by the unrelenting pessimism that has surrounded the upstream energy sector for the last six months. The culprits are of course, the collapse in oil prices since December, and the absolute rout in gas prices. Even the short-term uplift provided by the OPEC+ announcement of a 2 mm BOPD cut, has withered due to fears about an economic slowdown and, more recently, fears about the banking sector. On the encouraging side, we have seen quite a drawdown in crude stocks since the first of the year, a point which under-pins every bullish thesis I've run across for crude .

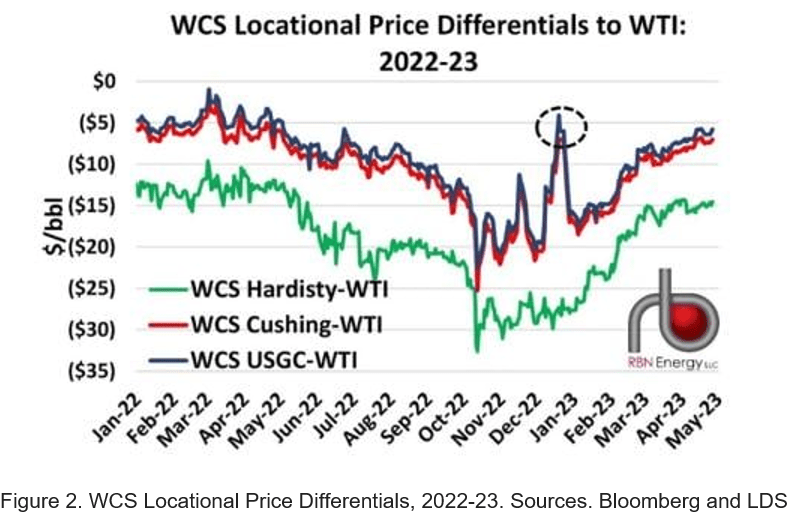

Ok, let's leave that for a minute. The Canadian E&P's have had a few extra monkeys on their back for the last half year or so. There is lack of pipeline export access, due in part to TC Energy's Keystone pipeline break , the massive U.S. SPR releases that competed with WCS, and the gross WCS discount to WTI-averaging over $20 per barrel , with some location differences as the RBN Energy graphic shows below, since late last year. And, finally, there was a BP refinery fire in Ohio that made a lot of Canadian crude homeless.

RBN Energy WCS Discount chart (RBN Energy)

{kind=link}

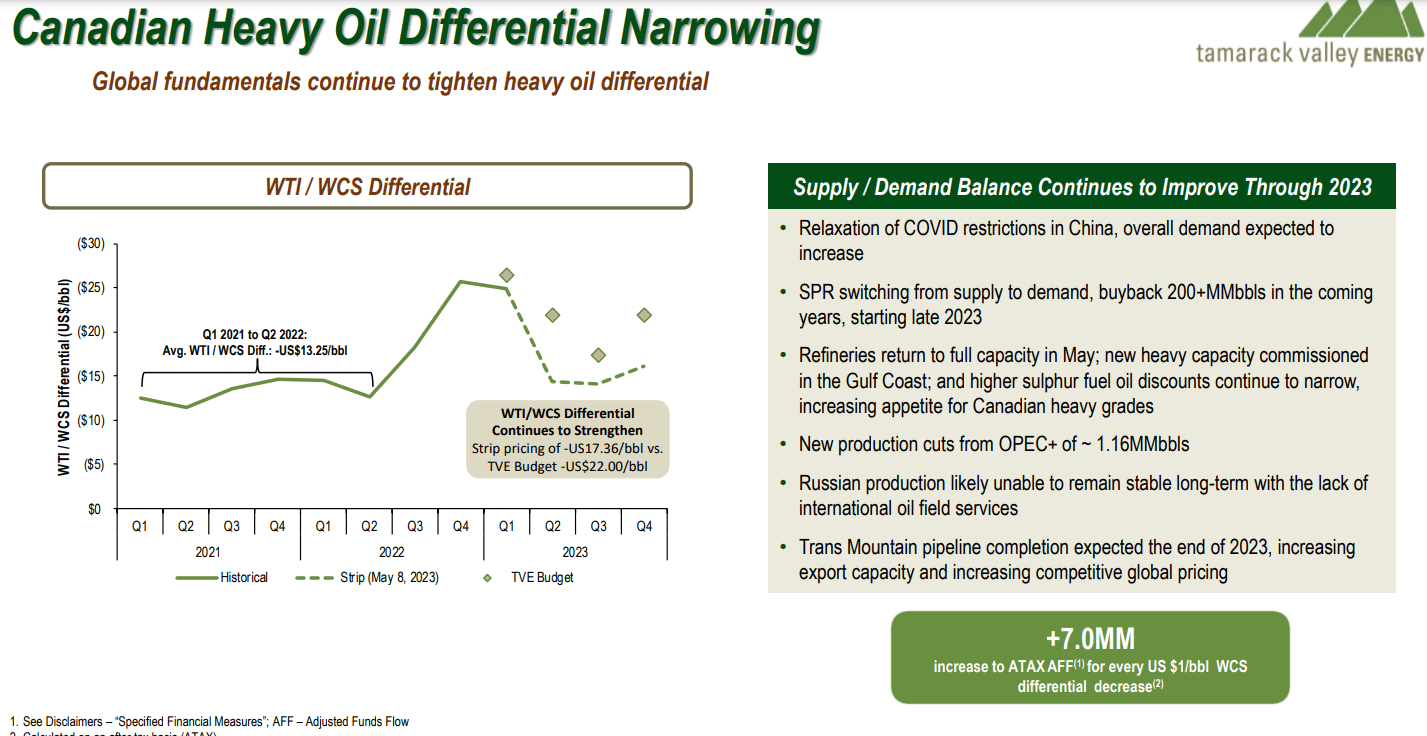

RBN goes on to note that with two of the demand killers for WCS taken out of the equation (SPR releases, and the Keystone pipeline back on line), WCS at the Hardisty hub should begin to trade more in line with WCS-Cushing, and WCS-USGC. That would narrow the discount probably toward $10 bbl, and put a lot more money in producers pockets. TVE discusses this in the slide below.

TVE chart of WCS Discount (TVE)

{kind=link}

Bottomline: things should begin to improve for Canadian exports, and for Canadian producers.

The Tamarack story

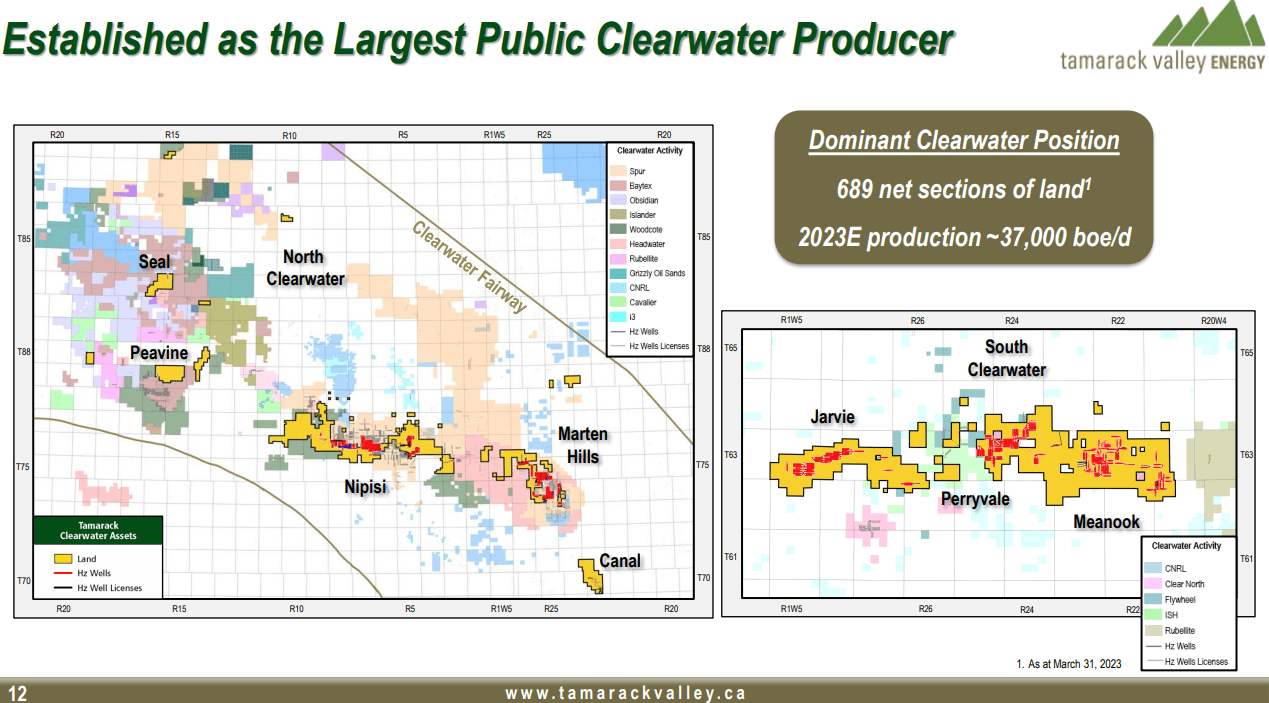

The Tamarack story has changed a good bit in recent years with acquisitions bringing new acreage in areas diverse from the Cardium play that forms their legacy. Last year they made a hail Mary, $1.1 bn of DeltaStream Energy , targeting that company's Clearwater acreage, and emerging as the largest acreage holder in that play. Much of it in the hot Nipisi, and Marten Hills areas. You've heard this all before, but it bears repeating the Clearwater has been called the most exciting play in North America, due to its high sandstone permeability, and low gravity crude that flows without steam injection, and lends itself well to waterflood for secondary recovery. DeltaStream brought 23K BOPD of production with it, so is well on the way to paying out its acquisition cost in about a year and a half. With the focus on its high oil-cut production, the company should be back on track for growth for the rest of 2023.

TVE footprint in the Clearwater (TVE)

{kind=link}

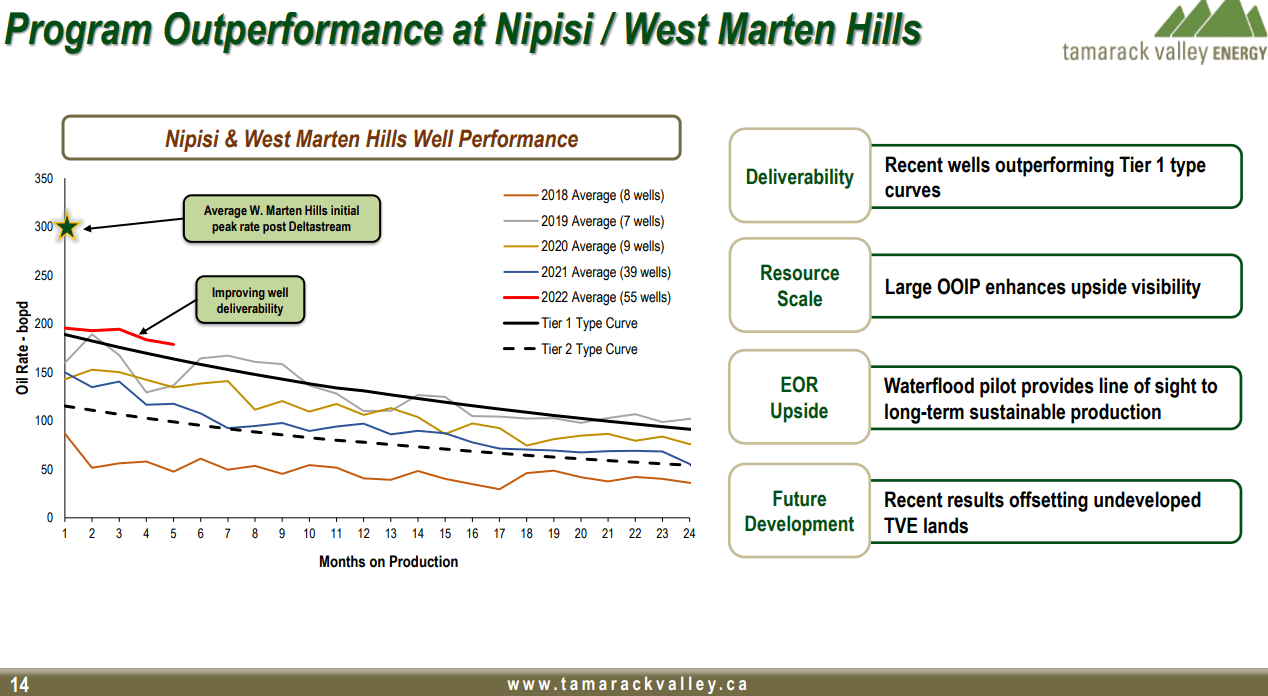

If you note the slide below, the performance curve has been trending toward high tier shale performance. This trend has continued in 2023, with IP30 rates of 300 bopd at West Marten Hills as the Company continues to delineate the pool and target areas with favorable viscosity. Building on results in this area, Tamarack plans to drill an additional 22 wells in the second half of 2023. The company is also experiencing strong results at Charlie Lake, where a total of 19 wells will be drilled in 2023. IP-30 rates of over 700 BOEPD have been seen, with a 60% oil cut and a EUR performance curve of 180K over 12 months.

TVE chart on Nipisi performance (TVE)

{kind=link}

Exploration/Delineation Update

A waterflood pilot is planned for Saddle Hills in Q4 2023. This project will capitalize on existing development well spacing that is conducive to successful multistage frac waterflood. Successful pilot results would have material impacts across the Charlie Lake fairway asset base with the long-term potential to tie production into the Wembley facility.

Tamarack continues to drive further inventory expansion through both the Seal Clearwater exploration results and their continued success on the West Nipisi Joint Venture. At Seal, the Company drilled and tested three separate Clearwater equivalent sands off one pad. Total production from the three wells on a peak IP30 basis is approximately 380 bopd. The lowermost sand was drilled with only three legs to test the commerciality of the sand, whereas the middle and upper sands were developed with 6-leg multilaterals and laterals approximately 1.25 miles in length.

Owing to the strong results, Tamarack will advance to full development on these lands. Given the multiple zones, management expects development at Seal to drive strong capital efficiencies and economics with large-scale multi-well pads pushing lateral lengths to 1.5 miles. Anticipated development would result in pad costs of approximately $34 to $40 million and production rates of 2,200 - 3,000 bopd per pad. At Seal, Tamarack owns 17 net sections with multizone potential and has a farm-in on 7 additional sections to accommodate future delineation.

Source .

Q1 2023 and full year guidance

For Q1 2023 , the company noted average 67,938 boe/d, representing a 64% year-over-year increase and a 6% increase over the fourth quarter of 2022. Production through January and February averaged over 68,800 boe/d. The TC energy outage caused an underlift of about 1,000 bopd from earlier estimates.

Adjusted funds flow, or AFF, came to $157.3 million, slightly below the $166.8 mm for Q-4, 2022, and free funds flow of $9.1 million in the first quarter reflected the production impact of the unplanned third-party outages and a wider year-over-year WCS differential. The capital budget of $425-475 mm is intended to deliver 67-71K BOEPD of production in 2023. Flat to slightly higher, and quite a bit below my earlier YE 2023 close out of 75K BOEPD. The company cites dispositions and the pipeline downtime for about 1,500 BOEPD of this underlift.

The base dividend is currently $0.15/share annually which represents a 4.3% yield at the current share price, and is not likely to be raised pending debt reduction. Debt repayment remains the immediate focus to achieve the enhanced return of capital thresholds whereby the Company will return from 25% up to 75% of excess funds flow on a quarterly basis.

Your takeaway

The combination of a lower WTI price in the low $70's and a doubling of the WCS discount drove Tamarack Valley Energy Ltd. cash flow to a one year low, but still 60% above March of 2022. So, we can count our blessings for small favors.

On a TTM basis, Tamarack is trading at 3X EV/EBITDA, and $30,400 per flowing barrel. Neither of these are excessive for a company that will furnish the steady income stream Tamarack will. Narrowing the WCS discount will add $251 mm of EBITDA to the balance sheet -nearly a 50% increase, so it will be very significant... if it happens. In that scenario, to keep that same multiple, Tamarack Valley Energy Ltd. shares will need to move toward $5.00 per share, a 2-bagger from current levels.

For further details see:

Tamarack Valley Energy: A Narrower WCS Discount On The Horizon