CA - TC Energy: A High Yield And Growing Dividend Pipeline Play

2023-08-16 06:21:31 ET

Summary

- TC Energy has experienced a significant drop in share price, which has made it look incredibly cheap.

- The company is undergoing changes, including sales and a split into two separate entities.

- Despite the challenges, TC Energy is expected to see growth in EBITDA and dividends, making it an attractive investment opportunity.

Written by Nick Ackerman.

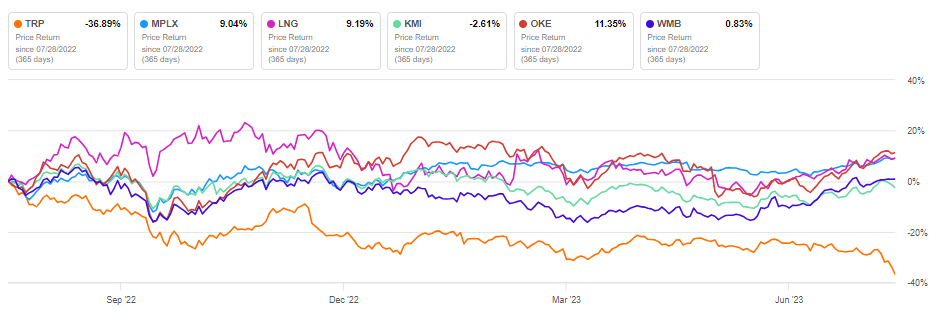

TC Energy Corp. ( TRP ) has certainly been struggling lately with a significant drop in their share price. In fact, it hasn't only been a recent struggle but more in the last year, as shares are down nearly 37% as of writing. This is a company that has made an appearance on our monthly screening dividend-growth articles a number of times. It's also a sizeable Canadian pipeline player, so it's a name I've had on my radar off and on but not really on my watchlist.

Lots of Moving Parts

Of course, it goes without saying that there are a lot of moving parts in this case. The valuation drop has factored some of that in, but there are a lot of unknowns. They recently sold a 40% interest in their Columbia Gas Transmission and Columbia Gulf Transmission pipelines to Global Infrastructure Partners. The next day that pipeline had a fire erupt.

With their earnings, they announced their intent to split off into two different companies. One is the liquids pipeline business, and then the other will focus on natural gas and "alternative energy opportunities including nuclear and upped hydro energy storage." The latter is primarily the largest part of their business and the fastest in terms of expected growth going forward.

{kind=link}

Finally, the price of natural gas and oil has been under significant pressure. Pipelines work primarily with fixed-rate contracts, which can dampen the volatility of their earnings, but lower commodity prices tend to pressure the share prices of the companies regardless.

Looking Cheap

Given the attractive valuation we are currently seeing, I believe it's worth giving some further attention to and initiating a position. The drop in the last year for TRP has been significant relative to peers.

{kind=link}

The price itself is going back to near Covid levels.

Ycharts

In terms of the EV/EBITDA multiple, we are seeing a similar valuation of when it dropped during Covid as well.

{kind=link}

A lower price on its own doesn't tell us if something is cheap. Additionally, something can be cheap relative to its history, but it's because going forward, things are expected to turn out worse.

In this case, going forward, EBITDA is still expected to continue to rise despite all the moving parts we touched on above. That would mean the forward EV/EBITDA ratio would be even lower at closer to 10.5. This year they expected comparable EBITDA to rise 5 to 7% as the combined company.

TRP Comparable EBITDA (TC Energy)

Growth in comparable EBITDA isn't anything new for this company, as it's been delivering earnings growth over time through many different events.

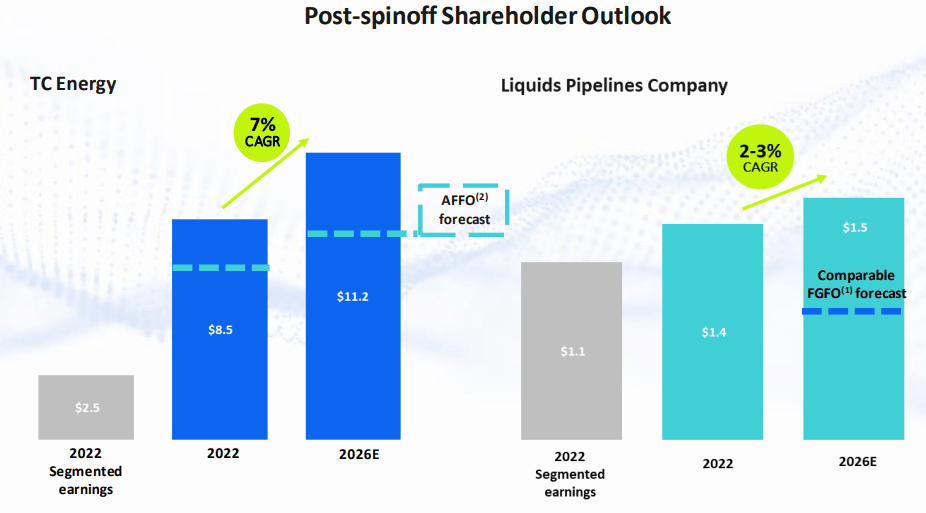

After their spin-off of the liquids business, they actually anticipate comparable EBITDA growth to accelerate for their natural gas/alternative energy business that's left over. They noted this in their earnings call .

At close of the spin-off transaction we expect that 96% of our adjusted EBITDA will be either rate regulated or long-term contracts. Post transaction, our 2022 comparable EBITDA is expected to grow at a 7% compound annual growth rate through 2026.

Of course, the liquids business isn't going to be worthless on its own but will see comparable EBITDA at CAGR closer to 2-3%. In the first half of 2023, they saw the liquids pipeline comparable business rise 6%. So this could be a conservative figure as well. Post-spinoff, what's left of TC Energy is expected to grow a bit faster at nearly 7%.

{kind=link}

TRP has a long history of growing its dividend. They also expect that the liquids business will grow its dividend by 2-3%, in line with its comparable EBITDA growth.

Despite slower expected growth in the dividend going forward of 3-5%, the current yield is quite elevated, which compensates for some of the anticipated slower growth. Again, this could be some conservative guidance so that they can surprise the upside. Since 2000, the dividend has been increasing at a 7% CAGR.

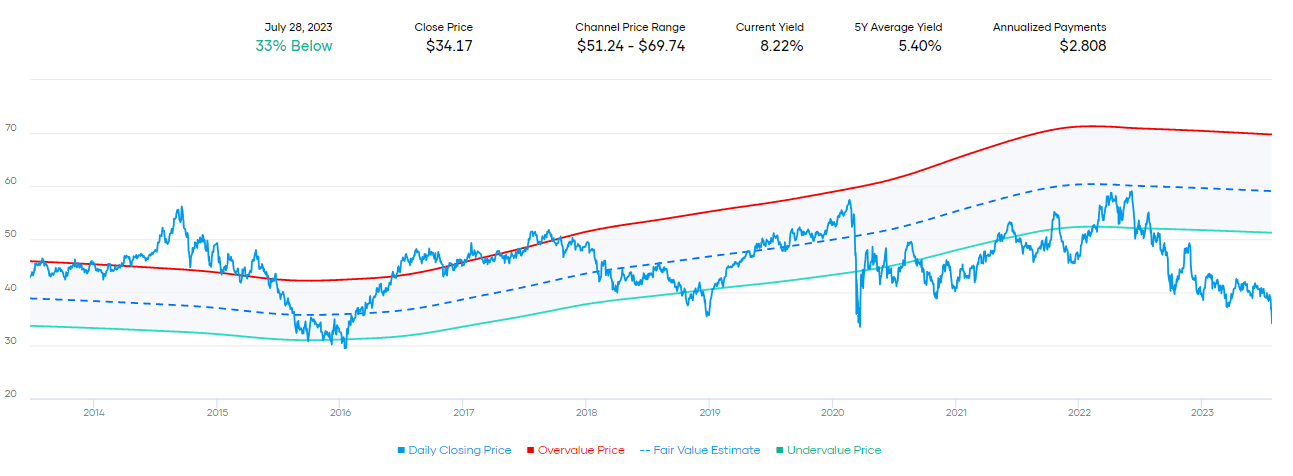

In terms of its current dividend yield, it's well below the historical average, and this is another way to value the company currently and highlight just how cheap this stock is looking currently.

{kind=link}

Depending on where you look at the dividend chart, it could give an investor some pause as it would seem like a variable payout. However, this is generally due to the CAD to USD conversion. This is a Canadian company that pays in CAD, and when looking at the CAD chart, we see a smooth consistency over the years of trending growth.

TRP Dividend History (TC Energy)

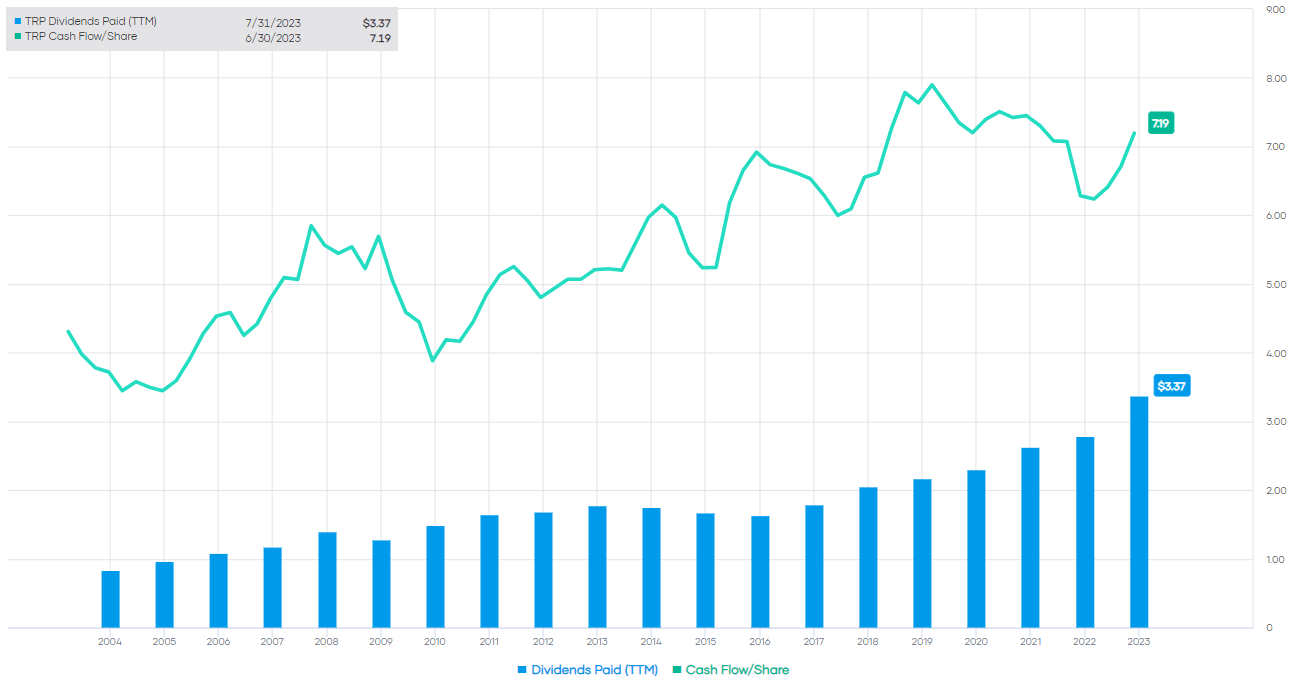

This dividend appears to be well covered through cash flows the company can generate as well. As we noted, earnings have been growing, and operating cash flow has followed a similar rising trend.

{kind=link}

However, when factoring in capital spending, the company has continued to spend more than the cash flows coming in. That's why debt and share offerings have also been coming in to fund new projects. As an example, last year , the company had cash from operations of $6.375 billion but had a Capex of $8.961 billion. More recently, the first half of 2023 saw the company bring in a cash flow of $3.584 billion but spent $6.024 billion.

That being said, only around $0.9 billion was maintenance Capex. That's the spending that is recurring, with the other Capex being projects that they could theoretically stop spending or that are going to produce future earnings growth.

During the six months ended June 30, 2023, we placed approximately $2.1 billion of Canadian natural gas, U.S. natural gas as well as liquids pipeline capacity capital projects into service. In addition, approximately $0.9 billion of maintenance capital expenditures were incurred.

Conclusion

TRP is looking quite cheap and could be providing a time to enter this name. I'm unsure if I'm going to end up holding TRP over the long term. However, I will enjoy the added income that this company will provide with its generous and growing dividend yield. In terms of other energy exposure, I carry positions in Enterprise Products Partners ( EPD ) and Chevron ( CVX ). I also hold a position in the small natural gas pipeline player DT Midstream ( DTM ) after DTE Energy ( DTE ) spun them off. So overall, my exposure to energy and pipelines, more specifically, isn't aggressive, allowing me to feel comfortable adding a bit more, even if it is a more speculative play.

For further details see:

TC Energy: A High Yield And Growing Dividend Pipeline Play