CA - TC Energy: Growth Business Strategy And Attractive 7.5% Dividend Yield Make Stock Appealing

2023-09-05 00:48:39 ET

Summary

- TC Energy is a prominent energy infrastructure company operating in the US, Canada, and Mexico.

- The company's separated assets and infrastructures in various energy platforms make it prominent and well-positioned to meet future energy demand.

- TRP's financial outlook is positive, with a focus on generating adjusted EBITDA from regulated rates and long-term contracts, leading to improved cash flow and shareholder returns.

Introduction

TC Energy ( TRP ) is a prominent energy infrastructure company operating in the United States, Canada, and Mexico. TC Energy's main financial drivers are related to its extensive infrastructure assets and commercial agreements. The company has comprehensive operations in natural gas and liquid pipelines, power generation, and natural gas storage facilities. In this article, I investigate TC Energy's financial and business outlooks and indicate if the company is still a profitable investment.

TRP business outlook

After the downturn of 2020 and other supply constraints like the Russian invasion of Ukraine, everyone realized that all forms of energy are required to make countries capable of meeting energy demand. As I explained in my previous update , TC Energy's separated assets and infrastructures in a wide range of energy platforms make it prominent. In minutiae, the company has facilities for transporting natural gas from the Western Canadian and the Appalachian basins. They also transit crude oil to Gulf Coast Refineries and generate nuclear in Ontario, Canada. It is worth noting that the company is building infrastructure for importing natural gas into Mexico. Although these vast facilities cater to a higher growth outlook for the company, the management needs to spend plenty of capital expenditures continuously to protect this growth path.

It is worth noting that an unforeseen incident in the Columbia Gas Transmission Pipeline caused the management to drop their operations at reduced pressure in late July. "The cause of the failure is currently unknown, but based on initial observations of the failed pipe, environmental cracking is the suspected cause." Based on the PHMSA report. Although the company returned to service the adjacent parts of the pipeline system that were not impacted by the incident directly, we may see this impact on the company's third-quarter operation results. The reduced pressure at the Columbia Gas Transmission caused TRP stock price to drop by 13%; however, it is not a concern as the infrastructure and operations will be fixed soon.

As you may all know, after global events last year and the energy constraints, the management decided to separate into two businesses to keep the strength of each balance sheet and take advantage of tax incentives for higher growth opportunities. Through this spin-off, TC Energy moved toward a more regulated business model related to renewables. For instance, approximately 75% of TRP's comparable EBITDA will be from nuclear and firming resources by the end of 2030, which are highly regulated.

TRP financial outlook

The spin-off brings the opportunity for the company to generate circa 96% of its adjusted EBITDA from regulated rates and long-term contracts, which will diminish its risk of reliance on commodity prices to a great extent. As a result, the management expects to grow their 2022 comparable EBITDA at a 7% comparable annual growth rate by the end of 2026. On the other hand, the management plans to sustain their capital spending at a minimum range and thus expects ample free cash flow in the coming years. With the mentioned free cash flow, their shareholder returns and leverage conditions are expected to improve.

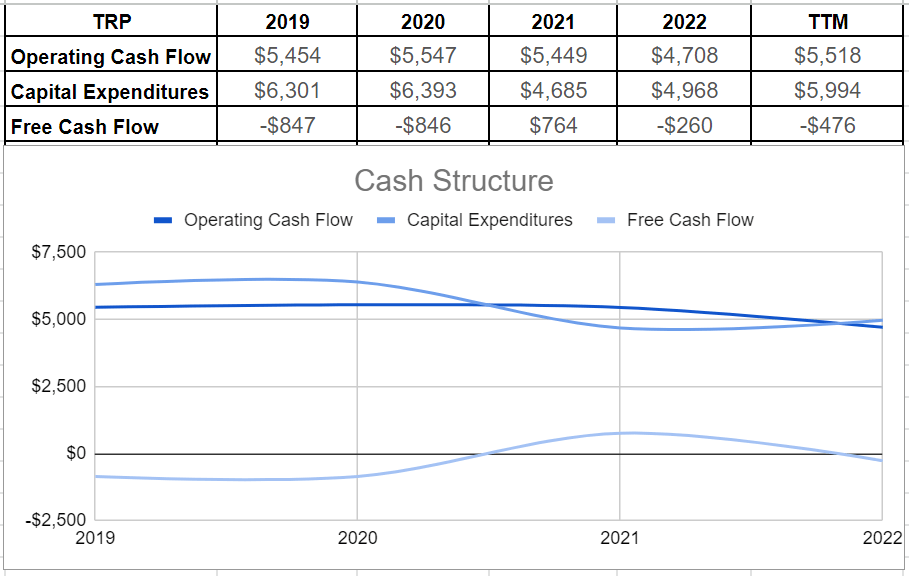

As Figure 1 demonstrates, TRP's operating cash flow increased by 17% to approximately $5.5 billion in TTM versus $4.7 billion at the end of 2022. Although the high amount of capital expenditures of $5.5 billion in TTM led to $476 million of free cash outflow, the company is expected to generate more cash flow from operations due to their spin-off, thereby generating higher free cash flow in the future. In the second quarter of 2023, TC Energy paid CAD$0.96 dividend cash, which based on their 1,029,000,000 outstanding shares, accounts for CAD$987.8 million or approximately $1.28 billion of dividend payment. The company's cash from operation was enough to cover their dividend payment. It is worth noting that capital spending usually is paid by debt and equity financing in the companies in this industry.

Figure 1 - TRP's cash structure (in millions)

{kind=link}

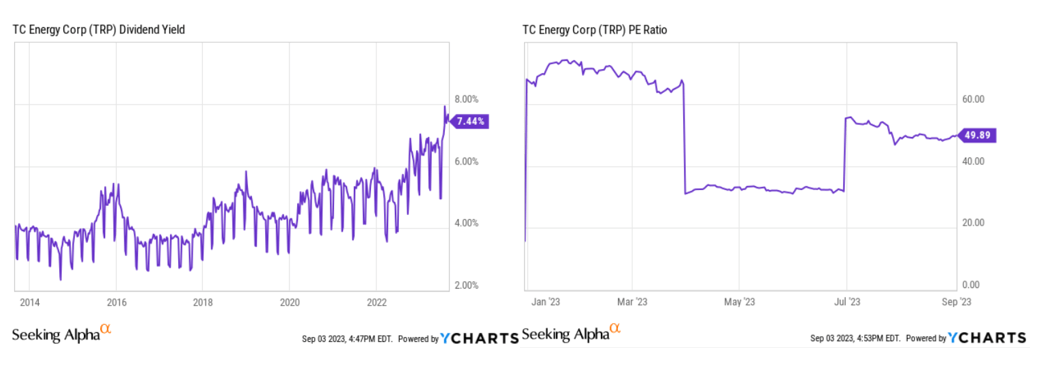

TC Energy provides a 7.45% dividend yield, which is an attractive element of the company. Also, as Figure 2 illustrates, their yield has been on a growing path during the last ten years. In addition, as the management asserted, their liquids business expects to grow its dividend by 2-3% yearly by 2026. Furthermore, TRP's PE ratio of 49x shows a considerable plunge year-to-date, which is another sign that the stock is cheap now and is likely to recover. As a result, currently, TC Energy's financials offer both capital appreciation and increasing dividend yield, while the stock is lower than its historical records.

Figure 2

{kind=link}

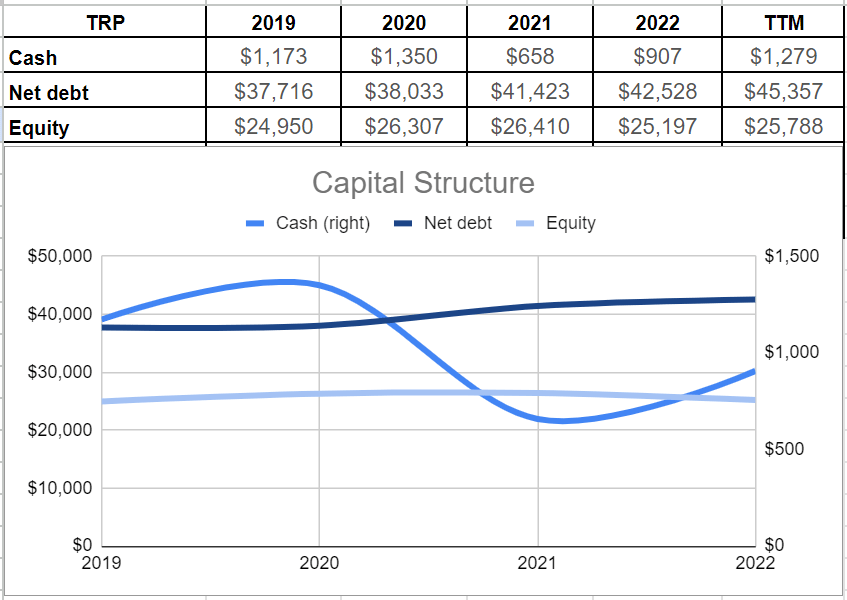

Analyzing the company's capital structure indicates that TC Energy could improve its cash balance to the same level as before the 2020 outbreak and reach more than $1.2 billion of cash generation in TTM. In addition, their net debt level increased to over $45 billion in TTM, which shows the company's higher-than-expected costs from projects like the Coastal GasLink pipeline.

Regarding the company's deleveraging, it is good to hear that the management has made deleveraging a priority and thus took their first step of selling 40% of interest in their Columbia Pipelines to GIP in the recent quarter. With this transaction, the management targets to improve their leverage condition considerably and reach a leverage ratio of 4.75x. As they mentioned:

...with the transaction with GIP, and then with the spin-off, we believe that only an incremental $3 billion of additional divestitures over the course of the next 18 months will be required for us to get below 4.75 times debt to EBITDA by the end of 2024."

It is worth mentioning that the management made more efforts for deleveraging, including filing the sale of its stake in its Nova Gas Transmission System ((NGTL)) in Western Canada in August 2023 . "The NGTL system connects the Western Canadian Sedimentary Basin, which produces most of the natural gas in western Canada, to domestic and export markets." This selling would assist them in declining their debt levels and incline their capability of providing shareholder returns.

Figure 3 - TRP's capital structure (in millions)

{kind=link}

Risks related to TRP investment

Despite TC Energy's solid financials and sustainable dividend yield, the company is not secure from risks related to temperatures and the impact of climate change on both their services demand and their infrastructures. Moreover, as mentioned earlier, the company is pursuing a highly regulated business model, as a result, Governments policies and regulations related to decarbonization and energy transition may affect energy supply and demand and TRP's operations and cash flows. Moreover, TC Energy is growing its investments and increasing its capital spending on several projects. If the management cannot pursue their deleveraging process, they may face hardship in generating revenue and shareholder distributions.

Conclusion

TC Energy has a prominent position to meet energy demand in the future. TRP is a leading midstream company that has the largest natural gas networks in the North America. Furthermore, the spin-off brings the opportunity for the company to generate circa 96% of its adjusted EBITDA from regulated rates and long-term contracts, which will diminish their risk of reliance on commodity prices to a great extent. Also, the management expects to grow their 2022 comparable EBITDA at a 7% comparable annual growth rate by the end of 2026, which brings 3-5% annual growth for their dividend. When all was said and done, the company's year-to-date PE ratio is very low, which shows that the stock price is very cheap now and will recover. Looking ahead, I believe that the management's growth business strategy coupled with attractive 7.5% dividend yield make the stock still appealing for investment.

As always, thank you for reading, and I appreciate your comments.

For further details see:

TC Energy: Growth Business Strategy And Attractive 7.5% Dividend Yield Make Stock Appealing