NVDA - Tech Ruled The First Half Of 2023 The Industry You Need To Watch In The Second Half

2023-06-19 09:00:00 ET

Summary

- Tech stocks have staged a massive comeback in 2023, but value investors should consider looking into currently unloved sectors like healthcare.

- The healthcare sector has underperformed in 2023, but the long-term outlook remains solid despite near-term challenges such as Medicare drug price negotiations.

- However, while the sector as such is comparatively attractive, it is still not cheap in absolute terms. A closer look at individual securities is warranted.

- The article covers Johnson & Johnson, Bristol Myers Squibb, Amgen and Pfizer, Cigna Group and life sciences and diagnostics powerhouse Danaher - four of these six stocks currently represent compelling opportunities.

Introduction

After the furious broad market sell-off that peaked in late 2022, tech stocks have made a big comeback so far in 2023. Driven by the boom in artificial intelligence, broadly-diversified companies such as Microsoft Corporation ( MSFT ) or more specialized players such as NVIDIA Corporation ( NVDA ) attracted particular investor interest - the stocks are up almost 60% and 300% from their respective 52-week lows. Apparently, the sky is the limit.

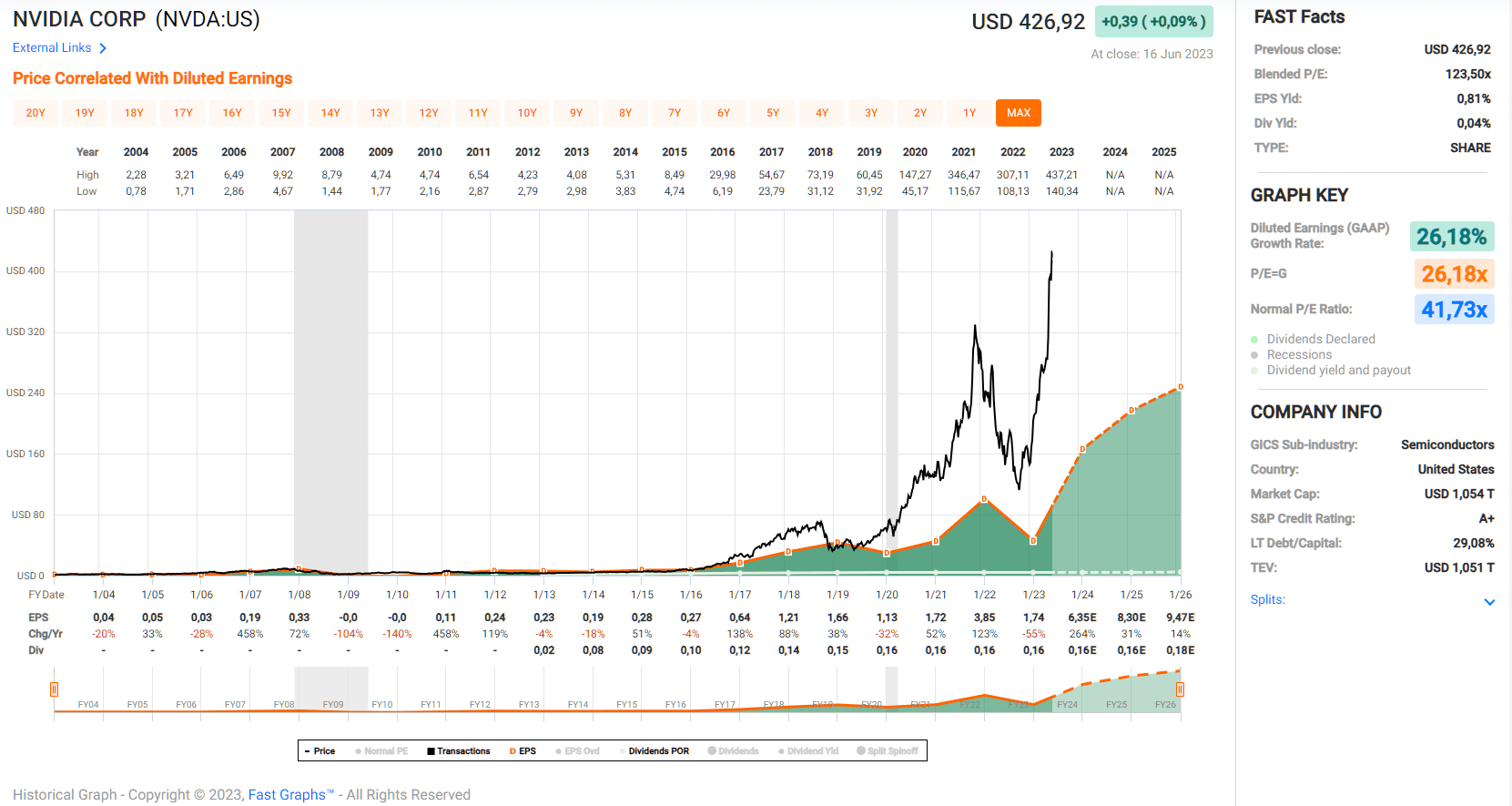

My regular readers know that as a dyed-in-the-wool value investor, I am not attracted by such a situation. Granted, the Hausse could continue, but rather than participate in a game of musical chairs, I prefer to look for value in currently unloved sectors. To be sure, I don't question the potential of artificial intelligence, but the fact that MSFT and NVDA are trading at non-GAAP price-to-earnings ratios of 35 and 53 , respectively, gives me pause. When including seemingly non-cash charges such as stock-based compensation, NVDA stock even trades at a blended P/E ratio of over 120, according to FAST Graphs (Figure 1).

In this article, I'll discuss a sector - and several individual stocks - that are currently unloved by Mr. Market. And while I can't say whether a rotation will occur in the second half of the year, I'm confident that the current period represents a good opportunity for long-term investors like myself.

Figure 1: Nvidia Corporation (NVDA): FAST Graphs chart based on diluted earnings per share (fastgraphs)

{kind=link}

When Everyone Is Looking In One Direction, Dare To Look The Other

I admit that the fear of missing out ((FOMO)) is an emotion that is difficult to keep under control. However, it's important to take a step back and recognize that investing in "hot names" comes with significant risks. The more a company's valuation is based on earnings and cash flows far in the future, the more sensitive it is to changes in the discount rate (i.e., the risk-free interest rate plus an equity risk premium). I covered this aspect of investing in another article .

Over the years, I have learned to appreciate the companies that use technology, not necessarily those that develop it. After all, high excess returns on invested capital ((ROIC)) are an invitation to compete and they revert to the mean over long periods of time.

Relying on hypes when investing is a recipe for disaster in my eyes. But just to be sure, that doesn't mean I'm not interested in investing in technology companies with a durable economic moat and at the right price, like Microsoft (see my comparative analysis with Alphabet Inc., GOOG / GOOGL ).

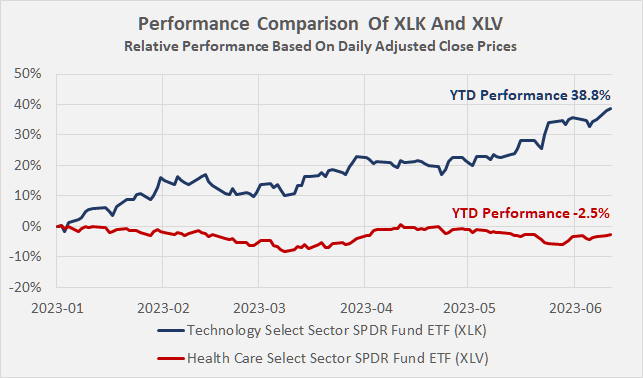

In this context, the significant year-to-date underperformance of the healthcare sector is hard to ignore. The Technology Select Sector SPDR Fund ( XLK ) has returned nearly 39% year-to-date, including dividends, while investors in the Health Care Select Sector SPDR Fund ( XLV ) are down 2.5% year-to-date (Figure 2). This is somewhat surprising given that the fund's third-largest holding ( 7.1% ) is Eli Lilly and Company ( LLY ), which is currently highly regarded by investors, in part because of the potential superiority of its type 2 diabetes and weight loss drug Mounjaro (tirzepatide) over Novo Nordisk's ( NVO ) Ozempic/Wegovy (semaglutide).

Figure 2: Technology [XLK] and Health Care [XLV] Select Sector SPDR Fund ETFs: Comparison of their year-to-date performance (own work, based on the daily adjusted close prices of XLK and XLV)

{kind=link}

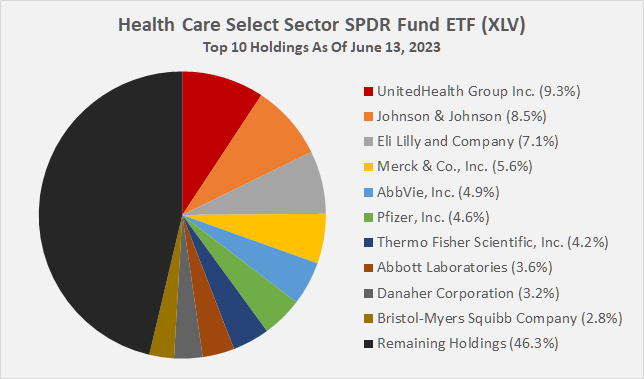

Aside from LLY, XLV's other top 10 holdings (Figure 3) underperformed. The fund is currently weighed down by insurance stocks such as UnitedHealth Group Inc. ( UNH , cost concerns ), pharmaceutical stocks such as Johnson & Johnson ( JNJ , talc litigation concerns ) or Pfizer Inc. ( PFE , capital allocation concerns ), as well as diagnostics and laboratory equipment giants Thermo Fisher Scientific Inc. ( TMO ) and Danaher Corporation ( DHR ), which have been blowing off steam after the rally triggered by COVID-19.

Figure 3: Health Care Select Sector SPDR Fund ETF [XLV]: Top 10 holdings, as of June 13, 2023 (own work, based on SSGA data)

{kind=link}

However, the discrepancy between technology and healthcare stocks is largely due to investors' increasing risk appetite after the bear market of 2022. CNN's infamous Fear & Greed Index is back in "Extreme Greed" territory, largely due to strong market momentum and a low put/call ratio (i.e., comparatively low demand for downside protection).

And while I do not claim to be able to time the market by asserting that healthcare stocks will outperform starting in the second half of 2023, I am confident that the current environment provides a good long-term opportunity to increase exposure to the sector.

One option would be to purchase shares in a low-cost exchange-traded fund (ETF) such as XLV (gross expense ratio of 0.1%, 30-day median bid-ask spread of 0.01%). However, while the valuation discrepancy with XLK (P/E of 27.5 vs. 17.5) is significant, a high teens earnings multiple is still quite high in the context of healthcare. XLV's 30-day SEC yield of 1.59% is also unlikely to be overly attractive to income-oriented investors, even though it is 16 basis points higher than the S&P 500's yield (e.g., SPDR S&P 500 ETF Trust , SPY ).

Instead of buying the entire basket of healthcare stocks, exposing oneself to very obviously overvalued stocks like LLY ( P/E ratio of 52 ), it pays to take a closer look at the other components of XLV. Consider the following six companies:

- Bristol-Myers Squibb Company

- Amgen Inc.

- Pfizer Inc.

- Johnson & Johnson

- The Cigna Group

- Danaher Corporation

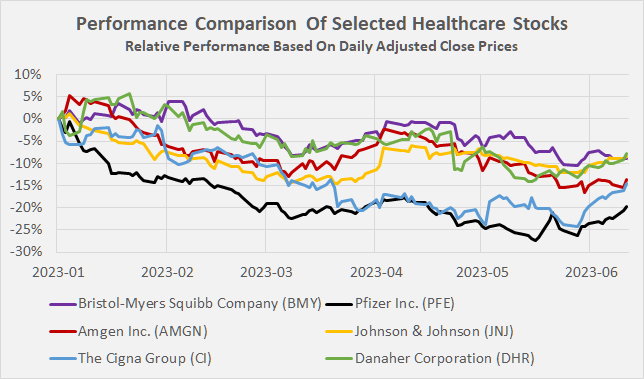

According to Figure 4, the six stocks have underperformed the index more or less significantly – between 5% (Danaher Corp.) and a whopping 17% (Pfizer Inc.), notably including dividends.

Figure 4: Performance comparison of BMY, PFE, AMGN, JNJ, CI, and DHR (own work, based on daily adjusted closing prices)

{kind=link}

An equally weighted portfolio of these six stocks translates to a dividend yield of currently 2.8%, which is significantly higher than that of XLV. The mini portfolio's average P/E ratio of around 13 is also significantly lower than that of the entire basket of healthcare stocks. And while I understand that it's never nice to catch falling knives (at least in the short-term), I would argue that these are all high-quality names. Buying these six companies provides exposure to a broad range of therapeutics (both small molecules and biologics), medical devices, insurance services and pharmacy benefit management, and diagnostics and laboratory equipment.

Let's take a closer look at these six companies.

Bristol Myers Squibb Company ( BMY )

Year to date, BMY is down nearly 9% including dividends - definitely quite a disappointment considering the market - in 2022 - finally showed some appreciation for CEO Caforio's bold $74 billion acquisition of Celgene in 2019. Considering its significant underperformance versus XLV, there must be something wrong, right? In short, the stock is currently plagued by the following issues:

First, Giovanni Caforio will retire as CEO effective Nov. 1, 2023, and will be replaced by former Chief Commercialization Officer Christopher Boerner . It looks like Caforio is leaving behind half-finished work. Second, BMY is highly dependent on three key assets (Eliquis, Revlimid and Opdivo), which together account for 65% of the company's current product revenues. Revlimid sales are declining rapidly as the drug has lost its key patent protection and generic competition is increasing. Third, recent quarterly results point to somewhat weaker growth in new drugs than previously expected, such as Sotyktu, Opdualog, and Camzyos - the latter acquired through the 2020 acquisition of MyoKardia for $13.1 billion. Finally, with 71% of first quarter 2023 revenue generated in the U.S. and a significant weighting on expensive treatments, it is difficult to overlook the potential impact by the relevant elements of the Inflation Reduction Act . It is likely that Eliquis, which currently accounts for 30% of BMY's sales and is marketed jointly with Pfizer, will be affected, as will some of BMY's more expensive cancer drugs.

While this all sounds like the current P/E of 8.2 is well justified, I would argue that BMY represents a very good long-term opportunity. I have shared my optimism for the company's portfolio and pipeline in other articles about the company ( original article , Q2 and Q3 2022 earnings updates), but acknowledge that some time has passed since my last coverage.

While I am not happy about Caforio's departure, the six-month transition period and the fact that he will continue to serve as Executive Chairman of the Board for an undetermined transition period do not suggest that his departure is related to misconduct. Nor do I think promoting a commercialization expert to CEO is a bad idea, given the stage BMY is currently in.

Having reviewed the recent earnings reports, I am still optimistic, if a bit less enthusiastic than before. The decline in Revlimid sales was in line with expectations, and in fact the company beat its own sales estimates for 2022, as I suspected in my Q3 update. Revlimid continues to be an important cash flow contributor, but is obviously in a rapid downtrend. As a result, I was quite pleased with the performance of Eliquis and Opdivo, which grew 6.6% and 14.5% year-over-year, respectively, and currently contribute 45% of BMY's revenue. Both still have significant room to run with estimated minimum market exclusivity through 2026 and 2028, respectively (p. 6, BMY 2022 10-K ).

Smaller contributions (Pomalyst/Imnovid, Orencia, Sprycel and Yervoy) disappointed somewhat, but this was largely due to exchange rate effects. New products such as Zeposia, Reblozyl, Abecma, and Breyanzi (expected peak sales of over $1 billion each) and Sotyktu, Opdualog, and Camzyos (expected peak sales of over $4 billion each) showed comparatively modest growth in the first quarter of 2023, making the company's original plan to achieve $10 billion in sales from its New Product portfolio by 2025 sound somewhat ambitious. As a long-term oriented investor, however, I give management the benefit of the doubt and am careful not to over-interpret a single lackluster quarter. Performance in fiscal 2022 was solid, in my opinion.

Given the fairly ambitious growth plan, the sharp erosion of Revlimid sales, and the potential impact of drug price negotiation initiatives, investors are likely also nervous about the relatively high level of debt. At the end of 2022, BMY's net debt was $30.0 billion, down just 4% from year-end 2019 levels. However, considering that BMY completed a $74 billion transaction (Celgene, 2019) and a $13 billion transaction (MyoKardia, 2020) in a very short period of time, the stable (and even slightly declining) debt over the period underscores Bristol's solid free cash flow, which is currently $13 to $14 billion annually. BMY has strong debt repayment capacity, so it is not surprising that Moody's has not yet seen any reason to downgrade BMY's long-term credit rating or put it on watch for potential downgrade. BMY has had a credit rating of A2 since February 2021, when the outlook was changed from negative to stable. Expected interest payments on long-term debt and upcoming maturities are also very manageable ($3.9 billion of debt matures in 2023, compared to $8 billion to $9 billion of post-dividend free cash flow). Therefore, the company is only marginally - if at all - impacted by a higher interest rate environment.

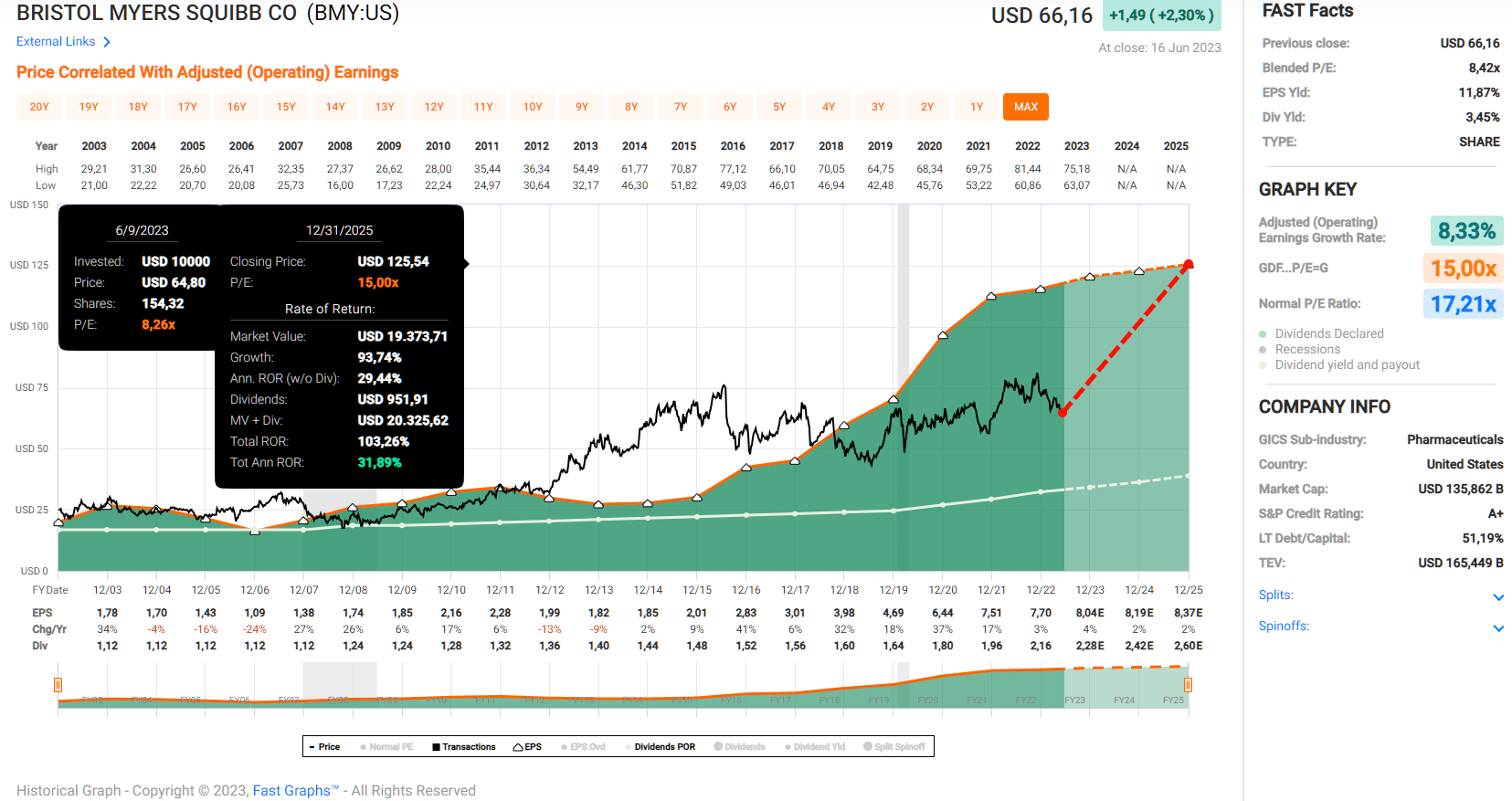

Overall, the market is likely overstating the somewhat lackluster quarterly results, and the departure of Caforio is not helping sentiment either. However, given the strong free cash flow and undeniably strong pipeline, I remain optimistic. The debt maturity profile also suggests no significant near-term challenges, and the ongoing share buybacks and stable credit rating underscore the company's solid foundation. And while I don't think it's reasonable to expect a mean reversion to a 15x earnings multiple (Figure 5), the return prospects of investing in BMY are still strong. Even if the stock reverts only an 11x earnings multiple by the end of 2025, assuming the pipeline-related fog has cleared up, investors can still expect an annual total return of about 20%. In my view, at a price in the mid-$60s, BMY stock represents a solid long-term opportunity for total return investors and dividend growth investors alike.

Figure 5: Bristol-Myers Squibb Company [BMY]: FAST Graphs chart, based on adjusted operating earnings per share (fastgraphs)

{kind=link}

Amgen Inc. ( AMGN )

Amgen can rightly be called the "king of biologics" as the company generates most of its revenues from such compounds. In the first quarter of 2023 , Amgen generates at least 76% of its revenues from biologics, which puts the company in a rather favorable position with regard to the upcoming drug price negotiation initiative. Recall that biologics can be selected for negotiation after 11 years, while small molecule drugs become eligible after 7 years. This is good news given that Amgen generated nearly 60% of its first quarter 2023 sales in the U.S.

Enbrel, Amgen's immunology superblockbuster that was approved in the U.S. already back in 1998 and in Europe in 2000, is now #2 in terms of sales, contributing 9% of the company's revenue. Prolia/XGEVA - a drug to treat osteoporosis by decreasing the development of osteoclasts - generated total sales of $1.46 billion in the first quarter, representing nearly 22% of total product revenues. The drug is expected to peak at about $6 billion, but keep in mind that there will be competition from biosimilars starting in 2025. Otezla (small molecule treatment for psoriasis and psoriatic arthritis), which was acquired from Celgene (see above), is now Amgen's third largest revenue driver, contributing 6% in the first quarter. As I discussed in my previous article , Tezspire (asthma) and Lumakras (lung cancer) are among the key future growth drivers, not including opportunities from the pending acquisition of Horizon Therapeutics (see below). Finally, investors should not underestimate Amgen's potential in the "ChatGPT moment" of biopharma - glucagon-like peptide-1 ((GLP-1)) agonists for the treatment of type 2 diabetes and obesity ( phase 1 trial of AMG 133 ). In my view, investors are currently underestimating the potential of companies other than the obvious darlings (Eli Lilly and Novo Nordisk), on the one hand, and the tumorigenetic potential of the class, on the other.

All in all, it is fair to say that Amgen's portfolio is well diversified, but it is still important to keep in mind the focus on biologics and the significant exposure to the U.S.

In one of my previous articles , I highlighted Amgen's leading profitability and consistent free cash flow growth. In an environment where many companies were more or less artificially boost earnings per share through debt-fueled share repurchases, Amgen remained comparatively conservative (don't over-interpret its low equity ratio and high debt-to-equity ratio, see explanation here ) and did not pay out more than it took in in free cash flow.

Of course, the pending acquisition of Horizon Therapeutics plc ( HZNP ) for an enterprise valuation of about $28 billion changes this picture somewhat, and this is already visible on the balance sheet, which reflects debt assumed via a bridge credit agreement. Gross debt increased year-over-year from $38.9 billion to $61.6 billion, and even when including the roughly $7 billion in cash, cash equivalents, and marketable securities (currently $31.6 billion), the leverage ratio increased from 3.5 times net debt to free cash flow to 6 times. Horizon will contribute about $1.0 billion, but its free cash flow has grown strongly in recent years and is expected to continue to do so, thanks largely to Tepezza, a biologic to treat thyroid eye disease. The drug generated $2.0 billion in sales in 2022 and is expected to peak around $4 billion. Horizon's portfolio looks solid (p. 5 ff., HZNP 2022 10-K ), but comes at a high price. However, given Amgen's strong track record, I give management the benefit of the doubt and do not want to underestimate the potential of the company's pipeline (p. 12 ff, HZNP 2022 10-K). Despite the good growth in Horizon's therapeutics, investors should still keep an eye on Amgen's leverage, in part due to the expected cash flow contraction of the main portfolio starting in 2025. I expect share repurchases to be temporarily suspended (or at least significantly reduced) - recall that Amgen has repurchased $15 billion worth of shares over the past three years, representing more than 10% of its current market cap. Also, given that Moody's recently revised the outlook on Amgen's long-term Baa1 credit rating to negative, I would like to see the company prioritize deleveraging over share repurchases until its leverage is back to a more reasonable level.

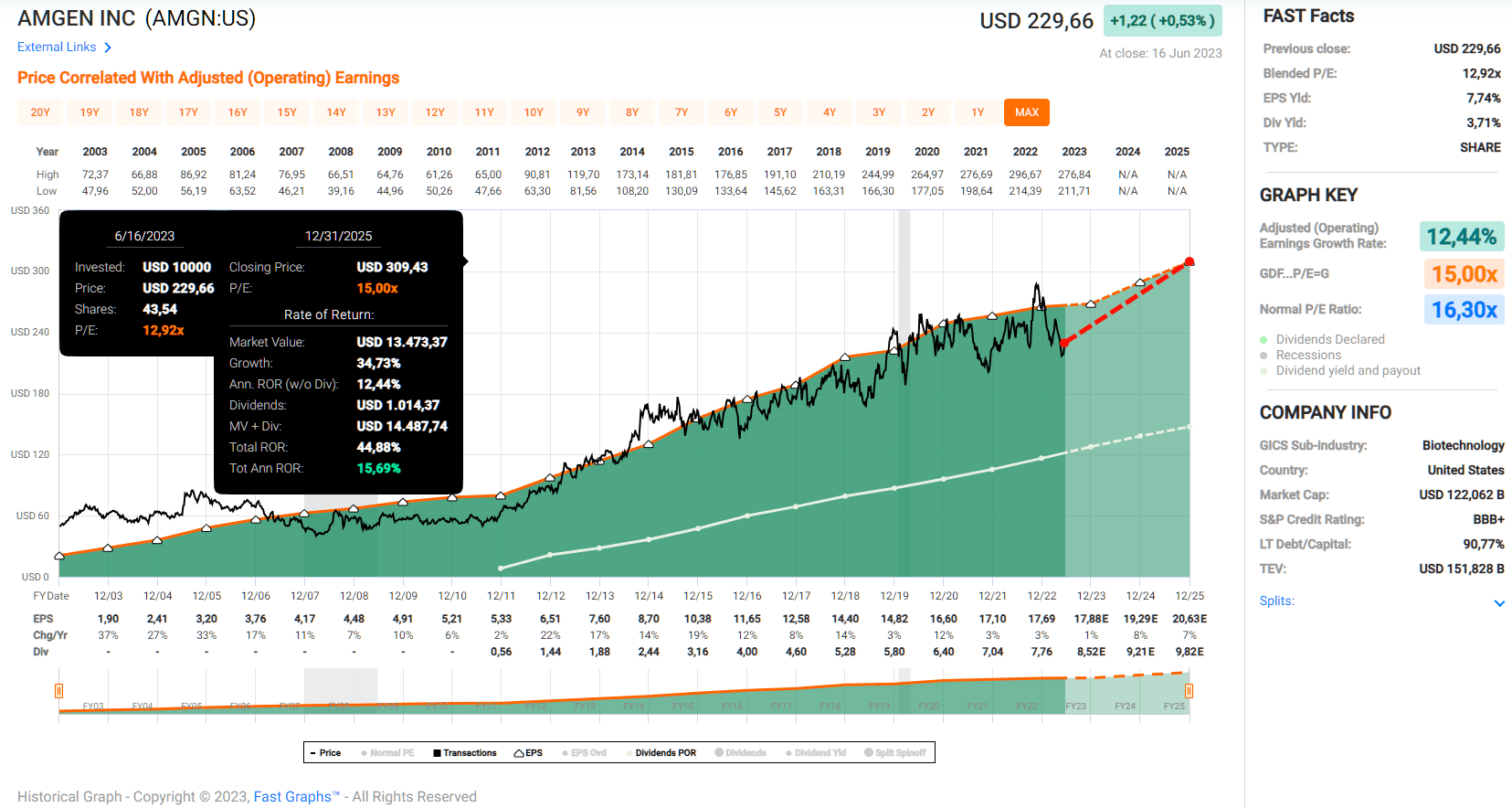

After a 20% decline from the all-time high of $290 reached in November 2022, which is largely attributable to uncertainties associated with the HZNP acquisition, I view AMGN stock as favorably valued today. The combined company trades at a forward free cash flow yield of over 8%, and from an earnings perspective, I would also say that AMGN is far from expensive:

Figure 6: Amgen Inc. [AMGN]: FAST Graphs chart, based on adjusted operating earnings per share (fastgraphs)

{kind=link}

I think it's reasonable to expect the stock to mean-revert in the coming years, representing an annualized return potential of about 15%, but of course this assumes that the Horizon integration goes well and growth turns out as expected. Amgen's earnings consistency is among the best in the industry, and its solid dividend performance is another aspect worth noting. Granted, the company has only been paying a dividend since 2011, but growth has been extremely strong at 16% on a compound annual basis over the past decade. While growth has slowed - highlighted by the five-year CAGR of 10% - I would argue that it is still very good, qualifying Amgen as a favorably-priced total return stock with dividend growth potential. Suffice it to say, I took advantage of the recent dip to add a few shares to my position.

Pfizer Inc. ( PFE )

The stock of pharma company Pfizer Inc., which has been selling-off dramatically following the Comirnaty- and Paxlovid-induced boom of 2021 and 2022, has finally rebounded thanks to the abovementioned "ChatGPT moment of biopharma". I admit that I started catching the falling knife, as I wrote in my bullish note in January 2023. At that time, the stock was still trading at about $45, so I am down more than 10% on the tranche I bought at that time. However, as a long-term investor, I'm not worried about the short-term underperformance. I am confident about Pfizer's long-term prospects, and view the current environment as a solid opportunity.

Investors are increasingly skeptical - rightly, in my view - of Comirnaty and Paxlovid sales. Some level of base sales will remain, but it would be foolish to expect their combined $56.7 billion top-line contribution (2022) to continue. In the first quarter of 2023, the revenue contribution from Paxlovid and Comirnaty was only 39%, and Comirnaty-related revenue was down almost 80% - hardly unexpected. In my opinion, it all depends on how well Pfizer's management uses the excess cash flows generated in 2021 and 2022.

Share buybacks and dividends are not a priority at the moment, underscored by the rather meager $2.0 billion in shares repurchased over the past three years. However, I appreciate the fact that Pfizer has not bought back a large number of shares during a period when the stock was quite expensive. Pfizer has increased its dividend by four cents a year since 2020, a rather meager 2.5% growth rate. However, it should be remembered that the dividend was not rebased after the spin-off of Viatris Inc. ( VTRS ) at the end of 2020. In my opinion, Pfizer definitely has the ability to return to more significant dividend growth, considering that the company is expected to pay out only about 50% of its projected free cash flow for 2024-2025.

In addition to the acquisitions of Arena Pharmaceuticals in December 2021 and Biohaven in October 2022 (see my last article linked above), the proceeds from Comirnaty and Paxlovid will be used to fund the acquisition of Seagen Inc. ( SGEN ). Of course, this does not mean that Pfizer will be able to pay Seagen with existing cash on hand (about $20 billion at the end of the first quarter, including short-term investments). Pfizer is spending about $43 billion on Seagen, significantly strengthening its oncology portfolio (28% of product sales in 2022, excluding Comirnaty and Paxlovid). Seagen currently has four marketed drugs, Adcetris, Padcev, Tivdak, and Tukysa (p. 109, SGEN 2022 10-K ). In 2022, these assets generated combined sales of $2.0 billion, making Pfizer's projected sales contribution of $10 billion by 2030 sound somewhat ambitious. However, I would argue that Pfizer had to de facto target a larger acquisition given the impending LOEs (losses of exclusivity). With Eliquis, Ibrance, and Vyndaqel, more than 30% of Pfizer's 2022 sales (excluding Comirnaty and Paxlovid) will be subject to generic pressure starting in 2026 (p. 7, PFE 2022 10-K ). However, Pfizer's pneumococcal vaccine franchise (particularly the 20-valent Apexxnar) still has room to run (estimated minimum exclusivity through at least 2033, Prevnar 13 through 2026). The franchise accounted for 15% of Pfizer's sales in 2022.

All in all, I would argue that Pfizer is one of the better diversified large pharma companies, but of course the uncertainties surrounding the Seagen acquisition and the upcoming LOEs have put a lot of pressure on the share price. To end on a positive note, Pfizer is one of the better geographically diversified pharma companies, and the Seagen acquisition is likely to be beneficial in this regard. Pfizer generated 58% of its 2022 revenues outside the U.S., making it one of the companies subordinately affected by the Inflation Reduction Act.

As with Amgen, Pfizer's long-term credit rating ( A1 ) outlook was revised to negative in light of the pending acquisition. I would argue that the company's debt-to-free cash flow ratio most likely remains manageable, but there is obviously considerable uncertainty due to the earnings opacity and the future of Comirnaty and Paxlovid.

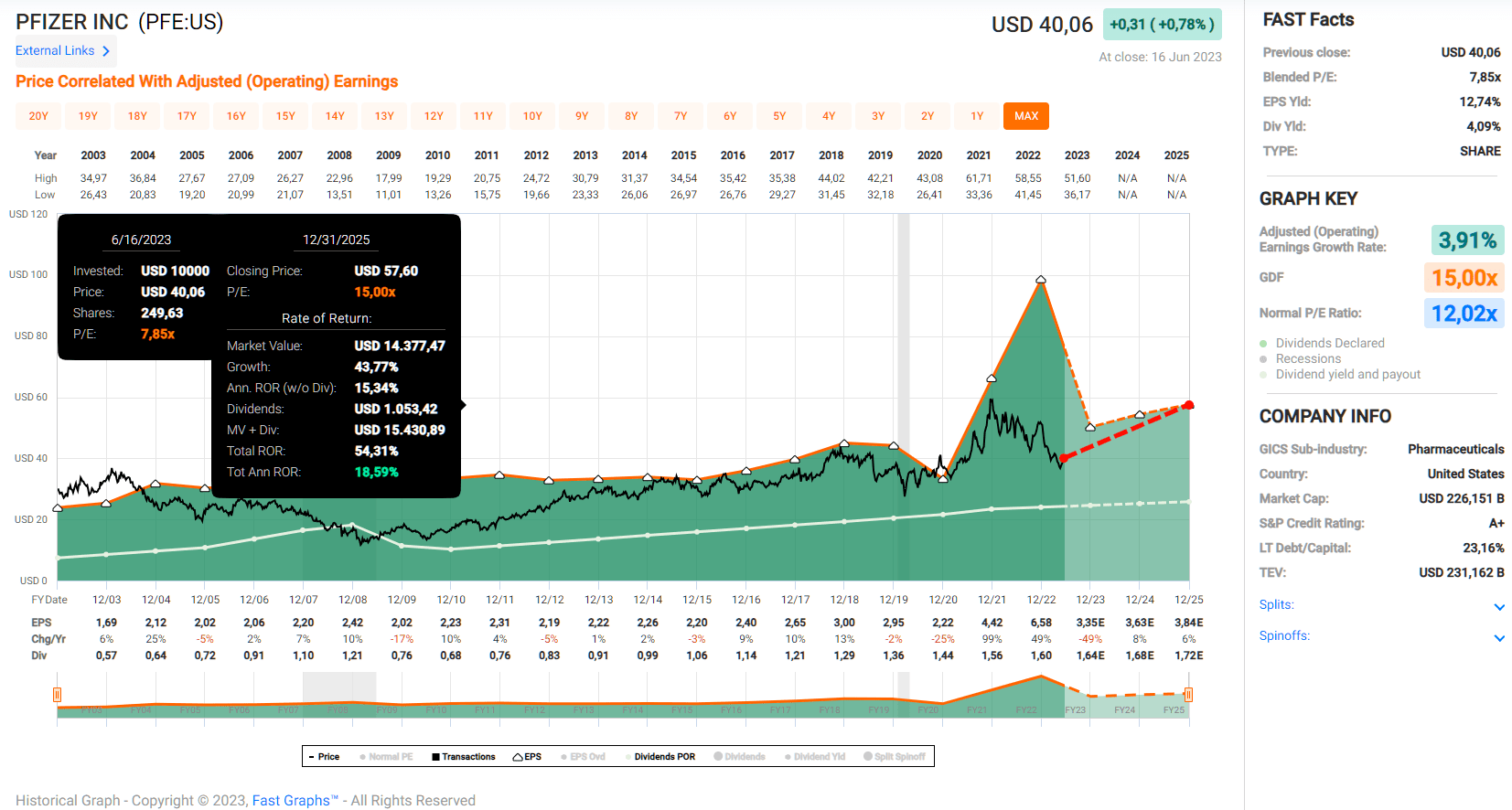

Largely because of these uncertainties and, of course, the aforementioned sector rotation and waning optimism for Comirnaty and Paxlovid sales, Pfizer is trading at or close to pre-pandemic levels. The market is more or less completely ignoring the company's commercial success since 2021. In my view, and despite Pfizer's arguably poor long-term performance (2002 to 2020 adjusted earnings growth of only 1.9%), Mr. Market is overly pessimistic here, but at the same time, I don't think mean reversion to 15 times earnings is realistic (Figure 7, 20% annual return potential) unless Pfizer pulls a rabbit out of the hat (e.g., regarding danuglipron, its oral GLP-1 receptor agonist, see phase 2 trial results ). However, even if the market grants PFE shares only a 12x earnings multiple by the end of 2025, the return potential of around 10% per year, including dividends, is still acceptable.

Figure 7: Pfizer Inc. [PFE]: FAST Graphs chart, based on adjusted operating earnings per share (fastgraphs)

{kind=link}

I have been a long time shareholder of Pfizer, but sold most of my position in late 2021. During the bear market in 2022, I began to add back to the stock and have added to my position on recent weakness. I welcomed the recent drop to well below $40 to bring my position to 1% of total portfolio value currently. However, as I do not want my individual pharma positions (with the exception of Johnson & Johnson, see below) to exceed 1.25% or 1.50% of my portfolio, I will not be an aggressive buyer going forward.

Johnson & Johnson ( JNJ )

I first covered Johnson & Johnson in early 2023 . In my in-depth analysis, I compare the company to Swiss giant Roche Holding AG ( OTCQX:RHHBY , OTCQX:RHHBF , which I am currently buying as well). JNJ is undoubtedly a well-diversified healthcare giant and is rightly referred to by some as a "healthcare mutual fund". However, its drug pipeline is a bit weak right now in relation to the size of the company, but I realize it's hard to move the needle on a $460 billion giant.

What I particularly like is Johnson & Johnson's very reliable growth, its deep-rooted acquisition culture and, of course, its level of diversification - including geography. About half of its sales are generated outside the U.S., which mitigates the potential impact of the relevant elements of the Inflation Reduction Act. That being said, Invega and Darzalex , which together account for 23% of JNJ's pharmaceutical segment's 2022 sales and 13% of total sales, among others, could be affected. However, I would not overstate the impact of the initiatives based on current evidence. Finally, regulators also need to be mindful not to be too aggressive or innovation could stall.

I was somewhat disappointed when I first read about the Consumer Healthcare spin-off, although I have come to the conclusion that the somewhat stagnant business could return to more meaningful growth as a stand-alone unit. In my view, the transaction was a potentially necessary step in the company's legal maneuvering to resolve talc-related litigation. However, the spinoff should not be viewed as a move to transfer talc liabilities to Kenvue Inc. ( KVUE ), as I explained in detail in my article on this still-evolving situation.

The talc litigation is still weighing on the stock, but JNJ has rebounded recently. It is likely that investors are increasingly confident that the company will be able to settle all current and future claims in the U.S. and Canada through LTL Management's renewed Chapter 11 filing , albeit with an increased amount of about $9 billion (originally about $2 billion). I shared my opinion on the situation in my April 2023 update . In my view, the talc liabilities will not have a material impact on the fair value of JNJ stock (the company currently generates free cash flow of over $20 billion per year). A discounted cash flow ((DCF)) analysis shows that the impact is likely about -1.4% if the model's terminal value is excluded, or less than 1% if it is included (as is typically the case in DCF analyses).

As indicated by the long-term credit rating of Aaa ( stable outlook despite ongoing litigation), JNJ's balance sheet is rock solid. The company could easily repay its debt as it comes due and still maintain its growing dividend (payout ratio of 50% to 60% of free cash flow). At the end of the first quarter of 2023, JNJ's net debt was $28.3 billion, up a whopping 75% year-over-year. The sharp increase was due to the acquisition of Abiomed Inc. for an enterprise valuation (i.e., including net debt) of $16.6 billion. However, despite this - at first glance worrying - development, JNJ would still be able to pay off all of its net debt with only about 1.5 years of free cash flow.

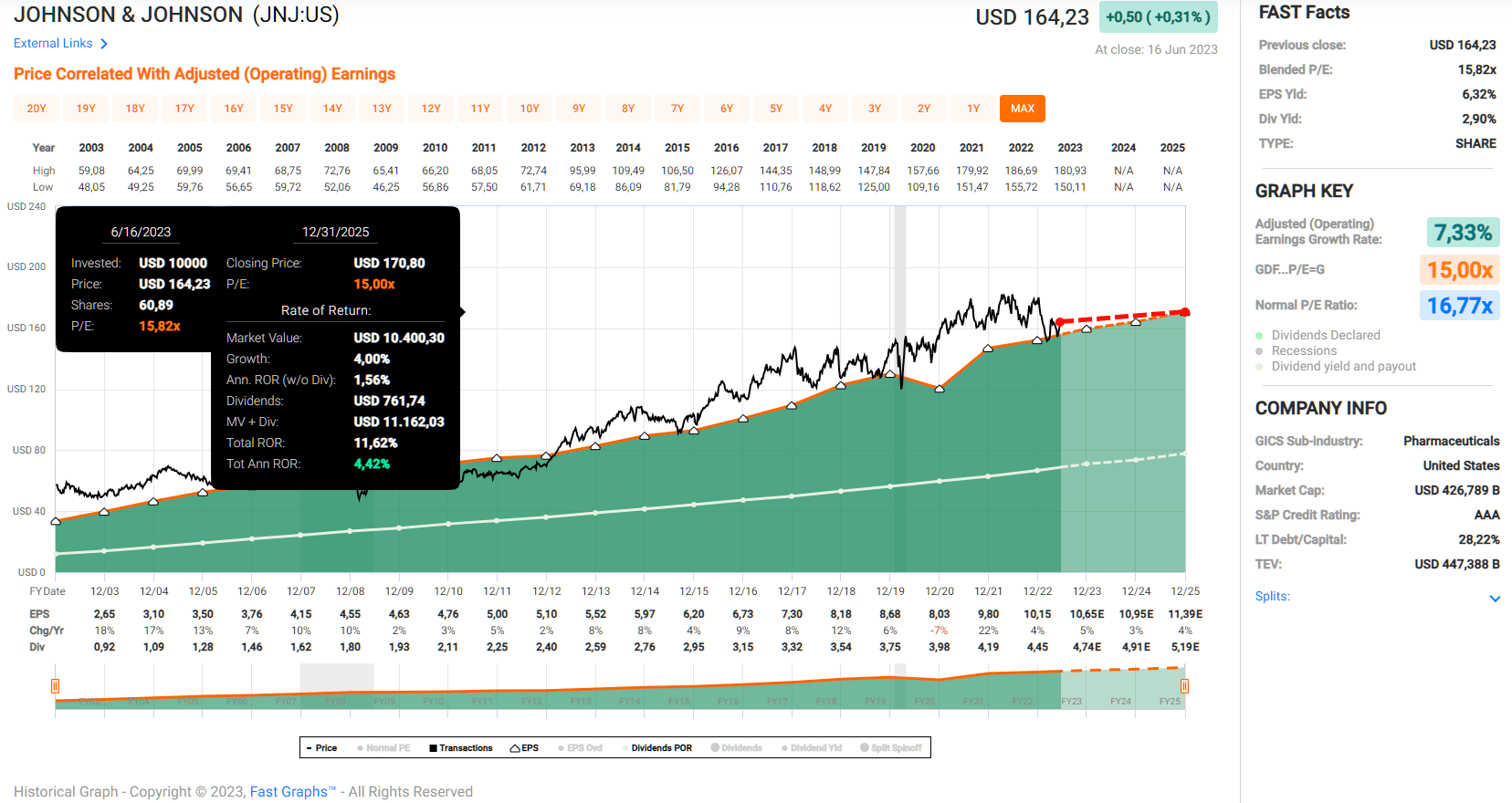

In terms of valuation, JNJ is one of the more expensive stocks I cover in this article. However, with a current price-to-earnings ratio of about 16, I don't think the stock is overvalued (Figure 8), but the return prospects - 4.4% annually including dividends - are not overly compelling either. Investors are paying the price for high earnings reliability, a rock-solid balance sheet and a steadily growing dividend. I think the Kenvue spinoff could unlock value for shareholders, improving the return outlook. All in all, I view JNJ stock at $160 as a formidable company at a fair price. However, since it is by far my largest position in healthcare, currently about 3.5% of the total portfolio value, I am no longer an aggressive buyer, but I do buy shares on weaknesses.

Figure 8: Johnson & Johnson [JNJ]: FAST Graphs chart, based on adjusted operating earnings per share (fastgraphs)

{kind=link}

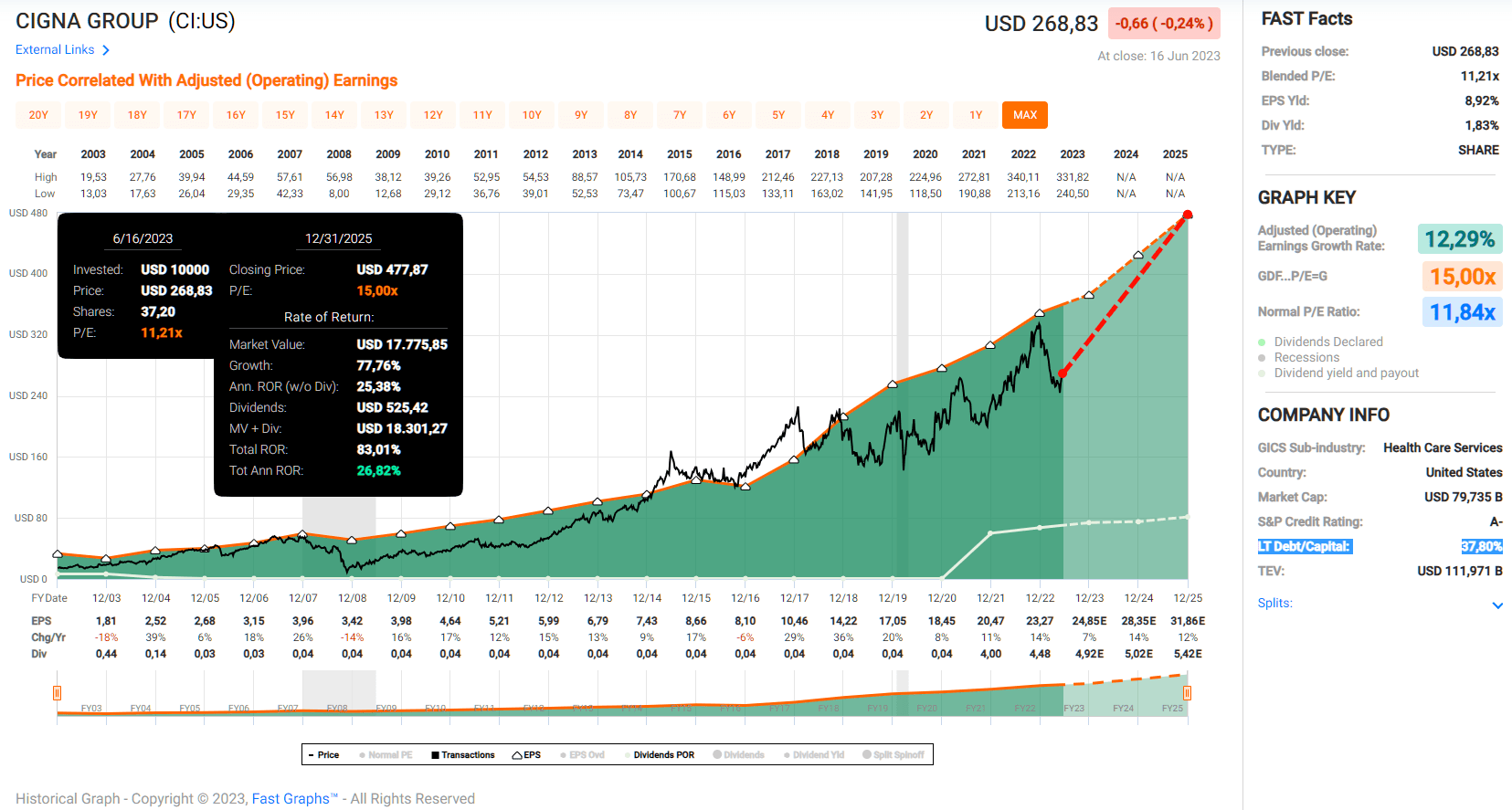

The Cigna Group ( CI )

I first covered insurance company and pharmacy benefit manager ((PBM)) in June 2022 and concede that I did not anticipate the stock's temporary outperformance during the bear market. In my November 2022 update , I explained where I went wrong in my earlier assessment.

In the meantime, the stock had completed its roundtrip and now trades at a blended P/E ratio of 11. In my article published prior to the May 2023 first quarter earnings report, I explained why I wanted to open a position but still decided to wait until after the results were released. I suspected a nice earnings beat due to the generally quite conservative nature of Cigna's management and tendency to under-promise to over-deliver. Suffice it to say, I was fortunate to still initiate my position in the $240 region, as the stock rose relatively quickly that day in response to solid results (good medical insurance trends, favorable medical cost ratio.

The 2018 acquisition of PBM Express Scripts was a bold move, but the combined company is starting to show its benefits. One aspect I particularly like is Cigna's focus on reducing medical cost growth (which is expected to be in the low single digits or below), which puts the company in a favorable position in the current environment. Other reasons include highly reliable earnings growth (see FAST Graphs chart below) and very strong free cash flow, as well as Cigna's international expansion plans. Of course, these come with many risks and uncertainties, but at some point a U.S.-focused insurer can only grow so much domestically. Over the past 20 years, Cigna's earnings growth has averaged 12% per year, even before adjustments. The company expects to maintain this growth rate in the future.

In absolute terms, debt is still quite high, as is the number of shares outstanding. Fully diluted shares outstanding increased from 250 million in 2018 to 380 million in 2019, but the company has been aggressively buying back shares - diluted weighted average shares outstanding decreased to 296 million by the first quarter of 2023. Considering that the stock traded in a broad range of $150 to $250 post-acquisition (and ignoring the run-up in 2022), I think the buybacks were quite efficient. Over the same period, Cigna's net debt declined from $31.9 billion to $23.7 billion, or by more than 25%. This is hardly surprising given the strong free cash flow of about $7.7 billion annually. Although Cigna's debt is still high in absolute terms, I don't think it's problematic because of its strong - and, more importantly, reliable - free cash flow. Rating agencies were also pleased with Cigna's performance since the Express Scripts transaction. Moody's, for example, upgraded Cigna's senior unsecured rating by two notches to Baa1 with a stable outlook.

And despite the post-earnings rebound, I still think the stock is very cheap. If CI stock returns to a 15x earnings multiple, investors would earn an annualized return of 27% through 2025 (Figure 9). However, since it is an insurance company, and taking into account pent-up demand in elected operations and increased scrutiny of PBMs , I would put the "fair P/E" a bit lower, around 13 times earnings. But even in that case, the expected annual return would be about 20%, and remember that the projected average dividend growth rate is only 6.6%. Taking management's capital allocation strategy into account, as well as the payout ratio of less than 20% of normalized free cash flow, solid growth prospects and reliable analyst estimates, I think it's reasonable to expect Cigna's dividend to continue to grow at about 10% per year .

Figure 9: The Cigna Group [CI]: FAST Graphs chart, based on adjusted operating earnings per share (fastgraphs)

{kind=link}

I am a big fan of Cigna stock at this level and will continue to add to my position in the coming weeks and months with available cash. I think the stock is a compelling opportunity for long-term oriented total return and dividend growth investors alike.

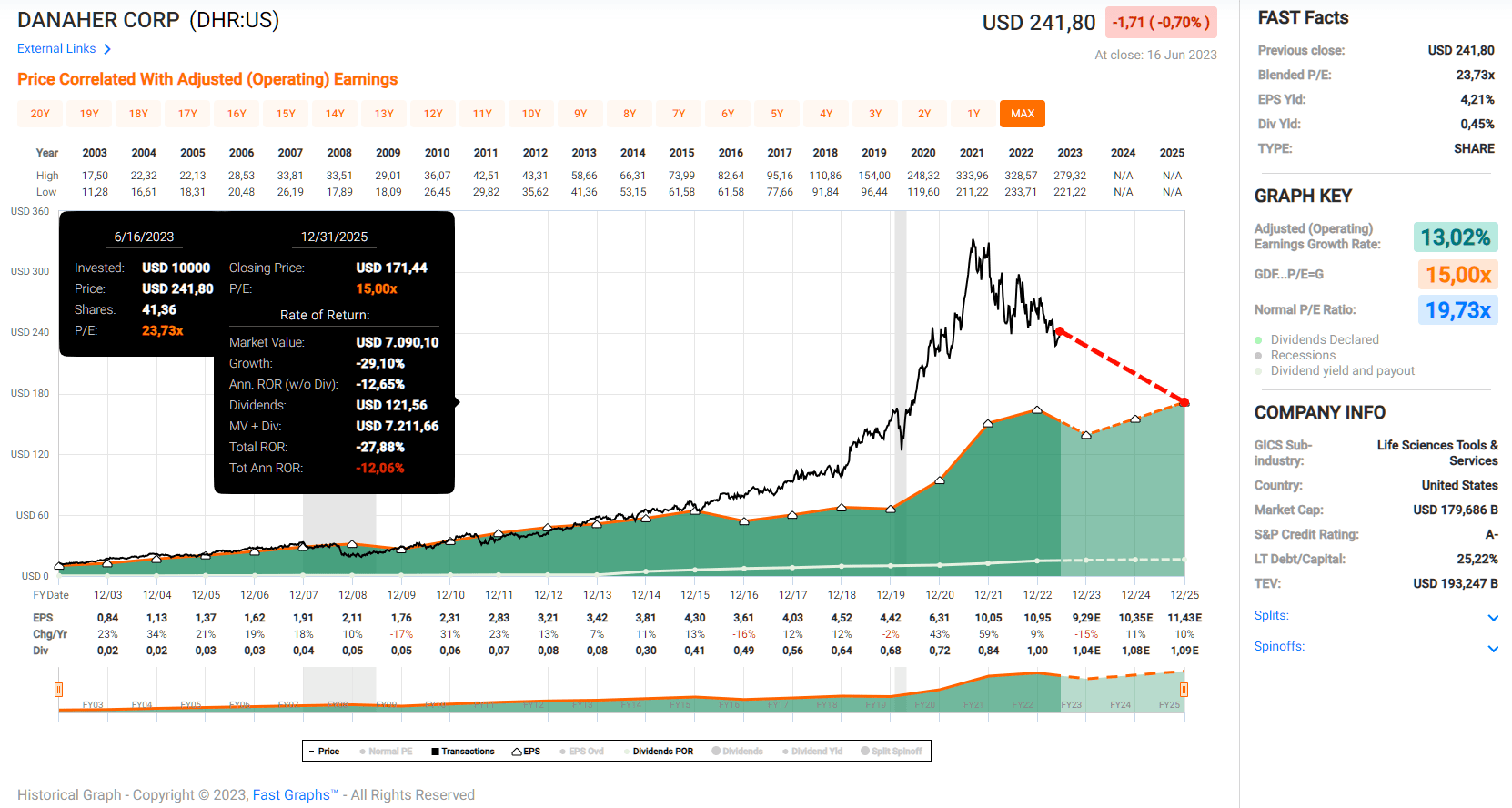

Danaher Corporation ( DHR )

To round out this "mini-portfolio" of high-quality healthcare stocks that I currently consider worth buying, I think it's worth taking a look at a name that is particularly strong in life sciences and diagnostics. Besides, Danaher Corporation is also active in environmental & applied solutions, but intends to spin off this segment (15% of sales in 2022) as a separate publicly traded company called Veralto .

I first looked at the serial acquirer in December 2022, and while the company currently benefits from a number of tailwinds, I found the valuation (26x earnings at the time of writing) not compelling. While long-term earnings and free cash flow growth of 12% is definitely very good, Danaher's return on invested capital ((ROIC)) and cash ROIC (CROIC) are surprisingly modest for a company with relatively low capital expenditures (about 15% of operating cash flow), suggesting that acquisitions are creating limited shareholder value. Investors should keep in mind that with a market capitalization of around $180 billion, it is increasingly difficult to move the needle through take-overs, and big acquisition targets rarely come cheap. Of course, the same is true for pharmaceutical and medical device giant Johnson & Johnson (see above). In addition, the life sciences industry is fairly consolidated with large companies like Thermo Fisher Scientific Inc. ( TMO ), Agilent Technologies Inc. ( A ), Waters Corporation ( WAT ) and Bruker Corporation ( BRKR ).

Danaher's balance sheet is very healthy. This is partly due to the company's occasional dilution of shareholders to fund acquisitions. However, the number of shares outstanding has remained largely stable over the last decade due to occasional buybacks. I view this financing approach (including through mandatorily convertible preferred stock, see my other article ) as very conservative and obviously sustainable.

At the end of the first quarter 2023 , Danaher's net debt stood at $12.5 billion, down 9% year-over-year. Considering that the company currently generates free cash flow of around $7 billion per year, it is fair to say that the debt is very manageable. Using full-year 2022 figures, Danaher's interest coverage ratio is also very conservative and is currently more than 30 times free cash flow before interest.

In terms of valuation, Danaher is by far the most expensive of the stocks covered in this article. With a blended P/E ratio of 24, a mean reversion to a 15 times earnings multiple would imply a negative return of 12% per year through 2025. The market has gotten ahead of itself with DHR stock, and this is nicely illustrated in the FAST Graphs chart in Figure 10. Although I am critical of DHR's earnings multiple expansion, I don't think the 15x figure is justified, especially considering the successful acquisition-driven growth strategy. I believe that an 18-20 times earnings multiple is a good reflection of Danaher's past performance and future prospects, so I don't see the stock as worth buying at this point (always keeping opportunity cost in mind).

I have Danaher on my watch list, but would not start buying until $200 or less. In the context of serial acquirers, however, I've been keeping a closer eye on U.K.-based Halma plc ( OTCPK:HLMAF , OTCPK:HALMY ; see my recent article ), an underfollowed company with a phenomenal track record spanning several decades. Halma is even more expensive than Danaher, but I would argue that its growth prospects are much better due to its considerably smaller size (market cap of around £9 billion).

Figure 10: Danaher Corporation [DHR]: FAST Graphs chart, based on adjusted operating earnings per share (fastgraphs)

{kind=link}

Concluding Remarks

In the first half of 2023, technology stocks staged a massive comeback. This is largely attributable to the potential that investors see in artificial intelligence and increasing risk-on sentiment. And while I don't question AI's enormous potential, as a value investor I always pay attention to the valuation of the stocks I buy. In my opinion, investors are once again underestimating the duration risk of stocks with cash flow profiles heavily weighted toward the distant future. I prefer to invest in high-quality companies with strong current cash flows that are trading at compelling valuations due to uncertainties or manageable near-term challenges.

Largely due to increasing demand for risk-on assets, the healthcare sector has significantly underperformed so far in 2023. The sector's long-term outlook remains solid, despite near-term challenges such as the upcoming Medicare drug price negotiation initiative and other inflation-dampening measures. Shifting funds out of technology stocks or funds and into a broadly diversified healthcare ETF like XLV seems like a promising endeavor, also from a risk mitigation standpoint.

However, looking at XLV's valuation, it is clear that the basket as a whole is still not a bargain, so it pays to take a closer look at the individual components. In this article, I briefly reviewed blue-chip pharma companies Bristol-Myers Squibb, Amgen, Pfizer, and Johnson & Johnson, as well as an insurance/PBM business (Cigna Group) and a life sciences and diagnostics blue-chip (Danaher).

Danaher is undoubtedly a well-managed company with a high-quality balance sheet and a leading portfolio in diagnostics and life sciences (brands such as AB Sciex, Molecular Devices, Phenomenex, Beckman Coulter, etc.). However, with a market cap of $180 billion, it is likely to become increasingly difficult for management to make value-enhancing acquisitions. At 24 times earnings, the stock is expensive, and even under conservative assumptions, the return outlook is rather poor.

JNJ stock is the most expensive of the five companies I consider worth buying today, but it is undoubtedly the highest quality company. A t 16 times earnings, the return prospects are relatively limited. However, I believe the Kenvue spinoff has the potential to unlock value, and a final settlement related to the talc litigation could improve investor sentiment and thus the stock price.

BMY stock is plagued by near-term uncertainties related to management, pipeline, and LOEs, but I remain optimistic about the company's prospects and consider its high debt (in absolute terms) to be very manageable. I recently added to my position due to the cheap valuation, but I am no longer an aggressive buyer. I focus on risk mitigation through diversification and therefore keep my individual pharma holdings at 1.5% of total portfolio value or less, with the exception of JNJ. My BMY position is now at 1.2% of total portfolio value.

AMGN and PFE are plagued by uncertainties related to their planned acquisitions (Horizon Therapeutics and Seagen, respectively). The debt incurred in the process is certainly significant, but looks manageable for both companies. Longer term, I am a bigger fan of the capital allocation skills of Amgen's management. Conversely, I appreciate PFE's better geographic diversification. Amgen is the better value right now in my opinion, and I think both companies could surprise positively in the context of GLP-1 agonists for type 2 diabetes and weight loss - a huge opportunity for pharma as a whole.

Finally, Cigna is probably the best pick from a return perspective, although I think the stock could remain range bound for an extended period of time due to increased scrutiny of PBMs and insurance companies lumped in with other financials (Cigna has a rather short duration float). However, as a long-term investor, I am not looking for quick short-term gains. I use opportunities like the current one to slowly but surely build my position. Currently, Cigna stock only makes up about 0.3% of my portfolio, and I would feel comfortable increasing my position to about 1%, provided the stock remains at a valuation of about 10 times earnings.

Leaving DHR stock aside, an equally weighted portfolio of the five companies would currently yield 3.2%, with a compelling five-year compound annual dividend growth rate of 7.4%. Therefore, and due to the portfolio's average P/E of only around 11, I would argue that the five stocks represent a compelling opportunity for total return and dividend growth investors alike. Nonetheless, I would keep Danaher on my watch list and consider buying the stock at $200 or less.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there is anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Tech Ruled The First Half Of 2023, The Industry You Need To Watch In The Second Half