CA - TELUS: About That Herculean One-Foot Putt

2023-12-03 18:00:00 ET

Summary

- TELUS stock has risen sharply and outperformed BCE Inc. and Rogers Communications Inc.

- Q3-2023 earnings beat consensus estimates.

- We tell you why the bottom is not yet in.

Note: All amounts are in Canadian Dollars. The stock price refers to the TSX quoted one, not the NYSE one.

On our last coverage of TELUS ( TU )( T:CA ), we maintained a neutral stance as the stock while lower than previously, was not resoundingly cheap. We favored covered calls to generate a defensive 10-12% total yield while protecting against downside. That defensiveness proved warranted as the stock dropped as much as 11% from that point. It has since risen sharply and is actually higher than when we wrote our last piece. It has also handily beaten BCE Inc. ( BCE )( BCE:CA ) and Rogers Communications Inc. ( RCI.A:CA ) over this timeframe.

Did we miss the bottom?

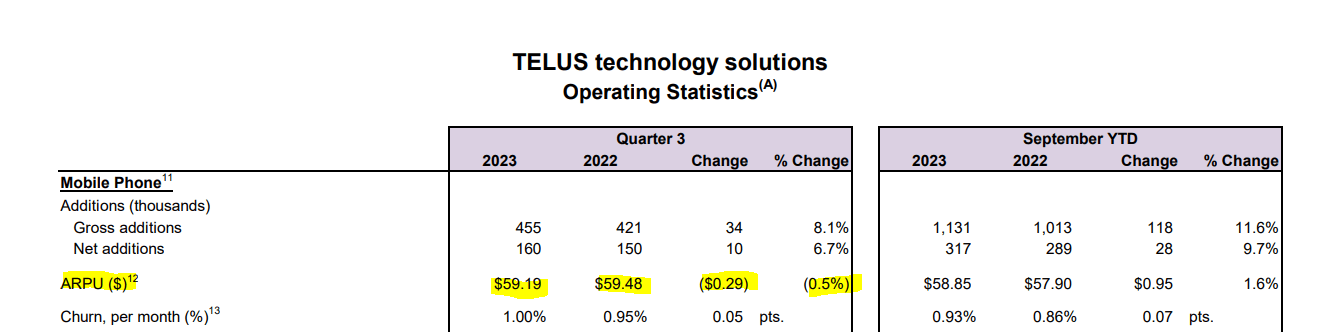

Q3-2023

One reason to suspect that the bottom might be in would be based on the very strong reaction off the timeframe in which the earnings were released. The simplistic view being, earnings were good and we are back to a bull market. But we don't think that is logical. Our primary issue with TELUS long position back in early 2022 , was based on poor valuation. Our refusal to go directly long even recently was also based on valuation. That would not correct with a single quarter. Even that quarter in question had a weak spot.

TELUS reported an adjusted earnings per share number of 25 cents and that came in 1 cent ahead of consensus. The adjusted EBITDA number beat as well by about 1%. Net additions were strong at 160,000. This was also ahead of consensus and it appears TELUS ate BCE's lunch in this area. But it did so while showing an average revenue per unit declining 0.5%.

{kind=link}

That was a surprise drop. This was the key focus on the conference call. We are posting three related talking points from that conference call on the ARPU issue. Note that these paragraphs are not continuous.

Notably, our postpaid churn is now in the tenth consecutive year at less than 1%, and we’ll soon be entering its 11th year. The close on mobile third quarter ARPU of $59.19 was down slightly year-over-year as a result of intense promotional activity in the market and heightened activity in the flanker space. This was mitigated, however, by our long-standing focus on AMPU-accretive loading, driven by our team’s passion for winning and retaining profitable customers. At the same time, we are maintaining a keen eye on efficiency by remaining highly disciplined on device subsidies and leveraging our leading digital capabilities.....

While ARPU momentum has softened by competitive aggression, deceleration of roaming growth versus pre-pandemic performance and a skew in loading towards lower ARPU segments, we remain disciplined on quality profitable loading.....

And as Zainul mentioned earlier, our device subsidy is declining at a rate 3.5x faster than ARPU. So in Q3, when you look at it, our device subsidy per subscriber declined by $1.05 year-over-year, which is quite a dramatic number. And we expect this to continue, along with the growing preowned device volumes that we’re seeing.

Source: TELUS Q3-2023 Conference Call Transcript

All that sounds good and TELUS remains confident that we will back driving this up. We think they are probably right for the next 1-2 quarters. But after that, we think we will come back to this point and realize this was the first warning sign of slowing demand and increasing competition. TELUS Health and TELUS International ( TIXT ) are doing well, but they remain too small to change the picture of TELUS' valuation in the next 3 years.

The Valuation Question

With utilities and utility-like companies, rarely do you see single quarter that makes or breaks the investment idea. It is almost always about valuation. On that front, TELUS has a lot of work to do. Consensus estimates for 2023 are at 96 cents. Focus first on the evolution of this over the last 12 months. From an estimated $1.35 all the way down to 96 cents.

Next look at the estimates for 2024 above. This started off at near $1.60 a share and is now down to $1.10. All during this time, we have analysts congratulating management for "solid quarters" and telling you to buy while the stock continues to drop. Each quarter also tends to "beat" estimates. How can all of this remotely make sense? How can a company that has its estimate dropping by over 30% for 2023 and 2024 be doing well? This is the game and it is a sad one. Analysts rush to downgrade estimates between quarters and then management makes the Herculean one foot putt to beat estimates. Congratulations, you have now been tricked into buying a stock where estimates seem to have no bottom.

We would be able to get behind this story as well, if those estimates came in the postal code of reasonable. The $1.10 for 2024 (and you can take it from us it will actually be well below that) puts it at a 23X earnings multiple. Even in the ZIRP arena this would be too much, let alone with 5% risk-free rates.

The growth groupies will be pleased to know that after all of this "growth" TELUS will produce earnings in 2024 that are 30% lower than the 2019 number of $1.43 (you have to adjust that $2.86 for a 2:1 stock split).

TELUS 2019 earnings

Even on a free cash flow basis, the dividend was not covered in 2020, 2021 and 2022. It won't be covered in 2023 and 2024. So if you see us constantly bring you away from worshipping the pedestal of the dividend yield, we do it with sound reasoning.

Verdict

There was a time, not so long ago, that we thought could form a sustainable bottom in the $22 range. We don't believe that to be the case. Our view is now that Canada is likely to face mounting challenges from the mortgage interest rate resets. Canadian mega banks are handling it by going the infinity route on mortgage amortization. Well 4 out of the 6 are at least.

Hanif Bayat

The Q3-2023 numbers already showed a decline in GDP and that is quite remarkable, considering how many immigrants we added in over the past 12 months. We will see tooth and nail competition in the quarters ahead from the telecom sector. Valuation does not look remotely appealing at 17-18X free cash flow and 23X earnings for TELUS. We would stay out and consider a Sell/Short Sell rating above $27.00.

{kind=link}

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

TELUS: About That Herculean One-Foot Putt