TER - Teradyne: A Technology Pioneer At A Crossroad - Risks And Opportunities Ahead

2023-06-28 22:42:17 ET

Summary

- Teradyne, a major player in the automated test equipment and robotics solutions space, is facing a cyclical downturn across most segments. However, the automotive and industrial SoC test markets are bright spots.

- The financial strategy involves prudent investments and maintaining financial discipline, with the aim to keep operations efficient throughout the cycle.

- The company's valuation suggests a fair amount of asymmetric risk-return proposition. However, the industry's cyclicality and the current macroeconomic landscape are cons.

Teradyne, Inc. ( TER ) carves out its niche as a major player in the automated test equipment and robotics solutions space, with a presence spanning various sectors that heavily lean on technology. The reach of their operations is substantial, covering industries from consumer electronics to aerospace and defense. Teradyne excels in the development and commercialization of automatic test systems and robotics products, aimed at an array of sectors. Their product suite includes semiconductor test systems, wireless test systems, storage and system level test systems, and robotics products.

At its essence, Teradyne's products strive to boost efficiency and pare down costs for its clients within the manufacturing and logistics sphere. Nevertheless, the wide-ranging nature of its product line and the variety of industries it caters to might render it susceptible to an array of hurdles. These include the need to maintain technological leadership, adjusting to fluctuating demand trends, and navigating the intricacies of the supply chain across multiple fronts.

The company is grappling with a contraction in revenue across most segments, which is a worrying trend. However, a deeper dive into their 1Q23 earnings call can shed light on the main challenges and opportunities that Teradyne is currently contending with.

Technology Advancements and Sector Shifts

The financial performance of the company is akin to a roller-coaster ride, primarily a reflection of the industry's cyclical nature, evidenced by alternating periods of rapid growth and sharp slowdowns in revenues and gross profits.

{kind=link}

However, it's critical to note that each cycle carries its distinct characteristics, and the current one is no different. Although the SoC market is in a slump, largely attributable to the reduced demand in the Compute and Mobility sectors, an unexpected growth has been noticed in the automotive and industrial SoC test market. This growth is fueled by fresh device applications such as electric vehicles, autonomous driving, and industrial digital transformation. Let's delve a bit deeper.

Per the company's management team, the Compute and Mobility sectors had accounted for over 70% of the SoC market for the past four years. Thus, their downturn considerably impacts the overall industry.

However, a silver lining presents itself in the robustness of the automotive and industrial SoC test market, which currently constitutes approximately 30% of the market. The demand in this sector is exceeding expectations, leading to extended lead times for some tester configurations. This rising demand can be attributed to a host of factors including new and emerging device applications, and customers' desire to replenish their inventory that had been whittled down over the past three years. As such, the intensity of this downturn in the SoC test market may not be as grave as previous cycles.

An additional dynamic particular to this cycle is the heightened tester demand originating from China-based chipmakers. While this demand exceeds the broader market, its long-term sustainability remains uncertain. These intricate dynamics contribute to the difficulty in accurately forecasting the timing and scale of the recovery.

All-in-all, the company projects a 20%-30% decline in the SoC market in 2023 from last year, dropping to a range of $3.3 billion to $3.8 billion, but anticipate a two to three percentage point increase in their market share.

As for the Memory segment, ongoing technological shifts continue to stimulate test demand even though an oversupply is constraining capacity expansion investments. They foresee the market to either remain stagnant or fall by 10% from last year, with a marginal increase in their market share.

Wireless Test Market and the Wi-Fi 7 Transition

Despite forecasts of a dip in sales in the wireless test market, the impending shift to Wi-Fi 7 could potentially fuel a resurgence in demand and growth within the sector.

Nevertheless, in the short term the LitePoint Wireless Test segment finds itself in the throes of a recognizable correction cycle, with sales projected to decrease by 20%-25% from the previous year, primarily as the transition to Wi-Fi 7 remains roughly a year away. Meanwhile, the revenue for the System Test group is anticipated to shrink by 20%-25% over the year. This reduction can be traced back to the dwindling demand for Hard Disk Drives (HDDs) and a decline in smartphone shipments.

Growth Potential in Robotics

As various other areas, Robotics is also struggling right now, in spite of near-term hurdles and a deceleration in the robotics division, the future outlook remains interesting. Factors such as escalating labor costs and a lack of sufficient labor could pave the way for an annual growth rate of 20%-30% in the interim, marking it as a viable candidate for a long-term investment. Let’s take a deeper look.

Revenues in Q1 2023 fell 14% relative to Q1 2022, reflecting the ripple effects of the conflict in Ukraine and a slowdown in industrial expansion. Over at Universal Robots, market conditions are proving to be challenging, with Q1 sales lagging behind those of the same period last year. Despite this, shipments to Europe have made a significant comeback to their highest levels, while demand in the United States and Asia dipped substantially in Q1. A notable internal challenge lies in their ongoing adjustment of their distribution system, which increasingly zeroes in on larger customers and OEM partners bearing higher long-term growth potential. This transition is inducing short-term headaches but promising indicators include robust pre-orders for the new high-payload UR20 cobot, slated to begin shipping in the middle of the year.

Mirroring Universal Robots, MiR is grappling with industry-wide obstacles and a seasonal lull in Q1 demand. Yet, their strategic move to intensify direct involvement with larger accounts has led to a surge of over 40% in unit installations in this segment since Q1 of 2022.

Given the unfavorable macro environment and absence of signs pointing to imminent improvements, the full-year revenue projection for the Robotics group has been adjusted downwards to 0%-10% growth from last year's $403 million. Nonetheless, the long-term perspective on robotics growth potential is still optimistic, with the possibility of 20%-30% annual growth over the midterm, primarily propelled by labor shortages and spiraling labor costs.

Financials

Their overarching strategy involves prudent investments and preserving financial discipline, even while anticipating a revival in demand. The objective is to keep the operations efficient, with investments funneling into their products and capabilities to feed future profits.

In the present, the company kicked off the first quarter with robust sales, raking in $618 million, which exceeded the midpoint of their guidance by $28 million. The non-GAAP EPS stood at $0.55. Operational expenditures have risen, primarily as a result of revenue losses leading to less dilution of fixed costs, consequently pulling down the operating profit from 25% to 15%.

The second-quarter sales projections are set between $625 million and $685 million, with a non-GAAP EPS ranging from $0.55 to $0.74, suggesting that the company is poised to maintain profitability for the rest of the year.

The financial strategy of the company involves keeping operational expenditure relatively flat, investing to fortify the global supply chain, supporting long-term growth initiatives in the testing and robotics realms, and generating healthy free cash flow.

The third quarter's sales are expected to be on par with the second quarter, while the fourth quarter is anticipated to witness a slight improvement, meaning the latter half of the year could see better performance than the first. The full-year gross margins are likely to hover between 57% and 58%.

The company's balance sheet exhibits robust strength, with a current ratio surpassing 3.3, showing progress compared to the same period last year. The company bears practically no debt on its balance sheet and maintains a low leverage profile.

This portrays an image of a company currently navigating a cyclical downturn, which may worsen if macroeconomic conditions follow suit. However, on the bright side, it boasts a sound cost structure, which is why it remains profitable. Additionally, its strong balance sheet should provide a buffer to weather any economic headwinds should they arise.

Valuation

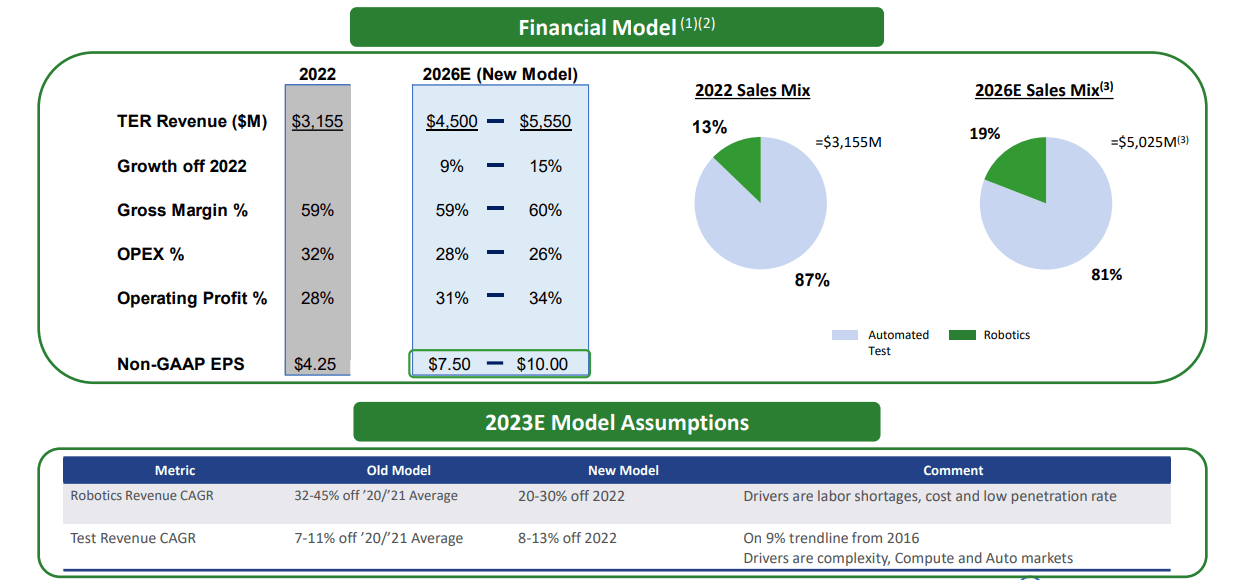

We've already delved into the short-term tribulations the company is grappling with, yet it's worth noting that the company has a history of intermittent bursts of revenue acceleration. To help us anticipate what lies ahead in the mid to long term, the company has furnished a forward-looking guidance.

{kind=link}

This prognostication is tremendously useful as it enables us to construct a bull and bear scenario to evaluate the company's current valuation. The bear scenario could be envisioned as a stagnation phase from 2023 to 2026, where, due to a host of issues, possibly a recession, the company is unable to cultivate growth. On the other hand, the bull scenario is the optimistic interval of the company's outlook for 2026. The findings are intriguing since they hint at a fair amount of asymmetric risk-return proposition. The odds implicit in the price suggest less than a 25% probability of the bull scenario coming to fruition.

Bull and Bear Scenarios for 2026 (Author's computations)

Regardless, the industry's cyclicality, twinned with the existing macroeconomic landscape, encourages me to defer any investment in this company for the time being. That being said, I do believe the company boasts intriguing technology and operates in sectors that are poised for remarkable growth in the upcoming years, while the valuation is not bad. I might be making a mistake by waiting, the macro scenario discourages me from entering the company right now.

For further details see:

Teradyne: A Technology Pioneer At A Crossroad - Risks And Opportunities Ahead