TER - Teradyne And Advantest: A Duopoly In The Semiconductor Value Chain

Summary

- Teradyne and Advantest dominate the semiconductor test equipment market with a combined market share of around 95%.

- I expect both companies to grow in line with the overall semiconductor market (6-8% CAGR) until 2030.

- The balance sheets are very strong, both companies are generating high returns on capital and act in a duopoly position in a growing market.

- My DCF valuations indicate that both companies are undervalued.

Introduction

In this article, I want to start coverage of Teradyne Inc. ( TER ) and Advantest Corporation ( ATEYY , ADTTF ). Both companies are semiconductor equipment manufacturers. Together, they own around 95% of the semiconductor test equipment market.

While Teradyne is a US-based company, Advantest is based in Japan. After already starting coverage on Tokyo Electron ( TOELY ) and Shimano ( SMNNY ), this will be my third article on a Japanese company.

As I already outlined in the articles on the aforementioned Japanese companies, I still think that the current weakness of the Japanese Yen (refer to the chart below) offers an opportunity to initiate a position with a possibility of currency tailwinds.

This is especially relevant for EU investors because the current strength of the USD might act as a headwind when investing in TER (if the USD starts to depreciate against the EUR) while the weakness of the YEN might act as a tailwind when investing in Advantest.

Businesses Overview

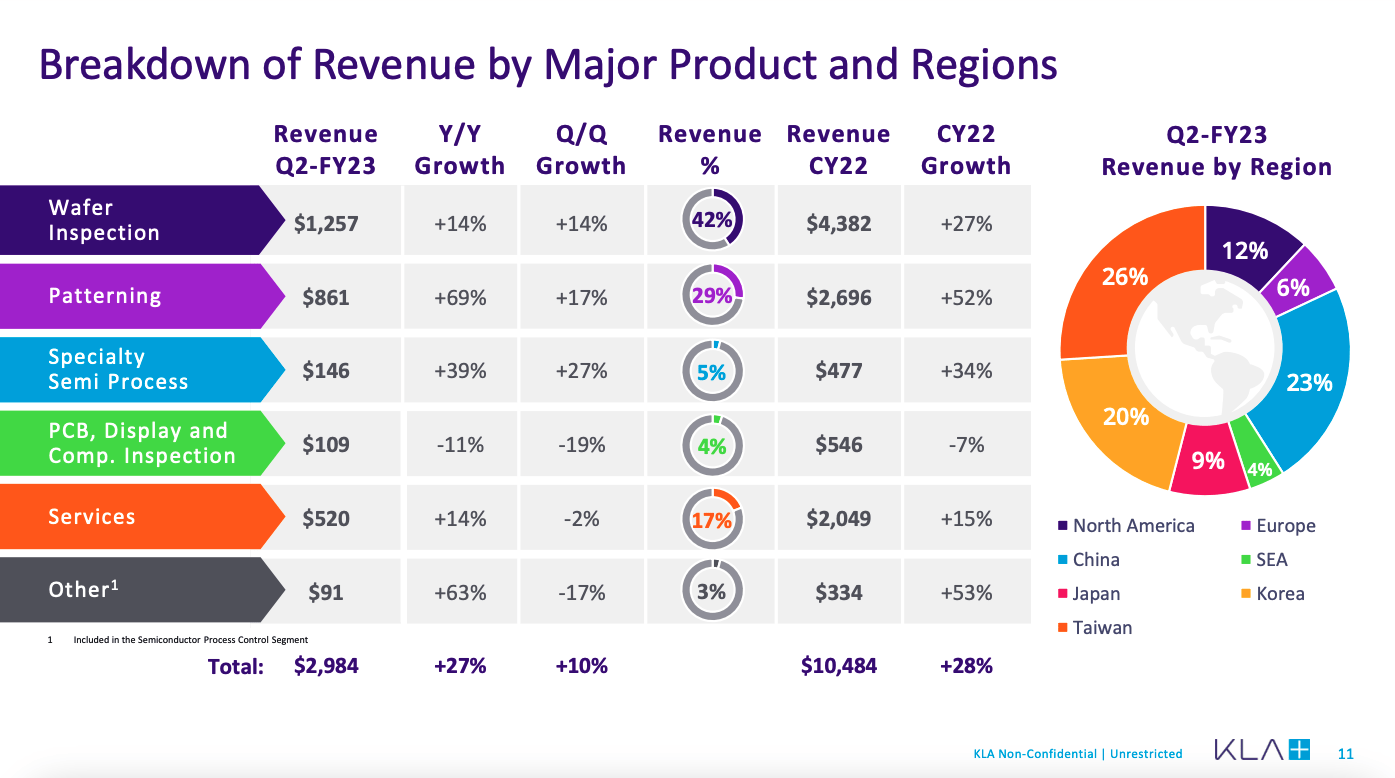

I want to start with an overview of Advantest's operations. Advantest operates in three segments: "Semiconductor & Component Test Systems", "Mechatronics Systems" and "Services, Support & Other". The first two segments account for 80% of revenues (70% Semi Test Systems and 10% Mechatronics Systems) while the Services segment accounts for the remaining 20%. This reminded me of the revenue distribution of one of my other holdings, KLA Corp. (NASDAQ: KLAC ). As can be seen in the slide from KLAC's latest earnings release below, KLAC also has a services segment that contributed 17% of sales in CY22.

KLAC CY22 revenue breakdown (KLAC 2nd quarter FY23 earnings presentation)

{kind=link}

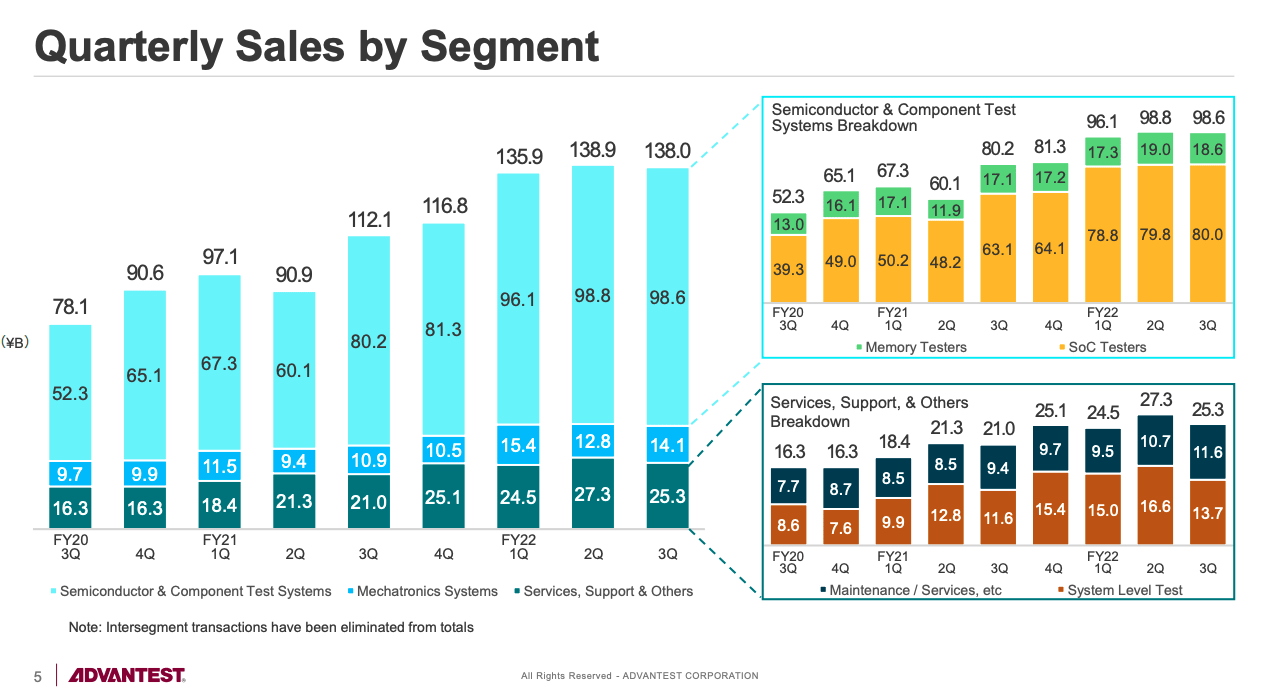

I think this is interesting because the Services segment is a much more predictable source of revenue and helps to counter the cyclical nature of the semiconductor equipment market. For reference, here is the slide from Advantest's latest earnings presentation showing the revenue breakdown over the past 9 quarters:

Advantest revenue breakdown (Advantest 3rd quarter FY22 presentation)

{kind=link}

Advantest's test equipment sales are around 80% SoC Testers and 20% Memory Testers.

Now I want to turn to Teradyne's operations. Teradyne operates in four segments: "Semiconductor Test" (Note: Services are included here and account for around 20% of the segment's revenue), "System Test", "Wireless Test" and "Industrial Automation". Teradyne's Semiconductor Test segment is a counterpart to Advantest's business. Advantest doesn't operate in any of the other three segments.

In FY2022, Semiconductor Test accounted for 66% of revenues, followed by System Test (15%), Industrial Automation (13%) and Wireless Test (6%). The key takeaway, in my opinion, is that Teradyne is much more diversified than Advantest. Advantest is the stock to buy if you want to own a pure-play semiconductor test equipment business. If you want to get exposure to Teradyne's other business segments, especially the Industrial Automation segment which consists of collaborative robots and autonomous mobile robots and is expected to grow at a high rate over the next couple of years, you should buy Teradyne.

As this article will focus on the semiconductor test market I won't further elaborate on Teradyne's other segments. I will probably write a stand-alone article on both companies sometime in the future and will cover Teradyne's other segments in the respective article.

Semiconductor Test Market

Testing is one of the steps in the value chain of manufacturing all kinds of semiconductors. Testing is conducted at two levels : (1) The wafer test that tests wafers and (2) the package test (final test) after packaging.

In my opinion, testing in itself (regardless of what has to be tested) can be very interesting from an investor's point of view. In one of my first articles on IDEXX Laboratories (IDXX) (a company that offers testing products and services in the animal companion space), I highlighted that as long as the underlying market is growing, the need for testing and therefore the testing market will grow as well (likely at the same rate). This is also true for the testing of semiconductors. Now I have no doubt that the semiconductor market will keep growing at a decent rate but to be honest I don't know which of the fabless semiconductor designing companies will stay ahead of the curve technology-wise. Who would have predicted a couple of years ago that Apple (NASDAQ: AAPL ) would come up with the M1/M2 chips and become one of Taiwan Semiconductor Manufacturing's (NYSE: TSM ) largest customers?

Investing in companies like Teradyne and Advantest that dominate a part of the value chain that enjoys the tailwinds of the semiconductor market growth with much less risk than the fabless semiconductor designing companies (regarding disruption of their business) has a much better risk-reward ratio.

Market Outlook

Now one thing that concerned me a bit is that several research portals state that the semiconductor test equipment market is only expected to grow around 3-5% over the next couple of years:

(1) marketsandmarkets.com: 4.7% CAGR from 2022 to 2027

(2) grandviewresearch.com: 3.3% CAGR from 2021 to 2028

(3) alliedmarketresearch.com: 4.2% CAGR from 2021 to 2030

(4) researchandmarkets.com: 3.1% CAGR from 2020 to 2027

This would be a pretty mediocre growth rate.

For the overall semiconductor market , McKinsey & Company estimates around 6-8% growth CAGR until 2030 (to $1 trillion). DIGITIMES Research expects a 7% growth CAGR which is in line with McKinsey's estimates.

Now the big question is: Will the semiconductor test equipment market grow slower than the overall semiconductor market? Let's take a look at what Teradyne and Advantest expect over the next couple of years. Who should know it better than the two companies that form 95% of the whole market?

As you can see in the slide below from Advantest's IR Technical Briefing from December 7, 2022 , Advantest estimates the ATE (Automated Test Equipment) market to grow in line with the whole semiconductor market which is expected to grow to $1 trillion by 2030. This is in line with the estimate of McKinsey.

Advantest Market Estimate (Advantest IR Technical Briefing Presentation)

{kind=link}

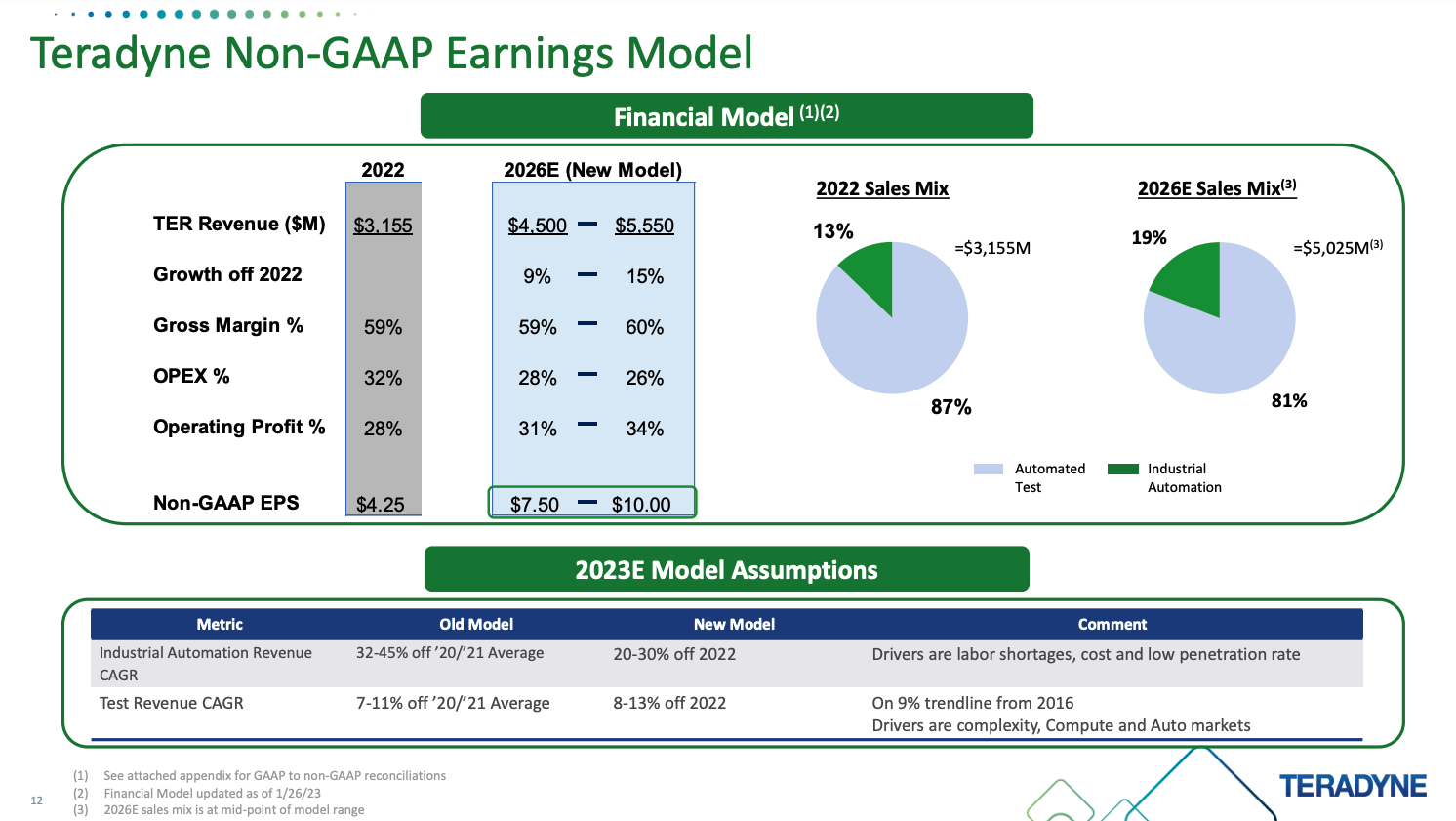

As can be seen in the slide from Teradyne's 4th quarter FY2022 presentation below, Teradyne expects test revenue CAGR of 8-13% until 2026 off of 2022 levels, up from 7-11% off of 2020/2021 average because the market declined in the mid-single digits in 2022.

Teradyne 2026 Financial Model (Teradye Q4 2022 Presentation)

{kind=link}

As can be seen in the next chart, the average overall quarterly YoY revenue growth rate of the two companies over the past decade came in at 12.38% (Advantest) and 8.65% (Teradyne). This is also more in line with the expected 6-8% semiconductor market growth CAGR.

Both Teradyne and Advantest are expecting test revenue to grow at least in line with the overall semiconductor market (6-8%). As this makes very much sense to me, I will rather trust the numbers from the two companies that dominate the industry than the numbers from the research portals above. Overall market growth for the semiconductor test market should be around 6-8% until 2030, so basically over the next decade.

Market Share

Next, I want to take a look at the market share. According to this Forbes article from May 2021, Teradyne CEO Mark Jagiela said the following in an interview:

There are high barriers to entry between Teradyne and Adventis, we control 90% of the market - which is growing at a 7% to 9% annual rate.

Source: Forbes article - Interview

Note that I cited the passage as it is. Adventis was probably a typo from Forbes and should be Advantest. So the Teradyne CEO states that both companies hold 90% market share. I decided to double-check this.

I took the test revenues of both companies (Teradyne: Semiconductor Test Segment; Advantest: Semiconductor & Component Test Systems + the Maintenance and Services part) and converted the YEN numbers to dollars with the conversion rates Advantest used in their 9M ending 2021 and 2022 earnings releases. Here are the numbers for the overall test revenues:

| Test Revenue in |

| CY2021 |

| CY2022 |

| Teradyne |

| 2,642 |

| 2,080 |

| Advantest |

| 2,773 |

| 3,084 |

| Total Test Revenue |

| 5,415 |

| 5,164 |

Next, I took a look at both company's total semiconductor test market estimates for CY2021 and CY2022:

| Test Market Estimate in $ million |

| CY2021 |

| CY2022 |

| (a) Teradyne |

| 5,600 |

| 5,250 |

| (b) Advantest |

| 5,904 |

| 5,560 |

| Mean = (a)+(b) divided by 2 |

| 5,752 |

| 5,405 |

Dividing the test revenue of both companies by the mean of the market estimates resulted in the following estimated market shares:

| Test Market Share |

| CY2021 |

| CY2022 |

| Teradyne |

| 45.9% |

| 38.5% |

| Advantest |

| 48.2% |

| 57.1% |

| Other |

| 5.9% |

| 4.5% |

My last part of the double-checking was to compare my numbers to statements from the management teams in the earnings calls.

In Teradyne's 4th quarter FY2021 earnings call , CEO Mark Jagiela stated the following:

For 2021, we estimate the SOC market was about $4.8 billion, up from $3.6 billion in 2020, which puts our market share at about 46% for the year.

The memory market in 2021 was about flat with 2020 at approximately $1 billion. Our Magnum family continues to shine in the NAND segment, and we're reinforcing our position in the DRAM segment, as the industry prepares for LPDDR5 and DDR5 ramps in 2022 and beyond. Our share remains at about 40%.

Source: Teradyne 4th quarter FY2021 earnings call

Since the memory market is smaller than the SOC market, the overall market share as stated here should have been around 45%, nearly in line with my estimated 45.9% as stated above.

In the 4th quarter FY2022 earnings call , Analyst C.J. Muse (Evercore) stated that the market share in CY2022 should have been roughly 37%. Teradyne President Greg Smith didn't deny this in his answer so this should be quite correct in the company's view. This is also nearly in line with my above estimate of 38.5%.

Lastly, in Advantest's 3rd quarter FY2023 Q&A session , an Analyst said that Advantest's 2022 share of the SoC tester market was in the range of 55-60%. As Advantest didn't deny this number, I think this is also in line with the company's estimates. This is also in line with my estimate above of 57.1%.

In conclusion, the numbers add up and Advantest and Teradyne dominated the semiconductor test market in CY2021 and CY2022 with around 95% of the market share.

Financials

In this section, I want to cover some of the main financial metrics. I want to start by looking at the balance sheets, in particular the net debt/net cash positions:

As we can see, both companies operated with a net cash position throughout the whole last decade. The financial health of the balance sheets is very good.

Revenue growth rates ranged around 8% and 12% for Teradyne and Advantest respectively (refer to the YChart in the "market outlook" chapter).

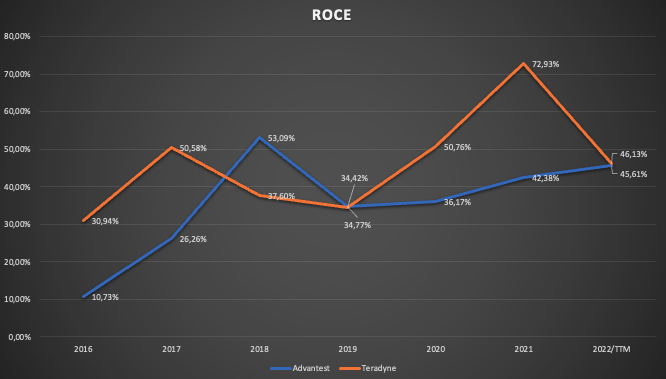

The next chart shows the Return on Capital Employed (ROCE) for both companies since CY2016:

ROCE for both companies since 2016 (Author Calculation from companies reports)

{kind=link}

Note that my definition of ROCE is EBIT/Capital Employed where the Capital Employed = Total Equity + Non-Current Liabilities - net cash position (if there is any). Both companies' ROCE is very high. This indicates a wide moat and, paired with the aforementioned sales growth because of the growing semiconductor (test) market, should have led to exceptional returns over the past few years. The total return for both companies' stocks can be seen in the following chart:

Both companies delivered above 550% total returns over the past decade, far outpacing the return of the broader market. In the case of Advantest, the total return in local currency was even higher (probably around 700%) if you factor in the currency effect I already highlighted in the introduction.

In conclusion, both companies are riding the tailwinds of growth in the overall semiconductor market, resulting in sales growth CAGR in line with the whole market, while operating in a duopoly. This duopoly position allows both companies to generate high returns on capital. These two effects together have led to exceptional returns in the past and I am confident that this will continue. Additionally, the balance sheets are strong and have been strong throughout the whole last decade.

Valuation

This is my first article where I write on two companies at once. I will just split this chapter into two separate ones.

Teradyne

As I am writing this, Teradyne is trading at $100.64 per share. With 164,300,000 shares outstanding at the end of the 4th quarter of FY2022, the market capitalization is $16.5 billion. After deducting the current net cash position of $872 million, the enterprise value (EV) amounts to $15.6 billion. FY2022 Non-GAAP earnings came in at $713 million so Teradyne currently trades at a PE of 22 (on the EV basis). The cash conversion over the last couple of years hovered around 80% on average. This would result in a normalized free cash flow yield (FCF-Yield) of 3.64% which will be the basis of my DCF valuation.

Now here comes a problem. These numbers are a result of the downturn in the semiconductor test market in FY2022. To make up for the expected backswing once the market recovers, I will use the numbers from Teradyne's FY2026E Financial Model (refer to the slide in the "Market Outlook" chapter). I will assume the midrange of test revenue CAGR of 8-13% off 2022 until 2026 and industrial automation revenue CAGR of 20-30% off 2022 for a total revenue CAGR of around 12%. For a margin of safety, I will ignore the company's estimate that the EBIT-Margin will expand from 28% to 31-34%. After 2026, I will assume 6% growth into perpetuity (lower end of the overall semiconductor growth rate until 2030).

The overall return potential should be the sum of the FCF-Yield and the estimated growth rate into the future. In this case, this should be around 15.64% (12% growth + 3.64% FCF-Yield) until 2026 and then 9.64% (6% growth + 3.64% FCF-Yield) thereafter. This should lead to an overall return in the low double digits in the case that the valuation remains unchanged .

To gauge the potential effect of a valuation change, here are the numbers for a DCF valuation assuming normalized $3.66 FCF per share (3.64% x $100.64 share price), 12% growth rate until 2026, 6% growth thereafter and a 10% discount rate:

Teradyne DCF Valuation (moneychimp.com)

The current value per share should be around $120, leaving close to 20% upside from current levels. Should the company be able to deliver on their estimates that the EBIT-Margin expands until 2026, any kind of margin expansion will be a bonus.

Advantest

Author Note: I will mainly refer to the ¥ numbers and add the US$ numbers for valuation and per share metrics.

Advantest's last quote on the Tokyo stock exchange was ¥10,930 ($80.09) per share. One local share equals one ATEYY ADR. There were 183,969,601 shares outstanding at the end of the 3rd quarter for FY2023. After deducting the net cash position of ¥23.8 billion, the enterprise value amounts to ¥1.987 trillion ($14.56 billion). With TTM Net Income amounting to ¥126.2 billion, Advantest currently trades at a PE of 15.75. Same as Teradyne, cash conversion over the past few years hovered around 80% so the current normalized FCF-Yield stands at around 5.08%.

Advantest estimates to lose a bit of market share for FY2024 while the overall semiconductor test market is expected to decline a bit as well. S&P Capital IQ estimates FY2024 revenue to decline by around 7.5%. For the last quarter of FY2023, net income for the full year is expected to increase by around 2% compared to the current TTM numbers so I will factor in a 6% decline in earnings for the next year. After adjusting for these estimates, the FY2024 FCF-Yield should be around 4.8% which will be the basis for my DCF valuation.

Again, the total return potential should be the sum of the FCF-Yield and the growth rate. I expect that Advantest will be able to grow in line with the mid-range of the overall semiconductor market growth rate of 7% until 2030. So in this case the total return potential, assuming no changes in valuation , should be around 11.8% (7% growth off FY2024 + 4.8% FCF-Yield).

Assuming ¥522 ($3.83) FCF per share (4.8% FCF-Yield x ¥10,930 share price), 7% growth over the next 8 years and 6% into perpetuity (I will assume 6% growth into perpetuity because the high ROCE indicates a wide moat that should enable Advantest to keep growing inside their industry at a decent rate) at a 10% discount rate results in the following DCF valuation:

Advantest DCF Valuation (moneychimp.com)

The present value per share should be around ¥14,783 ($108.32) per share, indicating around 35% upside from current levels. As for Teradyne, should Advantest be able to expand margins (which might be possible because when Teradyne assumes a possibility of margin expansion that should be true for the main competitor as well), this would be a bonus to any possible returns.

Risks

In my opinion, there are three risks to keep in mind. I will go over each of them from most dangerous (1) to least dangerous (3):

(1) While the semiconductor market is expected to grow with a CAGR of 6-8% until 2030, it remains a cyclical market. Just ask investors in the memory space. There might be some major downturns in the whole industry in the future. If you are not able to stomach those kinds of downturns, Teradyne and Adantest are not good investments for you and you should probably stick with non-cyclical SWAN stocks. Selling when the semiconductor market experiences a downturn can be devastating for your overall returns. This is more of a psychological risk than a fundamental risk.

(2) I think that the semiconductor test market will grow in line with the overall semiconductor market (CAGR of around 6-8%). Several research portals expect the market to only grow with a CAGR of 3-5%. I outlined my thoughts in this article and came to the conclusion that I will trust the market estimates from Teradyne and Advantest as the dominant players in the field. However, you need to decide for yourself if you want to go with this or calculate more cautiously with the lower growth rates mentioned above. This would lead to completely different valuation expectations and might end with the conclusion that both companies are overvalued at this point.

(3) This is a risk for Advantest which is the currency risk. I highlighted in the introduction that I think the current strength of the USD/EUR in comparison to the YEN might act as a tailwind and boost fundamental returns. However, this might as well backfire when rates in the US and Europe stay high or move even higher while Japan keeps rates near zero.

Final Thoughts and Conclusion

Teradyne and Advantest dominate the semiconductor test equipment market with a combined market share of around 95%. While Advantest is a pure-play in this sector, Teradyne is diversified over some more industries while the semiconductor test market still accounts for around two-thirds of total revenue.

The overall semiconductor market is expected to grow to $1 trillion by 2030 for a growth CAGR of 6-8%. While some research portals indicate that the test equipment market will grow slower (3-5% CAGR) than the overall market, I think Teradyne and Advantest are right in their predictions that the test market will grow in line with the overall market.

The balance sheets of both companies are strong (net cash position throughout the whole last decade) and ROCE is consistently high which indicates a wide moat. The high ROCE, combined with sales growth as a result of the growing semiconductor market as a whole, resulted in exceptional returns over the past decade. My DCF valuations indicate that both companies are undervalued. Any potential margin expansion would act as a boost to total return expectations.

The current strength of the USD/EUR compared to the YEN might act as an additional tailwind when investing in Advantest and boost total returns if the value of the YEN starts to revert to the mean (when rates in the US/EU come down again). For EUR investors, an investment in Advantest looks much more compelling because the current strength of the USD might act as a headwind in the case that the federal reserve should start lowering rates in the future, resulting in the USD depreciating against the EUR.

Overall, I rate Teradyne a buy and Advantest a strong buy.

For further details see:

Teradyne And Advantest: A Duopoly In The Semiconductor Value Chain