TER - Teradyne: If A Significant Dip Arrives I Will Become A Buyer

2023-09-21 13:10:52 ET

Summary

- Teradyne specializes in automation and provides electronic testing services for several industries which are expected to experience sustained demand.

- They are a leader in collaborative robotics and are well-positioned to benefit from our continued transition toward automated manufacturing.

- Our presently elevated interest rates have been causing demand for some of their goods and services to temporarily diminish.

- With a PEGY of 2.752x and an Inverted PEGY of 0.3633x, I currently consider the company overvalued.

- I currently rate TER as a Hold.

Thesis

Demand for automated manufacturing is still on track to continue rising over the coming decades. With the Fed still fighting to lower inflation, and the United Auto Workers recently beginning their historic strike against the big three, I am looking for buying opportunities to appear in manufacturing and a handful of other affected industries.

Teradyne, Inc. ( TER ) is well diversified within the automation field. They have a culture of adaptation and have proven they are willing to do what it takes to stay relevant as technology progresses. By acquiring Universal Robots in 2017 , they expanded into a new synergistic moat and granted themselves a significant business life cycle extension. Because the automation industry faces decades of continued demand growth, I believe they are a long-term compounder and are likely to be able to maintain attractive returns for many years to comes. This is why Teradyne is on a short list of long-term automation plays which, if their shares ever go on sale for cheap enough, I am planning on eagerly buying with both hands.

Because of the macro conditions we are currently facing, I believe it is possible that we will be presented with such a buying opportunity at some point within the next few quarters. After looking over their financials and valuation, I currently rate TER as a Hold.

Company Background

Teradyne is an industrial automation and electronic testing company. They were founded in 1960 and are currently headquartered in North Reading, Massachusetts. I went further into their history of acquisitions in my last article about Teradyne , but they currently operate in four segments : Semiconductor Test, System Test, Industrial Automation, and Wireless Test segments.

- "The Semiconductor Test segment provides wafer level and device package testing in automotive, industrial, communications, consumer, smartphones, cloud computer and electronic game, and other applications."

- "The System Test segment provides defense/aerospace test instrumentation and systems; storage test systems, and circuit-board test and inspection systems."

- "The Industrial Automation segment offers collaborative robotic arms, autonomous mobile robots, as well as advanced robotic control software for manufacturing, logistics, and light industrial customers."

- "The Wireless Test segment provides test solutions for use in the development and manufacture of wireless devices and modules, smartphones, tablets, notebooks, laptops, peripherals, and Internet-Of-Things applications."

Long-Term Trends

The Electrical & Electronics Testing, Inspection & Certification market is projected to experience a CAGR of 5.17% until 2030. The Industrial Automation market is expected to have CAGR of 9.8% through 2029. The Collaborative Robotics market is expected to have a CAGR of 32% through 2030.

Why Collaborative Robots?

Collaborative robots, often shortened to c obot , incorporate feedback sensors which will halt motion in the event of contact with a collision. Unlike most industrial robotic arms, this means cobots are safe enough to work around while they are energized.

To give all of you context, several years ago we had a non-collaborative industrial arm donated to my school. Our administrators were originally planning on installing it into the corner of one of the labs so it would take up less classroom space. Their plan included installing a safety rail and light curtain to keep everyone out of the danger zone while it was in use. Another engineering professor and I realized this would not be good enough and had to call a meeting with our administration to make them aware that the location was unacceptable. This particular arm was hydraulic and originally designed to pick up car frames. It was capable of moving fast enough that it blurred and had a 600kg lifting capacity. If a student were to ever remove the lines of code which prevented it from slamming itself into the cinder block wall, it was capable of compromising the entire building. The appropriately nicknamed "death arm" was later installed far enough out into the center of the room that it would have been impossible to make contact with the walls.

Guidance

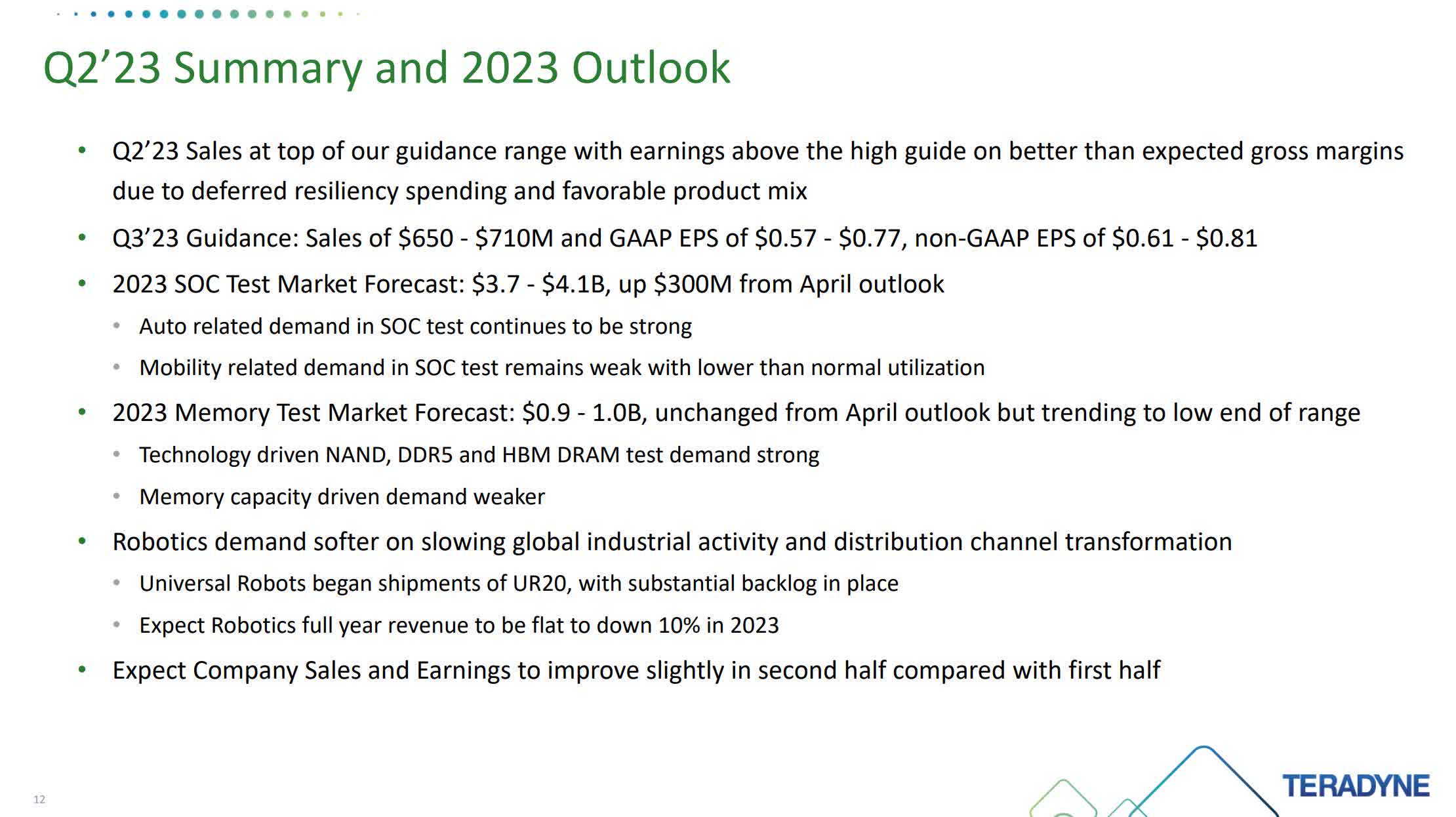

Their most recent earnings call revealed that their revenue for the second quarter fell into the top of the range for their previous guidance because supply constraints eased. This granted them higher than expected gross margins and resulted in earnings which were above expectations.

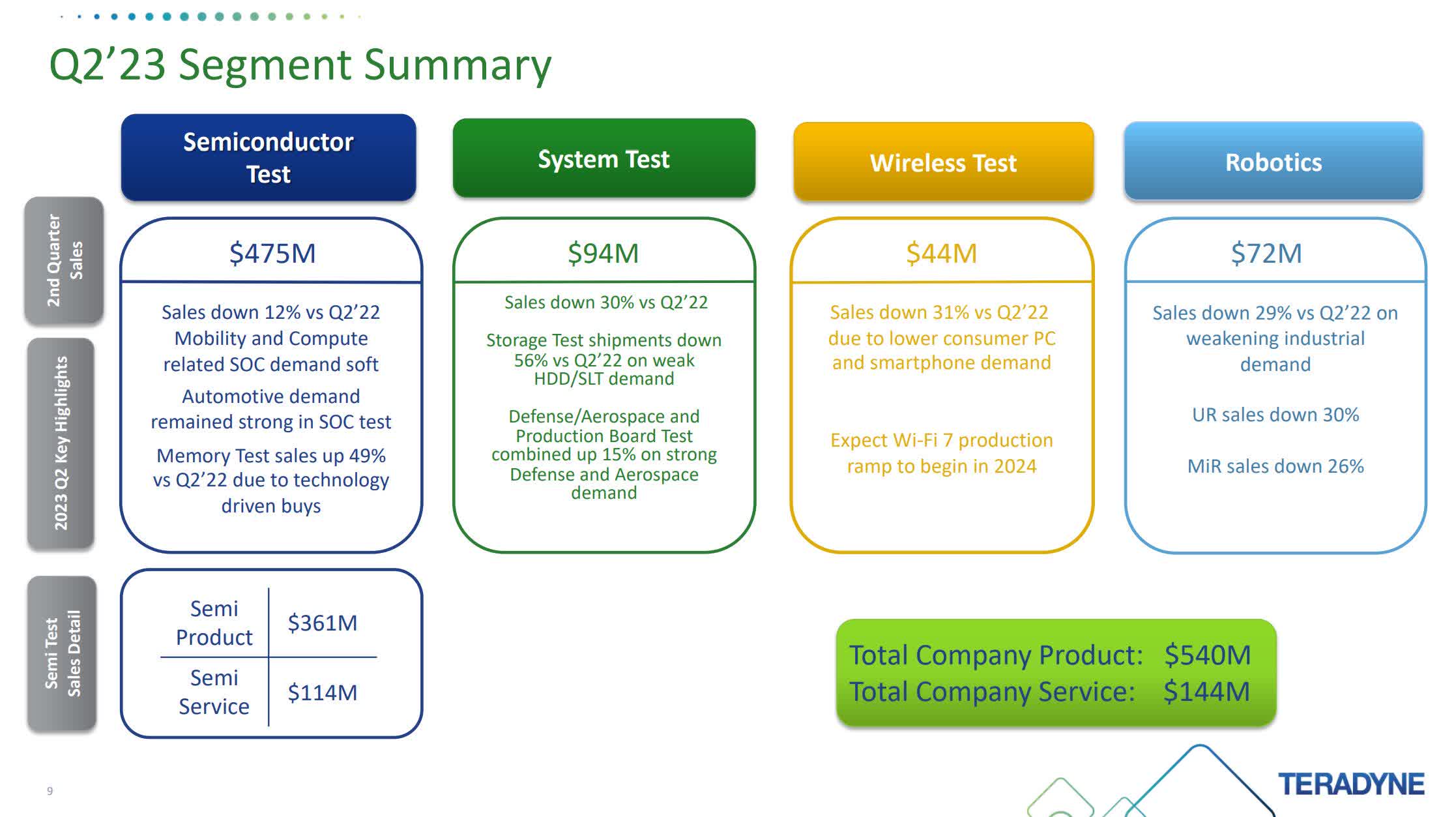

TER Segment Summary (Q2 2023 Presentation, Pg 9)

{kind=link}

In my last article I was talking about how I believed that the elevated interest rates were going to lower manufacturing demand. A few highlights from the transcript reveal the demand decline I was expecting are already beginning to show up in their guidance. This is hitting their revenue unevenly as their automotive and memory test segments are both still experiencing elevated demand.

- "Looking forward to the rest of 2023, we estimate the 2023 SOC test market will be $3.7 billion to $4.1 billion, down 13% to 21% from 2022. But up from our outlook in April. The continued weakness in mobility has been offset by sustained strength in the automotive segment."

- "In memory test, we expect the market will be at the low end of a $900 million to $1 billion range we described in April. In this market, the impact of AI is evident, especially in the HBM DRAM segment, where we see incrementally stronger test demand for Magnum products through the second half of 2023."

- "In the second quarter, robotics demand softened significantly. The trends that we noted in April have continued and intensified, challenging economic conditions, particularly low PMIs in Europe and the US have resulted in lower demand in our highest revenue regions. We have previously noted the channel transformation work at UR was having an impact on pipeline conversion. This trend has continued in Q2."

- "We saw record lead generation from two major automation trade shows in the quarter, but there's a clear reluctance from customers to place orders in the short term. As the result, we are now projecting full year revenue for our robotics group to be flat to down 10% from last year."

TER Quarterly Summary and 2023 Guidance (Q2 2023 Presentation, Pg 12)

{kind=link}

Annual Financials

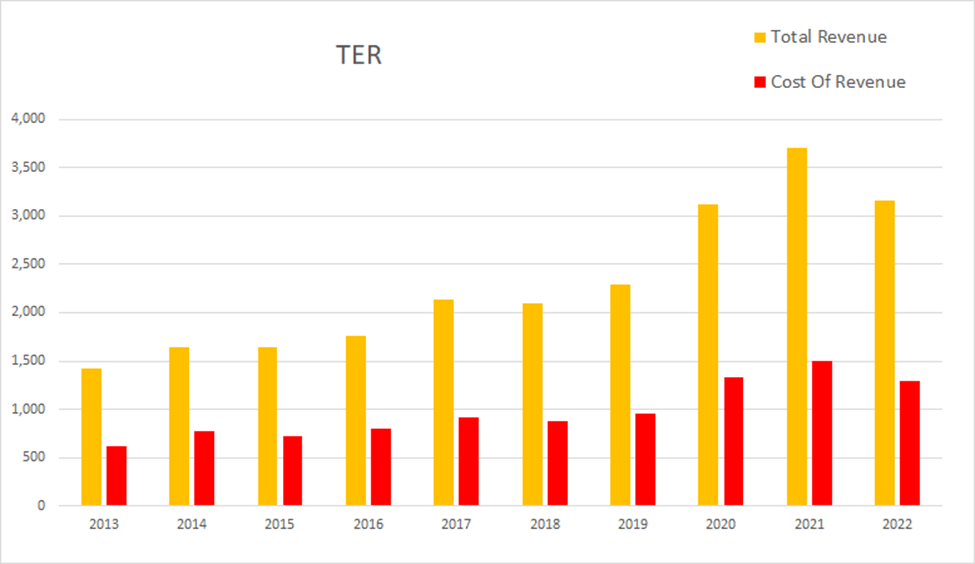

Teradyne has been growing revenue over the last decade. In 2013 they had an annual revenue of $1,427.9M. By 2022 that had grown to $3,155M. This represents a total rise of 120.95% at an average annual rate of 13.44%.

TER Annual Revenue (By Author)

{kind=link}

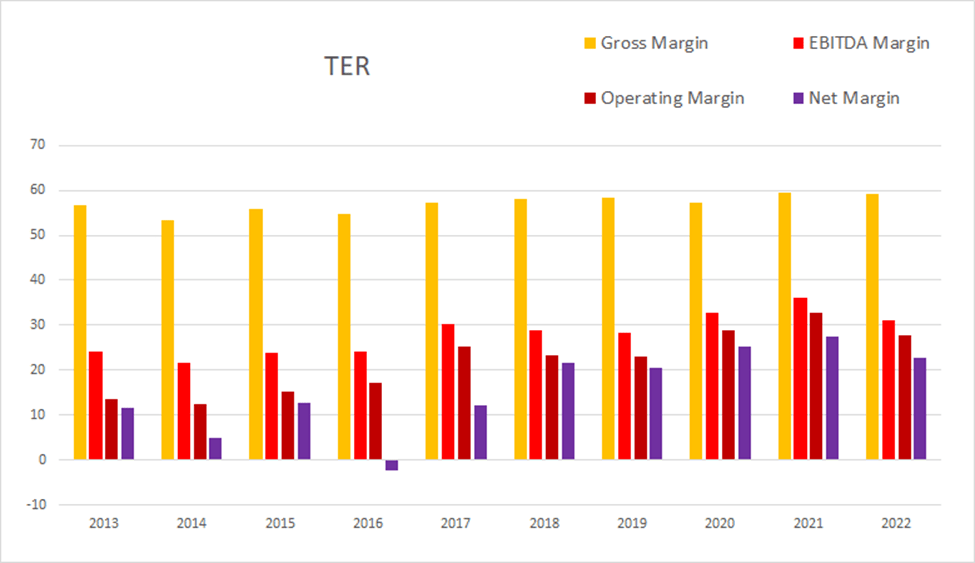

Their gross margins are consistently in the mid to high 50's. EBITDA, operating, and net margins have all experienced a significant expansion over the last decade. As of the most recent annual report, gross margins were 59.18%, EBITDA margins were 31.11%, operating margins were 27.60%, and net margins were 22.68%.

TER Annual Margins (By Author)

{kind=link}

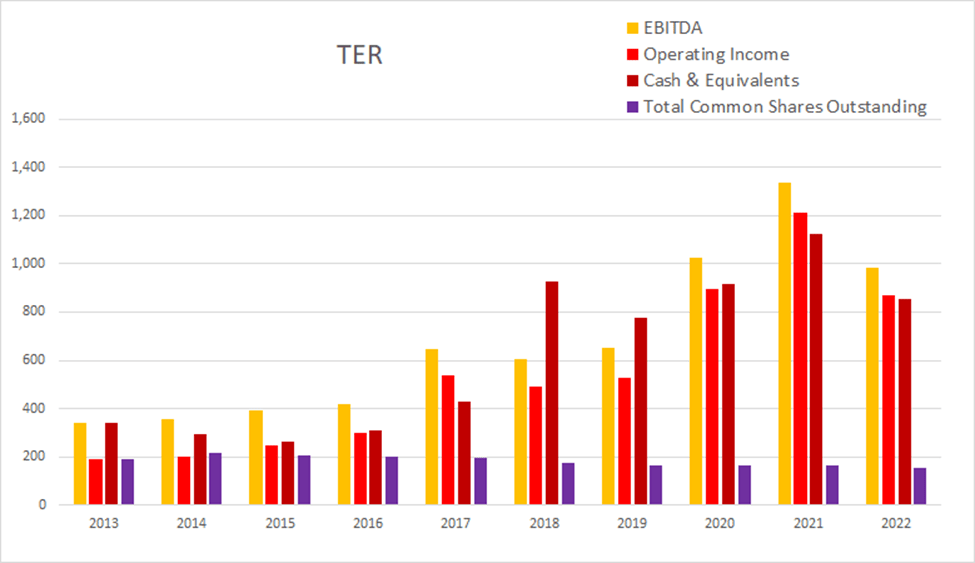

Teradyne has been buying back shares at an attractive rate. Total common shares outstanding was at 191.7M in 2013. By the end of 2022 that had dropped to 155.8M. This represents a 18.73% decline in share count, which comes out to an average annual rate of -2.08%. Over that same time period operating income rose from $192.2M to $870.9M, which is a 353.12% total rise, at an average rate of 39.24%.

TER Annual Share Count vs. Cash vs. Income (By Author)

{kind=link}

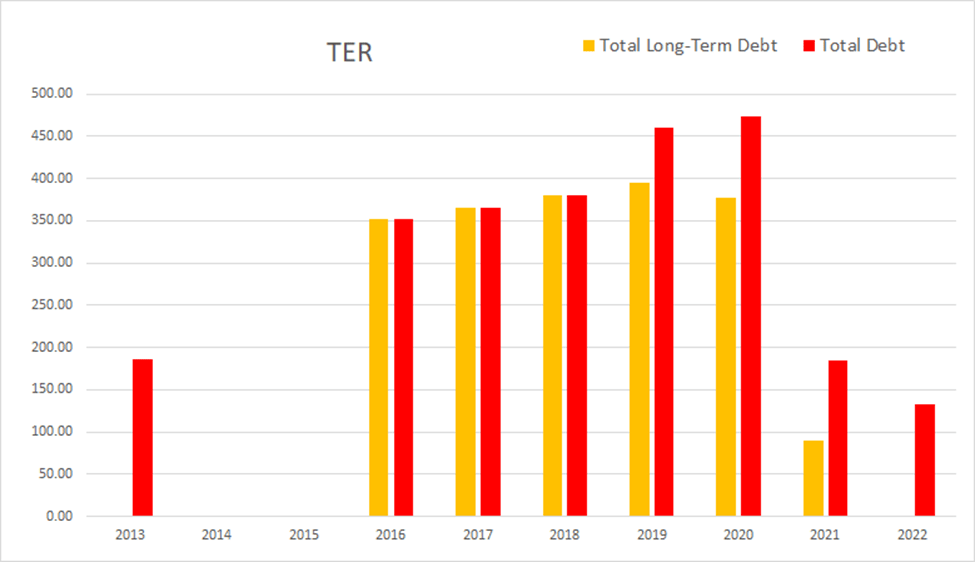

Teradyne has paid its long-term debt down to zero. As of the 2022 annual report, they only had $2.7M in net interest expense, total debt was $132.9M, and long-term debt was $0M.

{kind=link}

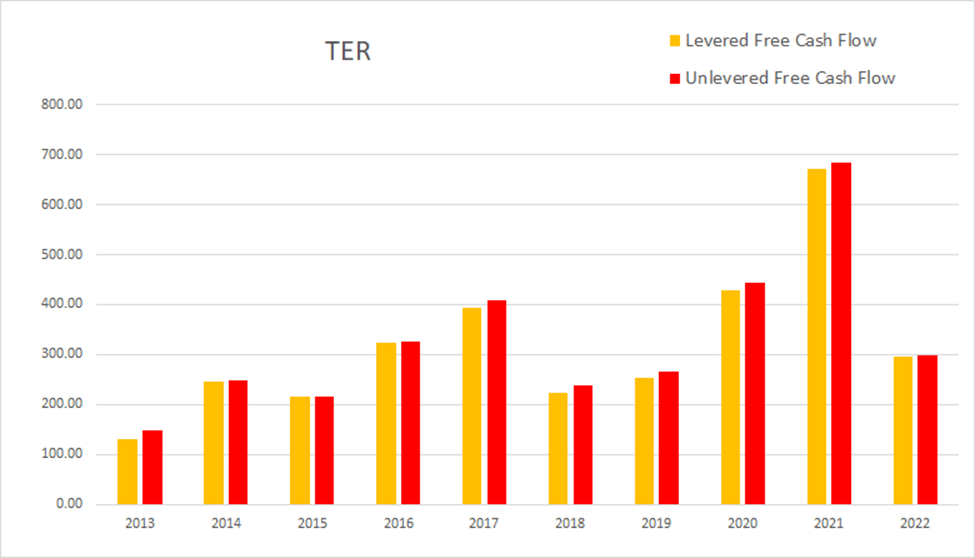

The company consistently produces positive cash flow. While it varies significantly from year to year, their cash flow appears to be improving over time. As of this most recent annual report, cash and equivalents was $854.8M, operating income was $870.9M, EBITDA was $981.6M, net income was $715.5M, unlevered free cash flow was $297.80M, and levered free cash flow was $295.50M.

TER Annual Cash Flow (By Author)

{kind=link}

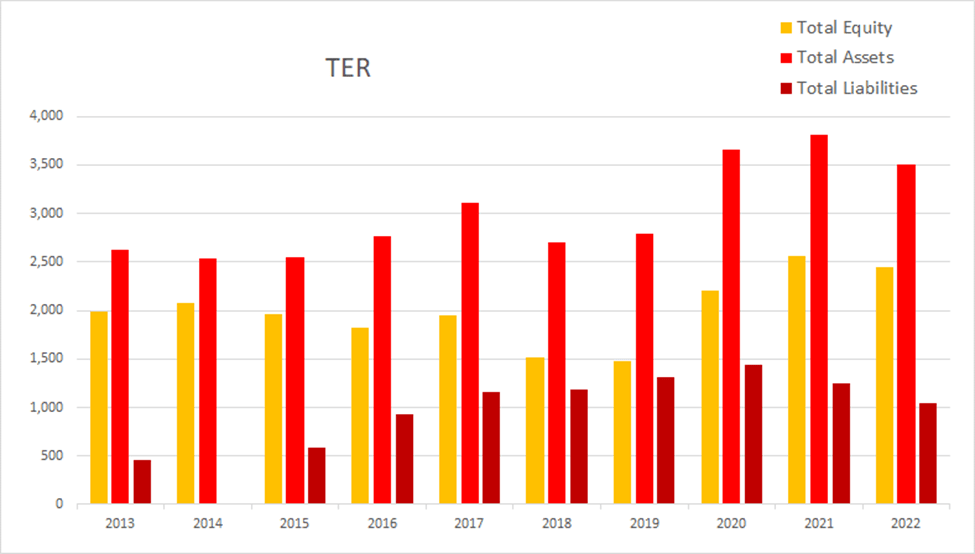

Their total equity was being warped by their debt situation. Both equity and assets have risen over the last decade.

{kind=link}

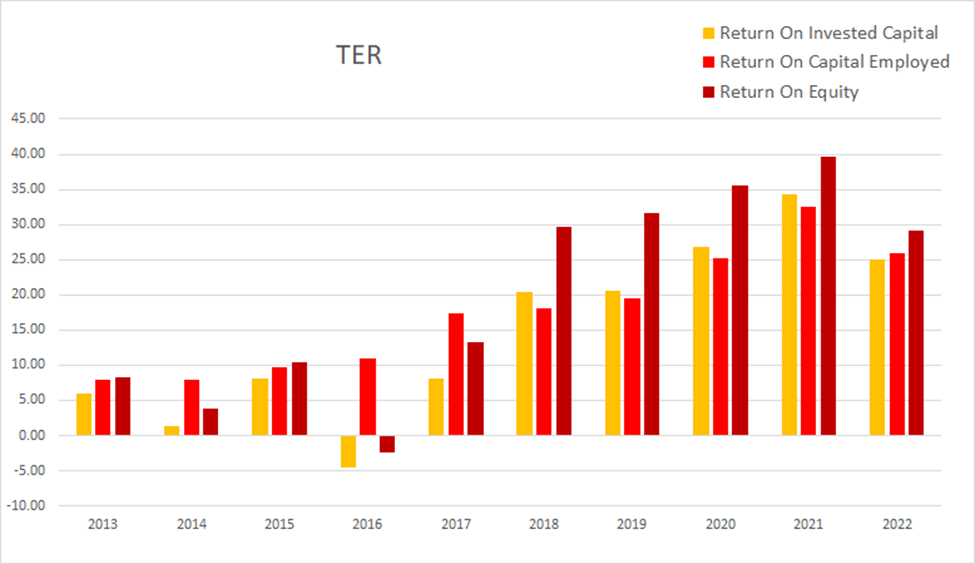

Their returns have become extremely attractive over the last several years. As of the most recent annual report ROIC was 25.03%, ROCE was 25.86%, and ROE was at 29.19%.

TER Annual Returns (By Author)

{kind=link}

Quarterly Financials

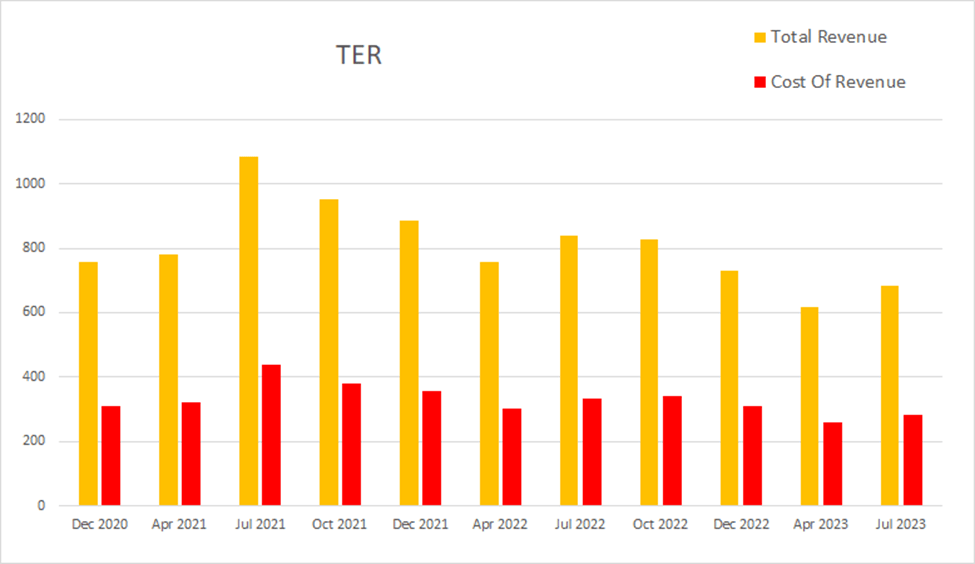

Their quarterly financials are more clearly showing the pace of their revenue decline. Eight quarters ago Teradyne had a quarterly revenue of $1,085.7M. Four quarters ago that had declined to $840.8M. By this most recent quarter that had dropped to $684.4M. This represents a total two-year decline of 36.96% at an average quarterly rate of -4.62%.

TER Quarterly Revenue (By Author)

{kind=link}

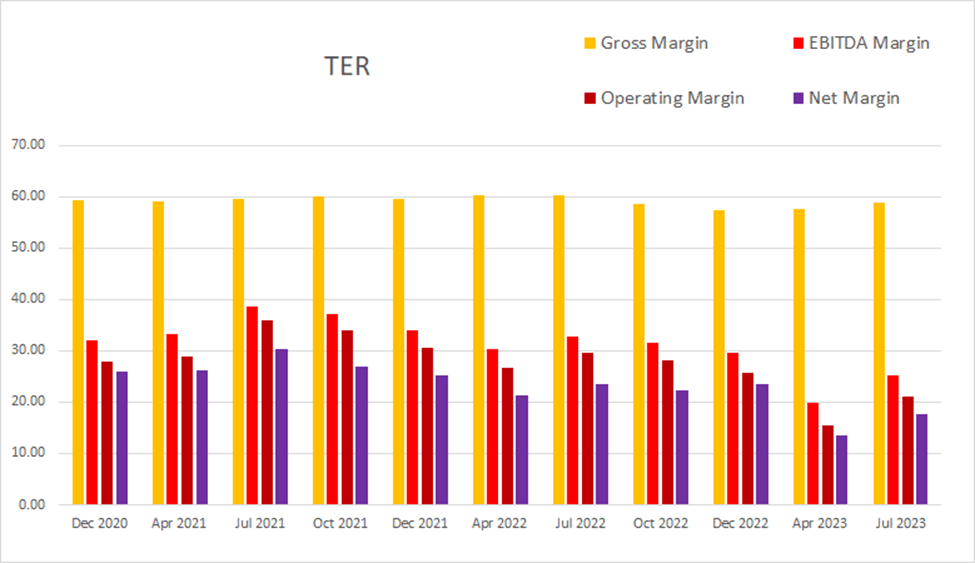

Their margins were quite consistent up until recently. I believe most of this contraction is due to a slackening of demand for some of their segments. As of the most recent quarter gross margins were 58.81%, EBITDA margins were 25.16%, operating margins were 21.19%, and net margins were at 17.55%.

TER Quarterly Margins (By Author)

{kind=link}

They buy back shares most quarters. The sum of their last eight quarters of buybacks comes to 7.03%; over the last four quarters it's 2.42%.

TER Quarterly Share Count vs. Cash vs. Income (By Author)

{kind=link}

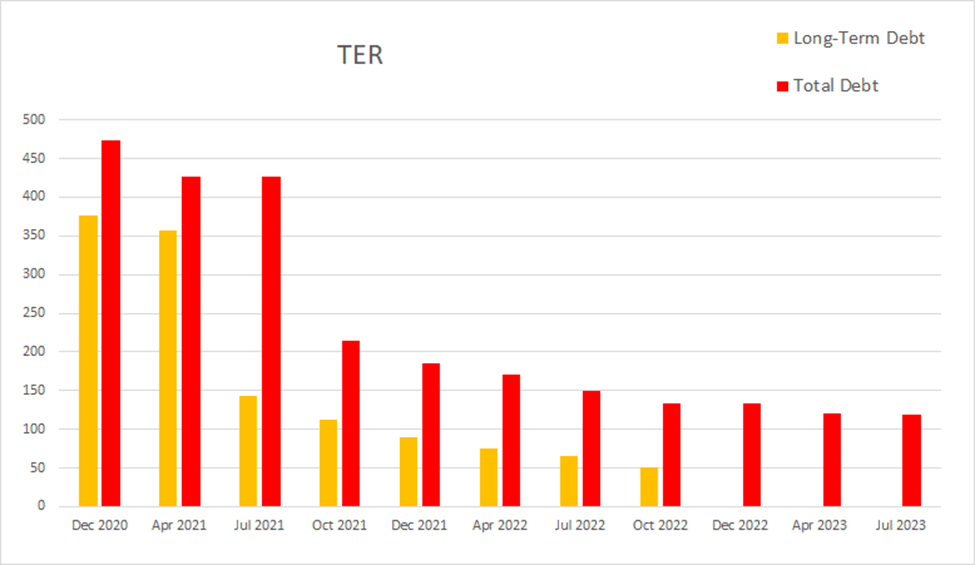

They have paid down their long-term debt, so their net interest expense is positive due to their interest and investment income. The most recent quarter, Teradyne had $5.3M in net interest expense, total debt was at $118.1M, and long-term debt was at $0M.

TER Quarterly Debt (By Author)

{kind=link}

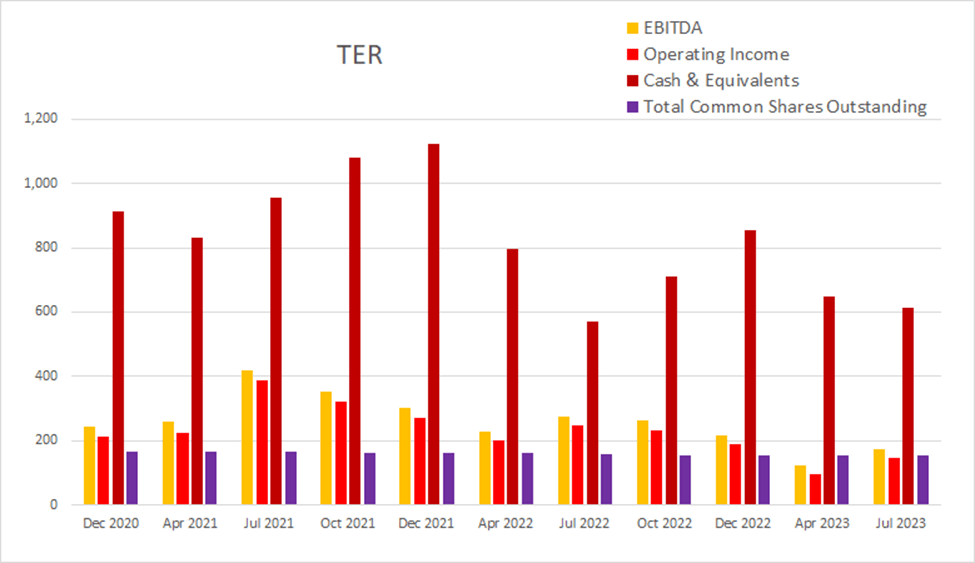

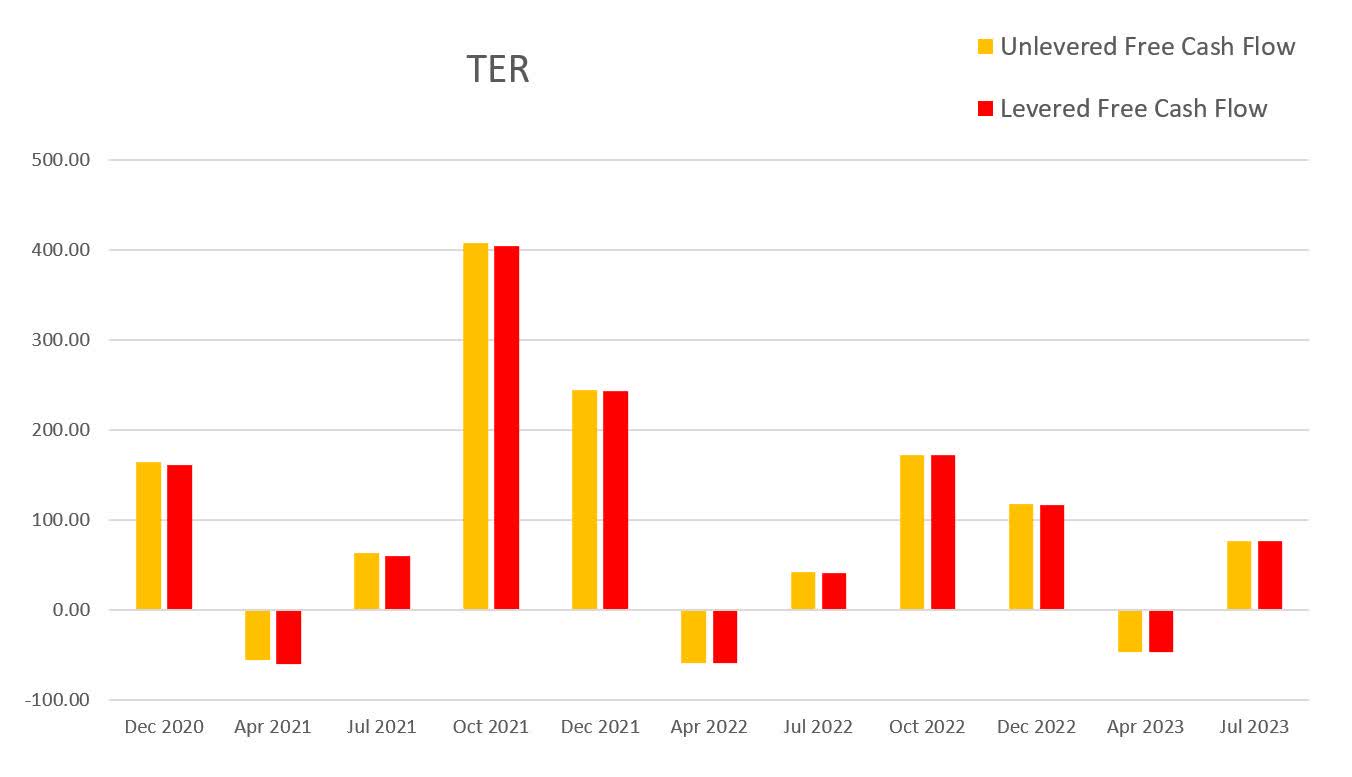

Although seasonality was more difficult to see when looking at revenue, margins, and income, it shows up quite clearly in their cash flow. Teradyne typically has less attractive financials every Q1 than the rest of the year. As of the most recent earnings report, cash and equivalents were $613M, quarterly operating income was $145M, EBITDA was $172.2M, net income was $120.1M, unlevered free cash flow was $76.8M, and levered free cash flow was $76.1M.

TER Quarterly Cash Flow (By Author)

{kind=link}

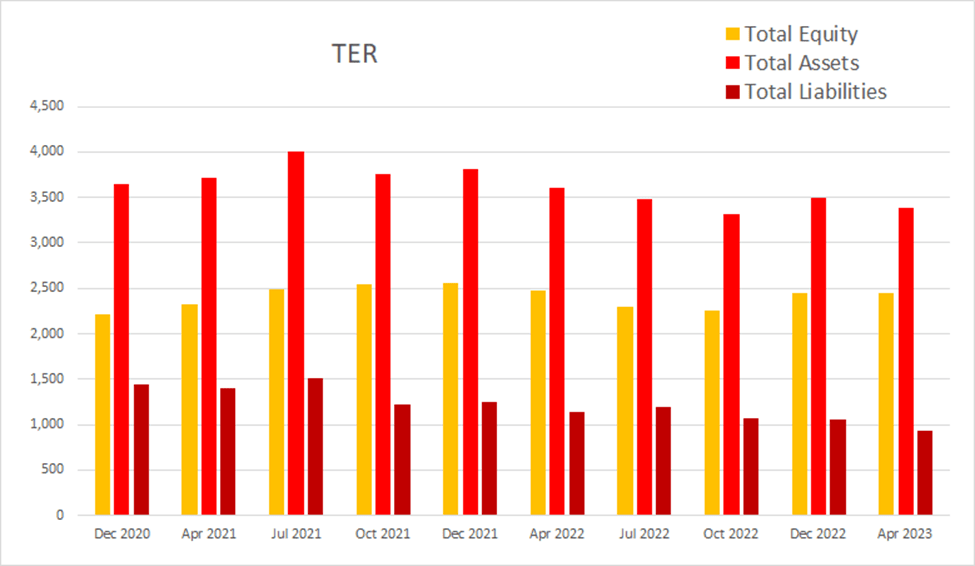

Their total equity appears to be slowly rising as liabilities drop.

TER Quarterly Equity (By Author)

{kind=link}

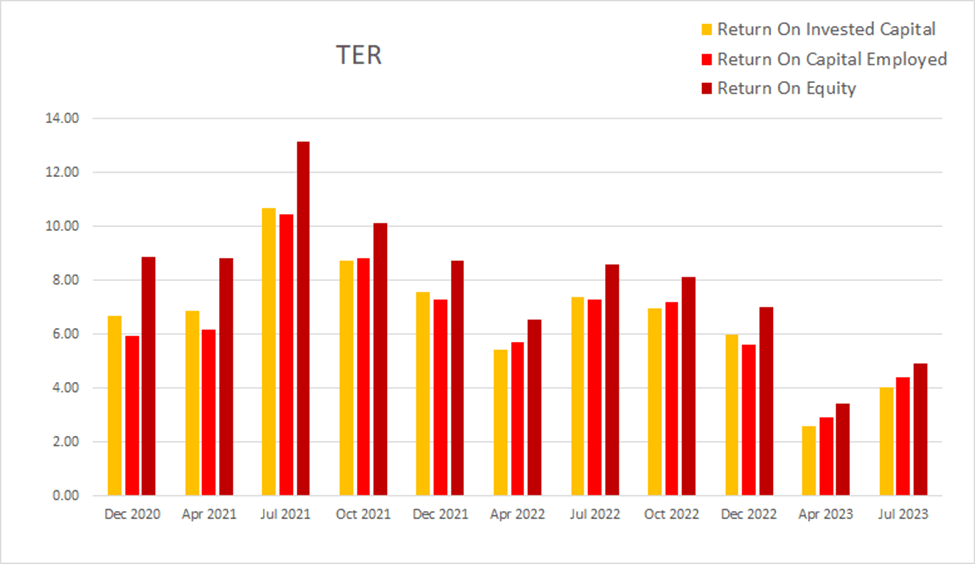

As to be expected, their returns appear to be dropping with their revenue. They appear to also be affected by the same seasonality that shows up strongly in their cash flow and less so in their margins. As of the most recent earnings report ROIC was 4.04%, ROCE was 4.43%, and ROE was 4.93%.

TER Quarterly Returns (By Author)

{kind=link}

Valuation

As of September 20th, 2023, Teradyne had a market capitalization of $15.06B and traded for $95.99 per share. Using their forward P/E of 35.81x, their EPS Long-Term CAGR of 12.56%, and their forward Yield of 0.45%, I calculated a PEGY of 2.752x and an Inverted PEGY of 0.3633x. These PEGY values imply that fair value is currently close to $34.87 per share.

When I tried looking at their longer timeframe valuation charts, their negative earnings value for 2016 was skewing them far too much. This is why both of the below charts only cover the last 5 years. Looking at their historical P/E over the last several years, it can dip below 20x and sometimes finds itself in the high teens.

TER 5-Year P/E (Seeking Alpha)

{kind=link}

Their EV/EBITDA chart is showing a similar story. Teradyne's valuation varies significantly but has stayed at or above around a 10x since it broke above 10x in 2019.

TER 5-Year EV/EBITDA (Seeking Alpha)

{kind=link}

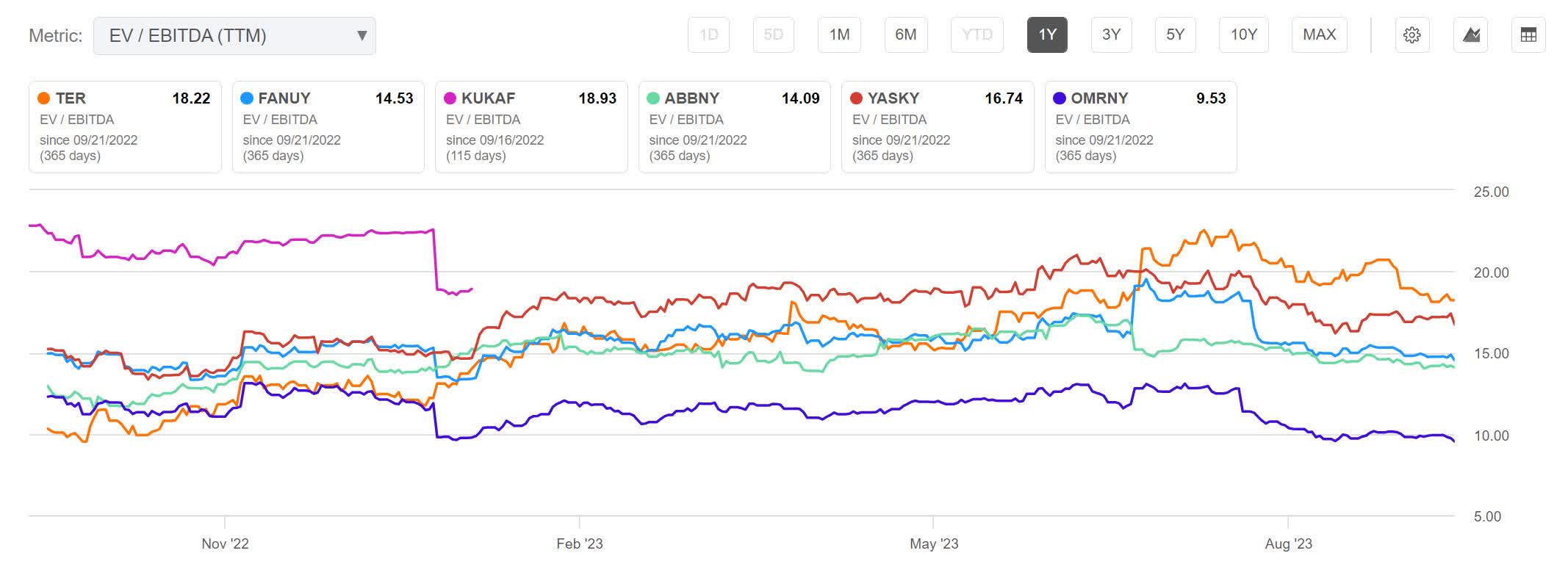

Teradyne produces more attractive returns than the rest of the robotics industry and typically trades at higher valuations.

{kind=link}

Because this company regularly trades with elevated valuations, I believe if I were to wait for the market price to fall close to its intrinsic value to buy, I may never get to own any Teradyne. For this reason, I will probably be forced to use historic valuations as a guide for what I should consider as "cheap" for Teradyne.

Risks

Teradyne has exposure to several industries. The cycles which affect those industries also affect Teradyne. The present United Auto Workers strike should affect revenue. If it were to become more severe or especially protracted, it may cause demand for Teradyne's auto-related services to suffer.

Teradyne has benefitted from a protracted AI craze. Demand for their testing services has risen. With most of the AI pure plays still a significant ways from finding profits, I have to believe that the euphoria will end before the industry will find its footing. If or when an AI winter arrives, I expect that the elevated demand the company has been blessed with will become a drought.

Teradyne is not the only company which makes industrial robotic arms. They face competition in this field from companies such as Fanuc ( FANUY ), KUKA ( KUKAF ), ABB ( ABBNY ), and others.

Catalysts

The company specializes in automation and provides services for several industries which are expected to experience sustained demand. Several years ago, while attending a robotics conference, one of the speakers was focused on what automation may look like in 2100. His "best case" scenario for the automation industry was that we would be able to replace up to 85% of today's labor tasks with automation. Because entirely new careers will be created, I do not believe this will translate to record breaking unemployment. However this should help explain why I believe the robotics and automation industry will experience sustained demand growth for decades to come.

While their current situation is characterized by slackening demand, Teradyne has several factors that contribute to their net demand. When the UAW's current strike ends, or if the AI euphoria elevates even further, the company may enter a period characterized by rising demand and earnings. Because of the cyclical nature of the industries they provide services for, Teradyne can expect to experience regular cycles of higher and lower demand.

Conclusions

In case you haven't caught on yet, I strongly believe in Teradyne's long runway and the opportunities it provides for long-term success. It is difficult to tell how deep their moats are, but I believe it has established itself as an important player in automation. Similar to Microsoft ( MSFT ), Teradyne has stayed relevant for decades in a highly-competitive industry. Both companies have achieved this by purchasing synergistic technology as it emerges.

I often find myself raving about how attractive it is to invest into companies which are innovators and adaptors because of their disruptive nature. However, repeatedly purchasing business life cycle extensions has its own advantages. These companies save on both R&D costs and sweat equity. They can wait on the sidelines while a new technology emerges and see how things develop as it approaches maturity before stepping in and buying. This has the added advantage of allowing Teradyne to choose from among several options and purchase the version of the technology which is the most synergistic with their current operations. I believe their acquisition of Universal Robots in 2017 will not be the last time they expand their business model in order to stay competitive.

With the yield curve inverted and the Fed still maintaining elevated rates to fight inflation, I believe we are still facing a recession. The soft-landing narrative currently being pushed on us may not materialize before stagflation takes over. However our current situation develops, I expect the economy to slow down and for the valuations for many companies to lower. I am patiently waiting for a potential recession to produce buying opportunities in several industries. Because of their already established moats and significant runway, Teradyne is one of the ones I am the most eager to buy.

For further details see:

Teradyne: If A Significant Dip Arrives, I Will Become A Buyer