TER - Teradyne: Improving Its Supply Chain And Profitable But Not The Time To Buy

Summary

- Teradyne is a supplier of equipment for testing and industrial applications.

- It is on track to achieve its second-highest revenue in its history despite some demand concerns, after having fixed supply-side issues.

- On the other hand, it is growing slower than competitors and the change in leadership at the top implies strategic changes.

- In these conditions, the stock is more of a hold.

Teradyne (TER) is a supplier of equipment for testing and industrial applications. The Company's Automated Test Equipment ("ATE") products are used to test semiconductors (chips) in wireless, memory, and complex electronic systems in order to ensure that they are top quality.

The stock has been underperforming the semiconductor sector symbolized here by the iShares Semiconductor ETF ( SOXX ) by about 12% since analysts at Stifel downgraded it back in January last year and lowered their price target to $115, down from $160 after the company suffered from a significant revenue shortfall and provided lower guidance.

Thus, my objective with this thesis is to assess whether the test equipment designer and manufacturer has recovered in what has been mostly an uncertain macroeconomic environment, especially given that its CEO had earlier mentioned that "Despite the drop in demand in the second half, we're on track to deliver our second highest revenue in history". For this purpose, I will consider the industry perspective, the competition as well as the supply chain for this manufacturing play.

I start by diving into the financial results for the third quarter of fiscal 2022 (Q3).

Revenues and Memory Strength

Teradyne's sales at $827 million were above the midpoint of its guidance in revenue. However, this was lower than in the same period last year as shown in the table below, due to a weakness in industrial automation, as had been forecasted by the management back in July. There was also some softness in the SOC or System on Chip and wireless testing devices businesses in turn caused by declines in the demand for smartphones, computing, and related products.

Quarterly Revenues (www.seekingalpha.com)

As for Profitability, the GAAP EPS (earnings per share) of $1.10 beat estimates by $0.08 .

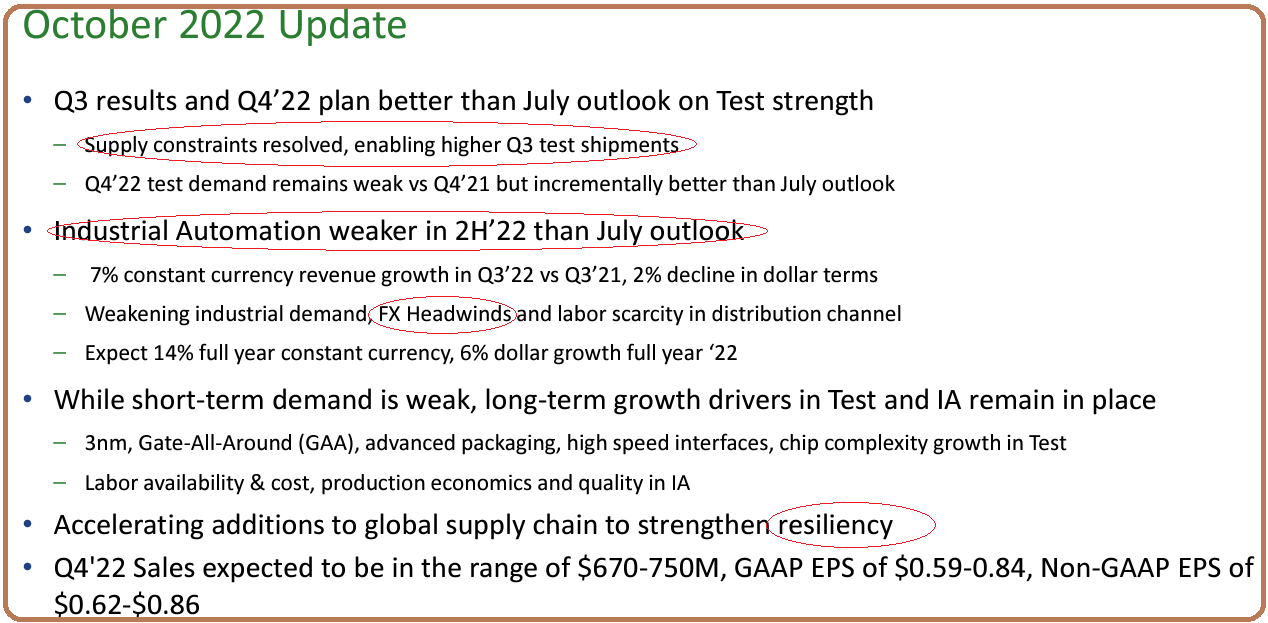

This was due to the resolution of some supply chain bottlenecks that allowed more chip shipments to customers than had been initially planned thereby contributing to more sales. Also, despite the fall in revenues, the company has maintained its gross margins at 58.7% (above table) despite having less of a revenue base on which to spread its fixed costs. This highlights cost control which is not always possible when you do not have full visibility on the demand side as is the case for Teradyne, which does not sell directly to end consumers like you and me. In order to address this shortcoming, the company updates its forecast every three months as pictured below.

October 2022 Outlook (static.seekingalpha.com)

{kind=link}

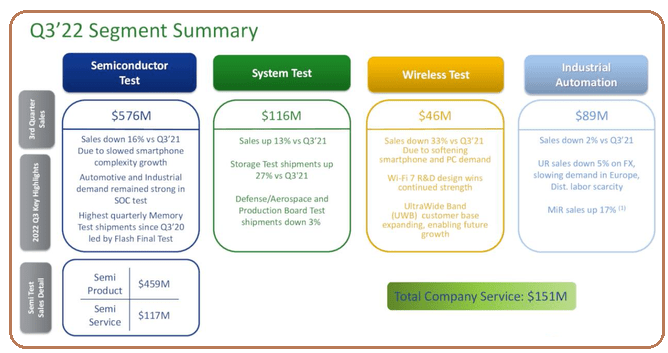

As seen above, the ability to address supply constraints helped in generating the " highest level of memory shipments" in two years at $125 million. Adding the $451 million obtained from SOC total revenue for the Semi Test revenue was $576 million.

Now, we are seeing uncertainties in the memory sector, namely with producers Samsung Electronics' (SSNLF) profits dipping by 23% due to pricing pressure and Micron's (MU) being close to the bottom . Now, it may sound strange that Teradyne has not suffered from this weakness in memory. The reason is that as part of the product cycle, server OEMs have to transition to new memory standards, both for flash and DRAM, which necessitates new testing devices produced by Teradyne and peers. There has also been strong demand from indigenous China customers, or local memory manufacturers which produce for the Chinese market.

As for SOC, there are long-term opportunities due to the higher dose of semiconductor content in electric vehicles or EVs. Also with more infotainment devices like advanced touchscreens mounted on the car's dashboard, automobiles are becoming more "computerized" thereby needing more chips compared to their predecessors. The company also saw continued strength in industrial analog with its simple but high-accuracy devices focusing on testing power management integrated circuits.

Second Highest Revenues despite Weakness in IA

Therefore, Teradyne can rely on SOC and memory for growth, but, in the meantime has improved its supply chains and diminished bottlenecks which should reduce revenue shortfalls from $50 million in Q3 to approximately $15 million in the fourth quarter (Q4).

Segmental Summary (investors.teradyne.com)

{kind=link}

Also, there is a possibility of Forex tailwinds in Q4.

In this respect, weakness in Industrial Automation which contributed $89 million in Q3 as pictured above was attributed to lower European demand, labor scarcity in the distribution channel, and Forex headwinds. In this case, as for many other U.S corporations exporting products to the rest of the world, the strong dollar reduced revenues reaching the income statement after converting from weaker currency overseas sales.

Noteworthily, at the time this forecast was made in October, the dollar was at a year high and has now depreciated by about 6% . Therefore, Teradyne could see better sales in Industrial Automation in dollar terms in Q4.

Along the same lines, according to the guidance, Q4's revenues will be $710 million (midpoint of $670 million and $750 million). Adding this amount to revenues from the first three quarters, I obtain $3.1 billion for FY2022, which, if things go as expected will effectively constitute the second highest revenues in the company's history. This amount is lower than 2021's 3.7 billion which was a record year especially due to the digital transformation requiring more chips and by ricochet, more testing devices.

The Industry Perspective, Market Share, and Valuations

To put this fall in revenues from 2021 to 20211 in the context of the wider industry, according to the SIA (Semiconductor Industry Association), global chip sales hit a record in 2021 at $555.9 billion, which is up 26.2% compared to 2020. However, it is expected to grow at only 8.8% in 2022. Hence, after a record 2021, the softness seen for Teradyne appears something normal.

However, this is far from the case when glancing at Teradyne's competitors. Here, Advantest (ATEYY) and Cohu (COHU) which also produce semiconductor test equipment were less impacted as shown in the orange and pale blue charts respectively. Pursuing further, Advantest which together with Teradyne had about 30% of the global market share for ATE back in May 2022 according to data compiled by Khaveen Investments , has been growing aggressively in the last four quarters as shown by the orange chart below. This could imply that Teradyne may be losing market share in testing which brought 88% of total revenues in Q3.

This said, the company should continue to benefit from testing needs for memory and SOC, but with a valuation score of "F", which means overvalued, this does not constitute an opportunistic buy, but, rather one which you want to put on your observation list. Another reason for this is the CEO change to be effected next month, which may bring a significant change in the strategy and execution.

Discussion and Conclusion

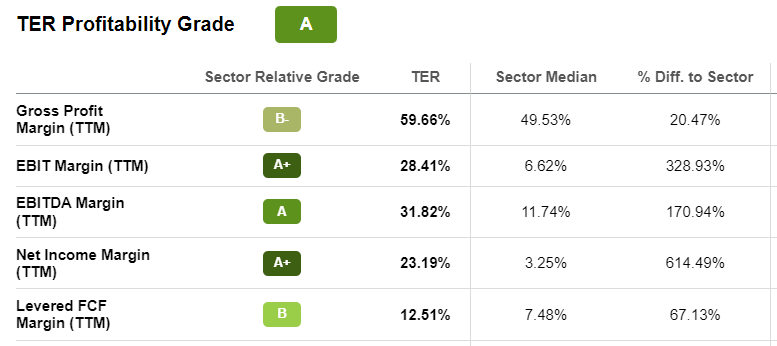

Therefore, it is more of a mixed picture for Teradyne. The company has some strong points especially in terms of profitability as I mentioned earlier and which is confirmed by its " A " profitability grade as pictured below. This includes the FCF margin which is a key metric to consider when the Fed is tightening monetary conditions and is one of the reasons why most SA contributors have been bullish on the stock.

Profitability Metrics (www.seekingalpha.com)

{kind=link}

Another of its strength is its out-of-China supply chain strategy.

The company has a large manufacturing footprint in China, and as part of its business continuity planning, it has added additional global capacity for these activities at an accelerated pace in 2022. This diversification strategy away from China should reach completion for the manufacturing part sometime this year.

On the other hand, while the U.S. government restrictions to deny China the most advanced AI chips in September last year, as well as the equipment to produce them, should not impact Teradyne in the short term, it will certainly take a toll in the future as the country recalibrates its chip industry.

Moreover, while Teradyne looks on track to achieve its second-highest annual revenues, its competitors are increasing sales much faster. At this stage, some may argue that its Industrial Automation offerings are promising for robotics in manufacturing, but, this segment as pictured above only accounted for only 12% of revenues in Q3. Therefore, one of the strategic imperatives for the new CEO who is President of Teradyne's Industrial Automation Group could be to promote inorganic growth through acquisition as the company disposes of a cash pile of $753.4 million , net of debt.

Finally, being aligned to SA Quant's position, I have a hold position on the stock, but, this said, after a 45.6% downside, there could be a surge as growth investors are regaining lost enthusiasm following a decrease in wage growth as per the latest job report, which implies that the U.S. central bank may be less aggressive in the way it hikes interest rates.

For further details see:

Teradyne: Improving Its Supply Chain And Profitable But Not The Time To Buy