BYDDY - Tesla Set For Continuing Sales And Revenue Growth In 2023

Summary

- Tesla, Inc. auto sales have continued to grow strongly around the world.

- Capacity is growing rapidly and new products will launch in 2023.

- Energy storage growth will kick in rapidly and be a long-term gamechanger for the company.

- Tesla stock is not in favor with investors and will probably tread water in 2023 despite being a leading player in the new economy.

- Short-term price cuts by Tesla will greatly harm legacy auto's efforts to get a slice of the EV pie.

The Tesla, Inc. ( TSLA ) stock price is reeling from the bear market and from being out of favor in the public eye and from short-sellers. However, as my article in October detailed, the company is actually in great shape.

Demand for its autos has grown at a tremendously rapid rate. That is why the company is ramping up production around the world. Increased production facilities will come online in North America and in Asia in 2023 and 2034. My article in September illustrated the way in which Asia will drive much of this growth.

New products coming onto the market in 2023 will include the Cybertruck and Semi, and probably lower-cost versions of the Model Y and Model 3.

The under-estimated energy storage line is kicking into gear and will become a significant revenue earner for the company. My article in July explained how this will happen.

However, I would not especially recommend buying Tesla stock at this point. History shows that when high flyers crash to earth on U.S. stock markets, it takes a long time to regain former highs, if ever. Long term, Tesla remains a great investment, though.

The Auto Demand Picture

What fell in 2022 was not Tesla sales but the expected numbers posited by analysts. The health of companies is not decided upon by analysts. They often have their own agendas or do not understand a company properly.

For 2022 as a whole, Tesla vehicle deliveries rose by 40% to 1.31 million and production rose 47% to 1.37 million (the difference being vehicles in transit to customers). This does not quite equate to headlines one sees about Tesla demand falling. In fact, it is an amazing feat in a year of world recession and Covid shutdown in China.

Tesla's recent price cuts are spurring demand strongly. Profit per unit will decline somewhat. However, with economies of scale and increased battery supply, Tesla can still greatly increase revenue and maintain its gross profit superiority over other brands.

In the USA, this should cause severe problems for the likes of Ford ( F ) and General Motors ( GM ). They are already late to the party and struggling with huge debts, with setting up new plants, and absorbing stranded assets from the declining ICE business.

In China, price cuts are part of the strategy to fight it out with the other serious world player on the electric vehicle ("EV") stage, BYD Company Limited ( BYDDF ). Apart from dominating the world's largest car market, these two will fight it out in the burgeoning European and Asian markets. Worldwide, about 5% of cars sales in 2022 were EVs. Within about 20 years, 100% of cars sales will likely be EVs.

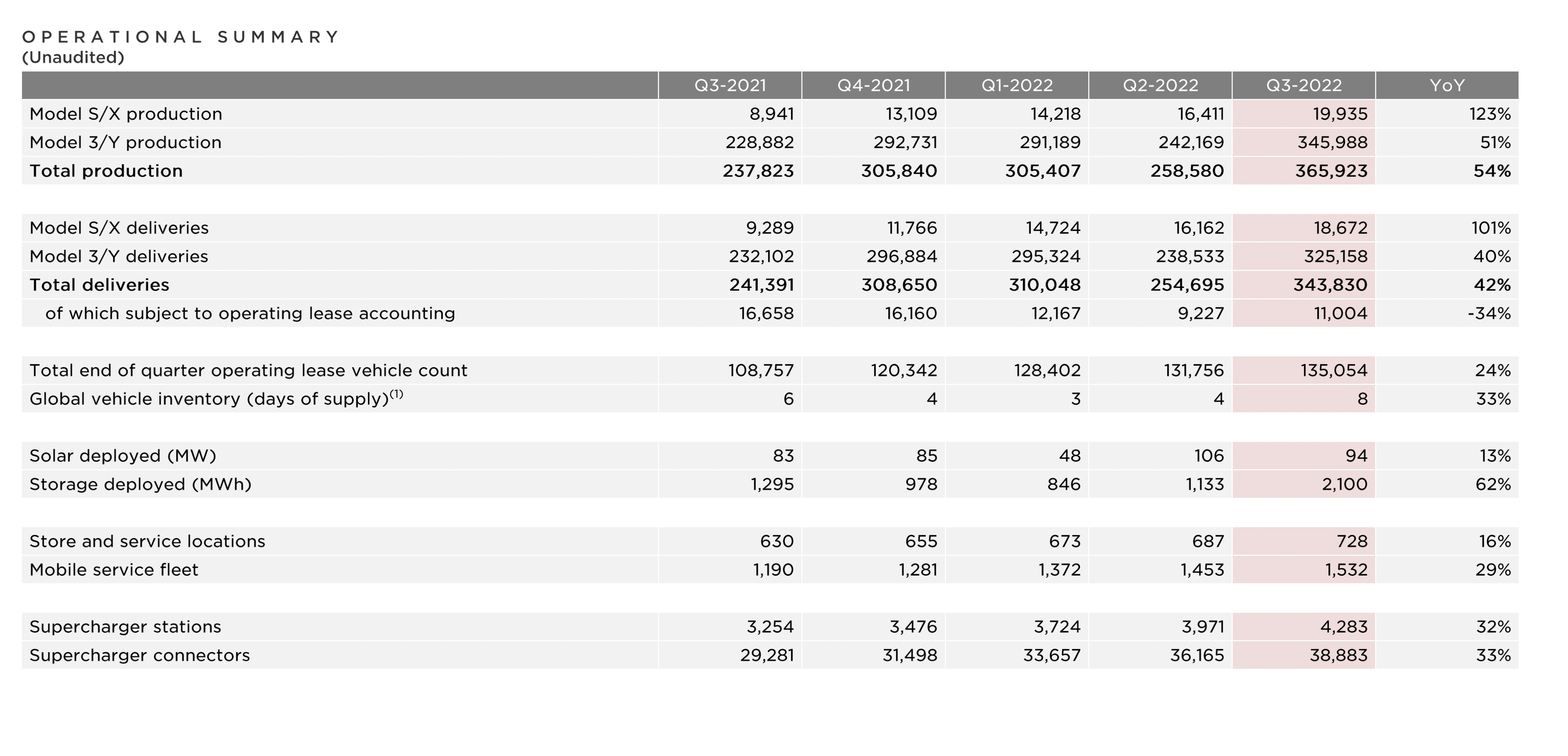

The Q3 2022 production figures had shown an increase of 54% year-on-year, as illustrated below by model.

{kind=link}

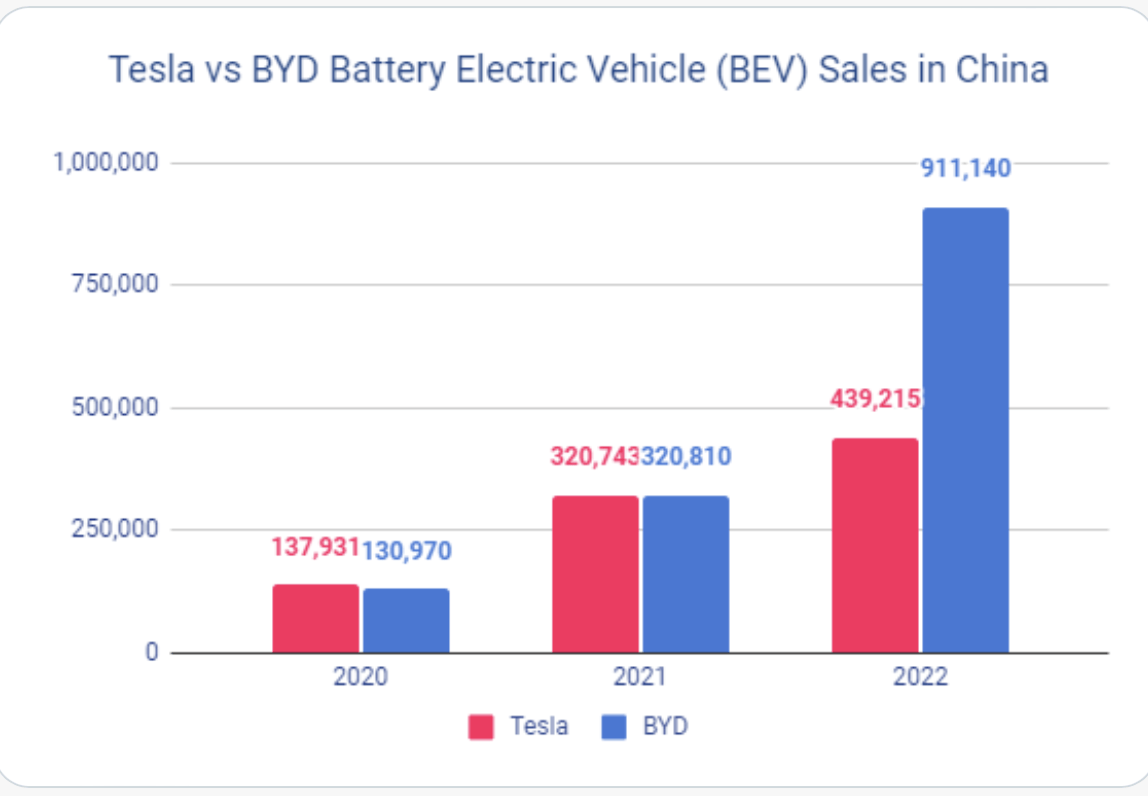

The World Market - Asia

China is the world's largest auto market. To an even greater extent, it is the world's largest market fo r EVs. As illustrated below, Tesla continues to increase sales dramatically. This is happening less rapidly, though, than BYD Auto, the world's largest EV company:

{kind=link}

Tesla and BYD continue to dominate the world's EV market (and, as my recent articles show, my rating for BYD is a very strong BUY).

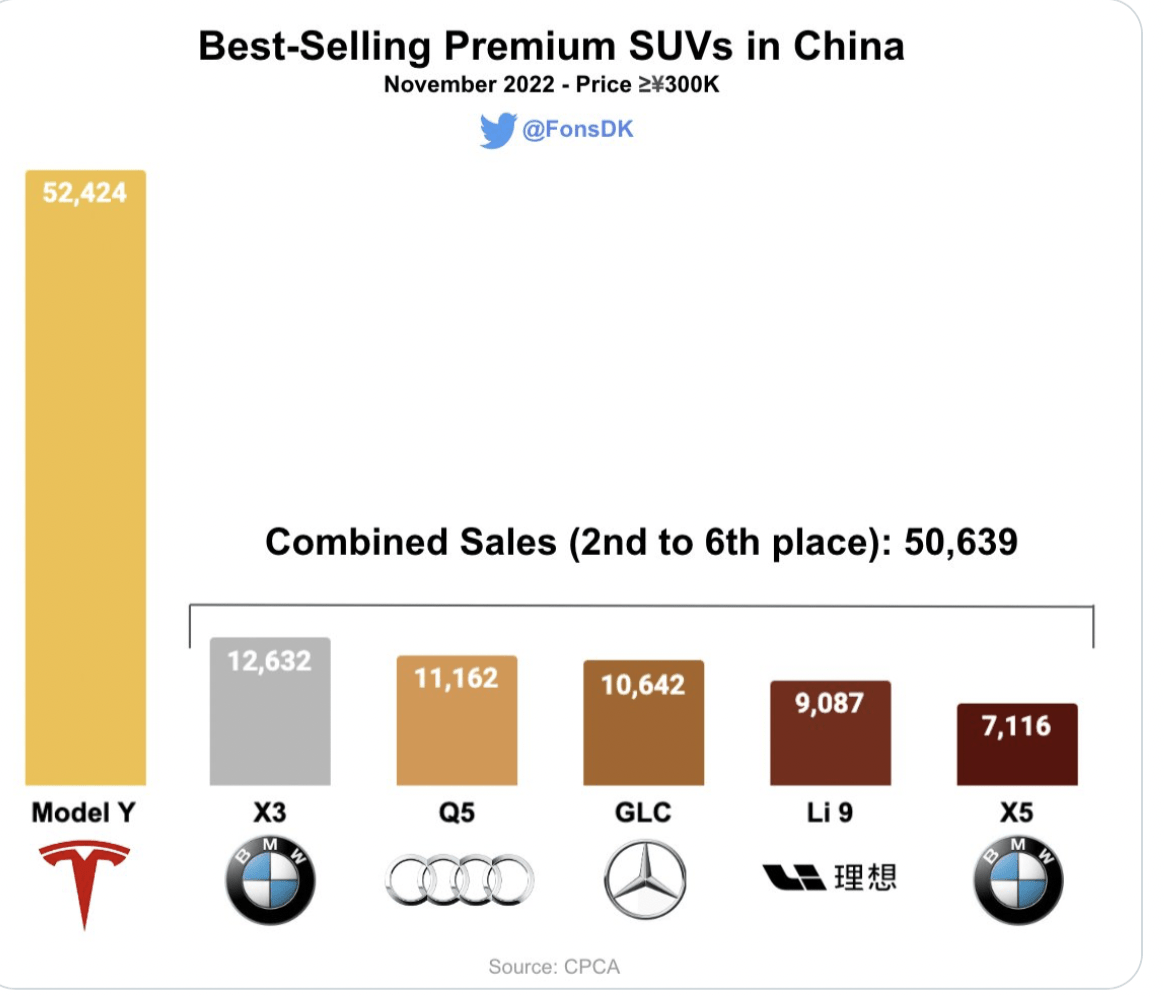

At the higher end of the market in China, Tesla has dominated, as the chart below illustrates :

{kind=link}

BYD has been moving into Tesla territory though, especially with the "Seal" model retailing at about $37,000. Tesla recently cut its prices to meet this challenge. The standard Model 3 was reduced by 13.5% to $33,515. The standard Model Y was reduced by 10% to $37,899. BYD has just introduced a new luxury "Yangwang" brand to take on Tesla at higher model levels.

The price discounting going on is not substantially an issue of falling demand. It is a matter of in/out costs for manufacturers falling and fierce competition for market domination between Tesla and BYD.

Whether the competition is legacy auto or new EV companies from China, they fall far behind the two giants of EVs today.

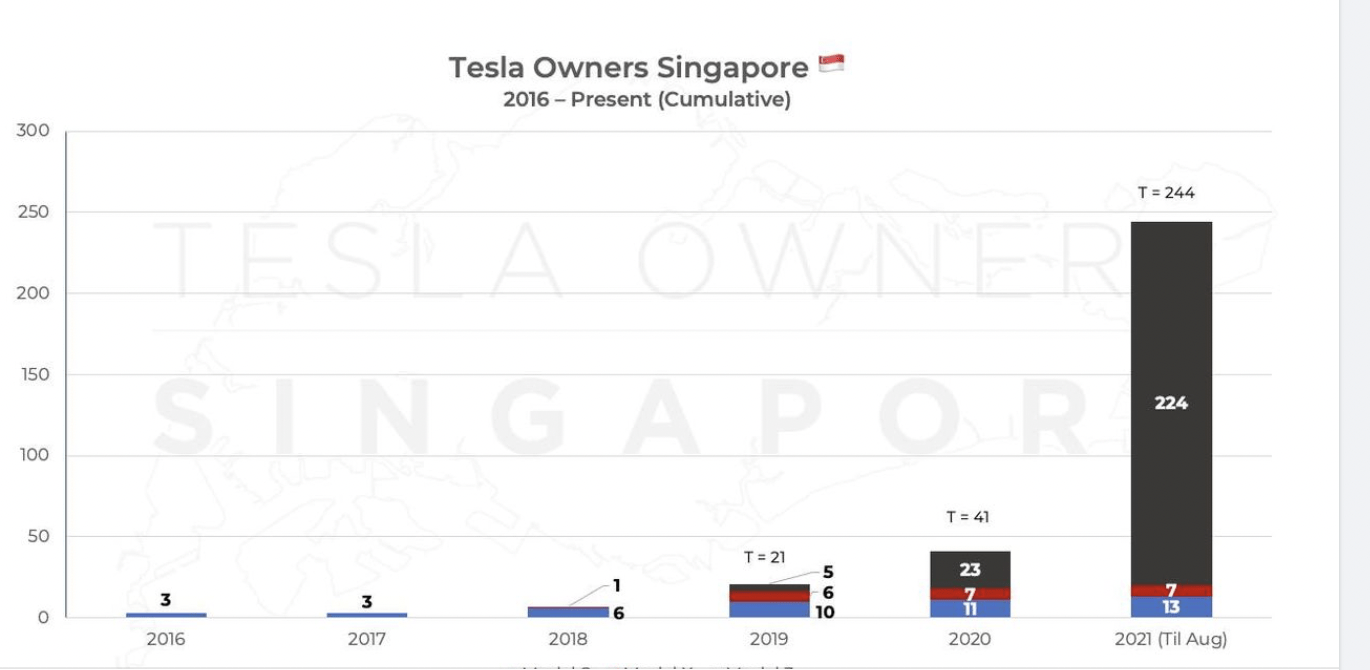

All around Asia, the same story can be told, as the company tries to meet the soaring demand in markets big and small. Singapore is an example of markets rapidly building up as supply becomes available:

{kind=link}

The only reason this did not happen sooner was because Tesla has been supply-constrained, not demand-constrained.

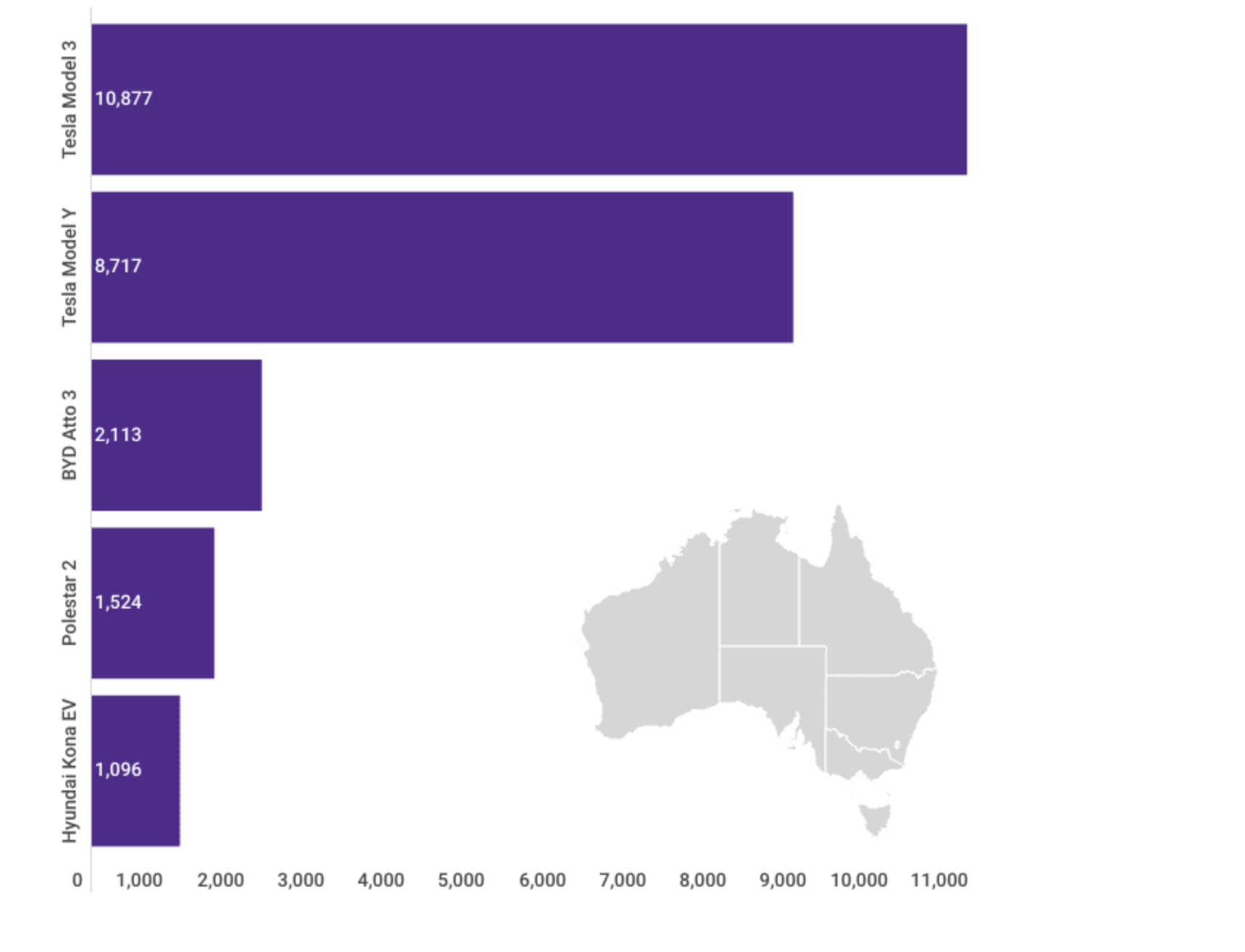

In the fast growing Australian market, we saw a microcosm of the world EV market as Tesla and BYD fight it out. Old legacy auto such as Ford and GM are nowhere to be seen. The graph below illustrates this:

{kind=link}

The World Market - Europe

It is the same picture in Europe, as shown by a recent tweet from Tesla in Europe:

{kind=link}

It is odd to read comments about demand for Tesla products failing, yet Tesla being the EV leader in market after market. European countries are leading the transformation from internal combustion vehicles ("ICE") to EV and in virtually every country, the market leader is Tesla.

The World Market - USA

The company recently cut prices of the Model 3 and Model Y by about 20%. This was partly to enable buyers to get into the tax credit price range. Prices were also reduced for the Model S and Model X. Falling costs were another driving factor.

According to figures from the automobile New Data Center, Tesla sold 491,000 cars in the USA last year. This made it by far the top-selling luxury brand in the country. BMW (BMWYY) is in second place at probably about 330,000 cars, with Mercedes (MBGAF) in third place at about 286,000 cars.

When final figures are in, it is expected Tesla sales will have increased over 40% in 2022. That makes the "falling demand" narrative for Tesla a bit puzzling. These increases in sales were despite the economy moving into recession and interest rates rising sharply

Tesla auto sales will continue to boom in the USA. New legacy auto competitors such as the Ford "Lightning" and GM "Silverado" will have serious problems making sales targets, and even more serious problems hitting profitability targets. The absence of BYD in the U.S. market will be a significant bonus for Tesla.

Supply

The Tesla rapid ramping up of more production also gives the lie to the lack of demand thesis. The Shanghai factory continues to expand. The company is known to be in discussions for their next Gigafactory in Asia. Indonesia is possible, as detailed here. South Korea and Thailand are possible locations, too.

In the USA, substantial expansion plans are ongoing for the Austin factory. In January, approval was given for a $716 million expansion there, which will include a cell plant and a cathode plant. This will most likely be for their own #4680 cells for the Model Y for the North American market. The Cybertruck should be coming onstream in Texas in mid-year. There have also been various reports about the next Gigafactory in the Americas.

This certainly does not suggest Tesla is seeing any fall in demand for their products.

Energy Storage

My article in July last year laid out the details of the huge potential. This is now transforming into numbers. The many skeptics who misunderstand the potential of this may now start to comprehend the reality of energy storage and power generation.

Energy storage has been hit harder than the auto section by the lack of supply. This seems it will be largely resolved in 2023 by the huge supply now online. As my article detailed, this will provide an additional minimum of $6 billion in orders this year.

The key issue is that previously Tesla was unable to support all the energy storage demand it encountered as it prioritized its battery capacity for auto demand. Now, with their new dedicated Lathrop factory finally under way, they have the capability of producing 10,000 commercial "Megapack" units per annum. This is already sold out until late 2024 as their web-site shows. The current sales price is about $1.53 million, and that would give an annual value of Megapack sales per annum about $16 billion. That excludes revenue streams from the smaller commercial product "Powerpack" and the residential "Powerwall" for which supply still cannot get near to demand. Last year, the company sold about 250,000 Powerwalls at about $12,000 each. There is currently an over one year waiting-list and the product is not even being marketed in most countries. We can now expect to see revenues explode as supply from Lathrop comes onstream.

Energy storage projects keep rolling in and the applications are extremely varied. For example, Megapack units have just been deployed to Australia's largest electric bus recharging station. They are becoming an integral part of the unstoppable movement away from a fossil fuel economy.

The projects just keep piling up for Tesla. My previous article detailed just some of these. The latest one to start construction is the Western Downs Battery in Queensland. This will be the largest such system in the country and is being developed by French company, Neoen, with whom Tesla is the default partner. This project will be 200 MW/400 MWh. Neoen currently has 6GW under construction or in operation and expects to have 10 GW by 2025. Australia will undoubtedly continue to be a very big market for Tesla's energy storage business and Neoen a price partner.

At the same time as Tesla was starting work on the largest such project in Australia, it was making final supplies to the largest such project in Europe. It is supplying 78 Megapacks (worth about $120 million) to the BESS at Pillwood in the UK. This is pictured below:

{kind=link}

In Belgium, they have just commissioned the 50 MW/100 MWh Deux-Acren project. That was using 40 Megapack batteries (worth about $60 million).

The energy storage business was slow to get going in Europe. It is now set to accelerate rapidly. Tesla's revenues will accelerate rapidly with it. The "Repower EU" concession scheme has come into force from the EU. Russia becoming a rogue state has made the EU finally recognize the dangers of relying on fossil fuel supply.

The previously troubled solar roof business seems to be ramping up and can be viewed as part of the general energy storage picture. The company recently completed its 500,000th solar panel and solar roof installation. This represents a not insubstantial 4GW of clean energy. This solar roof sector does, however, still face some problems.

Those critics who say the energy storage business will represent low margin one-off sales do not understand the business. The Megapacks are sold at high profit margins. Then there is the high margin software Tesla incorporate in their products. Then there is profitable ongoing service revenue. Each Megapack sold gets over $9,000 per annum service revenue over a 15 year contract period. So you can add $135,000 in recurring revenue to the Megapack $1.53 million sales price. The contract price for users to connect to the Tesla "Powerhub" monitoring and control software platform is not known, but is even more profitable. It has been estimated to be at least $10,000 per annum. Overall Megapack margins are seen to be running at about 45%

Tesla's stated aim is to deploy 1500 GWh per annum of energy storage by 2030. That would represent about the market share they had last year. In 2021 they did 3.9 GWh, worth about $3 billion. So $3 billion x 375 would equal over $1,000 billion. That would require an additional 37 new Lathrop plants.

Optimistic targets do not, of course, usually coincide exactly with reality, but the potential is immense. It explains why Tesla's target to get 50% of revenues from energy storage is very attainable.

Conclusion

Tesla is a good example of how markets tend not to price companies rationally. The price rose to crazily high levels in the first place, and have now fallen far below what the picture should be. One can discount some uncertainties such as FSD, "robotaxis," insurance, or "Optimus." They may or may not happen, but they are not needed for a healthy outlook.

The demand picture for autos is strong. Now they will have the supply they need. Margins may fall by about 20% in 2023 but deliveries should be up over 50%. Even after the latest price cuts, Tesla vehicles are still lower-priced than they were at the start of 2021. They will continue to have high margins.

The ramping up of production through current and future investments will produce a large increase in sales revenue over coming years. The potential of energy storage is enormous and misunderstood by analysts.

These all show a company in good health, and at the forefront of secular changes in society. Along with BYD, no other company is better placed to exploit these changes than Tesla, Inc.

For further details see:

Tesla Set For Continuing Sales And Revenue Growth In 2023