BYDDY - Tesla: What The Market Doesn't See (Rating Upgrade)

2024-01-16 09:20:00 ET

Summary

- Tesla stock has remained stagnant over the past six months and has recently experienced a 7% decline.

- The company is facing negative news, including mixed reviews of its Cybertruck, vehicle recalls, and a loss of market share in China.

- However, the market is not recognizing the long-term potential of Tesla, particularly in its energy, full self-driving, and charging segments.

Thesis Summary

Tesla ( TSLA ) has seen its stock go nowhere in the last six months. Though there have been ups and downs, the stock is now similarly priced as it was back in August.

Over the last month, Tesla has actually lost over 7%, as the market begins to price in more negative news.

Not only is Tesla no longer the top electric vehicle ("EV") seller over the last three month period, but the company has seen mixed reviews over its newly released Cybertruck, has had to recall over 2 million vehicles, and it continues to lose market share in China.

If ever there was a time to not be bullish on this EV maker, you might think it's now.

However, my thesis is that, while the market is already pricing in the not insignificant issues the company is facing right now, it is failing to see the great long-term potential the company still possesses.

By historical standards, Tesla’s stock is arguably “cheap.” I find this strange at a time when Tesla has taken great strides in the last 10 months to set itself up for the next 10 years.

By this, I mean that Tesla has made great moves in its Energy, full self-driving ("FSD"), and charging segments. In the future, these segments will contribute much more to the company’s profits than car sales.

I dive deep into just how much Tesla could stand to make from each of these ventures over the next 7 years in order to arrive at a possible price target.

In short, this is a pullback worth buying.

A Quick Update

Despite considering myself a Tesla bull, my last two pieces on the company have had neutral ratings.

During the 2023 Q2 earnings, I gave Tesla a neutral rating after it had already run up close to 50% in the months prior. This was based mostly on Technical Analysis.

{kind=link}

More recently, I gave the company another neutral rating after Morgan Stanley ( MS ) upgraded its price target to $400.

{kind=link}

The stock had recently had another runup, and despite my long-term conviction, I argued that the bank analysts were overly optimistic in the short term, as they were neglecting to price in the risk posed by China.

Well, over the last few months, I would argue that markets have indeed begun to price in a lot of the negative.

Sentiment certainly seems to have shifted somewhat. Out of the last 10 SA articles on Tesla, three rate the company a Buy, one a Strong Buy, One a Strong Sell, three a Sell, and two a Hold. Opinions are equally divided based on this small sample, but it does seem to me like the mega-bulls are a bit less vocal.

Plenty Of Reasons To Sell

There’s no shortage of reasons to be bearish on Tesla. Let’s begin with the most recent.

Supply Constraints

Tesla has been forced to shut down production in its largest factory in Europe, the Berlin Gigafactory. This has been due to a lack of key components, which have been delayed due to the disruptions caused to shipping in the Red Sea.

It's projected that Tesla might have to pause most of the output for close to two weeks. Tesla hasn’t been the only company affected, as it seems that Volvo is in the same boat.

This is, of course, bad news for the EV manufacturer, which has already faced issues in 2024, as the Cybertruck release has perhaps not caused quite the desired response.

Cybertruck and Other Issues

Cybertruck deliveries began around November 30th , with a starting price close to $60,000.

For starters, a couple of viral videos have already made their rounds through the Internet, showing Cybertrucks getting stuck in the snow. Not an entirely uncommon thing to happen to pickups, but also not a great look for a vehicle advertised as the pinnacle of technology in this space.

Furthermore, in an unofficial test carried out by a YouTuber, it was shown that the Cybertruck’s actual range was close to 254 miles, which is around 79% of the advertised range.

In all honesty, these issues with the Cybertruck should not come as a surprise, as Elon himself has mentioned many times just how complex the production of this car has been.

…But first order approximation, there’s like 10,000 unique parts and processes in the Cybertruck. And if any one of -- it will go as fast as the least lucky, least well-executed element of the 10,000. So, it’s always difficult to predict the ramp initially, but I think we’ll be making them in high volume next year, and we will be delivering the car this year.”

Source: Elon Musk.

Still, it remains to be seen just how well the market will react to this product. Musk estimated annual sales of up to half a million , but it is still unclear just how this will contribute to the bottom line.

On top of this, Tesla was also made to recall 2 million vehicles last month, as the U.S. National Highway Traffic Safety Administration claimed that the cars were inadequately monitoring drivers using self-driving capabilities. Their report claims, amongst other things, that the Tesla cars were not aptly checking that both hands were still on the steering wheel.

Fall in Demand

All of this happened as Tesla was dethroned by BYD Company Limited (BYDDF) as the largest EV seller in the last quarter. Tesla is selling fewer cars than its competition and has been losing market share in China for quite some time.

BYD vs TSLA (IQ Fund)

Tesla is facing more intense competition than ever this year from both other EV companies as well as traditional car companies that are now selling Electric and hybrid models.

Better Reasons To Buy

But all the noise surrounding Tesla in the last few months is just that: noise. These are, at most, short-term problems that will influence share prices in the immediate future. However, I am a long-term investor with a long-term horizon.

Over the next few years, Tesla stands to become a very different beast. In fact, its current revenues, most of which come from EV sales, will likely become smaller in proportion to its other segments as these realize their potential.

And, perhaps more importantly, these new sources of revenue will offer much higher margins than auto production.

The current auto production and sales are simply laying the groundwork for what’s to come.

Energy Storage

Yes, energy storage could be on track to become a very significant addition to revenues and, perhaps more importantly, earnings.

Indeed, auto production is a low-margin business, but that probably won’t be the case with energy storage, which, even in its recent infant state, has already surpassed auto margins.

Tesla gross margin by segment (Heller House)

Fellow SA contributor Luis Stevens recently compared the Megapack business (energy storage) to Amazon (AMZN) Web Services, or AWS. It seems like an apt comparison, as it holds both the promise of high growth and adoption while also carrying much larger margins than Tesla’s “main” business.

Last month, Tesla secured a 1.6 GWh Megapack project with the Melbourne Renewable Energy Hub ((MREH)), and this is only a sign of things to come.

According to Verified Market Research, the energy storage market could grow to $32.5 billion globally by 2030, growing at a CAGR of 16.3% .

However, Tesla has a much more ambitious growth target, estimating it can provide 1,500 GWh in annual energy storage deployment, which implies close to a 90% CAGR of its business.

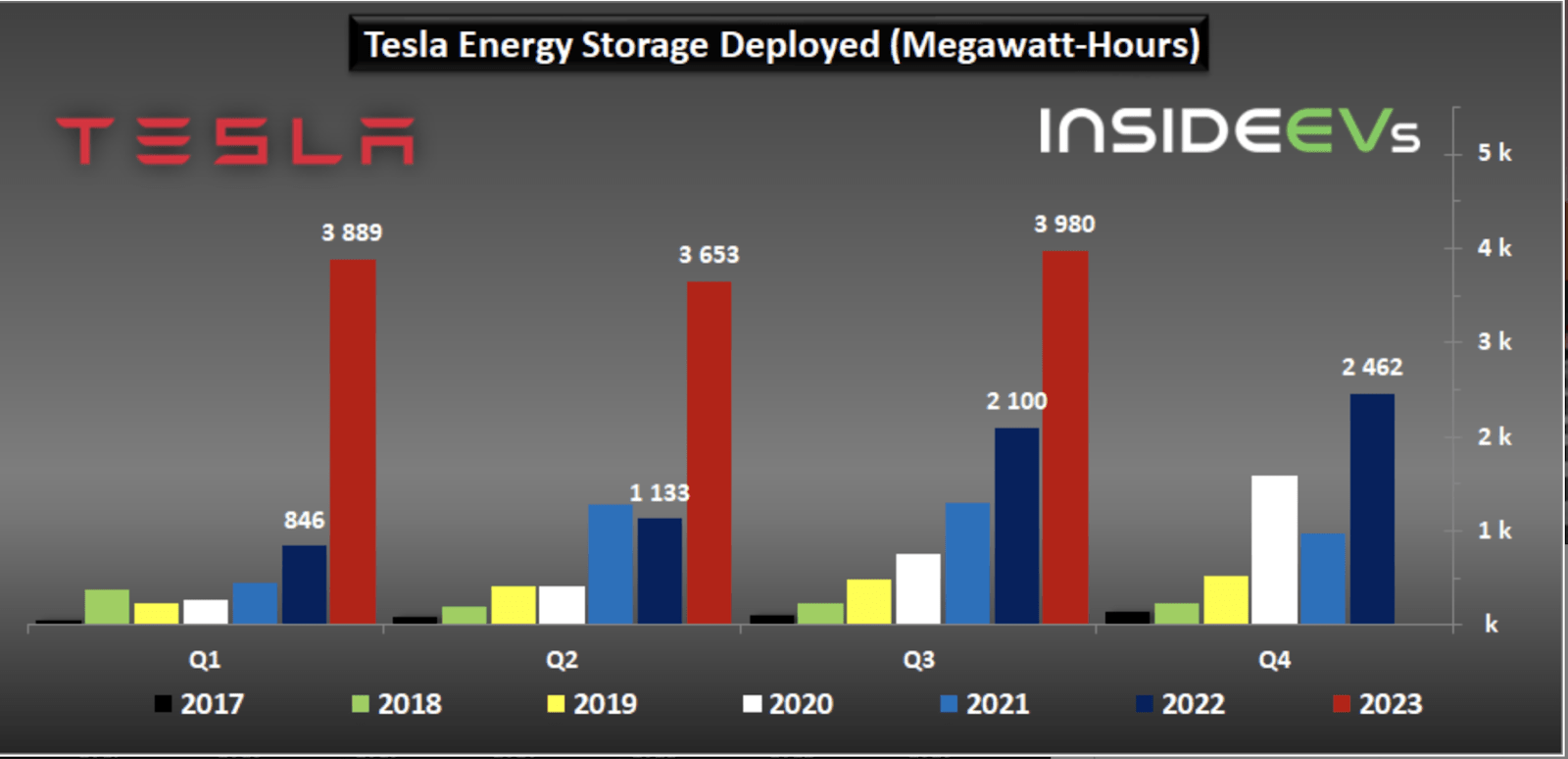

Ambitious as it may seem, the company did manage to almost double its Energy Storage deployment YoY in the last quarter.

{kind=link}

Full Self-Driving

Tesla’s full self-driving ("FSD") is not just a dream pipe, but is actually a business segment that is already arguably contributing $1-3 billion to sales. Even though this is still in beta mode, Tesla says it charges an upfront fee of $12,000 for FSD, or around $199 for a monthly subscription.

According to Goldman Sachs, FSD could contribute as much as $75 billion in revenues by 2030.

We believe that Tesla’s software-related revenue could be tens of billions of dollars per year by 2030 (mostly from FSD)," Delaney wrote. "These scenarios suggest that in an upside case FSD could account for tens of billions of revenue per year (and more if we consider licensing of Dojo or selling FSD to other OEMs).

Source: Delaney, GS .

We will reach our estimates for FSD revenues below.

Charging

Lastly, charging should also be a huge tailwind for Tesla in 2024. I wrote about supercharging a while back when Tesla first reached agreements with major car makers to lease out their superchargers.

In the last month, we have seen some significant moves in this regard. Firstly, in December, we just saw Volkswagen, Porsche and Audi adopt Tesla’s chargers. And, on top of that, the White House has also shown support to the idea of standardizing Tesla’s chargers.

Tesla’s supercharger network has always been a selling point for consumers, and now it is one for investors. This is the pick-and-shovel play of EVs. Everyone needs to charge their EV, and the company that dominates this market will do very well. Not only because it can make more revenues but also because it can do so with a higher margin.

Piecing It Together

Let’s piece it all together to estimate first how much annually the company could make by 2030 and, secondly, how much gross profit the company could generate from each of its segments.

Energy Storage Forecast

Starting with energy storage, we’ll take a middle-of-the-road approach between Tesla’s ambitious 90% growth and our market estimates.

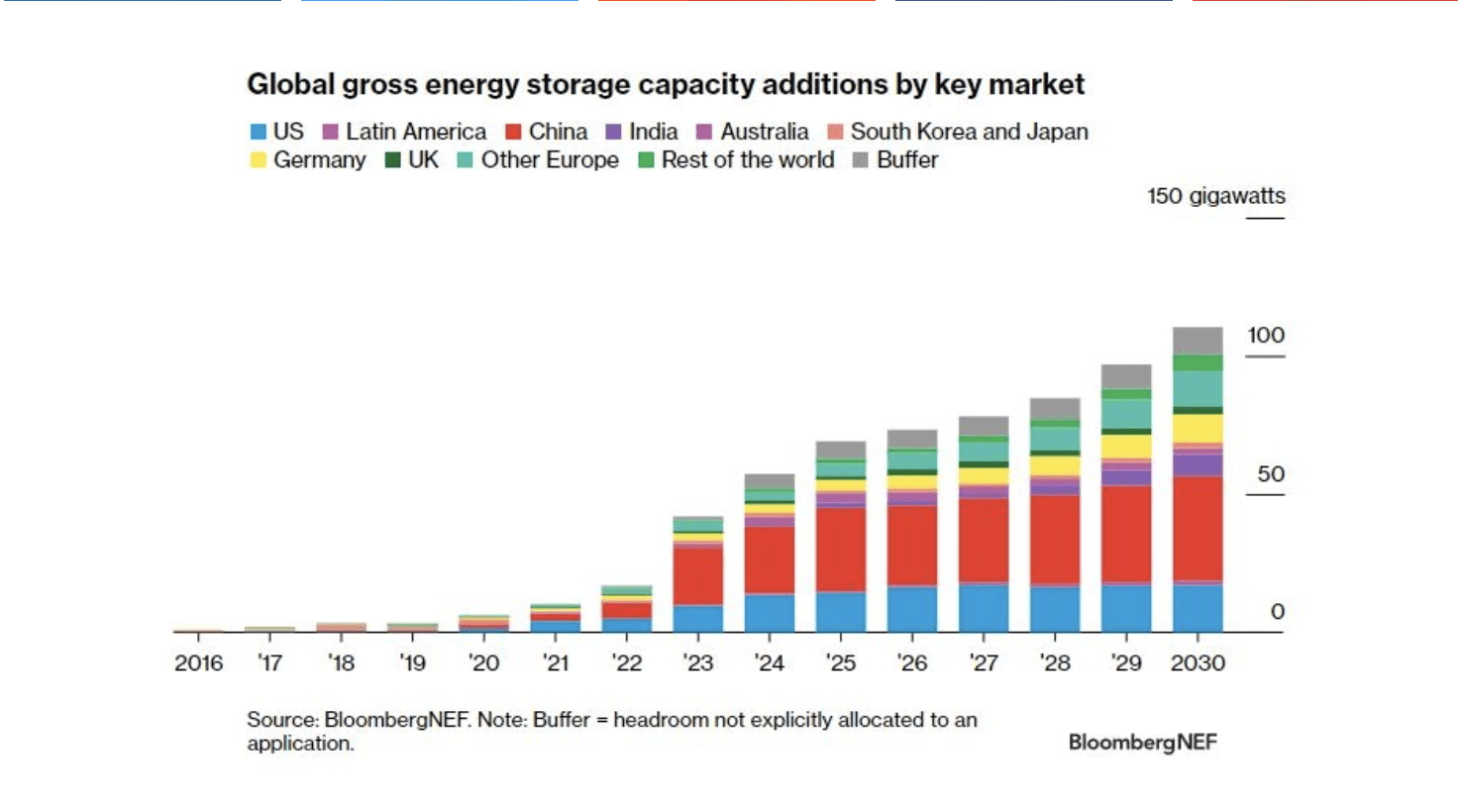

In the last 12 months, Tesla generated $6.2 billion in their Energy production and storage segment, deploying around 14 GWh. According to Elon , the company can take this to 1,500 GWh by 2030.

I find that very difficult to believe, unfortunately, and Elon has a track record of overpromising. In fact, 1,500 GWh, is 1.5 TWh, which is a little over what BloombergNEF estimates the whole world would need in terms of energy storage.

{kind=link}

Being generous, I believe Tesla may be able to become a key player and take a third of the market. Let’s also assume that these estimates are conservative and total demand reaches around 1,500 GWh.

Therefore, we can conclude that Tesla could perhaps be responsible for deploying and maintaining 500 GWh.

That’s still a 35x increase from today’s capacity. Applying this to revenues, we could expect $217 billion in revenues. Applying similar gross margins to today, around 25% according to the graph shown before, we have a gross profit of $54.24 billion in gross profits.

FSD Valuation

For full self-driving, we could take Goldman’s estimates at face value, which are up to $70 billion in revenues, or we could make our own calculations.

Again, we can take Musk's lofty targets and take them back to reality. Musk has publicly said he expects the company to reach a $20 million production level by 2030.

That’s a very ambitious target, which would imply around 40% CAGR over the next seven years. Instead, applying a more modest CAGR of 30%, we can reach a target for 2030 of 12 million.

Tesla Production Forecast (Author's work)

Now, let’s assume starting around 2025, Tesla can offer FSD on 1/4 of every new model it sells.

That would be almost 12.5 million cars using FSD. At $12,000 a piece, that’s $150 billion. Taking the low end of the software industry average gross profit margin , 75%, that implies $115 billion in gross profit.

That’s a bit higher than the GS estimate but not too far off, and I’m struggling to find how exactly they reached this calculation.

Charging

Moving on to charging, if Tesla can indeed establish itself as a standard for global EVs, then it certainly stands to make very substantial revenues.

The average car needs perhaps three charges per week, which is equivalent to around 225 Kw/h (75Kw/h per full charge.)

Multiply that by 52 weeks in a year, and that’s a yearly “charging consumption” per EV of 11,700Kw/h.

According to the IEA, there could be 350 million EVs roaming the streets by 2030.

And one last piece of important information:

Musk Tweet (X)

Musk stated that the Supercharger network aims for a 30% Gross Margin, and we know Tesla charges consumers around $0.40 per KWh.

That means if the Supercharger network could be used by 10% of the global fleet, that would be 35 million cars, charging 11,700Kw/h every year.

This, in turn, means each car generates Tesla $4,680 in revenues. $163 billion annually in revenues and $48.9 billion in gross profit of we multiply that by 35 million cars.

Car Sales

And, lastly, car sales. We have already projected 12 million production in 2030. Below are listed all the current price ranges for Tesla’s vehicles.

Tesla Prices (Solarreviews)

Based on these prices, a conservative average price would likely be around $60,000.

At 12 million units, that would be $720 billion in revenue. With an auto margin of around 20%, that’s $144 billion in gross profit.

Valuation

So, to sum up:

| 2030 Forecast |

| Revenue |

| Gross Profit |

| Energy Storage |

| $217,00 |

| $54,40 |

| FSD |

| $150,00 |

| $115,00 |

| Charging |

| $163,00 |

| $48,90 |

| Car Sales |

| $720,00 |

| $144,00 |

| Total |

| $1.250,00 |

| $362,30 |

That’s $1.2 trillion in revenues and $362 billion in gross profits.

But what does this mean in terms of valuation? The best thing we can do here is take the gross profit, and apply a Price/GP ratio.

Currently, Tesla’s Gross Profit stands at just under $19 billion . With total shares outstanding of 3.176 billion, that means gross profit per share of just below $6, and a P/GP of around 36, given today’s price of $218.

Now, if we were to apply the multiple to our 2030 forecast, then we’d have a gross profit of $114 a share, and a target price of $4100.

However, this seems very ambitious, and one would expect this ratio to be much smaller.

Since we made the Amazon/Aws comparison, maybe this could serve as an indication of how the gross profit for Tesla could compare to its price as the company matures.

Amazon has a gross profit of $225.152 billion and 10.3 billion shares outstanding. That means around $22,5 GP per share and a P/GP ratio of 6.8.

Applying a 6.8 ratio to our 2030 Tesla forecast yields a perhaps more realistic price target of $775.

Final Thoughts

While the market is looking at the negative short-term news, it is overlooking all of the great improvements to the long-term thesis that are taking place. Tesla, Inc. is killing it in energy storage, charging and FSD, and this is going to be a bigger part of the pie every year.

For further details see:

Tesla: What The Market Doesn't See (Rating Upgrade)