CA - Tetra Technologies: 2 Birds 1 Stone

Summary

- In this article, we discuss TETRA Technologies' Q3 2022 earnings report.

- We also dig into the weeds on their lithium extraction and water desalination businesses.

- We are maintaining a buy on Tetra Technologies below $4.00 and reiterating a target of $8.00 as the industry gains steam in 2023.

Introduction

Note - this article appeared in the Daily Drilling Report on November 4th.

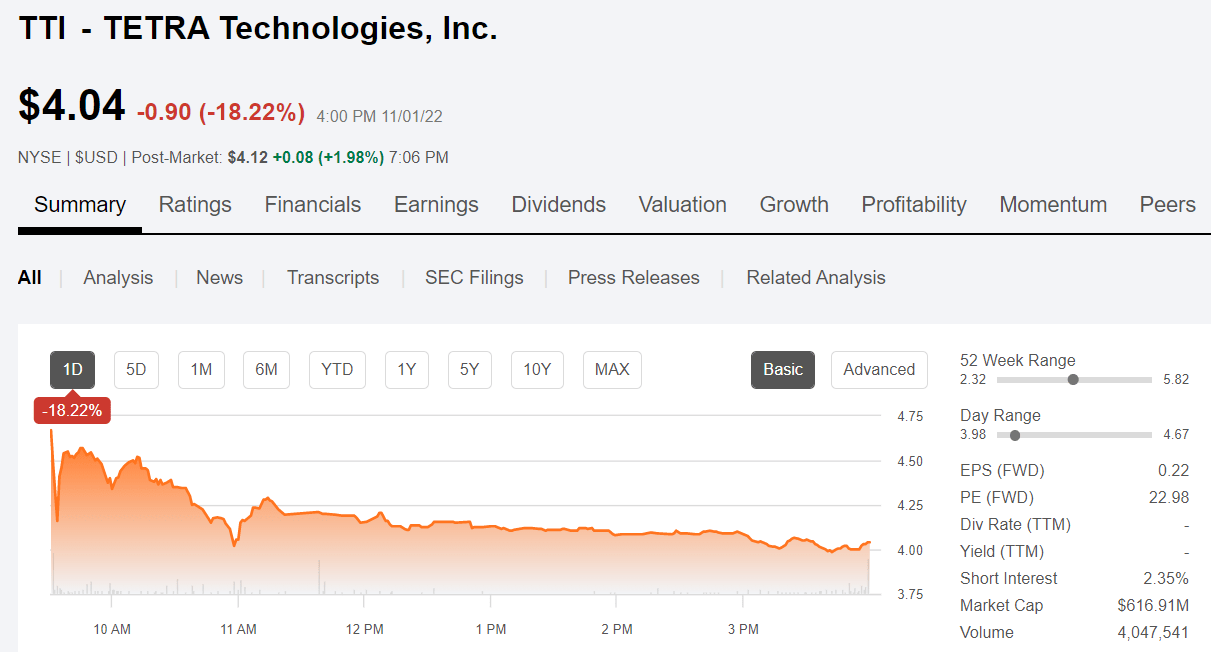

TETRA Technologies, Inc. ( TTI ) disappointed the market with its Q3 2022 earnings release . The market didn't take it kindly and took the company down a peg. A big peg, as in like 18.22% in a single day. Wow. The market is a bit of a nervous nellie, and when the conference call began, TTI stock began to sink like a stone, cracking $4.00 before rebounding a bit.

TTI price chart (Seeking Alpha)

{kind=link}

In this article, we will identify the key areas that led to the selloff and provide some context.

We will also look at the discussion around TTI's efforts to begin developing the mineral wealth highlighted in previous articles . Now as before, the bromine and lithium reserves that have now been quantified in a resource report . Bromine reserves have been quantified at 5.25 Mtons. Lithium reserves have been detailed at 234 Ktons.

Here as in the past, I will tell you that the reason to buy TTI is for the promise of the rich potential of these mineral reserves. I think of this as the "Manhattan Project " for the company. It is essential to the inflection in growth that I foresee for the TTI. As with the historical wartime project, this endeavor involves developing cutting-edge technology that will have a profound impact on one of the most critical problems the oilfield faces - dealing with produced water. This technology will help to recycle oilfield brines and at the same time extract needed mineral resources for the burgeoning EV battery markets. Two birds, get it?

The oilfield and chemical businesses are strong, despite having some ups and downs, and justifies my earlier share price projection of $8-9.00 per share. The mineral business, should it develop , and I have to stress this is still at a nascent stage but has the potential of contributing materially to TTI's revenues a few years down the road. Perhaps far beyond what the oilfield and chemicals businesses will ever do.

A brief word on the lithium potential

Sociedad Quimica y Minera de Chile ( SQM ) is one of the largest miners of lithium globally. Let's go back in time and look at a one-year chart on this company. In Q-2 of 2021, SQM reported $212 mm of EBITDA. In Q-2, of 2022 they reported $1,318 in EBITDA. 6X+ in 4 Quarters!

Price chart on SQM (Seeking Alpha)

{kind=link}

What happened obviously is that the price of lithium carbonate went nuts. (Do follow the link here.)

The slide (not shown but linked) below illustrates the opportunity toward which TTI is planning. In the middle 20s, demand begins to outstrip supply. The adoption of Battery Electric Vehicles-BEVs, containing batteries which weigh ~1,200# and contain ~140# of Li2CO3 will drive demand for Li. About of global car production is expected to be BEVs in 2030, or ~40 mm unit s, demanding ~2,800 Mtons of Li2CO3. Spongey numbers but they suggest a gap between supply and demand of ~400 Ktons annually, that will sustain long-term pricing at high levels. (Do follow the link here.)

Elijio Serrano, CFO of TTI commented in regard to the urgency with which the company was pursuing the development of these reserves in the company call yesterday:

We are very focused and have a high sense of urgency to bring both the bromine and the lithium assets to market as a demand and the returns are already there by others that are already producing such key minerals. To demonstrate how those in the lithium business are benefiting from the high lithium prices and strong market demand, let me give you an example of such returns SQM, publicly traded global lithium producer increase their lithium EBITDA from $41 million in the second quarter of last year to $1.2 billion in the second quarter of this year. A 30 times year-over-year increasing quarterly lithium EBITDA as a result of the high market prices.

The urgency is appropriate, as beginning in the late twenties, there is a gap between demand and supply. He who hesitates is lost. The early bird gets the worm. Duck on a June bug.... you get the idea.

A word about Direct Lithium Extraction - DLE

The process for extracting the lithium from the field brine from the Smackover formation in Southern Arkansas. There is a lot of infrastructure already in place for bromine - a mineral that's been extracted for decades, but lithium is special and some exotic processes are having to be proved out to remove it. None of these are new technology except as it is being applied to lithium. In fact, there is a governmental project aimed toward expanding and proving out this technology in lithium applications. A broad shot of the technologies being trialed is discussed in the linked NREL document :

DLE technologies can be broadly grouped into three main categories: adsorption using porous materials that enable lithium bonding, ion exchange, and solvent extraction. Scaling up any of these techniques to full production capability remains a challenging task.

Brady Murphy, CEO of TTI discusses this at a fairly high level:

As also noted in our third resource report, our research team has demonstrated successful pilot unit results for a direct lithium extraction process that we will continue to validate in the coming months. This will provide -- this will involve proving out each step in the process from the lithium-rich brine production from the wells of our Smackover leases through the DLE and purification process to a high purity lithium chloride solution. We continue to believe that we are in a unique position with a US resource rich in two key minerals, bromine and lithium for the energy storage markets in the ability to produce both minerals for much of the same brine production wells and pipeline infrastructure.

I have some confidence in the Tetra team in this regard. This is a brine chemistry problem as much as anything, and TTI is good at chemistry. There is also a similar project run by Standard Lithium ( SLI ) as a JV with Lanxess ( LNXSF ) in their Eldorado, Arkansas location. TTI has leased some acreage to SLI for the production of lithium and receives payments in SLI stock, the price of which varies according to its own market dynamics. TTI retains the rights to any bromine produced. Earlier this year TTI monetized its SLI holdings for a gain of several million dollars.

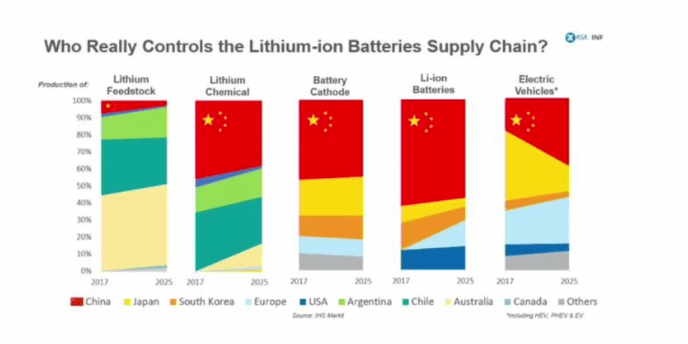

The government has recently declared lithium to be a critical mineral . So critical it was an essential element of the IRA infrastructure bill. You can see from the Dallas Fed Energy Conference slide below exactly what is driving this concern. The U.S. over the last 30 years has outsourced much of its critical supply chain and related processing infrastructure to China. We will avoid commenting on just how short-sighted that was, and note that it went on largely unnoticed until the Pandemic. You don't see a lot of blue-USA, in the slide below. The increasingly strident rhetoric between the U.S. and China since has propelled the gaps shown in this slide to the top of mind position with many our policymakers, as they restructure the economy toward electricity.

Dallas Fed Graph on minerals supply (Dallas Fed)

{kind=link}

The takeaway is that we are extremely exposed supply-chain-wise to being able to fulfill the ambitious goals that policymakers are setting forth in that regard. This means that TTI is acting with all due haste to meet an opportunity that has not only government sanction but the wind in its sails.

Elijio Serrano comments on their engagement with the DOE to secure IRA resources to assist financially in the exploitation of their bromine and lithium reserves:

The $1 trillion bipartisan infrastructure bill and the over 400 billion Inflation Reduction Act that was passed earlier this year contains several grants and loan programs that we believe are very applicable to what we'll be doing to bring critical minerals of lithium and bromine in this Smackover Formation to market and to build and expand manufacturing capacity to support battery storage.

We are very engaged and are having dialogue with the Department of Energy and will be and have been applying for government grants and loans to support our upcoming investments. We will report the progress of this initiative in the future as key milestones are achieved.

The crossover between DLE and produced water management

Desalinization through Reverse Osmosis is a proven technique for freshening water. In my last article, I discussed how Tetra was employing its proprietary SandStorm cyclones to remove solid particulates from water streams. This is something different. With this technology, TTI is using membrane filtration to begin the process of stripping and concentrating the elemental lithium in the field brine. Desalinated water is a by-product of this process.

Brady Murphy, CEO of TTI was quoted in the press release, describing the opportunity set for water reclamation:

According to Rystad Energy Research, the U.S. will produce close to 23 billion barrels of water from producing oil and gas wells in 2022 with nearly 13 billion barrels being disposed of in saltwater disposal wells (SWDs). Our strategic relationships with KMX and Hyrec will allow us to create new, sustainable markets for produced water, reduce the industry's reliance on disposal and preserve precious fresh water resources.

This crossover between managing produced water and extracting elemental lithium gives TTI a broad opportunity set that extends to producing water for agricultural and industrial uses. This opens the door to multiple streams of income that do not now exist but are just over the horizon.

One problem with desalination is the energy cost associated with it. TTI's new partners have taken innovative approaches to the reverse osmotic process that lowers the energy inputs while operating at high efficiencies.

Q3 2022

TTI experienced some cost inflation due to having to buy bromide off contract to build inventory for upcoming Q-4 work. This is a necessary evil you might say. No one keeps inventory for call-off without a contract to which it is tied. TTI noted this was a one-off expense. Supply chain issues also hit the EU chemicals business.

Water and Flowback services, revenue of 76 million, improved 29 million or 62% year-on-year and 9.9 million or 15% quarter-on-quarter. Adjusted EBITDA of 13.2 million improved by 8 million or 158% year-on-year and 3.2 million or 33% quarter-on-quarter. Completion Fluids & Products' third-quarter 2022 revenue of $59 million increased year-on-year by 22% and decreased from the second quarter of 2022 by 21% as the prior quarter benefited from the seasonal uplift for the European industrial chemicals business. Adjusted EBITDA of $14.7 million, which included a $0.2 million unrealized gain from investments, decreased $3.0 million sequentially. Completion Fluids & Products Adjusted EBITDA margins were 24.9% in the third quarter compared to 23.7% in the second quarter of 2022.

Adjusted EBITDA for the third quarter was $18.6 million in comparison to 18.7 million in the second quarter but was up 24% from $15 million in the third quarter of last year. The third quarter included $2.7 million of non-recurring charges and expenses. This compares to $4.7 million in the prior quarter. Cash from operating activities was $2.1 million. Capital expenditures net of cash proceeds from the sale of assets was $12 million, compared to $10.3 million in the second quarter.

Free cash flow or cash from operating activities was negative $9.8 million in the third quarter. Working capital consumed $8.6 million in the third quarter compared to $4 million of cash generated in the second quarter. This was required to build inventory for some significant deepwater international projects coming up in the fourth quarter.

Total debt outstanding with $154 million at the end of September, while net debt was $129 million. At the end of the quarter, their net leverage ratio was 1.7 times and improvement from 1.8 times at the end of the second quarter. Liquidity at the end of the third quarter was $92 million.

Notable gains in the third quarter and guidance

In Argentina an award for an additional early production facility, which is on track to commence operations in the first half of 2023. Tetra is successfully expanding its footprint into Latin America with these Early Production Facilities, EPS which include high-margin rentals of SandStorm cyclones.

GoM service base was buttressed by a multiyear contract renewal for one of the most active deepwater super majors in the Gulf of Mexico that was executed in the third quarter. The Kimberlite report indicated that TETRA holds the second-highest market share in completion fluids in the Gulf of Mexico at 30%. Within the report, Kimberlite mentions, TETRA technologies continues to be the top-performing supplier in the Gulf of Mexico and receives the highest customer loyalty ratings as measured by the Net Promoter Score.

They are currently executing a smaller TETRA CS Neptune completion fluid job in the UK and have another job confirmed, expected to be delivered in the first quarter of 2023. UK jobs do not have the impact of GoM jobs as the volumes are smaller due to shallower water. No GoM jobs were discussed, but as the Lower Tertiary rock of the deepwater GoM is probed they are likely to develop. It only takes one.

Their customer for zinc bromide Pureflow, Eos announced recently they will be shifting some of their planned Q4 deliveries into 2023 to allow their customers to take advantage of a significant tax credits under the Inflation Reduction Act. This will impact TTI's planned Q4 delivers to Eos. They expect each of these issues to become one-time events for the fourth quarter.

Your takeaway

The fluids business is always capital intensive, requiring significant investment ahead of deliveries. As I noted before, these are good problems to have. Both the Completion brines and water management businesses are showing quarter-over-quarter gains in the top and bottom lines. As I noted in the past article the current share price is not reflective of the true valuation of the company's prospects going forward. I fully expect that when the market adjusts after the Powell implosion, and oil prices stabilize or move higher, TTI will resume its march higher.

I don't view the company as a straightforward oil and gas play, as I have taken some pains to note. There is real, intrinsic value in the bromine and lithium minerals on their Arkansas leases, with development projects underway. Their water strategy rings true and as discussed is a viable and growing business. The synergy between the two will provide further uplift from efficiency increases and lower costs. Two birds, one stone!

I'll close this out with my price calculation from the prior report, as I think it is still realistic.

Tetra has a robust and growing oilfield service business that is delivering positive cash flow. It has a number of projects in the pipeline for its Neptune product, including one pending in the GoM that could ramp revenues by $10-$15 mm by itself alone. With traditional brines the Completion Fluid side of the business has been generating about $65 mm per year. Add a Neptune job into that and we can arrive at $80-85 mm per year. With the growth projected in Deepwater projects there should be more Neptune jobs. Over 10 years that's $850 mm. Add in a couple of hundred mm for the water business and back out corporate costs of ~$150 mm, and then add in the debt at $153 mm and you get an EV of $1,053 bn/128 mm and you get a share price in the $8's for TTI.

That is before any mineral revenue comes along. TTI has seen the mid-$3s as recently as late September. Thanks to the current renewed China-Lockdown panic, TTI is back in the upper $3s. I view TETRA Technologies, Inc. as being in a buy zone in the sub-$4.00 range.

For further details see:

Tetra Technologies: 2 Birds, 1 Stone