CA - TFI International: The Road Ahead Looks Bright For This Logistics Leader

2023-12-20 07:41:50 ET

Summary

- TFI International Inc. presents an enticing investment opportunity in the logistics industry, boasting a strong North American presence.

- Despite recent revenue dips attributable to market conditions and divestitures, the company is experiencing improving operating ratios across its segments.

- At a forward multiple of 9.44x EV/EBITDA, TFI shares look attractive, trading at a discount to its historical multiple and peer group.

All $ amounts in , not , unless otherwise specified

Investment Thesis

TFI International Inc. ( TFII:CA ) is exactly the kind of company I like to own. Profitable with steady growth and at an attractive valuation. A leader in logistics services, TFI International stands out a compelling investment due to its robust operating model and growth opportunities ahead. Despite a recent revenue decline coming off a very strong period last year, TFI's focus on efficiency improvement, evidenced by improving operating ratios across segments, signifies a commitment to profitability. The company's acquisition-driven strategy, backed by a history of prudent acquisitions and a solid cash position, positions it well for future growth. With a reasonable valuation and a discount to its historical multiple and logistics peers, TFI looks like an attractive stock to consider.

Business Overview

TFI International is a transportation and logistics company that provides a wide range of trucking and logistics services across North America. Serving over 80 cities in both Canada and the US, TFI's network offers services like less-than-truckload ((LTL)), truckload (TL), parcel delivery, courier services, logistics, and freight management. Essentially, these services include moving goods or packages from one location to another, whether it's a small parcel, partial truckloads, or full truckloads, and the services involved in managing and coordinating these movements efficiently. By geography , about two-thirds of revenue comes from the US with the remaining third coming from Canada. No single client accounts for more than 5% of revenue.

Since 2008, TFI International has done over 125 acquisitions on both sides of the border. The company's acquisition strategy has been a direct result of the strong free cash flow it generates as it focuses on targets that are immediately accretive earnings per share and free cash flow, fit in nicely with existing segments, and themselves generate high free cash flow.

Recent Developments

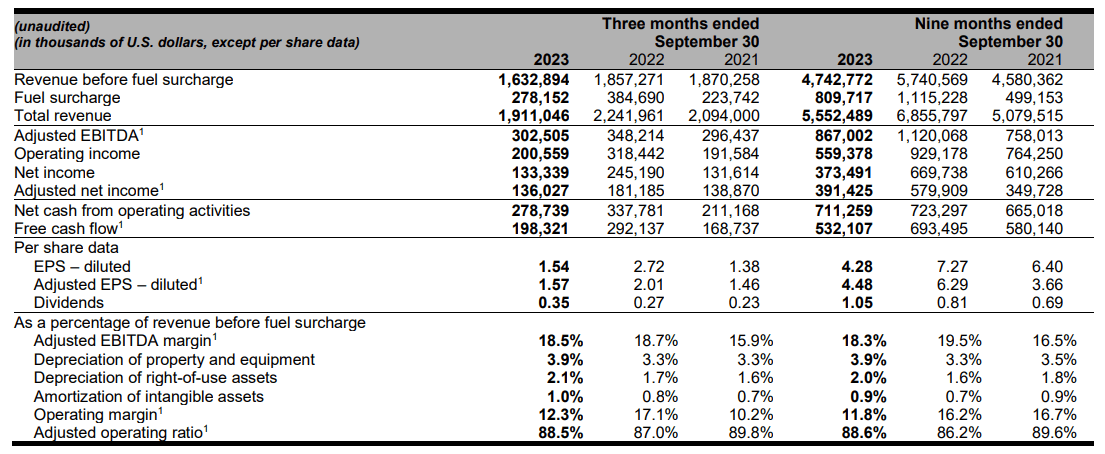

When looking at the most recent quarter for TFI International, the company had revenues of $1.91 billion for the three-month period ending, which was down from the $2.24 billion from the same period last year. We can also see this reflected in earnings too, with adjusted EPS came in at $1.54, down from $2.01. A lot of the weakness we are seeing is really due to two main factors, namely softer market conditions and the sale of CFI's Truckload, Temp Control and Mexican Logistics Businesses to Heartland Express last year in August for $525 million. CFI was generating about $450 million of revenue and approximately $50 million in 2021 for TFI so a decent chunk can be attributed to the sale.

{kind=link}

On the earnings call , management also reaffirmed full year guidance for 2023 with adjusted EPS in the range of $6.00 to $6.50 and free cash flow in the range of $ 700 million to $800 million. It's previous guidance of $200 million to $225 million in net capex has already been exceeded this year with over $500 million spent on acquisitions and share repurchases given the company's strong balance sheet and free cash flow.

On the EPS guidance, given that we already 3 out of 4 quarters into the year, this would imply EPS of 1.52 to $2.02 (-12% to +17%). This is obviously a pretty big range, so I think it reflects the reluctance of management to change their guidance given the uncertainty that may be on the horizon. However, management also noted that from what little they've seen quarter-to-date, the numbers look encouraging, so it's likely they will finish the year closer to the top of the guidance range.

While revenue across all segments was down, I think it's helpful to dive into each one to provide some color to the broader picture:

- P&C: revenues declined 7% (number of packages also down 7%), but overall the segment is performing well given weaker demand and with less contribution from fuel surcharge.

-

LTL: revenues declined 12% on a 4% decline on shipments, but operating income came in at $100 million which was virtually flat year-over-year. This really speaks to margins (particularly in the Canadian segment where operating ratio was 77.2% compared to 72.8% the prior year).

- Truckload: revenues declined 21% on weaker demand and the sale of CFI but operating ratio improved from 81.1% last year to 87.5%.

The basic takeaway in my opinion is that while revenues came down, operating ratios largely improved, which bodes well for the overall profitability of the company. In many ways, the overall demand environment is outside the company's control, but certainly an improvement on margins and operating ratios can buffer the impact of the decline. One key standout note was the company's LTL segment. The US LTL segment is at 90% operating ratios and we're starting to see the Canadian LTL segment improve as well hovering just over 77%. Management expects that with a bit of volume pick up and a marginal improvement on pricing, it should be able to sustain its operating ratios. With an intense focus on operating ratios and the company's return on invested capital both as an enterprise and throughout their individual segments, I believe the company should be able to sustain margins and see a meaningful increase in free cash flow once demand returns.

While the company didn't explicitly express their thoughts on how the demand environment may improve, I would bet that they view it positively adding another four tuck-in acquisitions this quarter (bringing the full total to 11 year to date) and raising the quarterly dividend by 14%.

When asked about the potential for M&A and more buybacks, CEO Alain Bedard had this to say:

Well, you know, buyback, we really love buyback. So I'll give you an example. We just renewed our NCIB, Scott. All right. And we have an order to buy 1 million shares depending on the price. So this is, you know, this is the focus depending on the price, we're there, we've renewed our NCIB, and we're going to be, you know now. If there's a major transaction, okay, and I think that if you look at history, normally you have something of size in '24. We did a lot of nice tuck-ins in '24. We're probably very close to being done for, I mean, '23. We're probably close to being done in '23. We got this $500 million placement just to get ready to be in a position, okay, in a better position. Our leverage is 1.39 right now. We should be closer to 1.2 at the end of the year. So we have a lot of dry powder on our line of credit with our bankers. Now we have cash. We got $300 million to $400 million of cash at the end of the year. Okay. So we're well positioned to do something of size in '24. Now, it's always the same story with TFI. There's always one -- not just one file that we're working on. There are always more than one. So I think that the possibility of doing something of size in '24, I would put that at 65%, 75%.

What this says to me is that the company is really readying up for another big acquisition. Since 2014, the company has completed 89 acquisitions , 5 of which were major acquisitions, indicating that these types of acquisitions really only take place every couple years for TFI.

While the demand environment might not be the hottest we've seen, when we consider the company's recent $500 million private placement bringing their average interest rate to 4.5%, TFI has a very low cost of debt to make an acquisition happen. Right now, with leverage coming down to the lowest levels the company has had in the last five years, I believe it's only inevitable the company makes a big acquisition. And clearly, as evinced by the CEO's comments and 4 small tuck-ins this quarter, there is no shortage of opportunities right now.

Valuation

Historically, TFI has traded at a forward multiple within the range of 5.2x to 12.1x EV/EBITDA. At a forward multiple of 9.44x EV/EBITDA, TFI looks to be trading a little higher than its historical average. When we consider that TFI has been able to grow revenues and EPS at 16.5% and 14.9% over the last 20 years, 9.44x forward EV/EBITDA seems like a reasonable multiple. Going forward, I don't expect that kind of growth but it was growing at around 7.3% in the first five years pre-pandemic, so that should give a good indication of what growth good look like going forward in the next few years.

Based on the 16 analysts with one-year target prices on TFI International, the average price target is $187.27, with a high estimate of $222.98 and a low estimate of $122.42. From the average, this implies about 19.5% upside from the current price, indicating that analysts are currently bullish on the stock.

Compared to comps like XPO, Inc (XPO), J.B. Hunt Transport Services Inc. (JBHT), C.H. Robinson Worldwide, Inc. (CHRW), and Old Dominion Freight Line, Inc. (ODFL), at 11.9x, 11.6x, 16.5x, and 20.4x, TFI International looks attractive at 9.44x.

When it comes to valuation, there are a few risks I'd want to highlight. As mentioned, with the company seeing a weaker demand environment, any worsening of demand for the trucking and logistics industry could certainly bring down revenues. This could take the form of lower consumer spending, resulting in few deliveries and lower demand for trucking and logistics services.

On the costs side, labor costs and fuel prices would be things to watch for. TFI does have a union labor force for which they just paid a 5% increase this quarter after reaching a tentative 5-year contract with the union. Any sort of disputes or disagreements between TFI and the union would be factors to monitor but with a tentative contract so far agreed upon, that risk is mitigated for now.

With fuel prices, you might be inclined to think that higher fuel costs would hurt a company like TFI (as fuel costs are often a key input costs in logistics). However, TFI like many other trucking and logistics companies, charges its customers a fuel surcharge, meaning it earns revenues that help to offset part of the fuel cost. So in softer markets like the one we are seeing right now (as compared to last year, TFI earns less money on fuel charge. On the topic of fuel charges, CEO Alain Bedard had this to say:

When fuel is expensive, we make a little bit of money on fuel. When fuel is not expensive like it is now, that profit is gone, right. So that is a little bit of a headwind for our Canadian LTL in our package. When fuel is low, I mean, we don't make -- we don't have a little bit of profit from fuel. When fuel is high, we do well on fuel because of our density which is very different than our US LTL operation because we never make money on fuel in the US LTL world like today.

Overall, I'd say the risks to TFI are fairly low, given the low valuation relative to its historical multiple and its peers, and the fuel surcharge and labor being relatively minor points of focus for investors going forward.

Takeaway

In summary, despite a revenue drop from last year, TFI International looks attractive due to its improving ratios and should be in a position to growth steadily in the future. With a record of strong acquisitions over its history, the company has been prudent in its capital allocation strategy. At a forward multiple of 9.44x EV/EBITDA, I feel comfortable recommending the company as a buy, given the discount to peers and historical valuation.

For further details see:

TFI International: The Road Ahead Looks Bright For This Logistics Leader